- Inks, Coatings, Adhesives & Sealants (ICAS)

- Viscosifiers Market

Viscosifiers Market Size, Share, and Growth Forecast, 2026 - 2033

Viscosifiers Market by Product Type (Natural, Synthetic), Application (Oil & Gas Drilling, Construction, Paints & Coatings, Personal Care), Formulation (Formulated Viscosifiers, Concentrated Viscosifiers), and Regional Analysis for 2026 - 2033

Viscosifiers Market Share and Trends Analysis

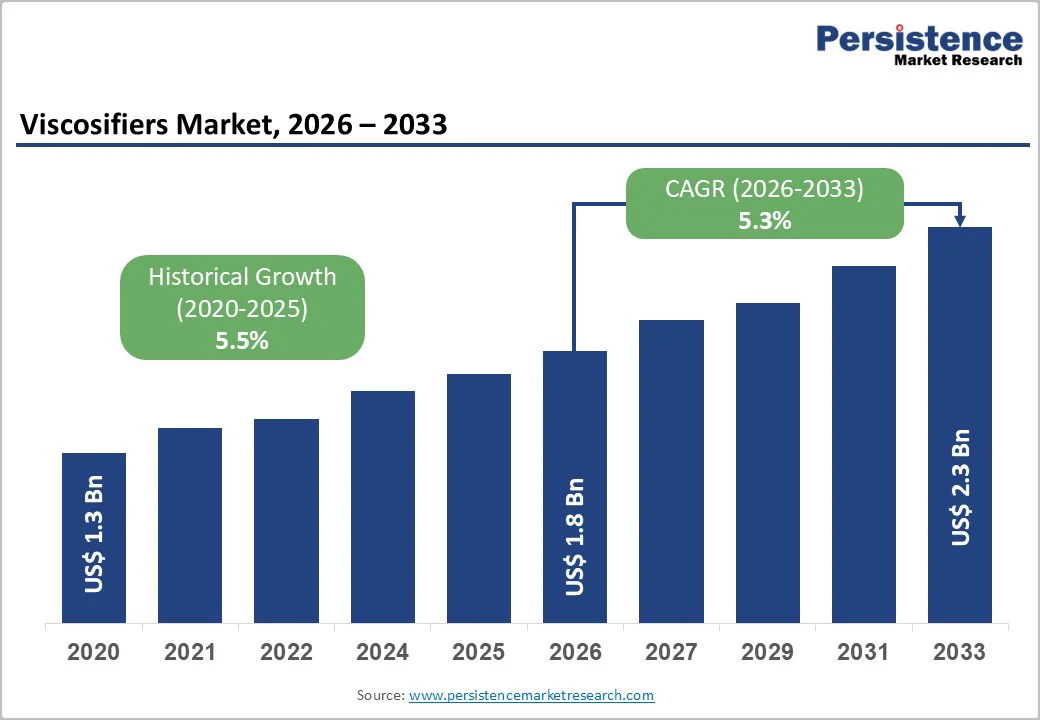

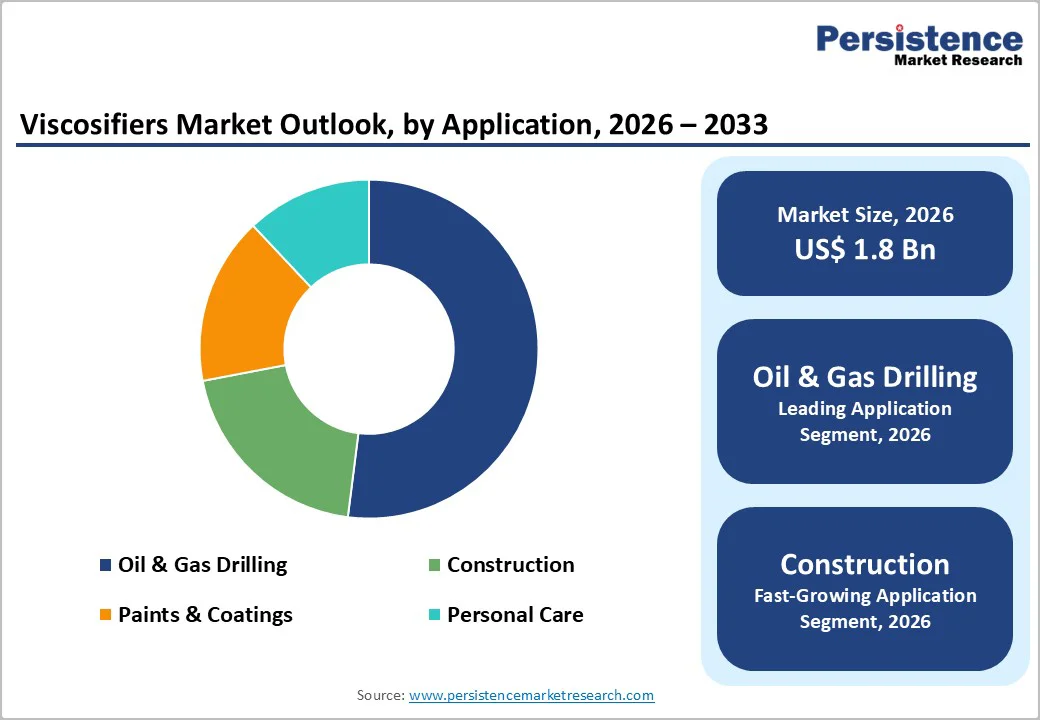

The global viscosifiers market size is likely to be valued at US$ 1.8 billion in 2026, and is projected to reach US$ 2.3 billion by 2033, growing at a CAGR of 5.3% during the forecast period 2026 - 2033.

