- Smart Packaging

- Candle Box Market

Candle Box Market Size, Share, and Growth Forecast, 2026 - 2033

Candle Box Market by Box Type (Mass Candle Boxes, Lock Bottom Boxes, Others), Candle Type (Container/Jar Candles, Craft/Artisan Candles, Others), Material, and Regional Analysis for 2026 - 2033

Candle Box Market Size and Trends Analysis

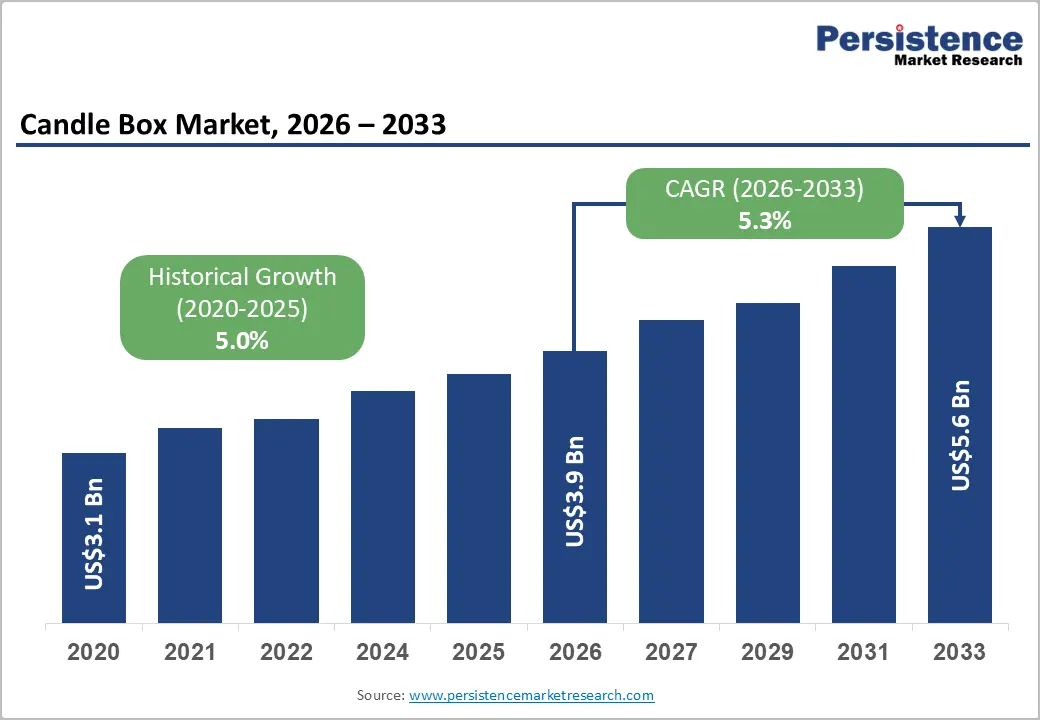

The global candle box market size is likely to be valued at US$3.9 billion in 2026 and is expected to reach US$5.6 billion by 2033, growing at a CAGR of 5.3% between 2026 and 2033, driven by the premiumization of gifting and home-fragrance products, a surge in e-commerce channels demanding robust secondary packaging, and the growing adoption of sustainable materials that enhance pack value and consumer perception.

The rising popularity of jar/container candles, which require protective and branded packaging, alongside the growth of artisanal and small-batch candle brands, is expanding the addressable packaging spend. Box manufacturers can capture higher margins through material innovation, finishing enhancements, and structural optimization. Market elasticity is moderate, with opportunities for converters to scale through value-added packaging services.

Key Industry Highlights:

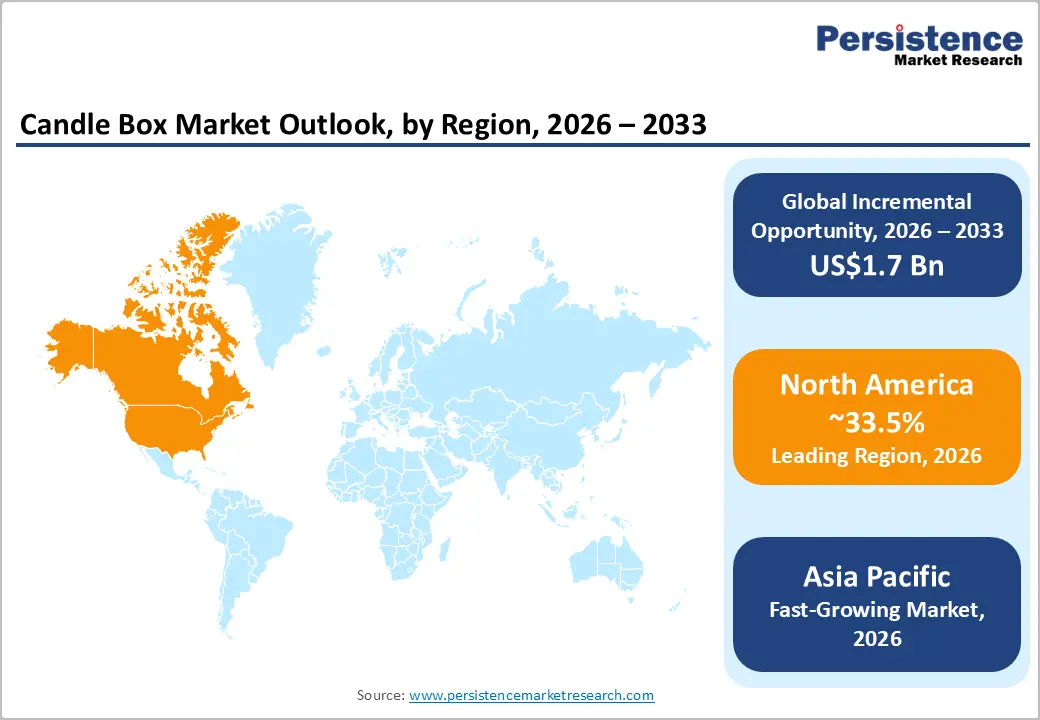

- Leading Region: North America is projected to lead the market with an estimated 33.5% share, supported by strong holiday gifting demand, high per-capita home-fragrance consumption, and advanced e-commerce fulfillment infrastructure.

- Fastest-growing Region: Asia Pacific is the fastest-growing region, driven by low-cost manufacturing in China, rising domestic consumption in India and ASEAN, and export-oriented rigid box production.

- Investment Plans: The industry is witnessing sustained investments in digital print lines, automation, and recyclable paperboard capacity, with major converters allocating capital toward short-run customization and reinforced lock-bottom formats to support DTC and online retail growth.

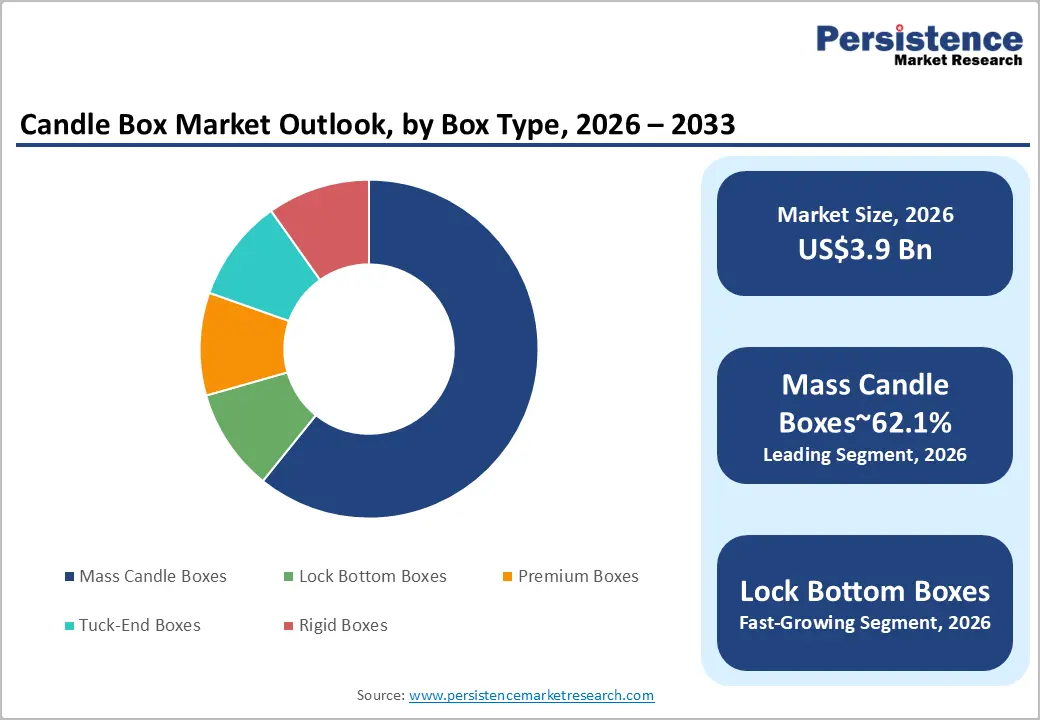

- Dominant Box Type: Mass candle boxes dominate with an anticipated 62.1% market share in 2025, owing to high-volume retail distribution and cost-efficient standardized carton formats.

