- Processed Food

- Canned Tuna Market

Canned Tuna Market Size, Trends, Share, Growth, and Regional Forecast, 2026 to 2033

Canned Tuna Market by Product Type (Light Tuna, White Tuna, Others), by Form (Solid/Chunk, Flakes, Shredded), End-user (Hypermarkets/Supermarkets, Convenience Stores, Specialty Stores, Online Retail, Others), and Regional Analysis, 2026 - 2033

Canned Tuna Market Share and Trends Analysis

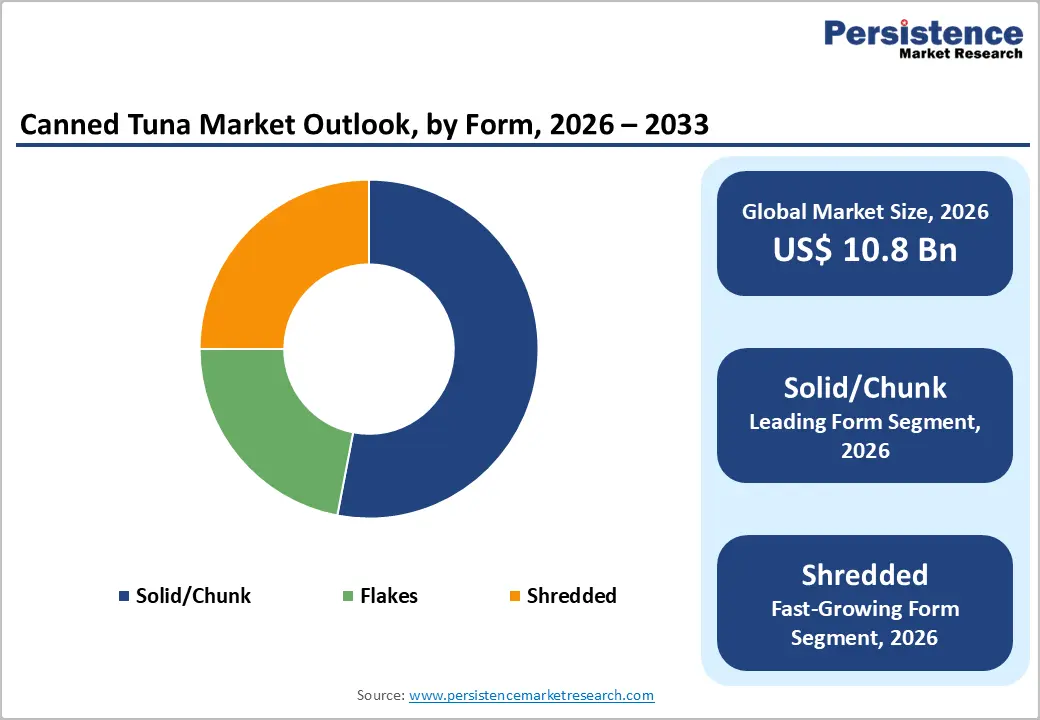

The global canned tuna market size is expected to be valued at US$ 10.8 billion in 2026 and projected to reach US$ 15.1 billion by 2033, growing at a CAGR of 4.9% between 2026 and 2033.

Canned tuna continues to balance everyday affordability with evolving expectations around sustainability, flavor, and convenience. As consumers demand protein that fits modern lifestyles without compromising ethics or taste, the category is steadily shifting from a basic pantry staple toward differentiated, value-driven offerings.

Key Industry Highlights:

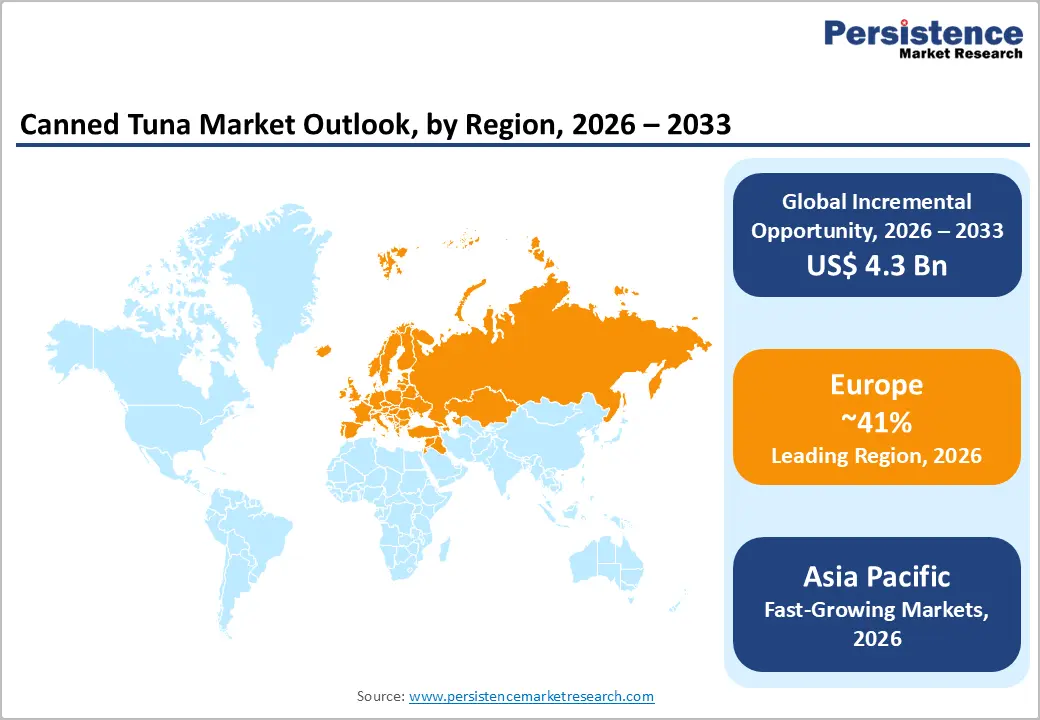

- Leading Region: Europe, holding approximately 41% market share, supported by strong seafood consumption traditions, deep retail penetration, and growing emphasis on responsibly sourced and premium tuna products.

- Fastest-Growing Region: Asia Pacific, expanding at an estimated CAGR of 7.4%, driven by urbanization, rising protein awareness, modern retail growth, and increasing adoption among younger, convenience-focused consumers.

- Dominant Product Type: Light tuna, accounting for around 68% market share, favored for its mild flavor, affordability, and versatility across everyday meals, ready foods, and foodservice applications.

- Fastest-Growing Format: Shredded tuna, gaining momentum due to ease of use, suitability for portion-controlled packs, and strong fit with ready-to-eat meals, wraps, salads, and flavored variants.

- Market Drivers: Rising demand for convenient, nutrient-dense protein sources, supported by busy lifestyles, fitness-oriented diets, shelf stability, and versatility across multiple meal occasions.

- Opportunities: Premiumization through sustainability certifications, traceable sourcing, and flavored tuna variants that appeal to ethically driven, taste-seeking, and younger consumers willing to trade up.

- Key Developments: In December 2025, ALDI Australia transitioned its full canned tuna range to MSC-certified sourcing; in November 2025, Dongwon F&B expanded its canned tuna presence into the U.S. market via Amazon.

| Key Insights | Details |

|---|---|

| Canned Tuna Market Size (2026E) | US$ 10.8 Bn |

| Market Value Forecast (2033F) | US$ 15.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.1% |

Market Dynamics

Driver - Rising Demand for Convenient, Nutrient-Dense Protein Sources

Fast-paced lifestyles are reshaping seafood consumption, placing canned tuna at the intersection of speed, nutrition, and affordability. The product delivers high-quality protein, essential omega-3 fatty acids, and micronutrients in a shelf-stable, no-preparation format. This balance appeals to urban consumers, fitness-focused buyers, and households seeking reliable meal components that require no refrigeration or cooking, fitting busy modern daily routines globally.

Beyond convenience, canned tuna aligns with protein-forward dietary trends emphasizing portion control and functional nutrition. Single-serve cans support calorie awareness, while versatility across salads, sandwiches, and ready meals strengthens everyday usage. As consumers prioritize foods that combine nourishment with ease, canned tuna continues to gain relevance as a dependable protein source across income groups, worldwide markets, retail channels, and diverse consumer segments.

Restraints - Sustainability Scrutiny and Overfishing Concerns

Heightened environmental awareness is reshaping perceptions of canned tuna, with sustainability questions moving to the forefront of purchasing decisions. Concerns about depleted fish stocks, bycatch impacts, and damage to ocean ecosystems affect consumer trust. Advocacy groups, retailers, and regulators increasingly scrutinize sourcing practices, creating pressure on producers to demonstrate responsible fishing methods and transparent supply chains across global tuna markets.

These sustainability pressures can slow expansion by increasing compliance costs and limiting raw material availability. Stricter catch limits and monitoring requirements reduce supply flexibility, affecting pricing stability. Smaller brands may struggle to absorb certification expenses or adapt sourcing quickly. As scrutiny intensifies, reputational risk becomes a real constraint, influencing partnerships, shelf placement, and long-term brand credibility in the competitive global canned tuna market.

Opportunity - Premiumization Through Sustainable Certifications and Flavored Variants

An evolution toward premium offerings is opening new growth avenues in the canned tuna market. Consumers increasingly associate value with sustainability credentials, clean labels, and differentiated taste experiences. Certified sustainable tuna, traceable sourcing stories, and responsibly managed fisheries allow brands to command higher price points while appealing to ethically driven buyers seeking quality beyond basic nutrition and lifestyle alignment, flavor exploration, and trust.

Flavor innovation further strengthens premiumization by elevating canned tuna from a pantry staple to a culinary product. Infusions with herbs, spices, oils, and regional seasonings attract adventurous consumers and younger demographics. For startups, combining bold flavors with verified sustainability creates differentiation, faster shelf recognition, and opportunities to compete against established brands through storytelling and niche positioning in global retail environments.