This steady growth trajectory is driven by expanding oil and gas drilling activities, particularly in unconventional resource extraction, coupled with increasing demand from the construction and personal care industries.

The market benefits from technological advancements in polymer chemistry, which enable the development of more efficient viscosifying agents with enhanced performance. Rising infrastructure investments across emerging economies and the growing emphasis on enhanced oil recovery techniques are expected to continue bolstering market expansion.

Key Industry Highlights

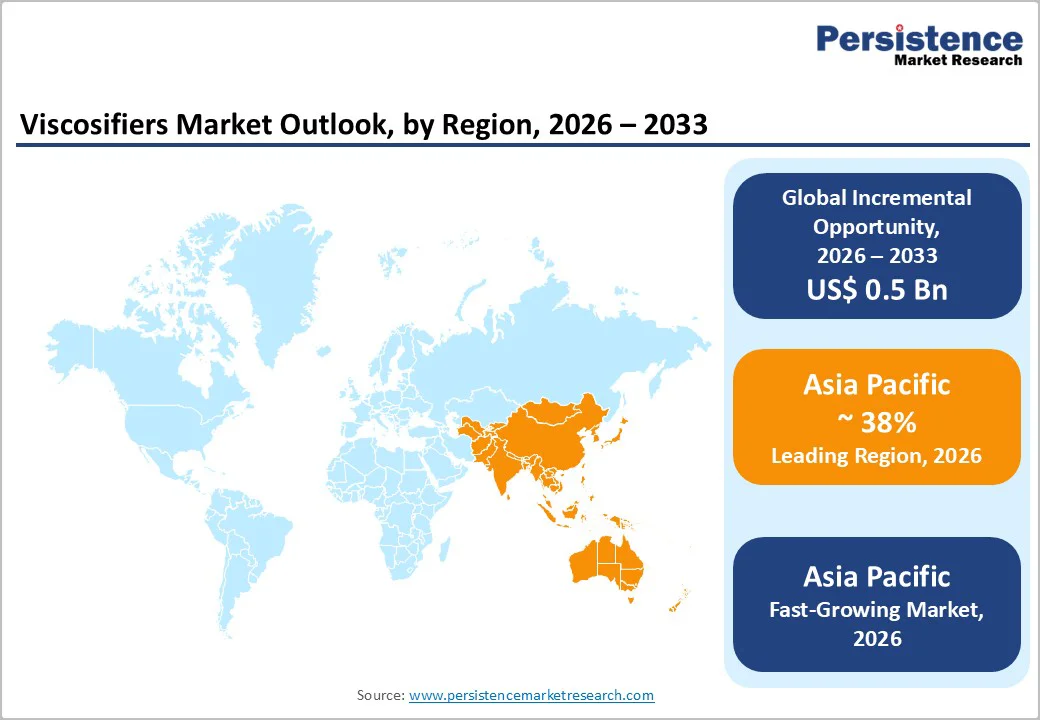

- Dominant Region: Asia Pacific is expected to command an estimated 38% market share in 2026, supported by massive infrastructure development and expanding manufacturing capabilities.

