- Non-food Packaging

- Corrugated Board Packaging Market

Corrugated Board Packaging Market Size, Share, and Growth Forecast, 2025 - 2032

Corrugated Board Packaging Market by Board Type (Single Face Corrugated Board, Single Wall (Double Face) Corrugated Board, Double Wall Corrugated Board, Triple Wall Corrugated Board), Flute Type (A Flute, B Flute, C Flute, E Flute, F Flute, BC Flute, EB Flute), End-use (Food & Beverages, Personal Care & Cosmetics, E-commerce, Electronics & Electricals, Healthcare, Others), and Regional Analysis for 2025 - 2032

Corrugated Board Packaging Market Size and Trends Analysis

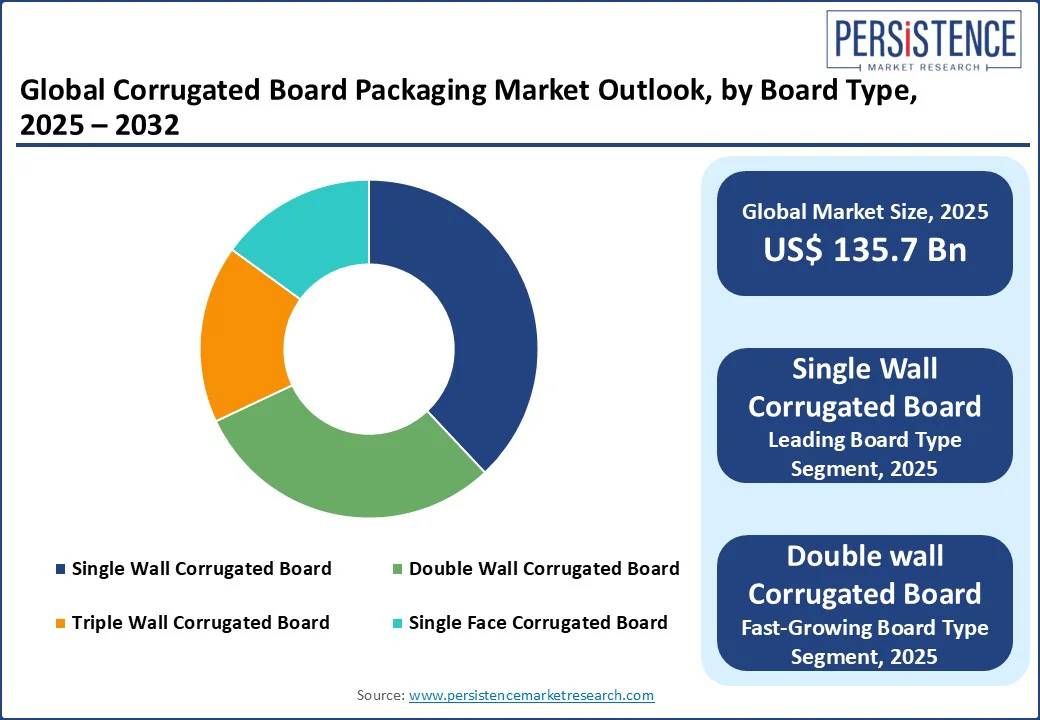

The global corrugated board packaging market size is projected to rise from US$135.7 Bn in 2025 to US$216.5 Bn by 2032, registering a CAGR of 6.9% during the forecast period from 2025 to 2032.

The corrugated board packaging market has experienced significant growth, driven by the rapid expansion of e-commerce, increasing demand for sustainable packaging solutions, and the versatility of corrugated materials across various industries. The sector is propelled by the need for cost-effective, durable, and eco-friendly packaging that meets the logistical demands of global supply chains while adhering to environmental regulations.

Key Industry Highlights:

