- Processed Food

- Canned Sausages Market

Canned Sausages Market Size, Share, and Growth Forecast, 2025 - 2032

Canned Sausages Market By Source (Poultry, Beef, Pork, Seafood), Packaging (Metal Cans, Glass Jars), Distribution Channel (Supermarkets/Hypermarkets, Specialty Stores, Online Retail), and Regional Analysis for 2025 - 2032

Canned Sausages Market Size and Trends Analysis

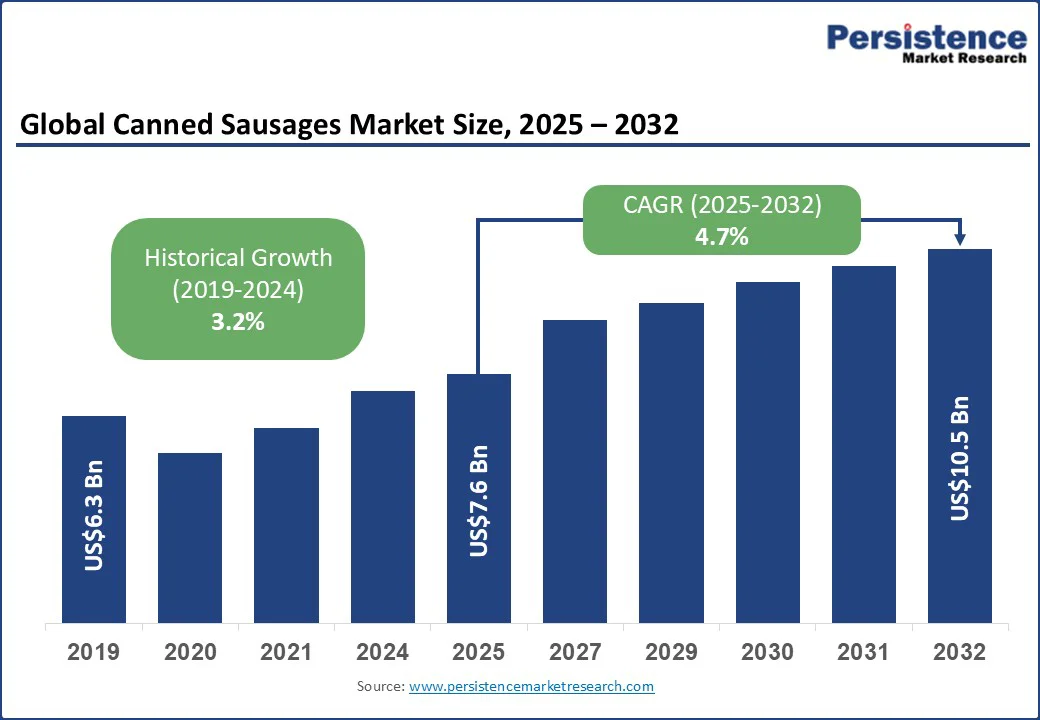

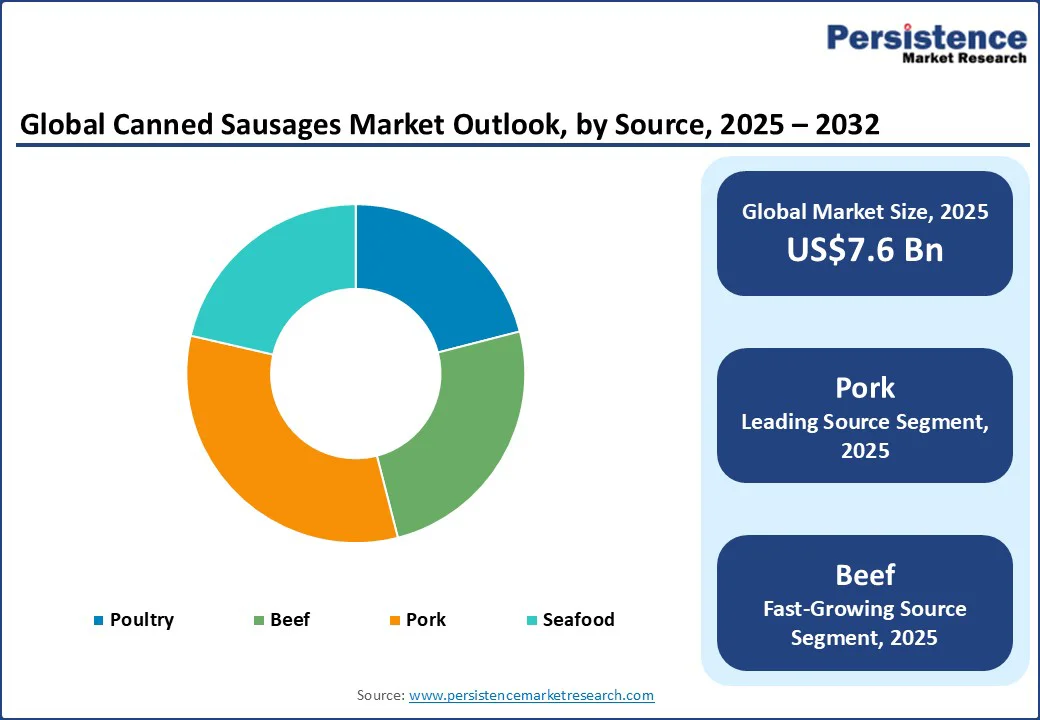

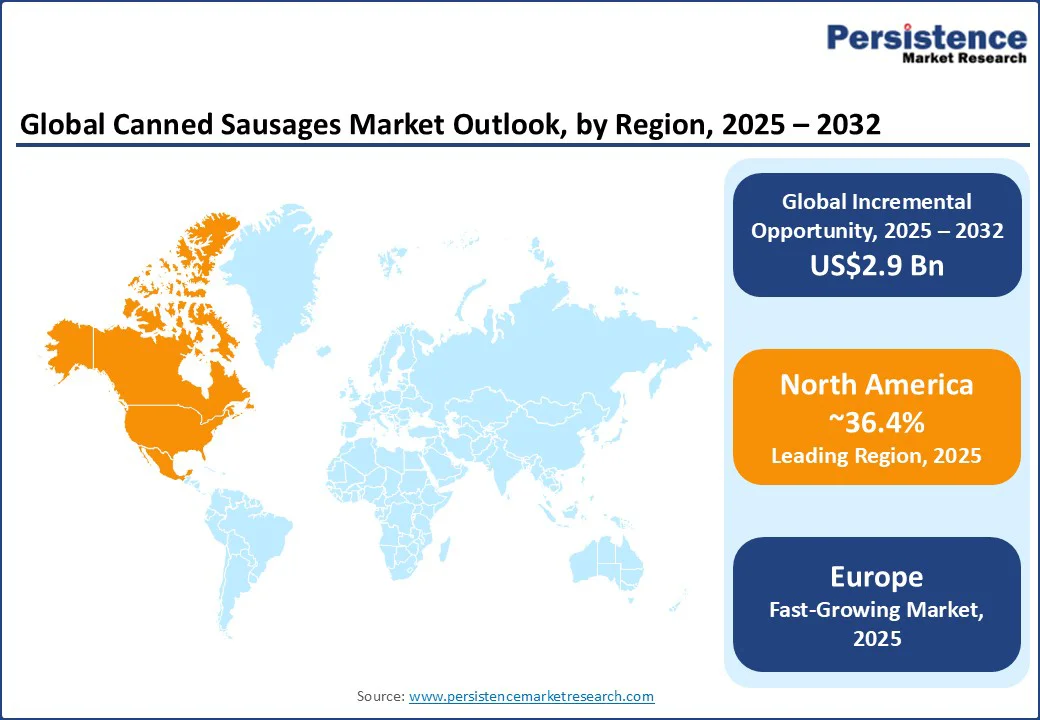

The canned sausages market size is likely to be valued at US$7.6 Bn in 2025 and is estimated to reach US$10.5 Bn in 2032, growing at a CAGR of 4.7% during the forecast period 2025 - 2032, driven by the rising demand for single-serve packs among young consumers and the launch of healthy variants such as those that are low-sodium or chicken-based options.

Marketing strategies highlight convenience and trust, with brands such as Meica in Germany promoting glass-jar sausages as preservative-free.