- Fastest-growing Regional Market: Asia Pacific is also set to be the fastest-growing market through 2033, owing to a strong demand for advanced polymers from the construction and oil and gas industries across China and India.

- Leading & Fastest-growing Product Type: Natural viscosifiers are poised to hold about 58% of the market revenue share in 2026, while synthetic viscosifiers are likely to be the fastest-growing through 2033.

- Application Dominance: Oil & gas drilling is slated to dominate with an estimated 52% revenue share in 2026, whereas construction is expected to post the highest CAGR from 2026 to 2033.

- Prominent Drivers: The continued focus of the global energy sector on maximizing hydrocarbon recovery from both conventional and unconventional reserves is a major growth catalyst for viscosifiers.

- Market Opportunities: The personal care and pharmaceutical sectors present substantial growth opportunities for specialty viscosifiers, driven by rising consumer demand for premium formulations and more sophisticated product performance.

| Key Insights | Details |

|---|---|

| Viscosifiers Market Size (2026E) | US$ 1.8 Bn |

| Market Value Forecast (2033F) | US$ 2.3 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.5% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Expanding Oil and Gas Exploration Activities

As energy companies deepen their focus on maximizing hydrocarbon recovery from both conventional and unconventional reserves, the viscosifiers market is likely to gain impetus over the next several years.

Viscosifiers are additives integral to drilling fluid formulations, helping maintain wellbore stability, facilitate cuttings transport to the surface, and minimize formation damage during drilling operations. As exploration and production activities intensify in increasingly complex reservoirs, operators are relying more on advanced viscosifier systems tailored to diverse geological conditions, fluid chemistries, and drilling strategies.

The rapid expansion of horizontal drilling and hydraulic fracturing, particularly in key shale basins and offshore developments, has significantly increased demand for synthetic and natural polymer-based viscosifiers.

At the same time, enhanced oil recovery techniques are gaining prominence as operators seek to extend the productive life of mature fields and improve overall reservoir performance. These enhanced oil recovery (EOR) methods rely heavily on viscosity-modifying agents to increase sweep efficiency, further reinforcing the strategic importance of viscosifiers within the broader oilfield chemicals portfolio.

Price Volatility of Raw Materials

The viscosifiers market operates in a highly volatile cost environment because producers rely on raw materials such as petroleum-based feedstocks, natural polymers, and specialty chemicals, whose prices can change quickly.

Crude oil price swings directly affect the cost of synthetic viscosifiers, since many of these products originate from petrochemical intermediates. In contrast, natural options such as guar gum are subject to additional instability from crop yields, weather events, and geopolitical conditions in key farming regions.

This volatility exposes manufacturers to margin pressure when input prices rise, and competitive conditions limit their ability to adjust selling prices, complicating contract structures, pricing models, and longer-term planning for both suppliers and downstream customers.

In this context, companies benefit from treating raw material risk as a strategic priority rather than a purely operational issue. Practical responses include diversifying the supplier base, negotiating more flexible pricing mechanisms, and, where feasible, using financial or contractual hedging tools to smooth input cost swings.

Firms can also invest in formulation R&D to increase flexibility across feedstocks, explore bio-based or regional alternatives to reduce exposure to single commodities, and collaborate more closely with key customers to co-create pricing and inventory strategies that transparently share risk.

By taking these steps, producers are better positioned to justify capacity expansions and technology upgrades, sustain innovation in advanced viscosifier solutions, and support more predictable medium- to long-term market development.

Emerging Applications in Personal Care and Pharmaceuticals

The personal care and pharmaceutical sectors offer significant avenues for expansion in the specialty viscosifiers market, driven by consumer expectations for superior product quality and formulation sophistication. In the realm of personal care, manufacturers are actively integrating advanced rheology modifiers to precisely control texture, stability, and sensory attributes across skincare, hair care, and color cosmetics.

This shift is particularly evident as brands navigate the "clean beauty" movement, in which natural and bio-based viscosifiers, especially those certified organic or vegan, are becoming essential for market differentiation. By using these specialized ingredients, formulators can develop products that deliver exceptional spreadability and feel while also meeting rigorous label claims on sustainability and ingredient transparency.