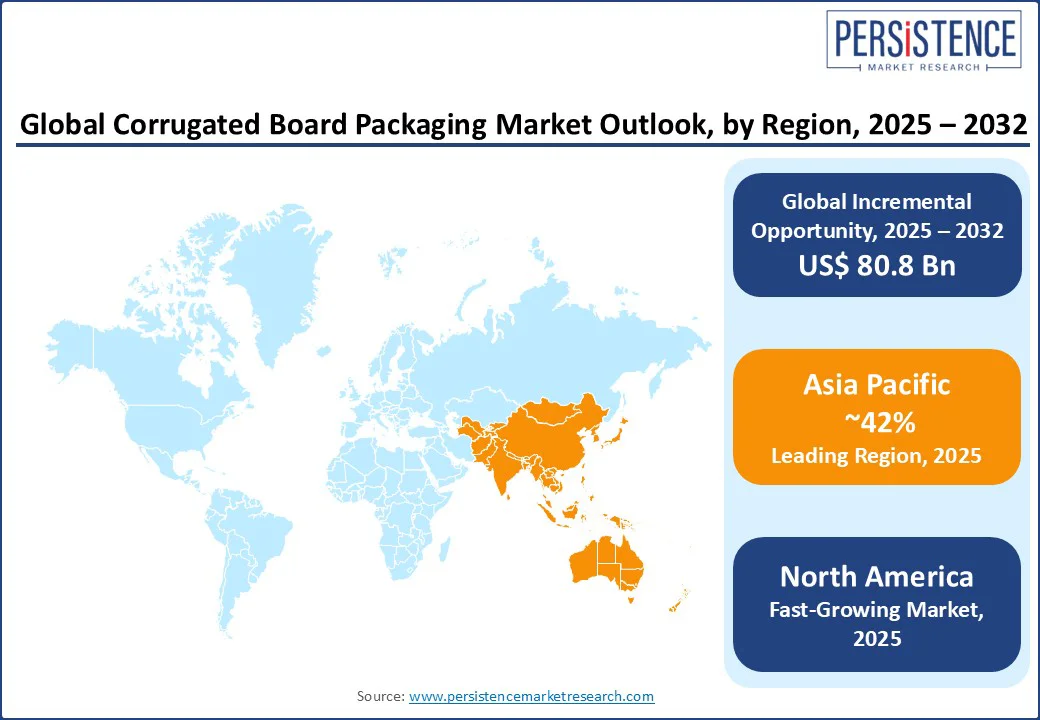

- Leading Region: Asia Pacific, holding a 42% corrugated board packaging market share in 2025, driven by advanced logistics infrastructure, a robust e-commerce sector, and rising urbanization, and the growth of middle-class populations is fueling greater consumption of packaged goods, boosting packaging demand.

- Fastest-growing Region: North America, fueled by rapid industrialization, e-commerce growth, and increased need for durable, cost-effective, and protective packaging solutions to ensure safe and efficient delivery of goods. Europe is advancing through initiatives such as the EU’s Circular Economy Action Plan, with significant funding allocated for sustainable packaging and waste reduction programs.

- Dominant Board Type: Single Wall (Double Face) Corrugated Board, commanding nearly 38% market share, reflecting its widespread use in retail and e-commerce packaging.

- Leading End-use: E-commerce, accounting for over 35% of market revenue, driven by the global boom in online shopping and logistics.

- Historical Growth: The sector registered a CAGR of 6.1% from 2019 to 2024, driven by increasing demand for sustainable and customizable packaging solutions.

|

Global Market Attribute |

Key Insights |

|

Corrugated Board Packaging Market Size (2025E) |

US$ 135.7 Bn |

|

Market Value Forecast (2032F) |

US$ 216.5 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

6.9% |

|

Historical Market Growth (CAGR 2019 to 2024) |

6.1% |

Market Dynamics

Driver- Surge in E-commerce and Logistics Demand

The exponential growth of e-commerce is a pivotal driver of the corrugated board packaging market. The rise in online shopping has significantly increased the demand for reliable and cost-effective packaging solutions to ensure safe product delivery. Corrugated board’s lightweight, durable, and customizable nature makes it ideal for shipping a wide range of products, from electronics to perishables. For instance, Amazon reportedly used over 7 billion corrugated boxes globally in 2023 to fulfill its logistics operations, underscoring the scale of demand e-commerce platforms.

Additionally, government policies promoting sustainable packaging, such as the EU’s ban on single-use plastics and India’s Extended Producer Responsibility (EPR) framework, have encouraged companies to adopt recyclable corrugated solutions. The affordability of corrugated packaging further supports its widespread adoption across both small and large businesses, making it a preferred choice in the evolving landscape of sustainable, high-volume e-commerce logistics.

Restraint- Fluctuating Raw Material Prices

Fluctuating raw material prices, particularly for kraft paper and pulp, pose a significant restraint on the corrugated board packaging market. Raw materials typically account for about 60% of total production costs, making the industry highly vulnerable to price swings.

