- Pharmaceuticals

- Crohn’s Disease Treatment Market

Crohn’s Disease Treatment Market Size, Share, Growth, and Regional Forecast, 2026 - 2033

Crohn’s Disease Treatment Market by Drug Class (TNF-alpha Inhibitors, Aminosalicylic Acid, Calcineurin Inhibitors, Corticosteroids, Interleukin (IL) Inhibitors, Others), Route of Administration, Distribution Channel, and Regional Analysis from 2026 - 2033

Crohn’s Disease Treatment Market Share and Trends Analysis

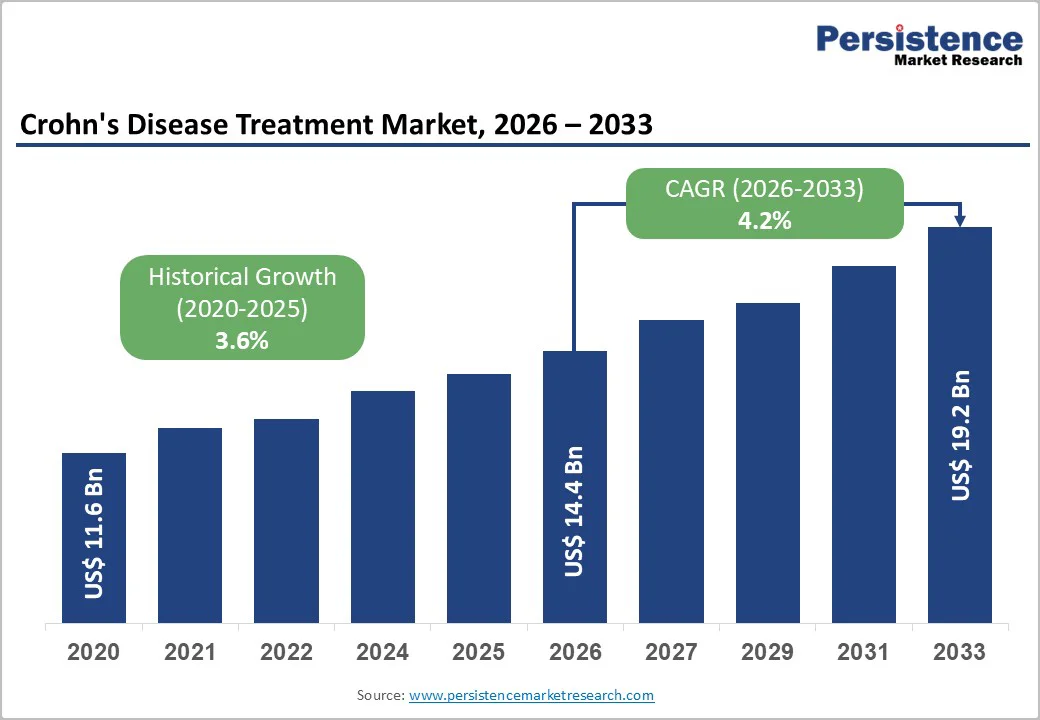

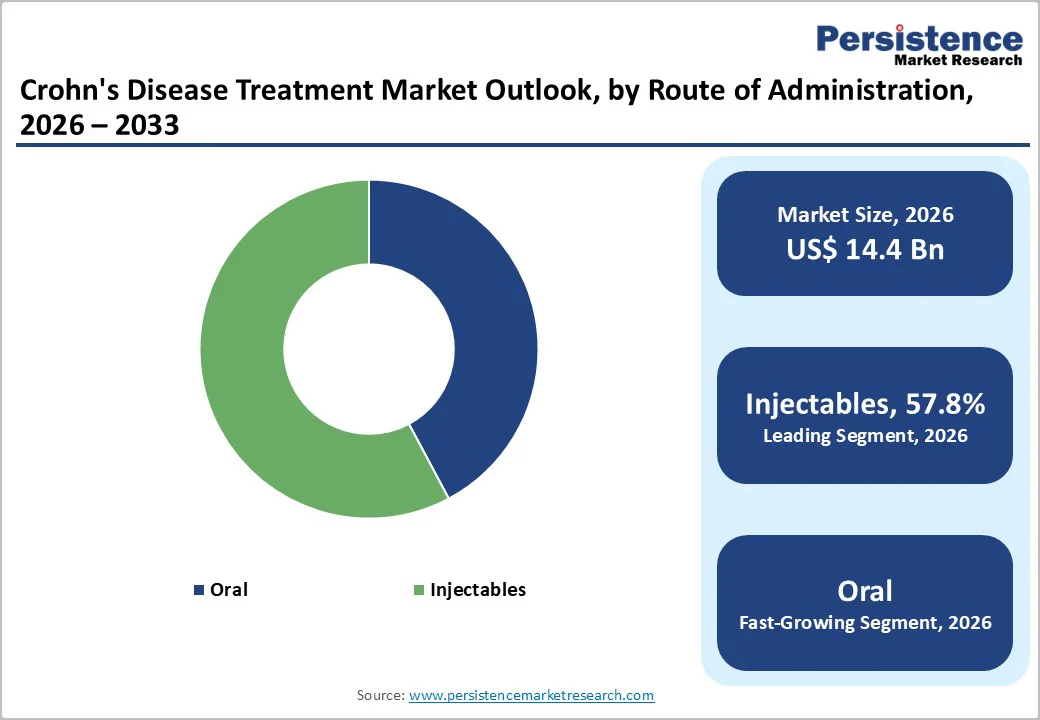

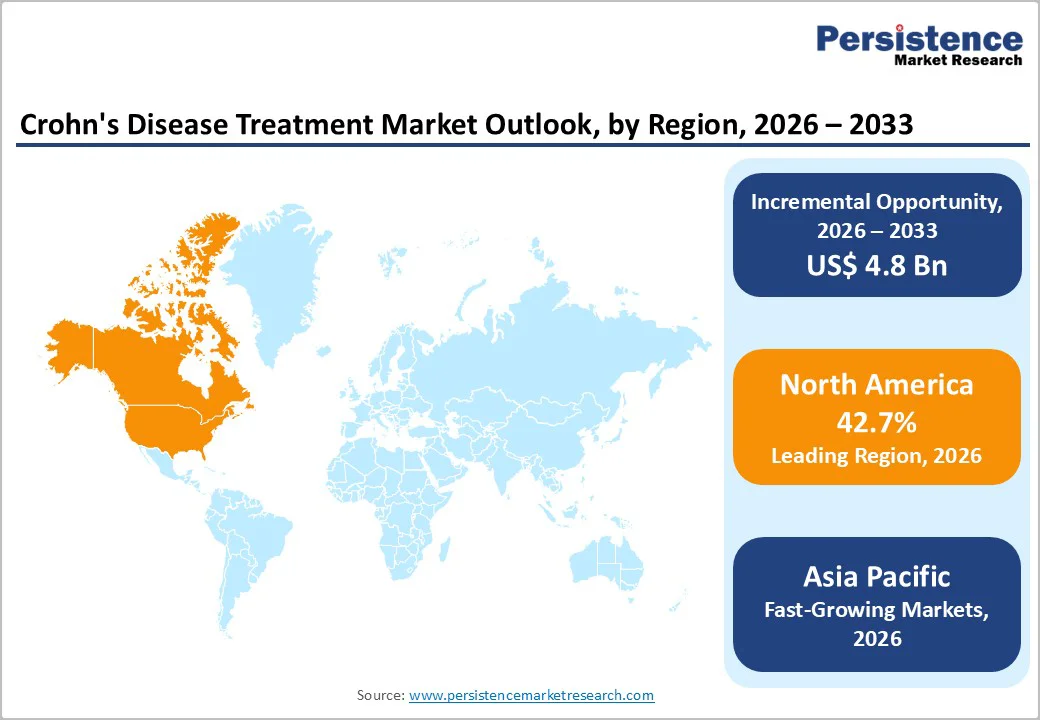

The global Crohn’s disease treatment market size is estimated to reach US$ 14.4 Billion in 2026 and is projected to reach US$ 19.2 Billion by 2033, growing at a CAGR of 4.2% between 2026 and 2033. The rise in disease prevalence, increasing diagnosis rates, and rapid uptake of advanced biologics and biosimilars has triggered the need for crohn’s diagnosis.

As healthcare systems shift toward targeted, long-term disease management, demand for IL-23 inhibitors, anti-TNF therapies, and cost-efficient biosimilar options continues to expand. Ongoing regulatory approvals, strong R&D pipelines, and strategic collaborations among biopharmaceutical companies further accelerate market growth. At the same time, greater focus on pediatric care, maintenance therapy, and real-world treatment optimization is reshaping clinical practice and reinforcing sustained investment in innovative Crohn’s disease therapies globally.

Key Industry Highlights:

- Leading Region: North America dominates the global market with 42.7%, driven by strong biologic adoption, early access to FDA-approved therapies, advanced healthcare systems, and high treatment affordability.

