- Smart Packaging

- Korea Heavy-duty Corrugated Packaging Market

Korea Heavy-duty Corrugated Packaging Market Size, Share, and Growth Forecast, 2026 - 2033

Korea Heavy-duty Corrugated Packaging Market by Board Type (Double Wall, Triple Wall, Others), Product Type (Pallet Boxes, Telescopic Boxes, Others), Capacity, End-use Industry, and Zone Analysis for 2026 - 2033

Korea Heavy-duty Corrugated Packaging Market Size and Trends Analysis

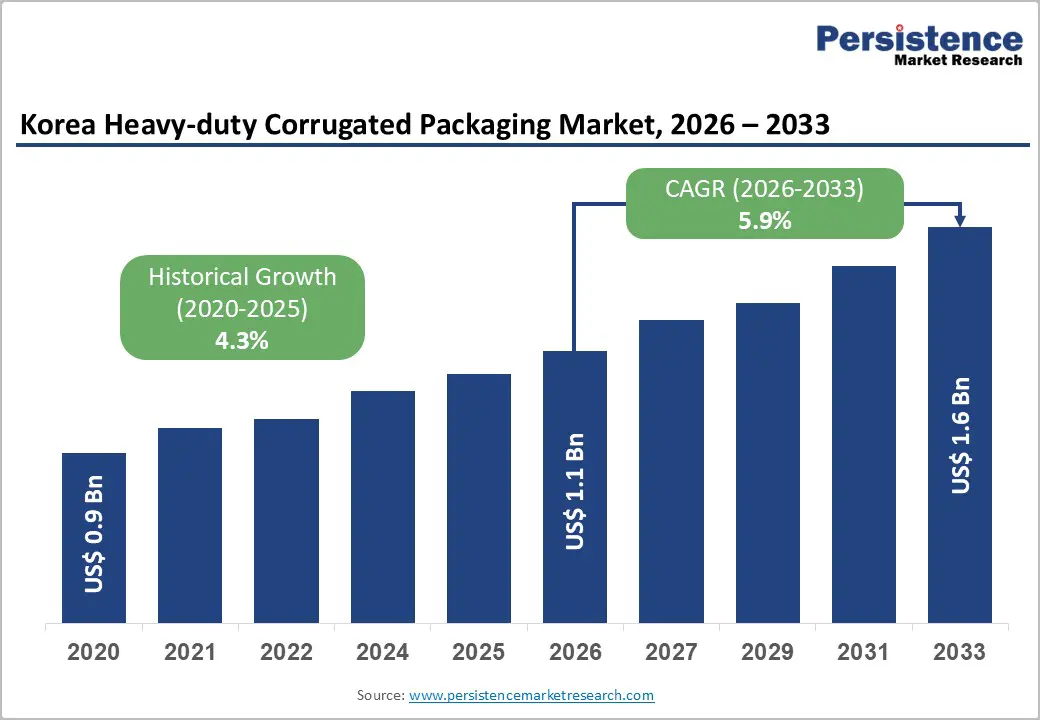

The Korea heavy-duty corrugated packaging market size is likely to be valued at US$1.1 billion in 2026 and is expected to reach US$1.6 billion by 2033, growing at a CAGR of 5.9% during the forecast period from 2026 to 2033, driven by rapid growth in export-oriented manufacturing, the Korea heavy-duty corrugated packaging market plays a critical role in supporting industrial logistics and bulk transportation needs.

The Korean heavy-duty corrugated packaging market serves key industries, including automotive, electronics, machinery, chemicals, and shipbuilding, in which high strength and product protection are critical. Growing shipments of high-value and heavy goods are driving demand for customized, multi-wall corrugated packaging for long-distance transport. Sustainability regulations and ESG goals are accelerating the shift to recyclable, fiber-based materials. At the same time, advances in corrugation design, strength, and moisture resistance continue to improve performance and cost-effectiveness across Korea’s industrial supply chains.

