- Pharmaceuticals

- HPMC Capsules Market

HPMC Capsules Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

HPMC Capsules Market by Product (Serum Separator Gel (SSG) Tubes, EDTA Tubes, Heparin Tubes, Plasma Separator Tubes, and Capillary Blood Collection Tubes), by Shape (Cylindrical and Round-bottom), by End User (Hospitals, Specialty Clinics, Diagnostic Laboratories, Blood Banks, and Academic & Research Institutions), and Regional Analysis from 2026 to 2033.

HPMC Capsules Market Share and Trend Analysis

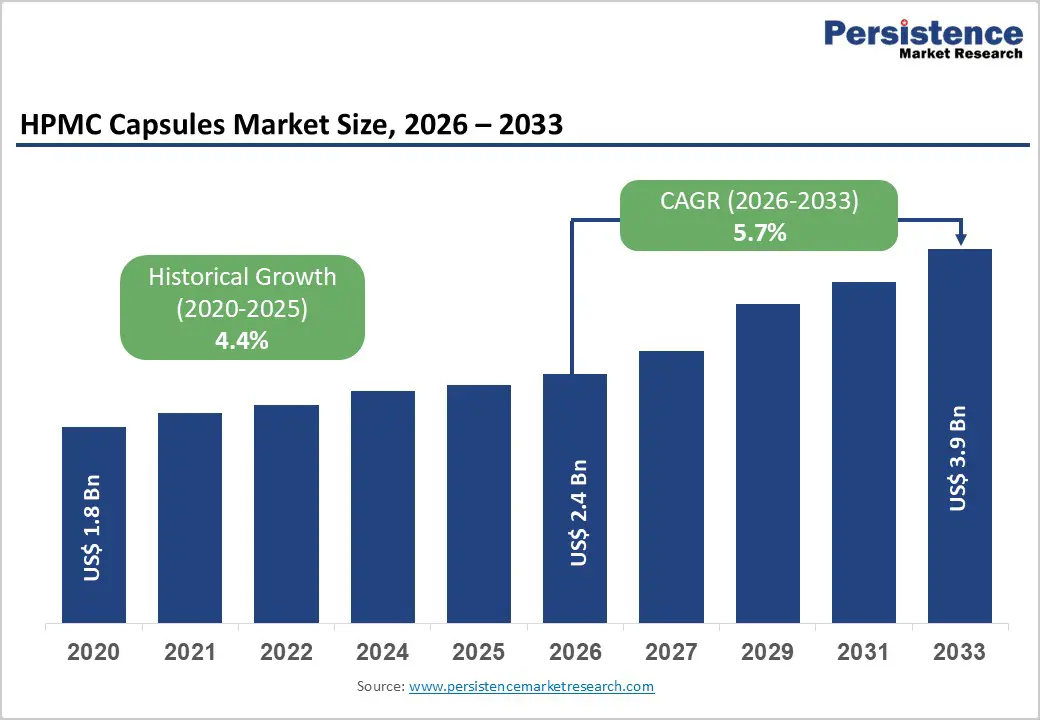

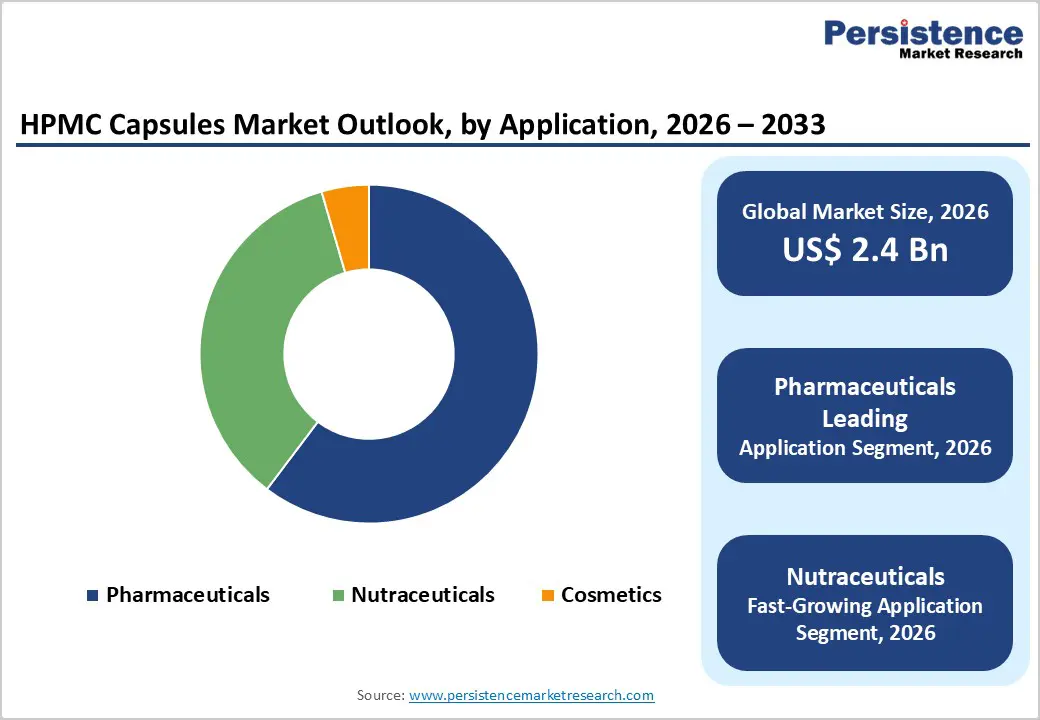

The global HPMC capsules market size is estimated to grow from US$ 2.4 Bn in 2026 to US$ 3.9 Bn by 2033. The market is projected to record a CAGR of 5.7% during the forecast period from 2026 to 2033.

Global demand for hydroxypropyl methylcellulose (HPMC) capsules is increasing steadily, driven by the expanding pharmaceutical and nutraceutical industries, rising preference for vegetarian and clean-label dosage forms, and growing consumption of oral solid medications worldwide. Drug manufacturers are increasingly adopting HPMC capsules due to their stability across temperature and humidity conditions, compatibility with a wide range of APIs, and suitability for global distribution. Growing prevalence of chronic diseases, long-term medication use, and higher consumption of dietary supplements are significantly increasing capsule demand across both developed and emerging markets. HPMC capsules are widely used across prescription drugs, generics, and nutraceutical products to ensure consistent dosing, reliable dissolution, and improved patient acceptability. Increasing emphasis on regulatory compliance, product safety, and standardized excipient quality is further supporting adoption. Technological advancements in capsule manufacturing, including improved machinability and dissolution performance, are enhancing usability for high-speed filling operations. In parallel, expanding pharmaceutical manufacturing capacity in emerging economies and rising investments in healthcare and preventive nutrition are reinforcing long-term global demand for HPMC capsules.