Consequently, suppliers who prioritize eco-friendly solutions serve as vital partners to beauty brands seeking to capture value in an increasingly crowded and conscientious marketplace.

In the pharmaceutical industry, viscosifiers serve a crucial functional purpose in high-value applications such as controlled-release drug delivery systems, ophthalmic solutions, and sterile injectables. These sensitive use cases demand high-purity materials that strictly adhere to pharmacopeia standards, ensuring consistent efficacy and minimal impurity levels.

Because these components directly influence patient safety and therapeutic outcomes, demand remains resilient against economic downturns, offering suppliers a stable revenue stream that is often insulated from broader macroeconomic volatility.

Furthermore, the rigorous regulatory documentation required for these ingredients creates high barriers to entry, allowing producers to command premium pricing. This dynamic can enable suppliers to secure attractive profit margins while fostering deep, strategic collaborations with research & development (R&D) teams at leading pharmaceutical companies to innovate next-generation medical treatments.

Category-wise Analysis

Product Type Insights

Natural viscosifiers are slated to command approximately 58% of the product-type revenue share in 2026. These materials have secured their leadership status through a combination of cost-effectiveness, consistent global availability, and reliable performance across diverse end-use applications.

Their straightforward processing requirements and excellent compatibility with water-based formulations render them particularly valuable in sectors where regulatory compliance, product safety, and environmental stewardship represent primary selection criteria.

Within most formulation frameworks, natural viscosifiers strike an optimal balance between affordability and functional capability, enabling manufacturers to meet performance specifications while avoiding the expense of synthetic substitutes.

Products such as guar gum, xanthan gum, cellulose derivatives, and starch-based solutions benefit from mature distribution networks anchored in established agricultural hubs across South Asia, East Asia, and North America, ensuring supply reliability and competitive pricing for end users.

Synthetic viscosifiers are positioned to experience the most robust expansion throughout the 2026 - 2033 timeframe, propelled by their superior technical capabilities and growing adoption in specialized applications requiring exceptional precision.

These formulations, including polyacrylamide derivatives, engineered polymers, and associative thickeners, deliver measurable advantages in thermal stability, salt resistance, and precisely tailored rheological profiles that natural alternatives cannot match.

Industries such as deep-water petroleum extraction, advanced coatings, and pharmaceutical development increasingly depend on these performance attributes to meet rigorous operational demands. For manufacturers navigating highly competitive environments, synthetic viscosifiers offer a compelling opportunity to enhance profit margins and establish meaningful technological differentiation.

Application Insights

Oil and gas drilling operations are expected to account for the largest share of the viscosifiers market revenue, at 52%, in 2026. This commanding position underscores the sector's essential dependence on drilling fluids to execute wellbore operations safely and efficiently. The dominance stems from sustained drilling campaigns across both conventional and unconventional resource bases, spanning shale formations, offshore installations, and deep-water environments.

Within drilling fluid systems, viscosifiers play indispensable roles by regulating rheological properties, facilitating cuttings removal, and preserving wellbore integrity under extreme pressures and temperatures.

Principal petroleum-producing regions, including North America, the Middle East, and offshore areas throughout the Asia Pacific, drive considerable viscosifier consumption through continuous exploration and production initiatives, ensuring steady demand for specialized formulations tailored to challenging subsurface conditions.

Construction stands poised to emerge as the fastest-growing sector through 2033, driven by global infrastructure investment, rapid urban expansion, and the adoption of innovative construction methodologies. Viscosifiers substantially enhance the functionality of cement slurries, mortars, grouts, and self-leveling formulations by elevating workability, reducing water requirements, and producing more consistent, higher-quality applications.

Growth within this segment is further reinforced by large-scale public infrastructure projects, rising residential construction activity across developing economies, and increased deployment of specialized construction chemicals in technically demanding applications.

The emergence of sustainable building standards and high-performance concrete technologies is driving heightened demand for advanced viscosifying agents that meet rigorous environmental criteria and stringent technical certification standards.

Formulation Insights

Concentrated viscosifiers are expected to account for approximately 70% of the market share in 2026. This commanding position reflects compelling economic fundamentals, robust operational alignment with industrial ecosystems, and sustained adoption across high-growth geographies.

The financial case is particularly persuasive: transporting and storing concentrated formulations deliver substantially lower costs than managing pre-diluted alternatives. This distinction resonates strongly with oil and gas operators processing substantial volumes and operating dedicated mixing facilities at drilling sites.

