- Non-food Packaging

- Corrugated and Folding Carton Packaging Market

Corrugated and Folding Carton Packaging Market Size, Share, and Growth Forecast, 2026 - 2033

Corrugated and Folding Carton Packaging Market by Product Type (Folding Cartons, Corrugated Boxes, Others), Structure (Single-Wall, Double-Wall, Others), End-use Industry, and Regional Analysis for 2026 - 2033

Corrugated and Folding Carton Packaging Market Size and Trends Analysis

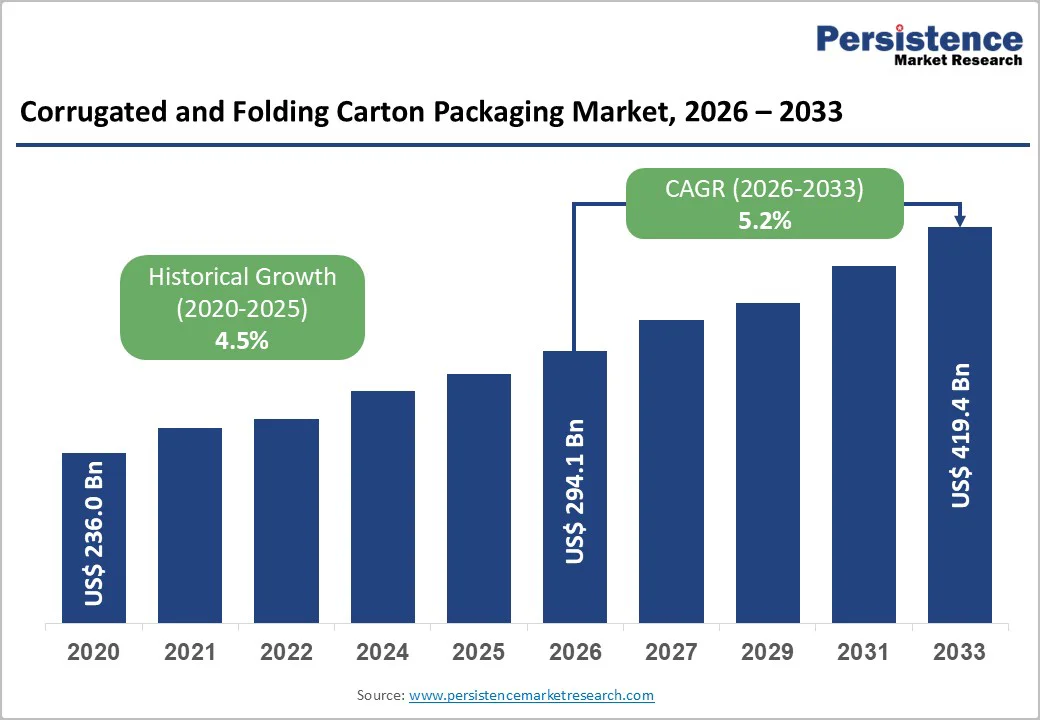

The global corrugated and folding carton packaging market size is likely to be valued at US$294.1 billion in 2026 and is expected to reach US$419.4 billion by 2033, growing at a CAGR of 5.2% between 2026 and 2033, driven by plastic reduction policies and retailer sustainability mandates.

Demand remains resilient across food and beverages, e-commerce, pharmaceuticals, and consumer goods, with converters investing in high-speed converting lines and digital finishing technologies.