Key Industry Highlights

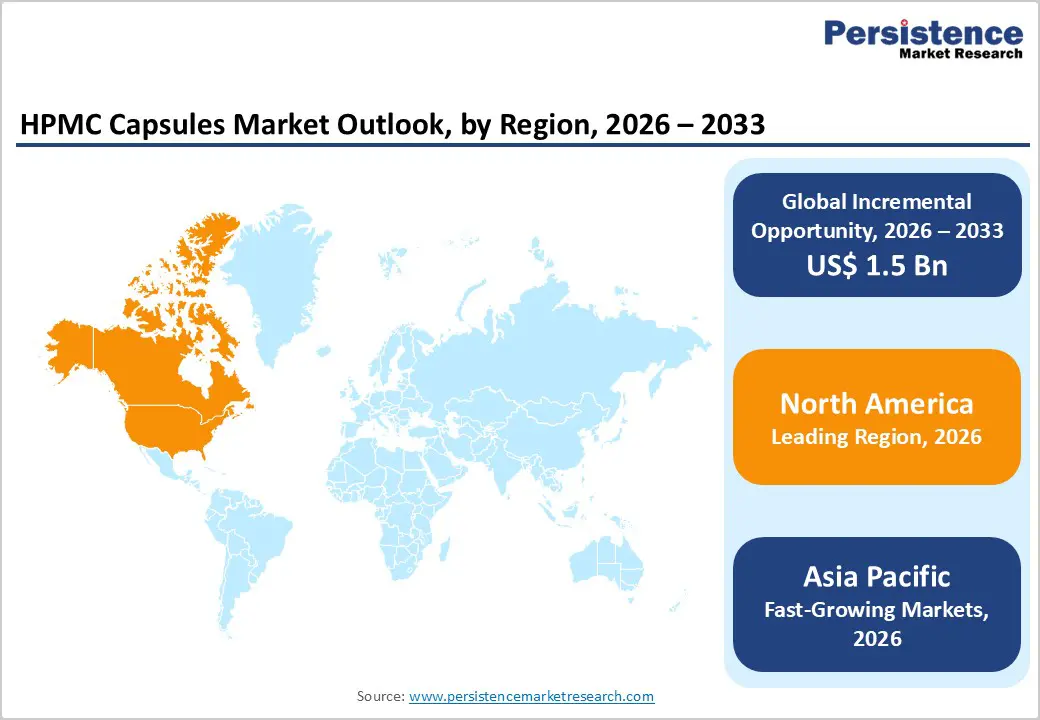

- Leading Region: North America holds the largest share at 47.3%, supported by advanced pharmaceutical manufacturing infrastructure, strong regulatory compliance, high prescription drug consumption, and robust nutraceutical demand.

- Fastest-Growing Region: Asia Pacific is expanding fastest due to rapid pharmaceutical production growth, increasing healthcare expenditure, rising awareness of vegetarian dosage forms, and strong presence of contract manufacturing organizations.

- Leading Product Segment: Gelatin HPMC Capsules dominate the market due to established pharmaceutical acceptance, strong mechanical properties, and high compatibility with automated filling lines.

- Fastest-Growing Product Segment: Non-Gelatin HPMC Capsules are growing rapidly, driven by clean-label trends, vegan preferences, and rising demand from nutraceutical manufacturers.

- Leading End User Segment: Hospitals remain a major segment, supported by high prescription volumes, institutional drug procurement, and continuous medication demand.

- Fastest-Growing User Segment: Nutraceutical manufacturers are scaling quickly as demand for plant-based supplements and preventive healthcare products continues to rise.

| Global Market Attributes | Key Insights |

|---|---|

| HPMC Capsules Market Size (2026E) | US$ 2.4 Bn |

| Market Value Forecast (2033F) | US$ 3.9 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.7% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.4% |

Market Dynamics

Driver – Rising Demand for Vegetarian Capsules, Expanding Oral Solid Dosage Production, and Regulatory Acceptance

Growth is strongly supported by the increasing global shift toward vegetarian, gelatin-free, and clean-label pharmaceutical products, driven by changing consumer preferences, religious considerations, and ethical concerns. HPMC capsules are widely recognized as a suitable alternative to traditional gelatin capsules, particularly for patients seeking plant-based dosage forms. At the same time, the continuous rise in oral solid dosage manufacturing—including tablets and capsules across both branded and generic drug segments is fueling sustained demand. Pharmaceutical companies favor HPMC capsules due to their superior stability under varying humidity and temperature conditions, making them suitable for global distribution and long shelf life requirements.

Regulatory acceptance across major pharmacopeias (USP, EP, JP) further strengthens adoption, as manufacturers can seamlessly integrate HPMC capsules into existing approval pathways. Growth in chronic disease prevalence, such as cardiovascular disorders, diabetes, and gastrointestinal conditions, has increased long-term medication use, supporting higher capsule consumption. Additionally, nutraceutical and dietary supplement manufacturers are increasingly adopting HPMC capsules to align with clean-label marketing strategies. The scalability of HPMC capsule production, compatibility with high-speed filling equipment, and reduced cross-linking risks compared to gelatin collectively reinforce their role as a preferred dosage form, driving consistent market expansion.

