- Processed Food

- Canned Meat Market

Canned Meat Market Size, Share, and Growth Forecast 2026 - 2033

Canned Meat Market by Product (Beef, Pork, Poultry, Seafood, Others), by Processing Type (Cooked, Smoked, Cured, Ready-to-Eat), by Sales Channel (Supermarkets & Hypermarkets, Convenience Stores, Online, Foodservice, Others), and Regional Analysis, 2026 - 2033

Canned Meat Market Share and Trends Analysis

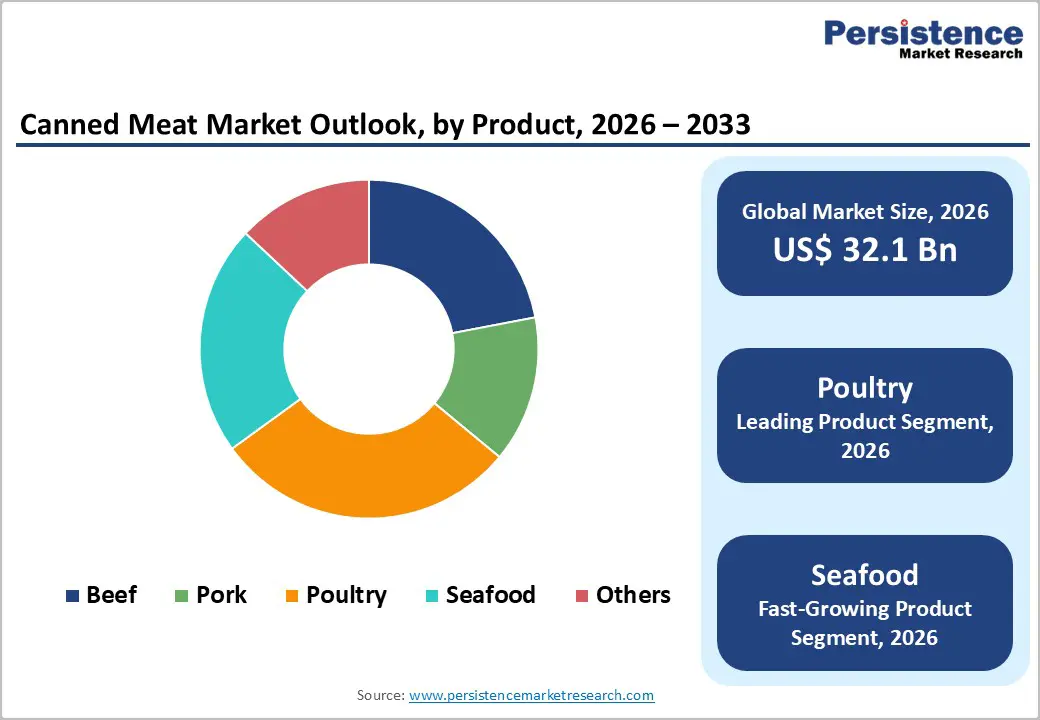

The global canned meat market size is expected to be valued at US$ 32.1 billion in 2026 and projected to reach US$ 43.7 billion by 2033, growing at a CAGR of 4.5% between 2026 and 2033. This robust trajectory is primarily driven by the growing demand for convenient, shelf-stable protein sources across diverse consumer segments, coupled with evolving lifestyle patterns among time-constrained urban populations seeking ready-to-eat meal solutions.

The market expansion is further reinforced by technological advancements in food preservation, including high-pressure processing and enhanced canning techniques that preserve nutritional integrity while extending product shelf life. Additionally, the increasing frequency of emergency preparedness initiatives and outdoor recreational activities has heightened consumer demand for long-lasting, portable protein options that require minimal preparation infrastructure.