Key Industry Highlights

- Leading Source: Pork sausages hold nearly 32.6% share in 2025, as they deliver familiar taste and versatility for regional flavors.

- Dominant Packaging: Metal cans, approximately 45.3% of the canned sausages market share in 2025, owing to their ability to ensure long shelf life and safe transport.

- Key Distribution Channel: Supermarkets/hypermarkets recorded about 39.6% of the market share in 2025, as they provide wide assortments, multipack discounts, and strong visibility.

- Leading Region: North America, with about 36.4% share in 2025, due to the steady demand for affordable proteins in discount and convenience channels.

- Fastest-growing Region: Europe, around 3.4% CAGR through 2032, backed by deep cultural integration of canned sausages in Germany and Poland.

- New Product Launch: Heinz recently partnered with Pilgrim’s Food Masters’ sausage brand Richmond to release new Heinz Beanz and Spaghetti with sausages.

| Key Insights | Details |

|---|---|

| Canned Sausages Market Size (2025E) | US$7.6 Bn |

| Market Value Forecast (2032F) | US$10.5 Bn |

| Projected Growth (CAGR 2025 to 2032) | 4.7% |

| Historical Market Growth (CAGR 2019 to 2024) | 3.2% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Rising Popularity of Ready-to-Eat Single Portions among Young Shoppers

Young consumers in urban areas are increasingly turning to canned sausages in small, single-serve packs for convenience. With busy lifestyles, many prefer compact cans that fit into lunchboxes, quick office meals, or late-night snacks, minimizing food waste.

For example, Japan-based brands have launched mini canned sausages aimed at students and working professionals who live alone, making portion control and affordability key selling points. This shift from bulk family packs to on-the-go packaging is transforming how producers market canned sausages, focusing on portability and everyday accessibility rather than traditional household stockpiling.

Shelf-stable Protein Food Gaining Impetus among Health-conscious Consumers

Fitness-focused consumers are increasingly open to canned sausages as a reliable protein source that is both affordable and shelf-stable. While fresh meat requires refrigeration and quick consumption, canned sausages are finding a place in gym-goers’ and outdoor enthusiasts’ diets as an emergency or travel-friendly protein fix.

Recent launches of chicken- and turkey-based canned sausages with reduced fat and sodium levels show how producers are complying with health trends without sacrificing the convenience of a ready-to-eat format. This balance of nutrition and practicality appeals strongly to consumers looking to maintain high-protein diets on tight schedules.

Novel Processing Extending Shelf Life without Compromising Quality

Modern preservation techniques have allowed canned sausages to shed their image of being overly processed or dated. Developments in vacuum sealing, retort packaging, and flavor retention now ensure that canned sausages maintain a fresh taste and better texture for longer durations.

Europe-based producers such as Tulip Foods have started introducing preservative-free recipes that still carry a long shelf life, reassuring consumers about safety and quality. These developments not only improve trust in the product but also make canned sausages more adaptable to markets that prioritize clean-label foods. As a result, storage stability is now a competitive advantage beyond just emergency use.

Health-conscious Buying Habits Influenced by Additives and Salt Content

One of the main restraints for canned sausages is the rising scrutiny over high sodium levels and preservatives. With increasing awareness of heart health, obesity, and processed meat risks, several consumers are actively reducing canned meat purchases in favor of fresh or minimally processed options. For instance, U.S. diet surveys have revealed a decline in processed meat intake among young buyers who associate additives with long-term health issues.

Even when companies launch reduced-salt or preservative-free versions, skepticism lingers, as the canned format itself carries the stigma of being unhealthy. This perception limits the ability of the category to attract health-conscious households, despite product development efforts.

Waste Challenges Linked to Non-biodegradable Packaging Materials

Sustainability is a key barrier slowing the growth of canned sausages, as metal cans are energy-intensive to produce and often end up in landfills. In regions such as Western Europe, where eco-consciousness propels consumer decisions, brands face pressure to demonstrate circular packaging practices.