Restraints – Higher Production Costs, Price Sensitivity, and Manufacturing Complexity

Market expansion is constrained by higher production and raw material costs associated with HPMC capsules compared to conventional gelatin alternatives. The specialized manufacturing processes, stringent quality controls, and dependence on high-purity cellulose derivatives contribute to elevated pricing, which can limit adoption in cost-sensitive pharmaceutical and nutraceutical segments. In emerging economies, manufacturers often prioritize lower-cost dosage forms to remain competitive, slowing the transition toward HPMC capsules despite their functional advantages.

Price pressure is particularly evident among generic drug producers and small-scale supplement manufacturers, where margins are narrow and procurement decisions are highly cost-driven. In addition, HPMC capsules may present formulation challenges for certain APIs, including slower dissolution under specific conditions, requiring formulation optimization and additional development time. Manufacturing complexity, such as tighter control over moisture content and machine settings during encapsulation, can increase operational costs and technical barriers for smaller manufacturers. Supply chain dependence on cellulose sourcing and limited availability of specialized capsule grades may also impact consistency in certain regions. Furthermore, lack of awareness among some manufacturers regarding recent improvements in HPMC capsule performance continues to slow adoption. Together, cost constraints, technical considerations, and competitive pricing pressures restrain faster penetration across all market tiers.

Opportunity – Growth in Nutraceuticals, Clean-Label Pharmaceuticals, and Emerging Manufacturing Hubs

Significant opportunities are emerging from the rapid expansion of the global nutraceutical and dietary supplement industry, where demand for plant-based, allergen-free, and ethically sourced dosage forms is accelerating. HPMC capsules align well with clean-label positioning, making them increasingly attractive for premium supplements, herbal products, and functional nutrition formulations. Pharmaceutical companies are also exploring HPMC capsules for modified-release and specialty drug applications, opening new avenues beyond conventional immediate-release formulations.

Emerging manufacturing hubs in Asia Pacific, Latin America, and parts of the Middle East offer strong growth potential as local pharmaceutical production scales up to meet domestic and export demand. Governments in these regions are supporting domestic drug manufacturing through favorable policies, creating opportunities for increased adoption of advanced excipients and capsule technologies. Technological advancements in HPMC capsule design such as improved dissolution profiles, enhanced machinability, and better compatibility with sensitive APIs are further expanding application scope. Strategic collaborations between capsule manufacturers, CMOs, and pharmaceutical companies can accelerate innovation and market penetration. As consumer awareness around sustainability and ingredient transparency continues to rise, HPMC capsules are well positioned to benefit from long-term structural shifts toward cleaner and more inclusive oral dosage solutions.

Category-wise Analysis

By Product, Gelatin HPMC Capsules Lead Due to Superior Processability and Broad Pharmaceutical Acceptance

Gelatin HPMC Capsules are projected to dominate the global HPMC capsules market in 2026, accounting for a revenue share of 70.0%. Their leadership is primarily driven by strong mechanical strength, consistent capsule performance, and well-established acceptance across pharmaceutical manufacturing workflows. These capsules demonstrate reliable machinability on high-speed filling lines, ensuring low breakage rates and uniform dosing accuracy. Gelatin HPMC variants are widely used for both prescription drugs and over-the-counter formulations, particularly where moisture control and capsule integrity are critical. Their compatibility with a broad range of active pharmaceutical ingredients (APIs), including hygroscopic and sensitive compounds, further supports adoption. Rising global drug production volumes, increasing demand for oral solid dosage forms, and regulatory familiarity with gelatin-based capsule systems continue to reinforce demand. Additionally, pharmaceutical manufacturers favor these capsules due to predictable dissolution behavior and ease of regulatory approvals, positioning gelatin HPMC capsules as the leading product segment.