Key Industry Highlights:

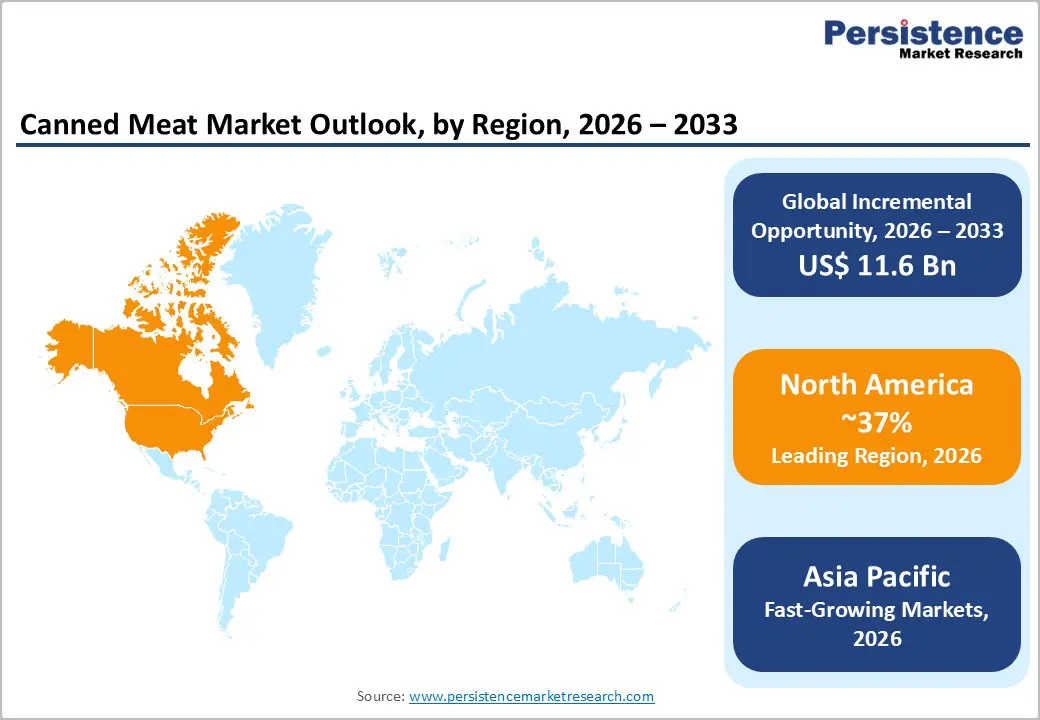

- North America maintains market leadership, commanding approximately 37% of the global market in 2025, driven by established consumption patterns, mature retail and foodservice infrastructure, robust brand presence of major manufacturers such as Hormel Foods, Tyson Foods, and Conagra Brands, and strong regulatory oversight that reinforces consumer confidence in product safety and quality.

- Asia Pacific emerges as the fastest-growing regional market with growth projected above 4.5% CAGR by 2033, fueled by rapid urbanization, expanding middle-class population, rising disposable incomes, retail modernization, and evolving dietary patterns in populous markets including China, India, and key ASEAN economies, where convenient, shelf-stable proteins increasingly supplement traditional diets.

- Poultry is the dominant product segment, holding approximately 29% share in 2025, supported by perceptions of healthfulness, competitive pricing relative to beef and seafood, versatile culinary use across home and foodservice applications, and robust supply chains, making it a core driver of overall canned meat category performance.

- Premium and specialty canned meat products present a key opportunity, as consumers show a growing willingness to pay for organic, clean-label, and sustainably packaged offerings; companies that invest in reduced-sodium formulations, innovative flavors, ethical sourcing, and eco-friendly packaging are well positioned to capture high-margin growth pockets globally.

| Key Insights | Details |

|---|---|

|

Canned Meat Market Size (2026E) |

US$ 32.1 Bn |

|

Market Value Forecast (2033F) |

US$ 43.7 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

4.5% |

|

Historical Market Growth (CAGR 2020 to 2025) |

4.1% |

Market Dynamics

Drivers - Accelerating Urbanization and Demand for Convenience-Oriented Food Solutions

The exponential growth in urban populations globally has fundamentally transformed consumer food consumption patterns, creating substantial demand for convenient, ready-to-consume protein alternatives. According to the United Nations Department of Economic and Social Affairs, approximately 56% of the global population resided in urban areas as of 2024, with projections indicating this proportion will escalate to 68% by 2050. This urbanization phenomenon correlates directly with lifestyle changes characterized by longer working hours, reduced time for meal preparation, and a heightened preference for products that are ready for immediate consumption. The U.S. Department of Agriculture (USDA) reported that American consumers allocated only 37 minutes per day to food preparation and cleanup in 2022, underscoring the compelling need for time-efficient meal alternatives. Canned meat products, which require no refrigeration and minimal preparation, align seamlessly with these evolving consumer requirements, offering shelf-stable protein sources with extended viability periods ranging from two to five years without degradation. Furthermore, the expansion of dual-income households and single-person living arrangements has amplified demand for portion-controlled, individually packaged protein options that minimize food waste while maintaining nutritional adequacy.