- Fastest-Growing Region: Asia Pacific market is expected to grow rapidly with a CAGR of 5.2% in forecast period, fueled by expanding biosimilar availability, improving diagnostic capabilities, rising healthcare investment, and growing awareness of inflammatory bowel diseases.

- Leading Drug Class: TNF-alpha inhibitors lead with 32.5% share, supported by proven efficacy, established clinical use, broad reimbursement coverage, and strong real-world outcomes in moderate to severe Crohn’s disease.

- Leading Route of Administration: Injectables remains dominant with 57.8%, driven by widespread biologic usage, reliable absorption, rapid symptom control, and increasing preference for subcutaneous self-administration.

- Leading Distribution Channel: Hospital pharmacies lead with 64.4% share, due to centralized biologic dispensing, specialist-driven treatment initiation, infusion-based therapies, and coordinated patient monitoring within hospital settings.

- Growing clinical trials and regulatory submissions for pediatric Crohn’s disease are improving early treatment access and reinforcing demand for safer, targeted biologic options.

- Growing dependence on Real-World Evidence (RWE) for treatment decisions, payer negotiations, and regulatory support enhances confidence in biologic performance and long-term safety.

- Strengthening collaborations between specialty hospitals and biopharma companies are supporting infusion service expansion, clinical trial enrolment, and biologic therapy adoption.

| Key Insights | Details |

|---|---|

|

Global Crohn’s Disease Treatment Market Size (2026E) |

US$ 14.4 Billion |

|

Market Value Forecast (2033F) |

US$ 19.2 Billion |

|

Projected Growth (CAGR 2026 to 2033) |

4.2% |

|

Historical Market Growth (CAGR 2020 to 2025) |

3.6% |

Market Dynamics

Driver - Market Expansion Through Advancing Technologies, Rising Demand, Clinical Adoption, and Improved Healthcare Infrastructure Growth

The global Crohn’s disease treatment market continues to expand as inflammatory bowel disease (IBD) affects nearly 10 million people worldwide, including both ulcerative colitis (UC) and Crohn’s disease. These chronic autoimmune conditions trigger persistent inflammation across the digestive tract, and Crohn’s disease in particular is marked by alternating flare-ups and remission, often impacting any segment of the gastrointestinal tract.

This rising prevalence has intensified demand for anti-inflammatory and immunomodulatory therapies. Clinicians routinely rely on agents such as Prednisone, Budesonide, and Budesonide-MMX to manage inflammation, bacterial complications, and gastrointestinal symptoms such as diarrhoea and persistent abdominal pain. Meanwhile, improved retail and online pharmacy channels-offering wide product availability and competitive discounts-support greater access to these therapies, reinforcing segment growth.

Innovative biologics are further shaping market momentum. In January 2025, Eli Lilly received FDA approval for Omvoh® (mirikizumab-mrkz) for moderately to severely active Crohn’s disease in adults, expanding on its October 2023 UC approval. With long-term Phase 3 results, global regulatory submissions, and strong efficacy signals from the VIVID-2 study presented at ACG 2024, Omvoh exemplifies the surge in advanced treatment options driving market expansion.

Restraints - High Costs, Limited Access, Regulatory Hurdles, And Operational Constraints

Despite strong therapeutic progress, several barriers continue to restrain the global Crohn’s disease treatment landscape. One of the most significant challenges is the high cost of advanced biologics and small-molecule therapies, which remain out of reach for a considerable proportion of patients, especially in low- and middle-income regions. Even where insurance coverage exists, frequent dose escalation, long-term usage, and combination regimens substantially increase financial burden.

Another limitation stems from clinical heterogeneity. Crohn’s disease presents differently across patients, with varying severity, anatomical involvement, and treatment response. This variability can delay diagnosis, complicate therapeutic selection, and often leads to trial-and-error approaches that lengthen the treatment pathway. Resistance or loss of response to biologics over time also remains a persistent issue, forcing patients to cycle through multiple therapies with inconsistent outcomes.

Regulatory complexity adds further constraints. Emerging therapies-particularly immunomodulators, novel biologics, and microbiome-targeted agents-face lengthy approval timelines and stringent post-market surveillance requirements. Additionally, limited specialist availability in developing regions and uneven access to colonoscopy, endoscopy, and biomarker-based diagnostics hinder timely management. Collectively, these structural and economic challenges temper the market’s growth potential despite rising global disease prevalence.

Opportunity - Emerging Growth Prospects Through Innovation, Unmet Needs, Strategic Collaborations, And Expanding Healthcare Penetration Worldwide

The evolving scientific understanding of Crohn’s disease is opening a new wave of market opportunities, especially as researchers explore multi-pathway targeting and microbiome-driven therapies. A major breakthrough began in 2022, when Johnson & Johnson reported promising outcomes from a novel combination strategy pairing a TNF-pathway rheumatoid arthritis therapy with an IL-23 inhibitor for moderate to severe UC.