Concentrated formats prove equally attractive to large industrial manufacturers in energy, construction, and processing sectors that possess in-house technical expertise, advanced mixing infrastructure, and comprehensive quality control protocols.

These sophisticated users leverage their capabilities to precisely customize formulations, tailoring viscosifier performance to address specific wellbore conditions, geological characteristics, or operational requirements that standard pre-formulated products cannot accommodate.

Formulated viscosifiers are positioned to achieve the most accelerated growth from 2026 to 2033, driven by expanding demand from personal care, pharmaceutical, food processing, construction chemistry, and small to mid-sized manufacturers that prioritize convenience, performance consistency, and regulatory compliance over absolute cost minimization.

These customers increasingly gravitate toward ready-to-use or pre-engineered solutions that integrate viscosifiers with complementary ingredients such as stabilizers and preservatives, substantially reducing formulation development timelines, internal laboratory demands, and regulatory navigation complexity.

This preference reflects organizational realities: many smaller and mid-sized enterprises operate with constrained technical resources and limited mixing capability, making pre-engineered systems not merely convenient but strategically essential for achieving market-competitive products while maintaining operational efficiency and compliance accountability.

Regional Insights

Asia Pacific Viscosifiers Market Trends

Asia Pacific is expected to occupy the top position in 2026, capturing approximately 38% of the viscosifiers market share and posting the fastest growth rate during the 2026 - 2033 forecast period. This dominance stems from four converging forces: massive infrastructure development, expanding manufacturing capabilities, rising energy consumption, and rapid urbanization.

The construction sector, the oil and gas industry, and broader industrial applications account for the bulk of regional consumption. The economies of China, India, Japan, and ASEAN each contribute substantially to this uptake.

Strategic investments in transportation networks, urban development projects, industrial facilities, and smart city initiatives directly increase consumption of construction chemicals and drilling fluids. Viscosifiers enable these applications to meet strict performance, durability, and process reliability requirements.

Offshore exploration and production in the South China Sea, the Indian Ocean, and surrounding Southeast Asian waters continue to drive steady demand for oilfield viscosifiers for drilling, cementing, and completion operations. Simultaneously, the region's developing personal care and pharmaceutical sectors create a fresh appetite for specialty-grade viscosifiers in premium formulations.

These industries require precise rheological control, high-purity standards, and superior sensory performance, thereby accelerating the adoption of advanced, application-specific solutions. The region also enjoys distinct manufacturing advantages, including competitive production costs, dependable access to key raw materials, such as natural polymers derived from agricultural outputs, and increasingly advanced formulation and process engineering expertise.

Europe Viscosifiers Market Trends

Europe remains a mature yet strategically significant market for viscosifiers, with demand concentrated in construction, personal care, and pharmaceutical applications rather than energy-related uses. Major economies such as Germany, the United Kingdom, France, and Spain lead consumption, guided by high expectations for product performance, safety, and sustainability.

The market’s focus has shifted from volume-based growth to high-value, specialty-grade viscosifiers that provide precise rheological control, greater functionality, and stronger environmental credentials. Although this transition results in slower growth compared with regions experiencing rapid industrial expansion, it ensures a stable demand base centered on advanced manufacturing and sophisticated consumer sectors that prioritize quality and compliance.

Continued growth of the European market reflects sustained investment in infrastructure renewal and green building initiatives that align with the European Union (EU)’s sustainability and climate goals. Policy frameworks such as the European Green Deal and various national climate strategies encourage the adoption of bio-based and low-impact viscosifiers while gradually restricting traditional petroleum-derived variants.

Additionally, the region’s stringent chemical regulatory system, particularly the Registration, Evaluation, Authorisation and Restriction of Chemicals (REACH) framework, raises compliance costs and entry barriers but stimulates research into safer, more sustainable alternatives. As a result, companies with strong regulatory, technical, and distribution expertise are well-positioned to lead in this evolving and environmentally conscious market.

North America Viscosifiers Market Trends

North America represents a substantial and strategically important market for viscosifiers, with the United States commanding regional consumption through extensive shale oil and gas operations, vigorous construction activity, and advanced manufacturing infrastructure. The region's leadership position rests on technological innovation, significant R&D expenditure, and the concentration of major chemical manufacturers alongside diverse end-users.