Rising Health Consciousness and Protein-Centric Dietary Preferences

Contemporary consumer dietary paradigms increasingly emphasize high-protein nutrition as fundamental to wellness, fitness optimization, and disease prevention strategies. The Food and Agriculture Organization (FAO) reported that global meat production reached approximately 360 million metric tons in 2023, reflecting sustained availability of raw materials supporting the canned meat industry. Medical and nutritional research consistently demonstrates that adequate protein intake supports muscle development, metabolic function, immune function, and satiety regulation, which are crucial for weight-control initiatives. This growing health awareness has propelled consumer preferences toward lean protein sources, with canned poultry products benefiting from perceptions of lower fat content than red meat alternatives.

The World Health Organization (WHO) acknowledges that processed meats, including canned variants, contribute significantly to protein intake, particularly in regions with limited access to fresh refrigerated alternatives. Moreover, manufacturers are responding to health-conscious consumers by introducing organic, low-sodium, preservative-free, and antibiotic-free canned meat formulations that address concerns about artificial additives while maintaining convenience. The integration of clean-label initiatives and nutritional enhancement strategies positions canned meat products favorably within the expanding health and wellness market segment.

Restraints - Health Concerns Associated with Processed Meat Consumption

The canned meat industry confronts persistent challenges stemming from public health advisories regarding processed meat consumption and potential health implications. The World Health Organization (WHO) has classified processed meats as Group 1 carcinogens, indicating sufficient evidence linking consumption to increased colorectal cancer risk, generating consumer apprehension and potentially constraining market expansion. Additionally, concerns regarding sodium content, which facilitates preservation but contributes to hypertension and cardiovascular complications, have prompted consumer scrutiny of nutritional labels.

The typical canned meat product contains elevated sodium, with some formulations exceeding 400–600 milligrams per serving, representing a substantial proportion of the recommended daily intake. Furthermore, historical concerns about the presence of Bisphenol A (BPA) in can linings, despite industry transitions toward BPA-free alternatives, continue to adversely affect consumer perceptions. These health-related concerns have prompted dietary shifts among certain consumer segments toward fresh, unprocessed protein sources or plant-based alternatives, potentially limiting market penetration among health-conscious consumers. Manufacturers must navigate increasingly stringent labeling requirements and invest in reformulation initiatives to address these concerns while maintaining product palatability and shelf-stability characteristics.

Price Volatility in Raw Material Procurement and Supply Chain Disruptions

The canned meat manufacturing sector is highly vulnerable to fluctuations in raw material costs, particularly for primary inputs such as beef, pork, poultry, and seafood. Hormel Foods Corporation disclosed during fiscal 2025 that pork belly prices surged 25%, pork cutout increased 10%, and pork trim rose 20% compared to preceding periods, while beef prices demonstrated substantial elevation throughout the fiscal year. Such cost inflation directly affects manufacturers' margin structures, particularly when pricing adjustments lag input cost increases due to contractual obligations or competitive market dynamics. Additionally, supply chain vulnerabilities have been exacerbated by disease outbreaks affecting livestock populations, including avian influenza, which constrained turkey supplies throughout 2024 and 2025, as reported by major industry participants. Climate change impacts on agricultural productivity, geopolitical tensions affecting trade flows, and transportation cost escalation further compound supply chain complexities. These cost pressures necessitate strategic pricing modifications that may adversely affect consumer demand elasticity, particularly in price-sensitive market segments. The inability to fully offset margin impacts within fiscal periods creates financial uncertainty that may constrain investment in innovation, capacity expansion, or marketing initiatives essential for long-term market development.