Category-wise Analysis

By Product Type Insights

Light tuna holds approx. 68% market share as of 2025, reflecting its strong alignment with everyday consumption habits. Its mild flavor, softer texture, and lighter color make it adaptable across salads, sandwiches, ready meals, and quick home recipes. Light tuna varieties, typically sourced from skipjack and yellowfin species, are widely available and priced competitively, supporting frequent purchases across mass retail channels. The product’s consistent taste profile and reliable shelf life further reinforce its preference among households, foodservice operators, and institutional buyers seeking dependable protein options.

White tuna, commonly associated with albacore, occupies a smaller yet premium-oriented segment. It attracts consumers who value a firmer texture and richer flavor, and is often positioned for gourmet applications and higher price tiers.

By Form Insights

Shredded tuna is projected to grow at a CAGR of 7.1% during the forecast period in the global canned tuna market, driven by shifting meal preparation habits. The shredded format offers immediate usability, eliminating the need for additional processing in kitchens. Its fine texture blends easily into wraps, pasta, spreads, and ready-to-eat meals, appealing to time-conscious consumers and foodservice operators. Growth is further supported by its suitability for portion-controlled packaging and flavored variants, which enhance convenience and taste appeal. Manufacturers favor shredded tuna for its versatility across product lines, including salads, meal kits, and snack packs. As demand rises for flexible, quick-serve protein solutions, shredded tuna continues gaining momentum across retail and institutional channels.

Region-wise Insights

Europe Canned Tuna Market Trends

Europe holds approximately 41% market share in the global canned tuna market, shaped by long-standing seafood consumption habits and strong retail penetration. Demand is influenced by preference for convenient protein sources aligned with health-conscious lifestyles. Southern European countries emphasize culinary integration, while Northern markets prioritize sustainability and transparency. Packaging innovation and private-label growth continue to reshape competitive dynamics across the region.

Germany and the UK show rising interest in responsibly sourced and flavored tuna options, reflecting ethical and taste-driven purchasing. France emphasizes premium positioning and culinary versatility, whereas Spain and Italy benefit from deep-rooted tuna traditions and high per capita consumption. Russia shows steady demand through shelf-stable value products, supporting consistent volume growth across diverse consumer segments.

Asia Pacific Canned Tuna Market Trends

Asia Pacific canned tuna market is expected to grow at a CAGR of 7.4%, supported by expanding urban populations and evolving dietary preferences. Rising awareness of protein intake and affordability, along with modern retail and e-commerce, drive adoption across emerging economies. The region benefits from proximity to major tuna fishing zones, supporting processing and export-oriented growth.

In India, canned tuna is gaining traction among young professionals and fitness-focused consumers. China shows increasing demand through online grocery platforms and ready-meal applications. Japan maintains steady consumption rooted in seafood culture, with emphasis on quality and origin. South Korea sees growth through flavored, single-serve formats aligned with convenience-driven lifestyles.

Market Competitive Landscape

The global canned tuna market displays a moderately consolidated structure, with established multinational brands holding strong shelf presence alongside regional players. Leading companies focus on capacity expansion, supply chain optimization, and consistent quality to protect market share. Investments in modern processing facilities and efficient logistics help meet rising global demand while managing cost pressures and regulatory compliance.

Startups are entering with differentiated value propositions centered on clean labeling, traceability, and sustainability certifications. Product innovation includes flavored varieties, portion-controlled packs, and premium offerings. Collaborations with fisheries, retailers, and certification bodies support credibility. Growing consumer awareness, the expansion of online retail, and evolving government regulations continue to shape competitive strategies across mature and emerging markets.

Key Developments:

- In December 2025, ALDI Australia committed to sustainability by transitioning its entire canned tuna range to Marine Stewardship Council (MSC) certification, reinforcing responsible sourcing and ocean-friendly practices.

- In November 2025, Dongwon F&B, South Korea’s top canned food producer, launched its popular canned tuna range on Amazon.com, signaling a strategic expansion into the US market.

- In June 2025, Liancheng Ocean Fisheries Group announced plans to construct a new tuna processing plant, aiming to capitalize on rising domestic demand and expand its production capacity.

- In February 2025, EROSKI introduced Spain’s first own-brand MSC-certified canned light tuna, emphasizing sustainable sourcing and responsible seafood practices.

Companies Covered in Canned Tuna Market

- Thai Union Group PCL

- Dongwon Industries Co., Ltd.

- Orkla ASA

- Bolton Group

- Tri Marine Group

- Kyokuyo Co., Ltd.

- PT. Aneka Tuna Indonesia

- Nauterra

- Aldi

- Frinsa Group

- Bumble Bee Foods, LLC

- Crown Prince, Inc

- Liancheng Ocean Fisheries Group

- Others

Frequently Asked Questions

The global tuna market is likely to be valued at US$ 10.8 billion in 2026, growing from US$ 8.5 billion in 2020.

Rising Demand for Convenient, Nutrient-Dense Protein Sources drives the global canned tuna market.

Europe, at 41% share (2025) dominates the global market.

Premiumization Through Sustainable Certifications and Flavored Variants is key opportunity for key players in the market.

Thai Union Group PCL, Bumble Bee Foods, LLC, Dongwon Industries, StarKist via sustainability, distribution scale.