Key Industry Highlights

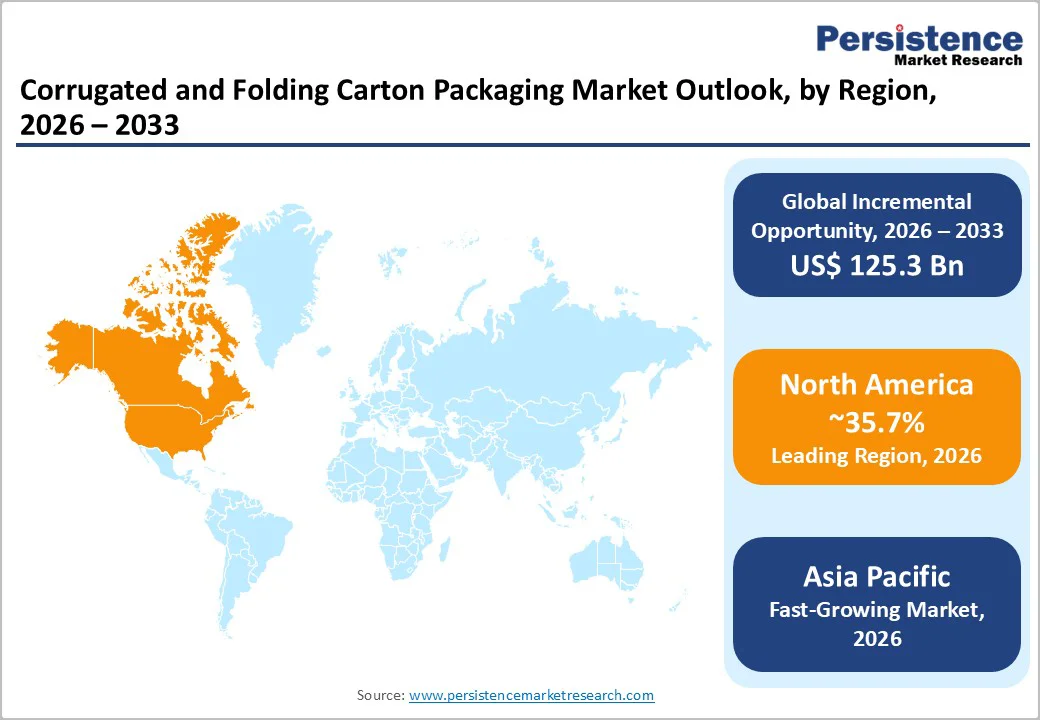

- Leading Region: North America, to contribute 35.7% of the global revenue in 2026, due to mature e-commerce networks, advanced converting infrastructure, and strong demand for corrugated and folding carton formats.

- Fastest-growing Region: Asia Pacific, projected to post the highest growth through 2033, supported by rapid industrialization, strong e-commerce expansion, and rising consumption of packaged FMCG and food products.

- Investment Plans: Strong capital deployment across regions, including high-speed digital printing lines, robotic palletizers, corrugator expansions, and greenfield converting plants. North American and European producers continue upgrading automation systems, while Asia Pacific investments focus on expanding containerboard capacity and localized converting operations.