Opportunity- Innovation in Premium and Specialty Product Segments Aligned with Evolving Consumer Preferences

The canned meat industry presents significant opportunities through product innovation to address evolving consumer sophistication and willingness to pay premium prices for enhanced quality, unique flavor profiles, and specialty formulations. Consumer demand for gourmet, organic, sustainably sourced, and ethnically inspired canned meat products is expanding, creating opportunities for differentiation beyond commodity-oriented offerings. The successful introduction of specialty canned seafood products featuring premium ingredients, unique seasonings, and artisanal preparation methods demonstrates viable consumer acceptance of elevated price points when justified by perceived quality enhancements. Hormel Foods Corporation exemplified this trend through 2024 product launches, including HORMEL BLACK LABEL OVEN READY Thick-Cut Bacon featuring patent-pending preparation technologies, and FLASH 180 Battered Sous Vide Chicken Breast, addressing foodservice operator requirements for versatile, pre-cooked solutions. Additionally, the integration of sustainable packaging innovations, including BPA-free linings, recyclable materials, and reduced-weight aluminum alternatives, addresses environmental consciousness among millennial and Gen Z consumers who increasingly incorporate sustainability criteria into purchasing decisions.

Manufacturers investing in clean-label formulations, eliminating artificial preservatives, reducing sodium content through advanced preservation technologies such as High-Pressure Processing (HPP), and obtaining organic or grass-fed certifications can command premium pricing while accessing high-value consumer segments. The convergence of convenience, quality, and sustainability attributes positions premium canned meat offerings favorably within the broader trajectory of the prepared foods market.

Category-wise Insights

Product Analysis

Poultry dominates the global canned meat market, commanding approximately 29% market share in 2025, positioning it as the leading product category driven by multiple convergent factors. Consumer preference for poultry-based canned products stems primarily from the widespread perception that chicken and turkey are healthier protein alternatives to red meat, with lower saturated fat content and lower caloric density. According to disclosures from major producers such as Hormel Foods Corporation, canned poultry products posted high-single-digit growth throughout 2024–2025, reflecting sustained consumer demand. The versatility of canned poultry products, which integrate seamlessly into diverse culinary applications, including sandwiches, salads, casseroles, and standalone meals, enhances their appeal across diverse consumer demographics and usage contexts.

Additionally, poultry’s neutral flavor profile supports extensive seasoning and flavor innovation, enabling manufacturers to introduce differentiated product variants that address ethnic cuisine preferences and contemporary taste trends. From a pricing perspective, canned poultry typically remains competitively priced relative to beef and seafood alternatives, enhancing accessibility across broad socioeconomic segments. USDA documentation that poultry is a staple protein source in American diets, coupled with favorable nutritional profiles endorsed by health organizations, reinforces category leadership. Furthermore, supply chain resilience, despite periodic challenges from avian influenza outbreaks, generally maintains adequate raw material availability supporting consistent production volumes and market supply stability.

Sales Channel Insights

Supermarkets & hypermarkets dominate the canned meat distribution landscape, capturing a 42% share in 2025 and serving as the primary consumer purchase destination for canned meat products globally. These large-format retail establishments offer comprehensive product assortments across diverse brands, protein types, processing methods, and package sizes within consolidated shopping environments, maximizing convenience through one-stop shopping. The extensive shelf space supermarkets and hypermarkets allocate to canned goods ensures prominent product visibility and facilitates impulse purchases among browsing consumers. Distribution analyses show that these retail formats effectively reach mainstream consumers through geographically dispersed store networks located in residential areas across urban, suburban, and increasingly rural markets.

The competitive pricing dynamics characteristic of supermarket operations, enabled by volume purchasing economies and periodic promotional activities, enhance the affordability of canned meat and stimulate trial among price-sensitive consumer segments. Furthermore, supermarkets and hypermarkets typically maintain rigorous quality assurance standards and established cold chain management for complementary fresh products, lending credibility to their canned product offerings through halo effects. The integration of private-label canned meat offerings by major retail chains provides additional value-oriented alternatives that expand category accessibility while creating opportunities to enhance retailer margins. Additionally, traditional shopping patterns of consumers who conduct weekly or bi-weekly grocery provisioning missions position supermarkets advantageously for stock-up purchases of shelf-stable items including canned meats that support household pantry inventory management strategies.