- Leading Candle Type: Container/jar candles lead with approximately 36.8% share, supported by higher protective requirements, premium branding elements, and increased per-unit packaging spend in gifting and home-fragrance segments.

| Key Insights | Details |

|---|---|

| Candle Box Market Size (2026E) | US$3.9 Bn |

| Market Value Forecast (2033F) | US$5.6 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.0% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Premiumization and Gifting Growth

Retailers and direct-to-consumer (DTC) candle brands are increasingly investing in branded secondary packaging to enhance perceived value and capture higher margins in gifting and lifestyle channels. Premium boxes command price premiums, particularly for limited-edition and seasonal SKUs, driving up average packaging spend. Growth in scented and container candles, which generally retail at higher price points, further increases demand for display-quality, protective boxes.

Packaging suppliers offering textured boards, soft-touch finishes, and integrated inserts benefit from higher average selling prices (ASPs) and improved margins. Trade data indicates that lifestyle-oriented candle segments consistently elevate box demand, particularly in developed markets with mature gifting cultures, reflecting stable growth for premium packaging solutions.

E-Commerce and Omni-Channel Distribution

The rapid expansion of online retail is reshaping candle box requirements. Structural integrity, including crush resistance and reinforced bottoms, is essential to protect products during shipping. Lock-bottom and crash-bottom formats are increasingly preferred for heavier jar/container candles, reducing transit damage and returns. Brands are standardizing pack formats to improve shelf readiness for click-and-collect and reduce logistics inefficiencies. While lightweight paperboard is adopted to manage shipping costs, premium rigid boxes and specialty finishes remain favored for repeat-purchase products. Industry data confirms higher per-unit packaging spend in e-commerce-dominated segments, creating opportunities for converters specializing in structural innovation.

Material Innovation and Sustainability

Sustainability drives demand for eco-friendly candle boxes, including compostable paperboards, biodegradable coatings, and fiber-based closures. Brands are replacing plastic laminates with recyclable barrier coatings or cold-foil alternatives, enabling premium aesthetics while reducing environmental impact. Regulatory initiatives targeting packaging waste further encourage the adoption of recyclable and certified materials, particularly in Europe and North America. Suppliers providing validated recycled content and end-of-life solutions capture growth from both mainstream and premium brands, offering a measurable value proposition tied to environmental compliance and consumer demand for sustainable, premium packaging.

Barrier Analysis - Volatility in Raw-Material Costs

Fluctuations in paperboard, pulp, and specialty finishing costs impact converter and brand margins. Sharp price increases, driven by energy or transport volatility, reduce profitability, particularly for small and artisanal producers. If cost inflation cannot be fully passed to consumers, the pace of premiumization slows. Historical data shows that pulp price volatility can lead to 3-8% year-on-year packaging cost swings for mid-sized converters. Limited hedging options mean that manufacturers often resort to short-term price surcharges or product reformulation, affecting consistent market expansion.

Regulatory and Recycling Infrastructure Gaps

While regulations increasingly emphasize recyclability and reduced plastic use, recycling infrastructure is inconsistent across regions. Boxes that are recyclable in one market may fail compliance in another due to laminate coatings or mixed materials, complicating cross-border SKU standardization. Brands either create market-specific packs or accept higher compliance risk. In markets with inadequate recycling systems, investments in sustainable packaging may offer limited real-world environmental benefit, slowing adoption and potentially leading to stranded inventory for converters.

Opportunity Analysis - Sustainable Premiumization

Combining recycled/biodegradable substrates with premium finishing allows brands to capitalize on both environmental objectives and gifting positioning. Eco-premium boxes, incorporating certified recycled board and compostable inserts, enable converters to sell design and compliance services, including material certification and end-of-life labeling. Consumer willingness to pay for verified sustainability is measurable, allowing suppliers to command 10-20% higher ASPs for specialty candle brands. This is particularly strong in North America and Europe, where regulatory oversight and conscious consumption trends amplify demand for eco-premium packaging.