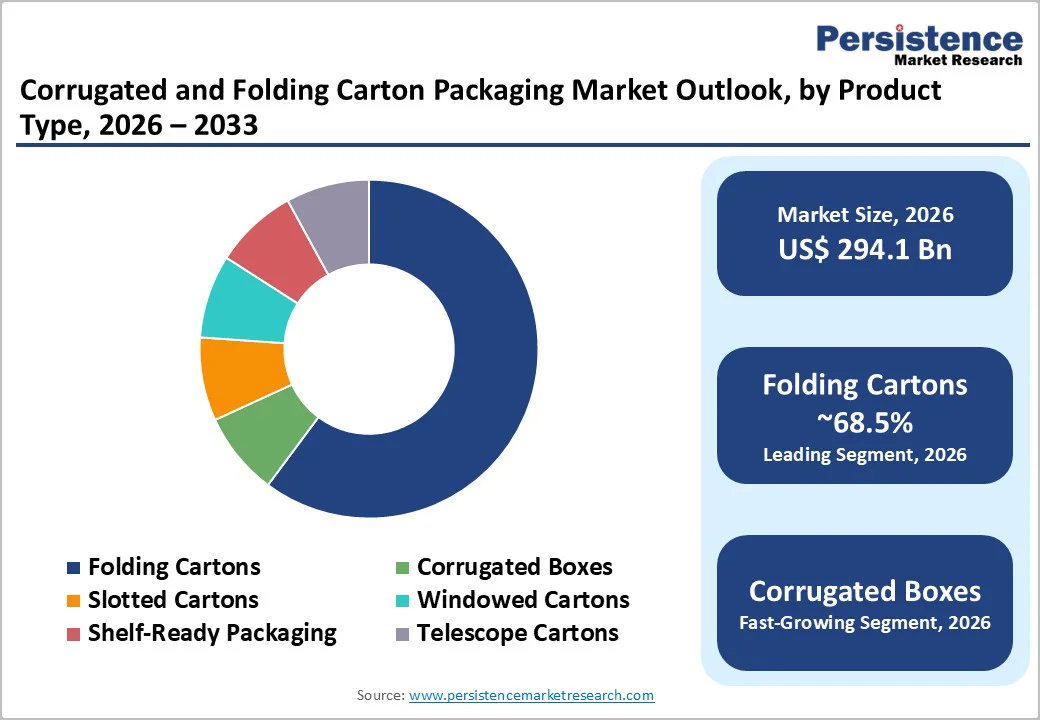

- Dominant Product Type: Folding cartons, estimated to hold over 68.5% of the global market share, driven by high usage across food, beverage, pharmaceutical, cosmetics, and premium consumer goods applications.

- Leading Structure: Single-wall corrugated structures, anticipated to capture 44.8% of the structure segment, due to their optimal strength-to-weight ratio and compatibility with automated distribution and omnichannel retail packaging.

| Key Insights | Details |

|---|---|

| Corrugated and Folding Carton Packaging Market Size (2026E) | US$294.1 Bn |

| Market Value Forecast (2033F) | US$419.4 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.2% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.5% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Sustainability and Regulation are Accelerating Fiber Substitution

Ongoing policy actions aimed at reducing single-use plastics across North America, Europe, and parts of Asia Pacific have driven widespread substitution toward recyclable corrugated boxes and folding cartons. Retailers and major consumer brands now include fiber-recyclability criteria in procurement, leading to measurable increases in demand for paper-based secondary and tertiary packaging.

Multiple national packaging waste guidelines encourage the use of renewable materials, and companies report rising interest in high-recycled-content board grades. This shift supports higher volumes and, in many cases, higher price realization through value-added coatings, premium graphics, or sustainability labeling. Over the 2026 - 2033 period, this regulatory tailwind is expected to remain a major contributor to both folding carton and corrugated box growth.

E-Commerce Logistics and Last-Mile Efficiency

The continued shift toward online retailing has intensified demand for corrugated shipping formats that balance durability, dimensional efficiency, and protective functionality. Corrugated boxes dominate parcel shipping due to their strength-to-weight ratio and ability to support automated filling, sorting, and right-sizing solutions.

Growing parcel volumes have increased order frequency for customized box sizes, tamper-evident structures, and box inserts engineered to reduce damage. These conditions have accelerated the adoption of digital printing, on-demand die cutting, and warehouse automation.

Corrugated packaging, therefore, remains a primary growth engine, with converters reporting increased volumes tied to subscription commerce, rapid replenishment systems, and enhanced fulfillment infrastructure.

Premiumization and Marketing Use of Folding Cartons

Folding cartons continue to expand their role in sectors where brand differentiation, print quality, and sustainability messaging are critical. Premium food, cosmetics, and pharmaceutical products frequently require multi-panel artwork, specialty varnishes, metallic accents, or complex structural designs that folding cartons can support at scale.

Market evidence indicates strong mid-single-digit growth in premium folding carton applications, driven by SKU proliferation and consumer preference for attractive, recyclable retail packaging. As brands pursue shelf impact, folding carton converters benefit from higher-value finishing technologies such as embossing, debossing, soft-touch coatings, and recyclable barrier layers. These capabilities justify capital investments and contribute to margin stability.

Barrier Analysis - Input Cost Volatility and Pulp/Paper Cycle Pressures

The market faces persistent exposure to fluctuations in pulp, recovered fiber, and kraft paper prices. Significant cost spikes compress margins for converters and may lead to pricing actions that affect downstream demand.