Regional Insights

North America Canned Meat Market Trends and Insights

North America maintains its position as the leading regional market for canned meat products, commanding approximately 37% of global market share in 2025, underpinned by deeply entrenched consumption patterns and mature distribution infrastructure. The United States represents the dominant country market within the region, characterized by established consumer familiarity with canned meat categories spanning multiple generations and extensive product availability across retail formats. Household panel and consumption data indicate that consumption of canned meat shows stable penetration across American households, supported by cultural acceptance of convenience foods and emergency-preparedness orientations that position canned proteins as pantry staples.

Asia Pacific Canned Meat Market Trends and Insights

Asia Pacific represents the fastest-growing regional market for canned meat products, driven by dramatic urbanization trajectories, rising middle-class populations, and evolving dietary patterns across populous nations, including China, Japan, India, Indonesia, Thailand, the Philippines, and Vietnam. China dominates in regional consumption and production, accounting for approximately 36% of production volume and nearly 38% of production, reflecting both its massive population and increasing consumer acceptance of convenient protein formats. However, growth rates are particularly dynamic in smaller economies, with import statistics showing double-digit annual growth in markets such as the Philippines and India as retail infrastructure modernizes and disposable incomes rise.

Competitive Landscape

The canned meat market features a moderately fragmented competitive environment in which numerous established and emerging participants compete through product innovation, branding, and strong distribution networks. Rivalry is intensified by the launch of new flavors, healthier variants such as low-sodium and clean-label products, and improved packaging formats that match changing consumer preferences. Players are also strengthening their retail and online presence while pursuing partnerships and geographic expansion to improve shelf access. As a result, long-term success depends on efficient operations, resilient supply chains, and clear product differentiation rather than relying solely on price competition.

Key Developments:

- In January 2026, Kazakhstan and Kuwait strengthened their bilateral trade and economic relations, placing greater emphasis on cooperation in the agro-industrial sector and food security. During a working visit to Kuwait, the Kazakh company Eurasia Agro Semey signed a Memorandum of Cooperation with ALMARAI National Co. to develop collaboration in supplying meat products to the Kuwaiti market, reflecting both countries’ intent to deepen commercial partnerships and expand agricultural trade flows.

Companies Covered in Canned Meat Market

- Hormel Foods Corporation

- Conagra Brands, Inc.

- Tyson Foods, Inc.

- JBS S.A.

- Kraft Heinz Company

- Campbell Soup Company

- Smithfield Foods, Inc.

- Bolton Group

- Princes Group

- Century Pacific Food, Inc.

- Zwanenberg Food Group

- Ayam Brand

- Others

Frequently Asked Questions

The global canned meat market is projected to be valued at US$ 32.1 billion in 2026, establishing the baseline for growth analysis by 2033, and reflecting sustained demand for convenient, shelf-stable protein solutions across both developed and emerging economies.

The canned meat market is driven by accelerating urbanization that creates time-pressed consumer lifestyles, rising health consciousness that supports protein-centric diets, increasing disposable incomes in emerging markets enabling higher animal protein intake, and expanding retail and e-commerce infrastructure that improves visibility, accessibility, and affordability of shelf-stable meat products.

North America is the leading region, holding roughly 37% of global market share in 2025, supported by long-established consumption habits, broad penetration of supermarkets, club stores, and foodservice channels, strong regulatory controls from agencies such as USDA and FSIS, and the presence of major global brands such as Hormel Foods Corporation, Tyson Foods, Inc., and Conagra Brands, Inc.

The most significant opportunity lies in emerging markets across Asia Pacific, Latin America, and the Middle East & Africa, where a rising middle-income population, rapid urbanization, and modernization of retail and digital commerce are expanding the addressable base for convenient protein products, especially when manufacturers localize flavors, formats, and price points to regional preferences.

Key players in the canned meat industry include Hormel Foods Corporation, Tyson Foods, Inc., JBS S.A., Conagra Brands, Inc., Kraft Heinz Company, Campbell Soup Company, Smithfield Foods, Inc Bolton Group, Princes Group, Century Pacific Food, Inc., Zwanenberg Food Group, Ayam Brand, Thai Union Group PCL, and Wild Planet Foods, Inc., which compete through brand portfolios, innovation, supply chain integration, and broad multi-channel distribution.