Upstream energy operations rely extensively on horizontal drilling and multi-stage hydraulic fracturing across major shale formations, such as the Permian, Eagle Ford, and Bakken basins, which require specialized viscosifier systems within drilling, completion, and stimulation fluids.

Infrastructure modernization efforts and sustained investments in transportation networks, utility systems, and industrial facilities are also foreseen to generate consistent demand for construction-grade viscosifiers used in cementitious systems, coatings, and various building materials. This creates a diversified consumption profile spanning energy extraction, construction projects, and industrial process applications.

Federal and state-level regulations enforced by environmental and occupational safety agencies continue to shape market evolution and product development priorities. These regulatory requirements emphasize environmental protection, worker safety, and chemical disclosure standards, which elevate compliance costs but simultaneously accelerate the transition toward safer, low-toxicity, and bio-based formulations.

North America hosts a concentrated network of global chemical leaders and specialized oilfield service providers, facilitating rapid technology deployment and close collaboration on customized solutions. Current investment patterns increasingly prioritize sustainable chemistry approaches, digital integration in formulation design and performance monitoring, and strategic partnerships between chemical suppliers, drilling contractors, and industrial customers.

Competitive Landscape

The global viscosifiers market features a moderately consolidated structure, with major companies such as BASF SE, Schlumberger Limited, Clariant AG, Akzo Nobel N.V., and Ashland Global Holdings Inc. collectively holding approximately 40 to 45 percent of market share.

These industry leaders focus on R&D to introduce advanced, high-performance viscosifiers specifically designed for the oil and gas sector, including solutions for extreme high-temperature and high-pressure environments.

The market landscape is highly competitive, as multinational corporations compete with regional players for market share through product innovation, mergers, acquisitions, and strategic alliances. Leading firms are expanding their portfolios with tailored viscosifier solutions that address unique drilling challenges, allowing them to maintain a strong competitive position.

At the same time, sustainability has become a central driver in the sector, prompting significant investments in eco-friendly viscosifier development. These efforts align with global environmental regulations and help companies strengthen their reputation and market appeal. As environmental standards tighten, manufacturers are increasingly prioritizing green chemistry and low-impact formulations, further shaping the trajectory of product innovation and market competition.

Key Industry Developments

- In October 2025, BRB Lube Oil Additives & Chemicals launched Viscotech Upcycled, a low-carbon viscosity modifier portfolio dissolved in high-quality re-refined base oils (RRBO) as a virgin oil alternative. These drop-in solutions cut cradle-to-gate carbon footprint by 60%, aiding scope 3 reductions and circular economy goals. Performance matches virgin-based modifiers, supporting automotive and industrial lubricants while aligning with PETRONAS Chemicals Group's 1.5°C emissions targets.

- In October 2025, Lubrizol’s Carbopol BioSense Polymer earned the Bronze BSB Innovation Award in the Environment/Raw Materials category for its naturally derived rheology modifier and sensory enhancer properties. This vegan, COSMOS/ECOCERT-certified polymer, with 98% natural origin content, delivers a rich, soft, silicone-like feel without stickiness or peeling, suiting serums, lotions, light creams, skin care emulsions, and sun care with organic UV filters. It adheres to green chemistry’s 12 principles, meeting the demand for high-performing natural ingredients in cosmetics.

Companies Covered in Viscosifiers Market

- BASF SE

- Schlumberger Limited

- Halliburton Company

- Baker Hughes Company

- Clariant AG

- Croda International Plc

- The Lubrizol Corporation

- Stepan Company

- Akzo Nobel N.V.

- Ashland Global Holdings Inc.

- Elementis Plc

- Kemira Oyj

- SNF Floerger

- Solvay S.A.

- Arkema S.A.

- Dow Inc.

Frequently Asked Questions

The global viscosifiers market is projected to reach US$ 1.8 billion in 2026.

Expanding oil & gas drilling, infrastructure construction, and specialty chemical demand in personal care/pharma are driving the market.

The market is poised to witness a CAGR of 5.3% from 2026 to 2033.

Formulation of sustainable viscosifiers for EOR/green construction, high-performance pharma formulations, and emerging EV battery production applications are key market opportunities.

BASF SE, Schlumberger Limited, Clariant AG, Akzo Nobel N.V and Ashland Global Holdings Inc. are some of the key players in the market.