Sudden increases in raw material costs can alter procurement decisions, prompting shifts to lighter grammages or alternative board grades. Such volatility can trigger single-year cost swings that materially affect converter profitability. In severe cycles, converters may delay capital expenditures or negotiate revised supply terms to manage cost pressure.

Logistics and Capacity Mismatches

Periodic imbalances in mill output, converting availability, or freight capacity can create supply bottlenecks. Surges in transport costs, container shortages, or localized downtime at mills may extend order lead times and force temporary use of suboptimal packaging formats.

These mismatches can result in increased emergency freight expenses, retooling costs, or delayed product launches for customers. Businesses relying on just-in-time inventory systems are particularly vulnerable, and the need for multi-sourcing and localized capacity becomes more pronounced in volatile market years.

Opportunity Analysis - Digital Printing and Personalization at Scale

The rapid advancement of digital printing systems enables shorter production runs, variable data printing, and personalized packaging for both corrugated and folding carton applications. Brands increasingly require package-level differentiation for regional promotions, limited editions, or seasonal campaigns.

Converters adopting digital finishing solutions benefit from reduced minimum order quantities, faster response times, and improved inventory optimization. Revenue per order typically increases when personalization or variable artwork is incorporated, making this a strong commercial opportunity. Digital capabilities also align with emerging e-commerce trends requiring on-demand, small-batch packaging.

Emerging Markets and Near-Shoring in APAC

Consumption growth in China, India, and ASEAN markets is reshaping global demand for foldable and corrugated formats. Rising incomes, increased packaged food penetration, and expanding domestic e-commerce infrastructure create significant incremental volume potential.

Manufacturers continue to relocate or expand operations in Asia Pacific to reduce freight exposure and improve supply chain resilience. Establishing local converting plants or partnering with regional suppliers enables faster delivery times and greater responsiveness to market-specific SKUs. This region is forecast to deliver the highest share of new global demand through 2033.

Category-wise Analysis

Product Type Insights

Folding cartons are anticipated to dominate the global packaging market, accounting for an estimated 68.5% of total market share, driven by broad adoption across food and beverages, pharmaceuticals, personal care, and premium consumer goods.

Their leadership is supported by strong aesthetic and functional advantages, including high-quality print reproduction, custom dielines, and value-added finishes such as embossing, foil stamping, and spot UV coatings that enhance shelf visibility and brand differentiation.

Folding cartons align with tightening sustainability regulations in Europe, North America, and parts of Asia due to their recyclability and high fiber recovery rates. They also offer operational advantages, shipping flat to save space and integrating easily with automated packaging lines.

Major FMCG players such as Nestlé and Unilever widely use them across food, personal care, and OTC products. In pharmaceuticals and cosmetics, folding cartons support compliance, traceability, tamper evidence, and premium shelf appeal.

Corrugated boxes are likely to be the fastest-growing product category, supported by the rapid expansion of e-commerce logistics, subscription-based deliveries, and industrial shipping. Growth is driven by their superior cushioning performance and adaptability to right-sized packaging formats. Corrugated manufacturers employ a range of flute profiles to achieve specific compression strength, edge-crush resistance, and impact protection.

E-commerce leaders such as Amazon and Flipkart rely heavily on customized corrugated mailers featuring tear strips, perforations, and integrated locking mechanisms to enhance customer experience and reduce packaging waste. Fragile goods benefit from engineered inserts and molded-paper cushioning solutions.

Continued investments in digital printing, automation, and modular gluing lines enable faster turnaround for SKU-intensive industries. In parallel, reusable corrugated formats are gaining momentum as retailers expand reverse-logistics systems and circular packaging initiatives, reinforcing long-term growth prospects.

Structure Insights

Single-wall corrugated structures are anticipated to be the most preferred option globally, anticipated to capture 44.8% of the market. They offer an optimal balance of rigidity, lightweight construction, and cost efficiency, serving diverse sectors such as consumer goods, apparel, small electronics, and general retail shipments.

Brands choose single-wall boards as they are available in diverse flute profiles, enabling tailored stacking strength while keeping paper usage to a minimum. This quality helps meet sustainability targets and supports retailer efforts to reduce packaging fees linked to volumetric inefficiencies.