These fluctuations are driven by several factors, including global demand for paper products, limited availability of recycled fiber, environmental regulations restricting deforestation, and supply chain disruptions due to geopolitical tensions or natural disasters. For instance, in 2023, the price of recycled kraft paper rose globally due to raw material shortages and logistical bottlenecks in Asia, significantly affecting manufacturers' profit margins.

The corrugated board industry is energy-intensive, relying heavily on electricity for processes such as pulping, drying, and corrugation. Rising energy costs, particularly in Europe and parts of Asia, have further increased operational expenses. In countries with unstable energy supplies or high tariffs, this cost burden limits scalability and affects competitiveness, especially for small and mid-sized producers.

Opportunity- Advancements in Sustainable Packaging Technologies

The growing emphasis on sustainability presents a significant opportunity for the corrugated board packaging market. Innovations in eco-friendly coatings, biodegradable adhesives, and lightweight corrugated designs enable manufacturers to meet stringent environmental regulations while maintaining product durability.

For instance, in 2024, Mondi Group introduced a water-resistant, fully recyclable corrugated packaging solution for fresh produce, reducing the reliance on plastic trays in supermarkets. This innovation aligns with the global push for circular economies, which encourages the use of recyclable and biodegradable packaging materials.

The advancements in digital printing technologies now allow high-resolution, customizable designs directly on corrugated surfaces, enhancing shelf appeal for brands in sectors such as food, beverages, and cosmetics.

For instance, Nestlé began using digitally printed corrugated packaging for seasonal promotions, improving both branding and recyclability. These developments position corrugated board as a preferred choice for sustainable and visually engaging packaging, driving market expansion across both developed and emerging economies.

Category-wise Analysis

Board Type Insights

Single Wall corrugated board dominates the industry, expected to account for approximately 38% of the industry share in 2025. Its dominance stems from its versatility, cost-effectiveness, and widespread use in retail, e-commerce, and food packaging. The single wall structure, consisting of one fluted layer sandwiched between two liners, provides sufficient strength for most standard applications while keeping production costs low. Its compatibility with various flute types, such as B and C flutes, enhances its applicability across industries.

The double wall corrugated board segment is the fastest-growing from 2025 to 2032, driven by increasing demand for heavy-duty packaging in electronics, automotive, and industrial applications.

Double-wall boards, with two fluted layers, offer superior strength and cushioning, making them ideal for protecting high-value or fragile goods during long-distance shipping. The rise of e-commerce and global trade, coupled with advancements in manufacturing that reduce production costs, is accelerating the adoption of double wall corrugated boards, particularly in emerging markets.

Flute Type Insights

C Flute holds the largest market share, accounting for approximately 25% of revenue in 2025. Its popularity is driven by its balance of strength, flexibility, and printability, making it ideal for retail packaging, e-commerce boxes, and point-of-sale displays. C Flute’s smaller flute height ensures a smooth surface for high-quality printing, which is critical for branding in consumer-facing industries such as food and beverages and cosmetics.

A Flute is the fastest-growing segment, fueled by its lightweight design and suitability for small, high-value products such as electronics and cosmetics. A Flute’s thin profile provides excellent crush resistance and printability, making it a preferred choice for premium packaging and e-commerce applications. The growing demand for compact, sustainable packaging solutions, particularly in urban markets, is driving the rapid adoption of A Flute.

End-use Insights

E-commerce leads the corrugated board packaging market, holding a 35% share in 2025. The segment’s dominance is driven by the global surge in online shopping, which requires durable, lightweight, and customizable packaging to ensure product safety during transit. Major e-commerce platforms rely heavily on corrugated packaging to meet logistical needs, with innovations such as right-sized boxes reducing material waste and shipping costs.

The healthcare segment is the fastest-growing, driven by the increasing use of corrugated packaging for medical supplies, pharmaceuticals, and diagnostic equipment. Rising global healthcare demands are fueling the need for sterile, durable, and eco-friendly packaging solutions. Regulatory requirements for safe and sustainable packaging in healthcare further accelerate the adoption of corrugated boards in this sector.

Regional Insights

North America Corrugated Board Packaging Market Trends

North America is rapidly emerging as the fastest-growing region in the global corrugated board packaging market, with the United States and Canada at the forefront of this expansion. The region’s growth is largely propelled by the explosive rise of e-commerce, which has significantly increased the need for durable, cost-effective, and protective packaging solutions to ensure safe and efficient delivery of goods. The presence of advanced logistics and distribution networks further strengthens the demand for corrugated packaging by enabling faster and more reliable shipping across vast geographies.