Customization for Artisan and DTC Brands

Small-batch and artisanal candle brands prioritize packaging that communicates craft provenance and story. Digital print, short-run finishing, and on-demand inserts allow converters to provide tailored solutions, unlocking repeat business and premium per-unit pricing. Suppliers offering integrated design studios, digital print lines, and fulfillment partnerships become strategic partners for DTC brands scaling via social commerce. High e-commerce penetration and supportive logistics ecosystems reinforce the value of rapid, customized packaging, creating a high-margin niche for converters.

Category-wise Analysis

Box Type Insights

Mass candle boxes are expected to account for 62.1% share in 2026, supported by large-scale retailers, supermarket chains, and private-label candle manufacturers. Typically produced using SBS or recycled paperboard with minimal surface finishing, these formats prioritize cost efficiency and production scalability. Lock-bottom and tuck-end carton structures remain widely adopted due to quick assembly and compatibility with automated filling lines. Major retail suppliers to chains such as Walmart and Target rely on standardized mass cartons to maintain supply consistency across nationwide distribution networks. Low average selling prices (ASPs) are offset by extremely high order volumes and repeat contracts, ensuring predictable demand cycles.

The segment also benefits from private-label expansion in discount retail and hypermarkets, where packaging efficiency and stackability are key procurement metrics. While premiumization trends influence niche formats, mass boxes remain foundational to overall market stability due to their volume-driven economics and established converter infrastructure.

Lock-bottom, crash-bottom, and reinforced rigid-style cartons represent the fastest-growing structural formats as candle weights increase and multi-pack assortments become common. Heavier glass container candles, three-wick jars, and gift bundles require superior compression strength and drop resistance, particularly for e-commerce shipments. Growth in online sales channels, including marketplaces such as Amazon, has made transit durability a measurable KPI tied directly to return-rate reduction.

Converters offering reinforced corrugated inserts, die-cut partitions, molded pulp cushioning, and ISTA-tested packaging solutions are capturing higher-margin opportunities. Brands focused on reducing product breakage during last-mile delivery increasingly adopt engineered packaging with enhanced structural integrity. Markets with strong online penetration, particularly North America and Western Europe, show the highest uptake of reinforced formats, as logistics optimization directly impacts profitability and customer satisfaction metrics.

Candle Type Insights

Container and jar candles are anticipated to account for 36.8% share in 2026, due to their protective requirements and premium presentation appeal. Glass, ceramic, and metal vessels require structural inserts, tamper-evident closures, and protective cushioning to prevent chipping or cracking during transit. Premium fragrance brands such as Yankee Candle and Bath & Body Works emphasize gift-ready packaging and strong shelf visibility, which increases per-unit packaging expenditure.

Home-fragrance, seasonal gifting, and specialty retail channels drive the bulk of demand, encouraging converters to integrate foam inserts, die-cut board supports, and FSC-certified paper solutions. The unboxing experience also plays a central role, as consumers increasingly associate packaging aesthetics with product quality. This segment delivers higher revenue per unit compared to pillar or taper candle formats due to its structural and branding complexity.

Craft and artisan candles represent the fastest-growing candle type segment, supported by direct-to-consumer (DTC) expansion and social-commerce platforms. Independent brands and small-batch producers invest in textured boards, embossing, foil stamping, and short-run digital printing to highlight craftsmanship and brand storytelling. Platforms such as Etsy have accelerated the visibility of boutique candle makers, increasing demand for differentiated, design-forward packaging.

Per-unit packaging spend in this segment often exceeds mainstream container candles due to customization and lower production volumes. Seasonal gifting campaigns, influencer collaborations, and limited-edition releases further amplify packaging innovation. Converters equipped with digital presses, rapid prototyping, and premium finishing capabilities are well-positioned to capitalize on this high-margin, fast-expanding niche within the broader candle box market.

Regional Insights

North America Candle Box Market Trends - E-commerce Durability, EPR Compliance, and Seasonal Premiumization

North America is projected to account for approximately 33.5% of the market share in 2026, supported by mature organized retail, strong e-commerce penetration, and high per-capita spending on home-fragrance and seasonal gifting. The U.S. remains the dominant contributor, driven by strong holiday sales cycles and brand-led premiumization strategies. Major candle brands such as Yankee Candle and Bath & Body Works continue expanding seasonal and limited-edition product lines, directly increasing demand for structurally reinforced and visually differentiated secondary packaging.

