- Medical Devices

- Capsule Endoscopy Market

Capsule Endoscopy Market Size, Share, and Growth Forecast 2026 - 2033

Capsule Endoscopy Market by Endoscopy Type (Small Bowel Capsule Endoscopy, Esophageal Capsule Endoscopy, Colon Capsule Endoscopy, Others), by Application (OGIB, Crohn's Disease, Small Intestine Tumor, Celiac Disease, Others), by End User, by Regional Analysis, 2026 - 2033

Capsule Endoscopy Market Size and Trend Analysis

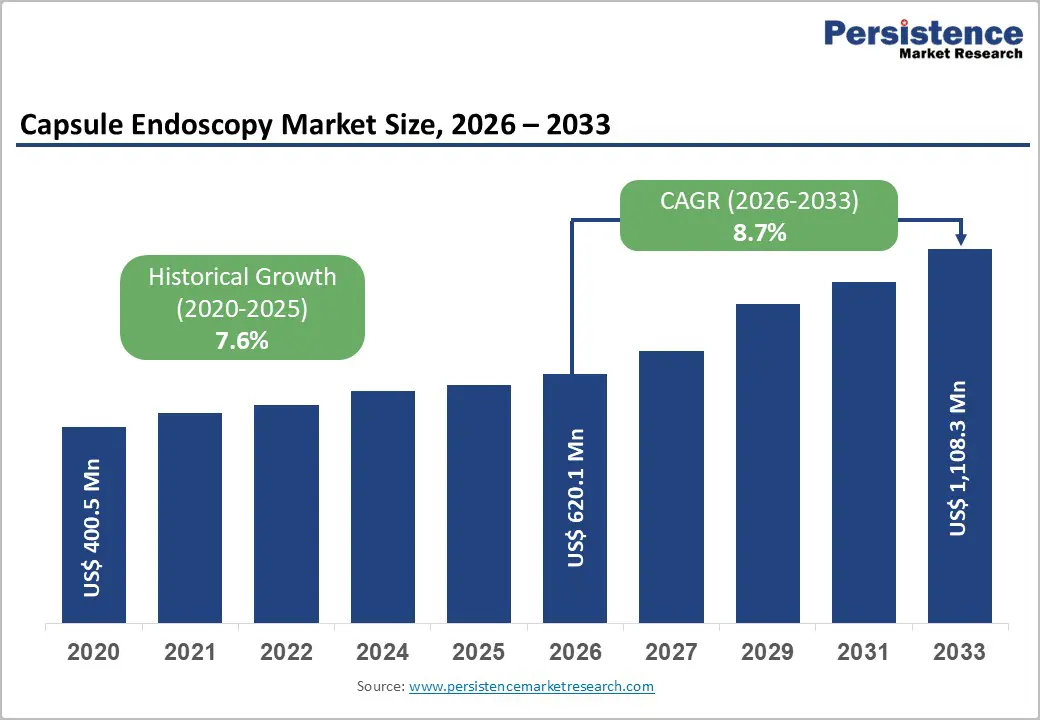

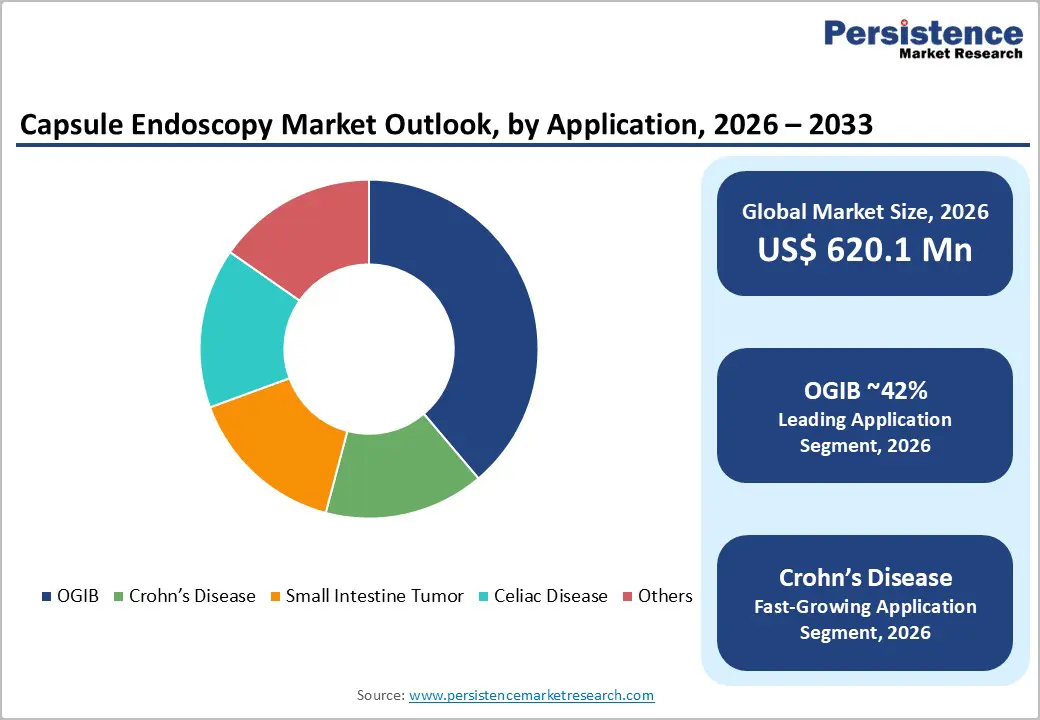

The global capsule endoscopy market size is expected to be valued at US$ 620.1 million in 2026 and projected to reach US$ 1,108.3 million by 2033, growing at a CAGR of 8.7% between 2026 and 2033. driven by rising adoption of minimally invasive gastrointestinal diagnostics capsule endoscopy procedures, increasing gastrointestinal disease prevalence, and stronger demand for wireless capsule endoscopy system technologies in clinical diagnostics.