Automated distribution centers use single-wall packaging extensively due to its compatibility with case erectors, robotic pick-and-place equipment, and automatic sealing systems. For example, fashion brands shipping T-shirts, accessories, or footwear through omnichannel models often rely on single-wall cartons for fast movement with low damage risk.

Food delivery meal kits also use coated single-wall structures for moisture resistance and controlled thermal performance.

Double-wall corrugated structures are likely to be the fastest CAGR and are projected to secure a substantial market value by 2036. Their rise is linked to the growing movement of heavy goods, fragile electronics, and industrial components that require superior protection.

Manufacturers in segments such as home appliances, power tools, HVAC units, and automotive parts rely on double-wall designs due to their improved edge crush strength, puncture resistance, and performance over long-distance shipping. Exporters in manufacturing hubs such as China, Vietnam, and Mexico increasingly specify double-wall solutions for cross-border shipments to ensure reliability through varied climatic and handling conditions.

For instance, double-wall corrugated boxes with reinforced corners are commonly used for transporting microwave ovens, compact washing machines, LED monitors, or precision-machined components.

Converters equipped with in-house ISTA testing labs and board optimization software offer tailored engineering assessments that help customers reduce excessive packaging while meeting protection benchmarks. This technical capability is helping accelerate adoption in industrial packaging and global supply chains.

Regional Insights

North America Corrugated and Folding Carton Packaging Market Trends - E-Commerce Scale & Recyclable Fiber Innovation

North America is anticipated to be the largest regional market, holding 35.7% of the global revenue in 2026. Its strength stems from a mature retail ecosystem, high packaged food consumption, and deeply integrated e-commerce networks that depend on corrugated packaging.

Demand for high-graphic folding cartons in consumer goods and pharmaceuticals continues to rise, and converters are developing recycled-fiber boxboards and recyclable insulated corrugated coolers to replace foam-based solutions. These innovations reinforce sustainability goals highlighted across major U.S. food and beverage categories.

The U.S. represents the bulk of regional consumption. A notable development is UFP Packaging’s 2025 opening of a 165,000-square-foot corrugated facility in Indiana, designed for e-commerce and custom high-graphic outputs. Canada contributes through sustainable fiber production, supporting mills and converters across the region, while Mexico’s expanding manufacturing base strengthens near-shoring flows and drives demand for durable transport packaging.

Growth is supported by three drivers: rising e-commerce shipping volumes, brand-owner commitments to recyclable packaging, and increased cross-border manufacturing that requires consistent corrugated supply. Emerging state-level Extended Producer Responsibility policies in the U.S. are pushing companies toward higher recycled content and improved recyclability.

Converters across North America continue investing in digital presses, robotic palletizing, and advanced inspection systems. Consolidation among major fiber-based packaging companies is improving supply stability and enhancing regional mill efficiency. These developments position North America to maintain its leadership through 2033.

Europe Corrugated and Folding Carton Packaging Market Trends - Regulatory Leadership & Advanced Fiber Converting

Europe remains one of the most advanced regions for fiber-based packaging, supported by strong consumer goods demand and some of the world’s strictest sustainability regulations. Germany, the U.K., France, and Spain dominate consumption, with Germany leading industrial and export packaging, while the U.K. drives e-commerce formats such as right-sized boxes and shelf-ready designs.

France’s luxury sector continues to boost premium folding carton demand. Recent consolidation underscores market evolution. In 2024, a major pan-European packaging producer acquired Western European assets of a regional rival, strengthening capacity for lightweight corrugated and high-quality folding cartons used in food, personal care, and retail packaging.

This merger enables greater responsiveness to short-run digital printing and sustainability-driven packaging redesigns.

Three key factors shape regional growth: strict EU packaging directives mandating recyclability and recycled content, retailer procurement standards focused on circularity metrics, and rapid advancements in recyclable barrier coatings that allow cartons to replace plastics in select food categories.