Key Industry Highlights:

- Investment Plans: Expansion of triple-wall corrugated board capacity and telescopic box production lines to meet rising demand for heavy machinery, chemical, and automotive export shipments; companies targeting integration of digital printing and RFID-enabled tracking in industrial cartons.

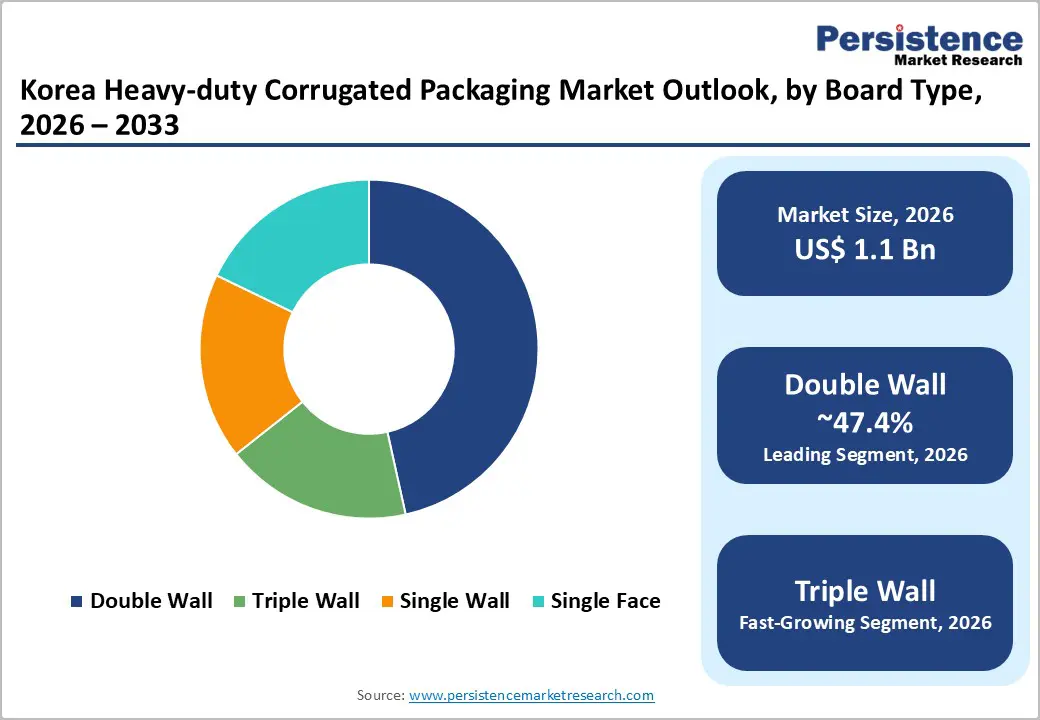

- Dominant Board Type: Double Wall is expected to hold a 47.4% share and is widely adopted for export-oriented and heavy component packaging due to its strength, cost efficiency, and logistics compatibility.

- Leading Product Type: Pallet Boxes is estimated to account for 33.8% share, preferred for bulk shipment handling, containerized exports, and warehouse efficiency across automotive and industrial segments.

| Key Insights | Details |

|---|---|

| Korea Heavy-duty Corrugated Packaging Market Size (2026E) | US$1.1 Bn |

| Market Value Forecast (2033F) | US$1.6 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.3% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Export-Led Demand for High-Compression Industrial Corrugated Packaging

Driven by Korea’s export-intensive industrial base, demand for heavy-duty corrugated packaging is closely linked to outbound shipments of automotive components, industrial machinery, and precision electronics. These products require export-grade heavy-duty corrugated boxes, multi-wall corrugated packaging, and high-compression-strength industrial cartons capable of withstanding long transit cycles, container stacking, and exposure to humidity during sea freight. The concentration of manufacturing clusters around ports such as Busan has increased the need for customized, pallet-optimized corrugated formats that reduce damage rates and improve logistics efficiency. As export volumes rise, packaging buyers increasingly prioritize performance-engineered corrugated structures over conventional transport packaging.