In addition to e-commerce, growing consumer awareness around sustainability and rising environmental concerns have led to a noticeable shift toward recyclable and eco-friendly packaging materials. Regulatory authorities in both the U.S. and Canada are implementing stricter policies to encourage the adoption of sustainable practices in the packaging sector. Corrugated board, being biodegradable and easily recyclable, is increasingly favored by both companies and consumers.

The United States, in particular, holds a dominant position within the region and is poised to sustain high growth rates due to ongoing investments in circular packaging solutions and the continued expansion of online retail infrastructure.

Europe Corrugated Board Packaging Market Trends

Europe holds a share in the global corrugated board packaging market, driven by strong sustainability initiatives, advanced manufacturing capabilities, and growing e-commerce adoption. Leading countries include Germany, the UK, and France. Germany benefits from its advanced industrial base and leadership in sustainable packaging, with companies investing heavily in recyclable corrugated solutions.

The UK’s market is bolstered by the rapid growth of e-commerce and initiatives promoting alternatives to single-use plastics. France’s market is supported by significant investments in sustainable packaging innovation. The EU’s stringent regulations, such as the Packaging and Packaging Waste Directive, drive the adoption of eco-friendly corrugated solutions, though compliance with complex environmental laws poses challenges. Europe’s corrugated board packaging market is projected to grow steadily from 2025 to 2032.

Asia Pacific Corrugated Board Packaging Market Trends

Asia-Pacific dominates the global corrugated board packaging market, accounting for over 42% of total revenue in 2022-2023. This regional leadership is primarily driven by several key factors. High industrial activity in countries such as China, India, and Japan creates consistent demand for corrugated packaging, both for domestic distribution and international exports. The rapid expansion of e-commerce across the region has further accelerated the need for durable, sustainable packaging solutions, especially for last-mile delivery.

Additionally, rising urbanization and the growth of middle-class populations are fueling greater consumption of packaged goods, boosting packaging demand. Among these countries, China leads the market, benefiting from a well-developed manufacturing ecosystem and significant export volumes that rely heavily on protective corrugated packaging. Furthermore, the country’s commitment to sustainability, supported by both government policies and corporate initiatives, has reinforced the adoption of recyclable materials, aligning with broader circular economy objectives.

Competitive Landscape

The corrugated board packaging market is characterized by strong competition, regional strengths, and a mix of global and local manufacturers. In developed regions such as North America and Europe, large firms such as International Paper and Smurfit Kappa dominate through scale, advanced technology, and established partnerships with e-commerce and logistics giants.

Meanwhile, in the Asia Pacific, rapid industrialization and growing online retail are attracting significant investments from both local and international players. Companies are focusing on sustainability, cost-efficiency, and customization to gain a competitive edge. Automation and digital printing have emerged as key differentiators, enabling mass personalization and faster turnaround times. Strategic alliances and R&D initiatives are further intensifying the competitive landscape.

Key Developments

- In September 2022, Palm Group strengthened its position in the Italian market by acquiring Orsini Imballaggi, a family-owned corrugated board manufacturing facility. This strategic acquisition enhances Palm Group’s production capabilities and footprint within Italy.

- In May 2022, Mondi committed USD 302 million toward expanding its corrugated board and cardboard manufacturing operations. The investment aims to boost capacity and improve operational efficiency across facilities in the Czech Republic, Poland, Germany, and Turkey. Notably, USD 199 million of the total investment is allocated specifically to Mondi’s Corrugated Solutions plant network in Central and Eastern Europe.

Companies Covered in Corrugated Board Packaging Market

- International Paper

- Georgia-Pacific

- WestRock Company

- Packaging Corporation of America

- Stora Enso

- Oji Holdings Corporation

- Smurfit Kappa

- Port Townsend Paper Company

- Mondi

- Others

Frequently Asked Questions

The Corrugated Board Packaging market is projected to reach US$ 135.7 Bn in 2025.

The surge in e-commerce and government-backed sustainability initiatives is our key driver.

The Corrugated Board Packaging market is poised to witness a CAGR of 6.9% from 2025 to 2032.

Advancements in sustainable packaging technologies are a key opportunity.

International Paper, Georgia-Pacific, WestRock Company, Packaging Corporation of America, and Stora Enso are key players.