Converters across Europe are investing in lightweighting, digital print capacity, and fiber-based barrier technologies, while mill-converter partnerships improve feedstock security and coordinated innovation. With strong regulatory momentum and consumer expectations, Europe continues to lead globally in sustainable packaging development.

Asia Pacific Corrugated and Folding Carton Packaging Market Trends - Industrial Expansion & High-Velocity Packaging Growth

Asia Pacific is likely to be the fastest-growing regional market, driven by rapid industrialization, rising consumer incomes, and expanding packaged goods consumption. China leads in corrugated output, supported by a vast manufacturing base and highly developed e-commerce logistics.

India is seeing accelerated demand for folding cartons and corrugated transit packaging in food, pharmaceuticals, and FMCG, while Japan and South Korea contribute advanced folding carton and digital print technologies.

ASEAN markets such as Vietnam, Indonesia, and Thailand continue to emerge as export and logistics hubs. Recent developments reflect this momentum. In India, multiple packaging manufacturers have announced new corrugated facilities equipped with automation and advanced converting to meet domestic and export requirements.

Private equity investments into leading Indian pharmaceutical packaging companies are enhancing local capabilities and improving supply chain resilience.

Growth is driven by rising e-commerce penetration, premiumization in packaged goods, and increased localization of packaging production to reduce import dependence. While sustainability policies vary, tighter restrictions on single-use plastics are accelerating the shift toward fiber-based packaging.

Significant investments in containerboard mills, converting plants, and digital printing in China and India support customization and speed. Consequently, Asia Pacific will remain the primary growth engine for corrugated and folding cartons through 2033.

Competitive Landscape

The global corrugated and folding carton packaging market is moderately concentrated, with a small group of large integrated producers holding substantial market influence due to their containerboard capacity, converting footprint, and multi-region customer networks.

These companies secure large supply contracts with multinational brands and benefit from vertical integration that supports cost efficiencies. Regional and mid-sized converters continue to play an important role by offering localized service, short lead times, and advanced finishing options. Market consolidation in recent years has intensified capital requirements and increased competitive pressure across both high-volume and specialty packaging segments.

Leading companies pursue strategies centered on vertical integration, digital transformation, and sustainability-aligned innovation. They emphasize cost leadership through optimized mill-to-converter networks and differentiate through technical packaging solutions, advanced printing, and rapid fulfillment. Smaller converters compete on customization, flexibility, and short-run capabilities.

Key Industry Developments

- In May 2025, James Cropper Paper & Packaging introduced Rydal Eco White at PCD Milan, a new, brighter recycled fiber material aimed at high-end corrugated and folding carton applications in luxury cosmetics and retail packaging.

- In April 2025, DS Smith launched the GoChill Cooler, a 100% recyclable and reusable corrugated cooler designed to replace expanded polystyrene and plastic coolers in food and cold chain logistics, reducing packaging waste and carbon footprint.

Companies Covered in Corrugated and Folding Carton Packaging Market

- International Paper

- Smurfit Kappa

- WestRock

- DS Smith

- Mondi Group

- Stora Enso

- Graphic Packaging International

- Amcor plc

- Georgia-Pacific LLC

- Huhtamaki Oyj

- Nine Dragons Paper Holdings

- Oji Holdings

- Packaging Corporation of America

- Pratt Industries

- Rengo Co., Ltd.

- Mayr-Melnhof Karton AG

- AR Packaging Group AB

- Seaboard Folding Box Company

- U.S. Corrugated, Inc.

- Alliabox

Frequently Asked Questions

The global market size is estimated at US$294.1 billion in 2026.

By 2033, the corrugated and folding carton packaging market value is projected to reach US$419.4 billion.

Key trends include rising adoption of recyclable and fiber-based sustainable packaging and strong growth in e-commerce, increasing demand for durable corrugated solutions.

The single-wall corrugated structures segment leads the market due to its extensive use in e-commerce shipping, industrial transport, and retail-ready formats.

The corrugated and folding carton packaging market is projected to grow at a CAGR of 5.2% between 2026 and 2033.

Major companies include WestRock Company, International Paper, Smurfit Kappa Group, Mondi Group, and DS Smith.