Sustainability Regulations Driving Recycled Heavy-Duty Corrugated Adoption

Regulatory pressure and buyer-driven sustainability criteria are further shaping purchasing decisions in the Korean market. Strong enforcement of recyclable industrial packaging standards, combined with global OEM requirements for high-recycled-content corrugated packaging, is accelerating the adoption of fiber-based heavy-duty solutions that meet both durability and environmental benchmarks. Packaging suppliers are responding by offering reinforced boards with recycled kraft liners and water-resistant coatings that comply with export regulations. For example, Korean automotive parts exporters have shifted to heavy-duty corrugated crates with over 70% recycled fiber content to meet European OEM sustainability audits while maintaining load protection for cross-border shipments.

Barrier Analysis - Reliance on Imported Linerboard and Limited Advanced Design Capabilities

Structural dependence on imported containerboard and specialty kraft liners continues to influence supply consistency for heavy-duty corrugated packaging producers in Korea. Limited domestic availability of high-performance linerboard suitable for export-grade multi-wall corrugated packaging forces converters to rely on overseas suppliers, increasing exposure to lead-time volatility and quality variation. This dependency complicates production planning for high-compression-strength corrugated boxes used in automotive and machinery exports, where even minor material inconsistencies can affect box performance during long-haul shipping and container stacking.

Limited Structural Testing and Design Capabilities among Mid-Sized Converters

Operational constraints also arise from the increasing complexity of industrial packaging customization within Korea’s manufacturing ecosystem. Demand for sector-specific heavy-duty corrugated solutions, such as vibration-resistant packaging for electronics or moisture-tolerant designs for marine logistics, requires advanced design capabilities and shorter development cycles. Many mid-sized converters lack in-house structural testing and simulation tools, limiting their ability to scale custom industrial corrugated packaging programs across multiple end-use sectors. As OEMs increasingly standardize packaging specifications across global supply chains, this capability gap restricts broader market participation.

Opportunity Analysis - Growth in Export Packaging for Moisture-Sensitive and High-Value Goods

The expansion of Korea’s export supply chains toward high-value and condition-sensitive goods is creating clear avenues for advanced heavy-duty corrugated packaging solutions. Exporters increasingly require moisture-resistant, heavy-duty corrugated boxes; reinforced multi-wall corrugated packaging for sea freight; and high-barrier industrial corrugated cartons that protect products during extended transit routes to Europe and Southeast Asia. These requirements create scope for converters to move beyond standard box formats and offer engineered designs that improve stacking strength, humidity tolerance, and cargo integrity, allowing suppliers to participate in higher-margin export packaging programs.

Value Creation through Digitally Enabled and Smart Industrial Corrugated Packaging

Technological differentiation within industrial packaging presents another growth pathway in the Korean market. Rising interest in digitally printed heavy-duty corrugated packaging, smart traceable industrial cartons, and custom-identified export packaging supports value creation across electronics, machinery, and premium consumer goods segments. Packaging integrated with QR codes, serialized markings, or logistics data enables better inventory control and damage tracking for global OEMs. For example, Korean electronics exporters are adopting digitally printed heavy-duty corrugated cartons with embedded tracking codes to improve warehouse automation and cross-border shipment visibility, strengthening long-term supplier relationships.

Category-wise Analysis

Board Type Insights

Double-wall corrugated board is expected to be the largest segment, accounting for approximately 47.4% of the market share in 2026, due to its optimal balance of strength, material efficiency, and cost. It is widely used for export-oriented industrial packaging, particularly for automotive components, electrical equipment, and mid-to-heavy machinery parts that require high compression strength without the excess weight of triple-wall structures. Korean exporters favor double-wall formats because they meet international stacking and transit durability standards while remaining compatible with automated packing lines and palletized logistics. Its versatility across sea, road, and warehouse handling makes it the default specification for many OEM supply contracts.