The shift toward non-invasive screening, particularly for small bowel evaluation, is driving adoption in hospitals and outpatient care. AI-enabled capsule endoscopy systems are improving diagnostic accuracy and reducing interpretation time. Growing use in Crohn’s disease and obscure gastrointestinal bleeding (OGIB), along with supportive FDA and CE approvals, is further accelerating global adoption.

Key Industry Highlights

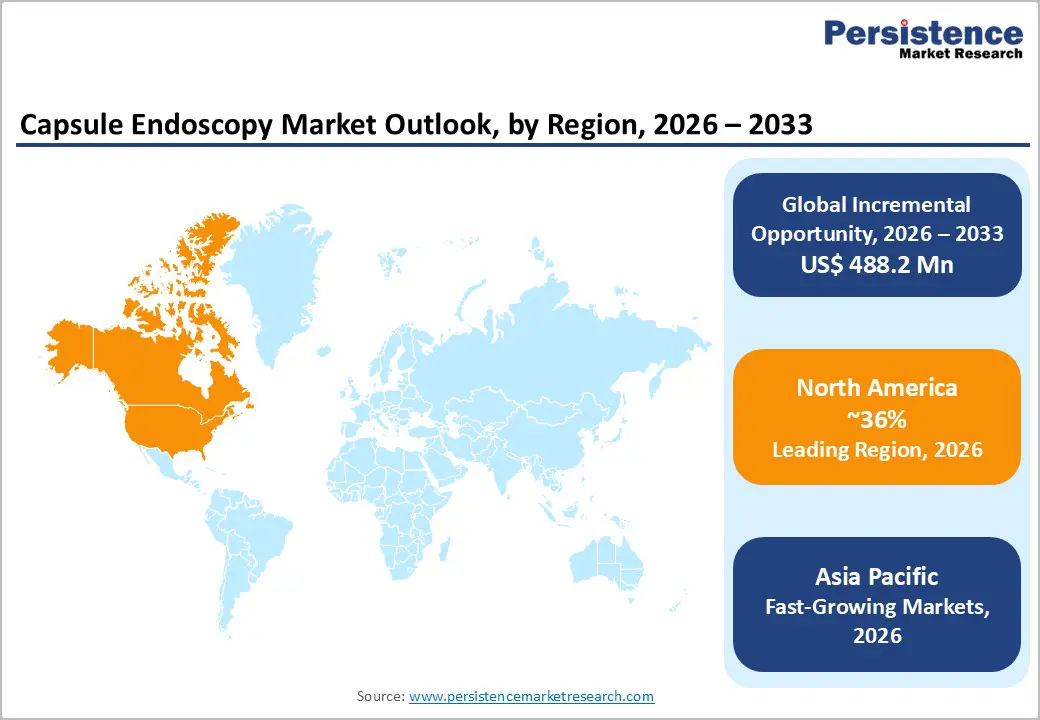

- Leading Region: North America led the Capsule Endoscopy market with a 36% share in 2025, supported by favorable Medicare reimbursement, strong clinical guideline support, and widespread adoption of Medtronic and Olympus platforms.

- Fastest Growing Region: Asia Pacific is projected to witness the fastest growth through 2033 due to increasing IBD prevalence, expanding gastroenterology infrastructure, and affordable capsule endoscopy systems from Chinese manufacturers.