For example, Germany-based retailers have begun prioritizing suppliers who can provide recyclable or lightweight cans, while some consumers are shifting to alternatives such as vacuum-sealed pouches that generate less waste. The challenge is that metal remains essential for long shelf life, creating a conflict between convenience and sustainability expectations. Unless companies invest in green packaging, environmental concerns will continue to restrain demand in eco-sensitive markets.

Military Rations and Emergency Relief Programs

Canned sausages have strong potential in government-led procurement for defense and disaster management. Their long shelf life, portability, and protein density make them ideal for military rations and relief packages.

Countries prone to natural disasters, such as the Philippines and Japan, often stockpile canned proteins for quick deployment during typhoons or earthquakes. Recently, defense procurement agencies in Eastern Europe have increased orders for shelf-stable meats, including sausages, to support troops stationed in remote areas.

Eco-labels and Transparent Supply Chains

Sustainability credentials are emerging as a differentiator in the canned sausage market, especially in Europe. Consumers are showing superior loyalty toward products with recyclable packaging, clean-label certifications, or verified farm-to-can sourcing.

For example, Germany-based retailers are giving more shelf space to canned meat brands that exhibit reduced carbon footprints or use light recyclable cans. Producers that invest in transparent sourcing and traceable supply chains can win over buyers who are increasingly attentive to environmental impact.

Plant-based and Hybrid Sausage Alternatives

The rise of plant-based eating presents a chance to reimagine canned sausages for new demographics. While the market is still niche, canned versions of soy- or pea-based sausages could appeal to flexitarians and vegetarians seeking long-lasting and ready-to-eat protein. Asia’s markets are already experimenting with canned mock meats, with companies in China launching shelf-stable plant-based luncheon products on e-commerce platforms.

Hybrid sausages that blend meat with plant protein could also attract health-conscious buyers who want low-fat options without giving up taste. As plant-based convenience foods expand, producers who adapt canned sausage formats to this trend can tap into a young, eco-aware consumer base.

Category-wise Analysis

Source Insights

Pork sausages are anticipated to account for approximately 32.6% of the market share in 2025. These have been the traditional bases for processed meats in various regions, especially Europe and Asia Pacific, where sausages are deeply tied to culinary culture. The flavor and texture of pork adapt well to canning, maintaining a familiar taste even after long storage.

Beef sausages are gaining impetus because they cater to consumers who want a richer flavor and higher protein profile compared to pork or chicken. In the U.S. and Australia, beef has long been associated with premium-quality meat. Canned beef sausages carry that same perception of being more filling and indulgent.

Packaging Insights

Metal cans are estimated to hold a share of nearly 45.3% in 2025. These provide unmatched durability, long shelf life, and resistance to external damage. They are lightweight and easy to transport, making them ideal for bulk distribution and government procurement for military or disaster relief programs.

Glass jars, on the other hand, are seeing steady growth because they cater to the rising demand for premium and eco-friendly packaging. Consumers increasingly associate glass with quality, freshness, and sustainability. In Europe, brands such as Meica have introduced sausages in glass jars, marketed as more natural and preservative-free compared to metal-canned versions.

Distribution Channel Insights

Supermarkets/hypermarkets are predicted to account for around 39.6% of the market share in 2025. They combine variety, visibility, and affordability in one place. Shoppers often buy canned sausages as part of bulk grocery runs, and these large stores provide wide assortments across brands, flavors, and pack sizes.

Online retail is gaining high popularity as it delivers convenience and accessibility, specifically for urban consumers who prefer doorstep delivery of non-perishable food. E-commerce platforms in Asia Pacific actively promote canned sausages during flash sales and bundle deals, making them affordable pantry fillers for young buyers.

Regional Insights

North America Canned Sausages Market Trends

In 2025, North America is anticipated to account for approximately 36.4% of the market share. Canned sausages are considered a staple in discount retail chains and convenience stores in the region. However, the category is under pressure from fresh and frozen sausage products.

Traditional brands such as Armour and Hormel maintain their grip through wide distribution and value packs, but consumer preference has shifted toward fresh options. This is leaving canned sausages positioned mainly as low-cost and long-shelf-life proteins.

Innovation in the U.S. is limited but noticeable. Some producers have launched chicken- or turkey-based canned sausages and low-sodium versions to comply with dietary concerns.