Triple-wall corrugated board is the fastest-growing board type, driven by the rising demand for maximum load-bearing capacity in automotive powertrain parts, industrial machinery, and chemical bulk transport. As export shipments increasingly involve heavier, consolidated loads and longer transit routes, triple-wall solutions are being adopted to replace wooden crates and metal containers. Their superior edge crush strength and puncture resistance improve cargo safety while supporting sustainability goals. For example, Korean machinery exporters shipping large industrial assemblies to Europe are shifting to triple-wall corrugated packaging to reduce packaging weight and comply with recyclability requirements without compromising structural integrity.

Product Type Insights

Pallet boxes are projected to dominate the product landscape, accounting for an estimated 33.8% market share in 2026, making them the leading product type in Korea’s heavy-duty corrugated packaging market. Their popularity is closely tied to Korea’s export-driven logistics model, where bulk handling, containerized shipping, and warehouse efficiency are critical. Pallet boxes offer high stacking strength, ease of forklift handling, and compatibility with standardized export pallets, making them ideal for automotive parts, heavy electronics, and industrial components. Their ability to consolidate multiple units into a single shipment also helps exporters optimize freight costs and reduce damage during long-distance transport.

Telescopic boxes are emerging as the fastest-growing product segment, supported by increasing demand for flexible and returnable industrial packaging solutions. These boxes allow adjustable height configurations, making them suitable for products with varying dimensions or irregular shapes, common in machinery and engineered components. Growth is further reinforced by their use in closed-loop and reverse logistics systems, particularly among Tier-1 automotive suppliers. For instance, Korean automotive component manufacturers supplying multiple assembly plants increasingly use telescopic, heavy-duty corrugated boxes that can be resized and reused, thereby improving logistics efficiency and reducing packaging waste across repeated shipment cycles.

Competitive Landscape

The Korean heavy-duty corrugated packaging market is moderately consolidated, with a mix of large domestic paper and packaging groups and specialized industrial converters competing on performance, customization, and supply reliability. Leading players benefit from integrated operations spanning containerboard production, corrugation, and logistics support, enabling tighter quality control and faster turnaround for export-oriented clients. Competition is particularly strong in automotive and electronics supply chains, where long-term contracts, consistent compression strength, and compliance with global packaging specifications determine supplier selection.

Strategic focus across the competitive landscape is shifting toward engineered packaging solutions and value-added services rather than volume-based pricing. Companies are investing in advanced box design capabilities, heavy-load testing, and customized multi-wall structures to serve high-margin applications, including machinery exports and bulk chemical transport. Partnerships with OEMs and logistics providers, along with incremental capacity expansion near major ports and industrial clusters, are strengthening market positions while raising entry barriers for smaller, non-specialized converters.

Companies Covered in Korea Heavy-duty Corrugated Packaging Market

- Korea Packaging Corporation

- Dongkuk Industrial Co., Ltd.

- Hankuk Paper Manufacturing Co., Ltd.

- LS Mtron Packaging

- Samho Paper Co., Ltd.

- Kyungdong Packaging Co., Ltd.

- Hansol Paper Co., Ltd.

- Silla Packaging Co., Ltd.

- Daehan Corrugated Co., Ltd.

- Woojung Industrial Co., Ltd.

- Jeil Paper Co., Ltd.

- Cheil Industries Packaging Division

Frequently Asked Questions

The Korea heavy-duty corrugated packaging market size in 2026 is estimated at US$1.1 billion.

By 2033, the Korea heavy-duty corrugated packaging market is projected to reach US$1.6 billion.

The Korea heavy-duty corrugated packaging market is expected to grow at a CAGR of 5.9% between 2026 and 2033.

Key trends include rising adoption of triple wall corrugated boards for heavy machinery and automotive components, increasing use of telescopic and pallet boxes for flexible bulk handling, integration of digitally printed and RFID-enabled packaging for supply chain traceability, and growing demand for sustainable, recyclable fiber-based packaging.

The leading segments are double-wall corrugated boards (47.4% share) and pallet boxes (33.8% share) due to their strength, cost-efficiency, and suitability for export-oriented industrial shipments.

Major players include Korea Packaging Corporation, Dongkuk Industrial Co., Ltd., Hankuk Paper Manufacturing Co., Ltd., LS Mtron Packaging, and Hansol Paper Co., Ltd.