- Dominating Segment: Small Bowel Capsule Endoscopy dominated with nearly 72% share in 2025, driven by its established role in diagnosing OGIB and Crohn’s disease and strong physician preference globally.

- Fastest Growing Segment: Crohn’s Disease monitoring is the fastest-growing application segment, fueled by rising biologic therapy usage, increasing demand for mucosal healing assessment, and growing preference for non-invasive monitoring technologies.

- Key Opportunity: Colon Capsule Endoscopy represents a major growth opportunity owing to increasing colorectal cancer screening initiatives, expanding clinical guideline inclusion, and rising patient preference for minimally invasive diagnostic procedures.

Market Dynamics

Drivers - Rising Global Prevalence of Crohn's Disease and Inflammatory Bowel Disorders

The increasing global incidence and prevalence of inflammatory bowel disease (IBD) encompassing Crohn's disease and ulcerative colitis is a major structural driver of the Capsule Endoscopy market. Small bowel capsule endoscopy is recognized as the preferred first-line imaging modality for the diagnosis and monitoring of Crohn's disease affecting the small intestine, a segment largely inaccessible to conventional endoscopy. According to the Crohn's & Colitis Foundation, approximately 3.1 million Americans are diagnosed with IBD, with Crohn's disease prevalence rising globally at an estimated rate of 1.5–2% per year across high-income countries. The European Crohn's and Colitis Organisation (ECCO) guidelines recommend capsule endoscopy as a standard diagnostic tool for suspected small bowel Crohn's disease, institutionalizing its clinical procurement within gastroenterology departments across Europe and North America. As IBD incidence accelerates in newly industrialized Asia Pacific markets, geographic demand expansion is further amplifying this driver.

Restraints - High Procedure Cost and Limited Reimbursement in Emerging Markets

Despite technological advancements, the adoption of capsule endoscopy devices remains constrained by high procedural costs and inconsistent reimbursement frameworks across regions. The cost of a single capsule-based diagnostic procedure remains significantly higher than conventional imaging or endoscopy methods, limiting accessibility in cost-sensitive markets. In several emerging economies, insurance coverage is either partial or absent, reducing patient affordability.

Regulatory bodies such as the U.S. Centers for Medicare & Medicaid Services (CMS) also provide selective reimbursement, primarily for OGIB and Crohn’s indications, restricting broader application. This creates a structural barrier to large-scale adoption, especially in outpatient facilities. As healthcare systems prioritize cost containment, budget limitations may slow procurement of advanced wireless capsule endoscopy system technologies, despite their clinical advantages.

Opportunities - Colon Capsule Endoscopy as an Emerging Colorectal Cancer Screening Modality

Colon Capsule Endoscopy (CCE) represents a transformative growth opportunity for the Capsule Endoscopy market, positioned as a patient-preferred, non-invasive alternative to conventional optical colonoscopy for colorectal cancer (CRC) screening. The American Cancer Society (ACS) estimates that colorectal cancer is the third most common cancer globally, with over 1.9 million new cases diagnosed in 2022. The U.S. Multi-Society Task Force on Colorectal Cancer and European Society of Gastrointestinal Endoscopy (ESGE) have both included colon capsule endoscopy in their CRC screening guidelines as a viable alternative for patients who are unable or unwilling to undergo conventional colonoscopy a population representing a large unmet clinical need. Medtronic's PillCam COLON 2 and Jinshan Science & Technology's NaviCam colon system are actively pursuing expanded regulatory approvals and payor reimbursement coverage for CRC screening indications across U.S., EU, and Asia Pacific markets, creating a high-growth commercial development runway through 2033.

Category-wise Insights

Endoscopy Type Analysis

Small bowel capsule endoscopy leads the capsule endoscopy market with 46% share in 2026, driven by its key role in diagnosing OGIB and Crohn’s disease, where conventional endoscopy has limited reach. It offers complete visualization of the small intestine, making it a preferred first-line diagnostic tool. The growing use of wireless capsule endoscopy system technologies is strengthening clinical adoption. Hospital upgrades across the U.S. and Europe for GI bleeding and anemia cases are reinforcing usage. This is increasing demand for capsule endoscopy devices in advanced diagnostic workflows.

Colon capsule endoscopy is the fastest-growing segment at 9.2% CAGR through 2033, driven by rising demand for non-invasive colorectal cancer screening and improved patient acceptance. It is emerging as an alternative to traditional colonoscopy in preventive care programs. Advances in minimally invasive GI diagnostics capsule endoscopy procedures are improving diagnostic accuracy. Expansion of national screening programs in Europe and Japan is supporting adoption. This is boosting demand for disposable capsule endoscopy devices in the market trends in preventive healthcare.