This paved the way for further innovation, culminating in 2024/2025 FDA approval of a dual-acting monoclonal antibody for both UC and Crohn’s disease. Clinical findings showed substantial symptom improvement and mucosal healing on colonoscopy and histology, strengthening expectations for broader global adoption. The company’s 2025 focus on mucosal immunology further signals a shift toward highly targeted, next-generation IBD treatments, offering major commercial potential as precision medicine gains traction.

Parallel innovation from emerging players is expanding opportunities even further. In July 2024, RedHill Biopharma announced positive Phase III results for RHB-104, a therapy aimed at eradicating Mycobacterium avium ssp. paratuberculosis, suspected to contribute to Crohn’s pathology. With higher remission rates at 26 and 52 weeks compared to placebo in a 331-patient trial, the findings highlight strong prospects for microbiome-modifying therapies—an area positioned to redefine future market expansion.

Category-wise Analysis

By Drug Class: TNF-alpha Inhibitors Dominate Due to Proven Efficacy and Broad Clinical Adoption

TNF-alpha inhibitors are expected to account for 32.5% of the global Crohn’s disease treatment market by 2026, supported by strong real-world outcomes, rapid symptom control, and established physician preference. Their ability to reduce inflammation, induce remission, and delay disease progression has positioned them as first-line biologics for moderate to severe cases. Widespread reimbursement coverage and long-term clinical evidence further reinforce their market hold. Continued development of optimized formulations and expanded regulatory approvals is expected to sustain the dominance of TNF-alpha inhibitors over the forecast period.

By Route of Administration: Injectables Lead Owing to High Bioavailability and Strong Biologic Uptake

Injectables are projected to command 57.8% of the global Crohn’s disease treatment market in 2026, primarily driven by the extensive use of biologics and targeted immunotherapies that rely on parenteral delivery for consistent and predictable absorption. Their superior bioavailability supports faster therapeutic action, making them preferred in moderate to severe disease. Increasing approvals of subcutaneous formulations, patient familiarity with self-injection devices, and hospital-based infusion therapies further expand uptake. As the biologic pipeline grows and advanced long-acting injectables enter the market, this route is expected to retain clear leadership.

By Distribution Channel: Hospital Pharmacies Lead Owing to Higher Biologic Utilization and Specialist-Driven Care

Hospital pharmacies are projected to represent 64.4% of the global Crohn’s disease treatment market in 2026, supported by the concentration of advanced biologic therapies within hospital settings. Complex treatments such as infusions, combination regimens, and newly approved targeted agents require specialist supervision, ensuring hospital-based dispensing remains dominant. These pharmacies also manage treatment initiation, monitoring, and reimbursement coordination, strengthening their role in patient care pathways. With rising adoption of high-cost biologics and expansion of gastroenterology centres, hospitals are expected to maintain their position as the primary distribution hub for Crohn’s disease medications.

Regional Insights

North America Crohn’s Disease Treatment Market Trends

North America is projected to command 42.7% of the global Crohn’s disease treatment market by 2026, driven by rapid biologics adoption, accelerated regulatory activity, and strong commercial readiness for both innovative and biosimilar therapies. The region continues to benefit from a steady inflow of product approvals that expand treatment access and diversify clinician choices. In June 2023, the FDA cleared ZYMFENTRA™ (infliximab-dyyb) for maintenance therapy in adults with moderately to severely active UC and Crohn’s disease after prior IV infliximab use, following robust pivotal data from the LIBERTY-UC and LIBERTY-CD trials.

The competitive landscape strengthened further with the February 2025 U.S. launch of YESINTEK™ (ustekinumab-kfce), one of the first approved biosimilars to Stelara®, broadening cost-effective options across Crohn’s disease, UC, plaque psoriasis, and psoriatic arthritis. Momentum continued in June 2025, when Johnson & Johnson submitted a supplemental BLA seeking to expand STELARA® approval to pediatric Crohn’s disease based on UNITI-Jr study results. Additional support came from the April 2024 FDA approval of SELARSDI (ustekinumab-aekn) under the Teva–Alvotech partnership, reinforcing the region’s readiness for ustekinumab biosimilar integration. Collectively, these developments strengthen North America’s position as the leading growth engine for Crohn’s disease therapeutics.