By Applicatiion, Pharmaceuticals Dominate Due to High Volume Drug Manufacturing and Regulatory Reliability

Pharmaceuticals are expected to dominate the global HPMC capsules market in 2026, capturing a revenue share of 60.0%. This dominance is driven by the extensive use of HPMC capsules in prescription drug formulations, generic medicines, and specialty therapeutics. Pharmaceutical manufacturers increasingly prefer HPMC capsules due to their stability across varying temperature and humidity conditions, making them suitable for global distribution. These capsules are widely used for immediate-release, modified-release, and combination drug formulations, supporting diverse therapeutic needs. Compatibility with automated capsule-filling equipment and standardized quality specifications enhances operational efficiency in large-scale production. Regulatory alignment with pharmacopeial standards further accelerates adoption across developed and emerging markets. While nutraceutical and cosmetic applications are growing steadily, pharmaceuticals remain the largest revenue contributor due to high manufacturing volumes, stringent quality requirements, and continuous demand for safe and reliable oral dosage delivery systems.

By End User, Hospitals Lead Due to High Prescription Dispensing and Institutional Drug Utilization

Hospitals are projected to dominate the global HPMC capsules market in 2026, accounting for a revenue share of 30.0%. This leadership is supported by high inpatient and outpatient volumes and consistent demand for capsule-based medications across multiple therapeutic departments. Hospitals routinely dispense oral solid dosage drugs for acute care, chronic disease management, and post-surgical recovery, driving steady consumption of HPMC capsules. Institutional pharmacies prioritize capsules that offer consistent quality, reliable dissolution, and compliance with regulatory and safety standards. The presence of integrated hospital pharmacies, strong procurement contracts, and centralized purchasing further strengthens demand. Hospitals also serve diverse patient populations, including geriatric and immunocompromised patients, where capsule safety and formulation stability are critical. Although retail and online pharmacies are expanding, hospitals remain the largest end-user segment due to continuous medication turnover, complex treatment protocols, and high prescription volumes.

Region-wise Insights

North America HPMC Capsules Market Trends

North America is expected to dominate the global HPMC capsules market with a value share of 47.3% in 2026, led primarily by the United States. The region benefits from a highly developed pharmaceutical manufacturing ecosystem, strong presence of branded and generic drug manufacturers, and advanced regulatory frameworks. Widespread adoption of HPMC capsules is supported by increasing demand for vegetarian and gelatin-free alternatives, particularly among health-conscious consumers and patients with dietary restrictions.

Pharmaceutical and nutraceutical companies in North America emphasize high-quality excipients, consistent capsule performance, and compliance with USP standards, driving sustained demand. Strong investment in research and development, along with high prescription drug consumption, further accelerates market growth. Additionally, favorable reimbursement systems and high healthcare expenditure support continuous innovation and product upgrades. The presence of leading capsule manufacturers, robust distribution networks, and growing demand for clean-label supplements ensures North America remains the most mature and revenue-dominant regional market.

Europe HPMC Capsules Market Trends

The Europe HPMC capsules market is expected to grow steadily, supported by well-established healthcare systems and stringent regulatory oversight across countries such as Germany, the U.K., France, Italy, and Spain. European pharmaceutical and nutraceutical manufacturers place strong emphasis on product quality, sustainability, and compliance with European Pharmacopoeia standards, driving consistent adoption of HPMC capsules. Rising demand for vegetarian, halal, and clean-label dosage forms aligns well with regional consumer preferences, particularly in dietary supplements and preventive healthcare products.

Aging populations across Europe are contributing to increased consumption of oral solid medications for chronic disease management. Public healthcare systems and private manufacturers are also investing in standardized dosage forms to improve supply chain efficiency and reduce formulation risks. Expansion of contract manufacturing organizations and growing focus on environmentally friendly excipients further support market growth. These factors position Europe as a stable, regulation-driven, and steadily expanding HPMC capsules market.