Application Analysis

OGIB leads the application segment with 42% share in 2026, due to its diagnostic complexity and the frequent failure of conventional endoscopy to identify bleeding sources. Capsule imaging is essential for detecting hidden small bowel lesions. The use of gastrointestinal capsule endoscopy procedures is now a standard diagnostic approach in such cases. Updated clinical guidelines in North America and Europe support capsule use after negative endoscopy results. This is driving strong hospital dependence on capsule endoscopy devices.

Crohn’s disease is projected to be the fastest-growing segment, expanding at a 9.5% CAGR, driven by the rising prevalence of inflammatory bowel disease and increasing demand for early diagnosis. Capsule imaging provides detailed mucosal assessment and improved disease monitoring, supporting better clinical outcomes. Growing adoption of capsule endoscopy in Crohn’s disease diagnosis, along with its earlier incorporation into IBD diagnostic pathways in developed markets, is further boosting uptake. This is contributing to increased use of advanced capsule endoscopy technologies in chronic disease management.

End User Analysis

Hospitals dominate with 62% share in 2026, due to strong infrastructure, specialist availability, and reimbursement support. They are the primary centers for capsule endoscopy devices, especially for complex and high-risk GI cases. Integration of AI-based imaging is improving diagnostic efficiency. Recent upgrades in hospital GI departments across developed markets are enhancing workflows. This is strengthening the adoption of wireless capsule endoscopy system technologies.

Outpatient facilities are expected to be the fastest-growing segment at 9.7% CAGR, driven by demand for cost-effective and faster GI diagnostics. They are increasingly used for routine evaluations and follow-ups. Adoption of minimally invasive GI diagnostics capsule endoscopy procedures is expanding outside hospitals. The growth of ambulatory care infrastructure in India and China is supporting this shift. This is the increasing use of capsule endoscopy devices in decentralized diagnostic settings.

Regional Insights

North America Capsule Endoscopy Market Trends and Insights

North America leads the global Capsule Endoscopy market with a 36% share in 2025, driven by the U.S.'s well-established Medicare and commercial insurance reimbursement frameworks for small bowel capsule endoscopy, high physician adoption rates supported by AGA and ASGE clinical practice guidelines, and the concentrated presence of leading device innovators. Growing AI-augmented capsule reading platform deployment is further accelerating procedural efficiency across the region's high-volume academic and community gastroenterology centers.

U.S. Capsule Endoscopy Market Size

The U.S. accounts for approximately 87% of North American Capsule Endoscopy revenues, estimated at roughly US$ 195 million in 2026. Medicare covers capsule endoscopy under specific CPT codes for OGIB and Crohn's disease indications. The CDC estimates over 3 million Americans diagnosed with IBD and approximately 150,000 new annual cases, sustaining a large and growing clinical referral base for capsule endoscopy procedures.

Canada Capsule Endoscopy Market Size

Canada is estimated to represent 13% of the regional market, driven by public healthcare support and expanding GI diagnostic capacity. Adoption of minimally invasive GI diagnostics capsule endoscopy procedures is rising in tertiary hospitals. Investment in hospital imaging infrastructure is improving access to capsule-based diagnostics. Collaboration with global medtech firms is supporting the availability of wireless capsule endoscopy system solutions.

Europe Capsule Endoscopy Market Trends and Insights

Europe is the second-largest Capsule Endoscopy market, underpinned by ECCO and ESGE clinical guidelines that broadly endorse capsule endoscopy across OGIB, Crohn's disease, and celiac disease indications, and by universal health system reimbursement in major markets including Germany, France, and the UK Growing European colon capsule endoscopy adoption for CRC screening supported by ESGE guideline inclusion is expanding the regional procedural base beyond the traditional small bowel indication.

Germany Capsule Endoscopy Market Size

Germany holds approximately 23% of European Capsule Endoscopy market revenues. The GKV statutory health insurance system covers small bowel capsule endoscopy for approved indications. Germany's high density of gastroenterology specialists approximately 5,000 gastroenterologists per Berufsverband Niedergelassener Gastroenterologen Deutschlands (bng) and active IBD management community drives strong procedural adoption of capsule endoscopy platforms.

UK Capsule Endoscopy Market Size

The UK accounts for approximately 16% of European Capsule Endoscopy revenues. NHS England commissions capsule endoscopy as a standard diagnostic investigation for OGIB and suspected small bowel Crohn's disease through tertiary gastroenterology centres. NICE has published guidance supporting capsule endoscopy for small bowel investigation, providing procurement authorization for NHS trusts expanding their gastroenterology diagnostic capacity.