Europe Crohn’s Disease Treatment Market Trends

Europe is expected to capture 28.4% of the global Crohn’s disease treatment market by 2026, supported by strong research collaboration networks, early adoption of data-driven clinical models, and multiple region-led initiatives targeting improved IBD management. Organizations such as the European Crohn’s and Colitis Organisation (ECCO) continue to advance scientific knowledge through active research partnerships, enabling faster translation of insights into therapeutic strategies.

A major accelerator for the region emerged in October 2025, when the Critical Path Institute (C-Path) launched the Critical Path Disease Modeling Coalition (CP-DMC) focused on pediatric inflammatory bowel disease. Developed with leading academic partners from ESPGHAN and backed by the Crohn’s & Colitis Foundation, the initiative aims to create regulatory-grade progression models that can streamline pediatric Crohn’s drug development across Europe.

Further momentum comes from the May 2025 INTERCEPT project under the Innovative Health Initiative (IHI). By validating biomarker panels and building a blood-based risk scoring system to predict Crohn’s development among 10,000 first-degree relatives, INTERCEPT introduces one of the most ambitious prevention-oriented frameworks in the field. With collaboration spanning Europe, North America, and South Korea, the program positions Europe as a frontrunner in early detection, risk stratification, and long-term disease prevention—key drivers for sustained market expansion.

Asia Pacific Crohn’s Disease Treatment Market Trends

The Asia Pacific region is set for accelerated growth, projected to expand at a 5.2% CAGR over the forecast period, propelled by rising biologic penetration, supportive regulatory pathways, and a rapid increase in biosimilar availability. Countries across the region are actively adopting cost-efficient therapeutic alternatives to meet growing demand for Crohn’s disease management, particularly as diagnosis rates improve and healthcare systems strengthen their focus on chronic autoimmune disorders.

A notable development occurred in May 2025, when Biocon Biologics Ltd. (BBL), in partnership with Yoshindo Inc., launched Ustekinumab BS Subcutaneous Injection [YD] in Japan. As a biosimilar to the reference product Stelara® (ustekinumab), the therapy aims to expand access to biologic treatment by offering a more affordable option without compromising clinical standards. Manufactured by Biocon Biologics and commercialized by Yoshindo, the launch underscores Japan’s rising role in the region’s biosimilar ecosystem.

With the growing regulatory support for biologics, increasing investments in local manufacturing, and strong partnerships between global innovators and regional pharmaceutical players, Asia Pacific is becoming one of the most dynamic markets for Crohn’s disease therapies. The steady introduction of high-quality biosimilars is expected to enhance affordability and significantly widen patient reach, solidifying the region’s upward market trajectory.

Competitive Landscape

The competitive landscape for Crohn’s disease treatment is intensifying as innovative biologics, IL-23 inhibitors, and a growing wave of ustekinumab and infliximab biosimilars enter the market. Companies are focusing on expanded indications, pediatric approvals, and long-acting maintenance formulations, while partnerships and commercialization alliances accelerate product launches and enhance pricing competitiveness across major regions.

Key Industry Developments:

- In May 2025, Bio-Thera Solutions and Hikma Pharmaceuticals announced FDA approval of STARJEMZA® (ustekinumab-hmny), a Stelara® biosimilar, marking Bio-Thera’s third U.S. approval and expanding treatment options for immune-mediated conditions.

- In December 2024, Celltrion announced FDA approval of STEQEYMA® (ustekinumab-stba), a Stelara® biosimilar for SC or IV use in adults and pediatric patients across plaque psoriasis, psoriatic arthritis, Crohn’s disease, and ulcerative colitis.

Companies Covered in Crohn’s Disease Treatment Market

- AbbVie Inc.

- Eli Lilly and Company

- Johnson & Johnson

- Pfizer Inc.

- CELLTRION INC.

- Amgen Inc.

- Organon group of companies

- Biocon Limited

- Fresenius Kabi USA, LLC

- Sandoz Inc.

- Hikma Pharmaceuticals PLC

- Teva Pharmaceutical Industries Ltd.

- Boehringer Ingelheim Pharmaceuticals, Inc.

Frequently Asked Questions

The global Crohn’s disease treatment market is projected to be valued at US$ 14.4 Billion in 2026.

Rising disease prevalence, increasing biologic adoption, and growing demand for targeted, long-term disease-modifying therapies drive market growth.

The global market is poised to witness a CAGR of 4.2% between 2026 and 2033.

Expanding use of advanced biologics and small molecules, personalized therapy approaches, and broader access in emerging markets present major growth opportunities.

Major players in the global are AbbVie Inc., Eli Lilly and Company, Johnson & Johnson, Pfizer Inc., CELLTRION INC., and others.