Asia Pacific HPMC Capsules Market Trends

The Asia Pacific HPMC capsules market is expected to register a relatively higher CAGR of around 7.3% between 2026 and 2033, driven by rapid pharmaceutical manufacturing expansion and increasing healthcare access. Countries such as China, India, Japan, South Korea, and Australia are witnessing strong growth in generic drug production, nutraceutical manufacturing, and export-oriented pharmaceutical operations. Rising awareness of vegetarian and non-animal-based dosage forms is accelerating demand for HPMC capsules, particularly in India and Southeast Asia. Expansion of contract manufacturing organizations and favorable government policies supporting domestic drug production further enhance market penetration.

Cost-effective manufacturing capabilities make the region attractive for both local consumption and global supply. Additionally, increasing healthcare expenditure, growing middle-class populations, and rising prevalence of chronic diseases are driving higher demand for oral solid dosage forms. These factors collectively position Asia Pacific as the fastest-growing regional market for HPMC capsules.

Market Competitive Landscape

The global HPMC capsules market is highly competitive, with strong participation from companies such as Lonza, ACG, Qualicaps, SUHEUNG, Sunil HealthCare Limited, and Roxlor. These players leverage extensive global distribution networks, strong brand equity, and diversified capsule and pharmaceutical excipient portfolios to address the rising demand for vegetarian, gelatin-free, and clean-label oral dosage solutions across pharmaceutical and nutraceutical applications.

Their offerings emphasize consistent capsule quality, dimensional stability, moisture resistance, high filling compatibility, and reliable dissolution performance, supporting use across a wide range of drug formulations and dietary supplements. Continuous product innovation, regulatory compliance (USP, EP, JP), material purity, scalability of manufacturing, and adherence to international pharmaceutical standards remain critical for sustaining competitive positioning in the global HPMC capsules market.

Key Industry Developments:

- In October 2025, ACG, a global leader in integrated solid-dosage solutions, announced a phased investment of USD 200 million to set up its first empty-capsule manufacturing facility in the United States, aiming to strengthen local production capabilities and meet growing North American demand.

- In January 2026, KornnacCaps, a leading empty capsule manufacturer, successfully shipped a batch of size 000 HPMC capsules to a major client in Egypt. This milestone highlights KornnacCaps’ growing international presence in the vegetable capsule segment and establishes a strong foundation for the company’s further expansion across the Middle East and African markets.

- In December 2024, Shandong Head Group, a manufacturer of cellulose ethers and HPMC empty capsules, announced plans to invest USD 80 million in a new US-based facility to better serve North American customers. The facility is expected to increase production capacity by over 20 billion HPMC capsules annually. Head Group, which operates a vertically integrated HPMC capsule supply chain, currently produces more than 30 billion capsules per year under its Caps-Healsee brand.

Companies Covered in HPMC Capsules Market

- Lonza

- ACG

- Qualicaps

- SUHEUNG

- Sunil HealthCare Limited.

- Roxlor

- NATURAL CAPSULES LIMITED

- Shanxi Guangsheng Medicinal Capsules Co., Ltd.

- Capscanada Corporation

- Mitsubishi Chemical Group Corporation.

- HealthCaps India

- Bright Pharma Caps

- DAH FENG CAPSULE INDUSTRY CO., LTD.

- Meihua Holdings Group Co., Ltd

Frequently Asked Questions

The global HPMC capsules market is projected to be valued at US$ 2.4 Bn in 2026.

Increasing consumer preference for plant-based, vegetarian/vegan and clean-label products, coupled with strong expansion of pharmaceutical and nutraceutical industries and sustainability focus, is driving HPMC capsule demand globally.

The global HPMC capsules market is poised to witness a CAGR of 5.4% between 2026 and 2033.

Expansion into emerging markets with growing healthcare sectors presents a significant opportunity for HPMC capsules.

Lonza, ACG, Qualicaps, SUHEUNG, Sunil HealthCare Limited, and Roxlor are some of the key players in the body HPMC capsules market.