Asia Pacific Capsule Endoscopy Market Trends and Insights

Asia Pacific is the fastest-growing regional Capsule Endoscopy market over 2026–2033, fueled by rising IBD incidence in urban populations, expanding gastroenterology specialist infrastructure, and growing domestic device manufacturing capacity in China and Japan. China is the dominant country market in the region, with Jinshan Science & Technology and Ankon Technologies developing cost-competitive domestic capsule endoscopy platforms that are expanding procedure access across China's large tier-2 and tier-3 city hospital network, supported by NMPA regulatory clearances for their products.

China Capsule Endoscopy Market Size

China is estimated to account for ~34% of the Asia Pacific market share, driven by large hospital networks and strong manufacturing capacity. It is a key producer and consumer of capsule endoscopy devices. Expansion of tertiary hospitals is improving access to advanced GI diagnostics. Rising focus on early detection is increasing the adoption of advanced diagnostic capsule endoscopy technology.

India Capsule Endoscopy Market Size

India contributes approximately 12% of Asia Pacific Capsule Endoscopy revenues. Rising urbanization-associated IBD incidence and growing awareness of non-invasive GI diagnostics are expanding the clinical indication base. AIIMS and major private hospital chains including Apollo Hospitals and Fortis Healthcare are deploying capsule endoscopy platforms for OGIB and Crohn's disease investigation in tier-1 cities, with growing demand from corporate health insurance networks.

Competitive Landscape

The global market exhibits a moderately consolidated structure, with Medtronic (through its Given Imaging acquisition) and Olympus Corporation commanding the majority of revenues through established PillCam and EndoCapsule platforms respectively. Fujifilm Holdings Corporation and IntroMedic Co. Ltd. compete in the premium imaging quality segment, while Chinese manufacturers including Jinshan Science & Technology, Ankon Technologies, and SonoScape Medical are gaining market share through cost-competitive platforms targeting the Asia Pacific institutional market. Key competitive differentiators include AI-powered reading software integration, capsule battery life and image resolution, proprietary RFID localization technology, and regulatory clearance breadth. Emerging business model trends include procedure-as-a-service and software subscription models for AI reading platforms.

Key Developments

- In March 2026, Fujifilm strengthened India’s diagnostic ecosystem by deploying advanced imaging and endoscopy-enabled systems across hospitals, improving access to high-precision gastrointestinal diagnostics. This reinforces broader adoption of integrated capsule endoscopy devices within multi-modality GI care pathways.

- In October 2025, Medtronic strengthened global dominance in capsule endoscopy systems, expanding its PillCam deployment across hospital networks, reinforcing leadership in capsule endoscopy devices with wide clinical adoption in GI diagnostics.

- February 2025: Medtronic received FDA De Novo authorization for an AI-powered automated capsule endoscopy reading module integrated with its PillCam SB 3 system, reducing small bowel image review time by up to 70% compared to manual expert review in clinical validation studies.

Global Capsule Endoscopy Market – Key Insights

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 400.5 million |

|

Current Market Value (2026) |

US$ 620.1 million |

|

Projected Market Value (2033) |

US$ 1,108.3 million |

|

CAGR (2026–2033) |

8.7% |

|

Leading Region |

North America, 36% market share |

|

Dominant Endoscopy Type |

Small Bowel Capsule Endoscopy, 72% market share |

|

Top-ranking Application |

OGIB, 42% market share |

|

Incremental Opportunity |

US$ 488.2 million |

Companies Covered in Capsule Endoscopy Market

- Medtronic

- Olympus Corporation

- CapsoVision Inc.

- IntroMedic Co. Ltd.

- Jinshan Science & Technology

- Fujifilm Holdings Corporation

- RF Co. Ltd.

- Check-Cap Ltd.

- Ankon Technologies

- BodyCap Medical

- Pentax Medical

- Medisafe Distribution

- Smart Medical Systems

- SonoScape Medical

- Others

Frequently Asked Questions

The global capsule endoscopy market is projected to reach US$620.1 million in 2026.

Rising gastrointestinal disease prevalence and growing adoption of minimally invasive GI diagnostics capsule endoscopy procedures drive the market.

North America leads the global market with a 36% share in 2025.

Opportunities include the expansion of wireless capsule endoscopy system adoption and the rising demand for AI-driven diagnostic solutions.

Key players include Medtronic, Olympus Corporation, Fujifilm, CapsoVision, and IntroMedic.