Convenience-driven packaging, such as easy-open cans and small portion sizes, has also appeared to attract single-person households and young buyers who want emergency pantry proteins. Private-label growth is significant with Walmart, Dollar General, and other mass retailers pushing house brands to meet demand from budget-conscious shoppers.

Europe Canned Sausages Market Trends

In Europe, canned sausages have a stronger cultural foothold compared to North America. It is especially evident in Germany, Poland, and Eastern European countries, where long-shelf-life meats remain part of everyday meals. German brands such as Meica and Tulip Foods still see steady demand for canned frankfurters and Vienna-style sausages, often marketed as quick meal solutions for households and camping use.

Retailers in Europe also use canned sausages as a value-for-money product, but unlike in the U.S., they are positioned more as traditional foods than just budget proteins. For instance, in Germany, Lidl and Aldi continue to stock private-label canned sausages alongside established local brands, reinforcing consumer familiarity with the category rather than phasing it out.

Asia Pacific Canned Sausages Market Trends

In Asia Pacific, canned sausages are positioned more as convenience-based, affordable proteins for urban households and working-class consumers. In countries, including the Philippines and Indonesia, brands such as CDO and San Miguel Foods have built powerful loyalty by delivering canned sausages as quick meal staples, often paired with rice for breakfast or lunch.

Their popularity is associated less with Western snacking culture and more with everyday family meals.

China is seeing rising traction in canned sausages through e-commerce platforms such as JD.com and Taobao, where local brands market them as pantry essentials for busy professionals. The pandemic boosted demand as households stocked up on shelf-stable proteins.

Even today, online sales of canned sausages remain steady due to the trust in long shelf life and ease of preparation. Japan and South Korea showcase a different angle, where canned sausages are marketed as camping and convenience food.

Competitive Landscape

The canned sausages market is dominated by big food processors and long-standing brands. Companies such as Armour (Conagra), Hormel, and a few Europe-based meat processors lead in terms of shelf space in supermarkets and institutional supply.

Their strength comes from large-scale production, established distribution networks, and brand familiarity, which keeps them ahead in the mainstream category. Private-label and retailer brands are another superior force in the market.

Business Strategies

Market leaders in the field of canned sausages rely on cost leadership through mass production and private-label partnerships while expanding into emerging markets with superior distribution. Innovation focuses on clean-label, chicken, and organic variants to attract health-conscious buyers. New trends include ready-to-eat meal integrations, microwave-friendly packaging, and premium niche flavors targeting young consumers.

Key Industry Developments

- In May 2025, Amylu Foods launched its Organic Chicken Sausages. These are now available in the refrigerated aisle at Harris Teeter, Fresh Thyme, and Gelson's.

- In October 2024, Jamaica Broilers Group entered the canned goods market as part of a broad effort to diversify its product lines and tap into new segments. The company’s recent launch of Vienna sausages under the Best Dressed Chicken brand marks its entry into the shelf-stable food market.

Companies Covered in Canned Sausages Market

- Conagra Brands, Inc.

- Hormel Foods Corporation

- Tyson Foods, Inc.

- Johnsonville, LLC

- Maple Leaf Foods Inc.

- Nestlé S.A.

- Campbell Soup Company

- The Kraft Heinz Company

- Dongwon F&B Co., Ltd.

- Zwanenberg Food Group

- Globus Canning Company

- Ayam Brand

- Tulip Food Company (Danish Crown Group)

- Bolton Group (Simmenthal)

- Goya Foods, Inc.

- Royal Foods Co., Ltd.

- Shanghai Maling Aquarius Co., Ltd.

- Pran Foods Ltd.

- Lotte Foods Co., Ltd.

- San Miguel Food and Beverage, Inc.

Frequently Asked Questions

The canned sausages market is projected to reach US$7.6 Bn in 2025.

High demand from disaster relief stockpiles and convenience for urban households are the key market drivers.

The canned sausages market is poised to witness a CAGR of 4.7% from 2025 to 2032.

Expansion into plant-based variants and premium positioning through glass jar packaging are the key market opportunities.

Conagra Brands, Inc., Hormel Foods Corporation, and Tyson Foods, Inc. are a few key market players.