Canada’s artisan candle segment is expanding through boutique and online channels, while Mexico contributes incremental volume growth in cost-effective mass box formats linked to cultural and religious usage patterns. Growth in omni-channel retail and marketplace fulfillment has intensified demand for durable, transit-tested packaging formats. Platforms such as Amazon have elevated packaging durability benchmarks, encouraging converters to engineer lock-bottom and reinforced cartons that reduce breakage during last-mile delivery. Regulatory developments are also reshaping procurement decisions.

State-level Extended Producer Responsibility (EPR) regulations in states, including California and Maine, are influencing material selection, accelerating the adoption of recyclable SBS and FSC-certified paperboard substrates. Investment trends across the region highlight digital print expansion and short-run finishing capabilities to support DTC brands. In recent years, packaging manufacturers, including WestRock, have invested in automated converting lines and sustainable paperboard solutions, strengthening supply reliability for consumer goods brands. These investments enable faster turnaround for seasonal SKUs and small-batch artisan orders, increasing per-unit packaging spend while improving operational efficiency. Partnerships between converters and sustainable board suppliers are also reinforcing North America’s leadership in recyclable and structurally optimized candle packaging solutions.

Europe Candle Box Market Trends - Circular Economy Mandates and Luxury Rigid-Box Innovation

Europe represents a significant and regulation-driven market for candle boxes, underpinned by a strong gifting culture and advanced sustainability mandates. Germany and the U.K. lead regional revenue generation, while France and Spain demonstrate healthy demand for premium scented and jar candles. Germany favors advanced finishes and rigid structural boxes that support high-end fragrance positioning. The U.K. shows strong adoption of DTC models, with brands leveraging online platforms to scale artisan and customized candle offerings. France’s luxury home-fragrance houses emphasize aesthetic packaging quality, and Spain maintains a steady demand for seasonal mass-market candle cartons.

Regulatory frameworks heavily influence packaging design and substrate selection. EU-wide packaging directives and EPR schemes require recyclability, mono-material construction, and responsible sourcing. These policies have encouraged converters to eliminate plastic window films and transition to fiber-based alternatives. Companies such as Smurfit Kappa have launched fully recyclable packaging solutions across European operations, replacing mixed-material constructions with paper-based formats. This shift supports compliance while enhancing brand sustainability credentials.

Investment across Europe focuses on sustainable substrate sourcing, regional finishing hubs, and cross-border compliant packaging designs. Converters are strengthening pan-European distribution networks to reduce lead times for multinational candle brands. Recent developments include the introduction of recyclable eco-lines and premium rigid-box capabilities for high-end fragrance brands, supporting luxury positioning while meeting environmental standards. The integration of digital print and embellishment technologies further enables short-run seasonal launches, reinforcing Europe’s balance between regulatory compliance and premium presentation.

Asia Pacific Candle Box Market Trends - Export-Scale Manufacturing and Emerging Domestic Premium Demand

Asia Pacific is the fastest-growing regional market for candle boxes, driven by cost-efficient manufacturing capacity, rising domestic consumption, and expanding intra-regional trade flows. China leads both production and domestic consumption, serving as a global supply hub for mass and structural candle cartons. Japan emphasizes premium finishing quality, particularly for luxury fragrance packaging. India and ASEAN economies are emerging rapidly, supported by expanding middle-class demand and increasing online retail penetration.

China’s manufacturing ecosystem enables large-scale production of lock-bottom and reinforced cartons for export markets, benefiting from automation and vertical integration. Companies such as Nine Dragons Paper continue expanding recycled paperboard capacity, supporting sustainable substrate supply for packaging converters. Japan maintains a premium orientation, with strong attention to finishing precision and aesthetic quality aligned with luxury consumer preferences. In India, DTC-driven artisan candle brands are partnering with regional converters to deliver short-run customized packaging for festival seasons and gifting occasions, particularly during Diwali and wedding cycles.

Regulatory frameworks remain fragmented across the region, though the adoption of certified recycled content is increasing in China and Japan. India’s evolving packaging waste management rules are gradually encouraging recyclable materials and responsible sourcing. Investment trends emphasize automation, digital print integration, and regional finishing facilities that shorten lead times for seasonal SKUs. Capacity expansions in China and Vietnam for reinforced and rigid box production strengthen export competitiveness, while India’s growing converter base supports domestic artisan and premium brand expansion. Collectively, these developments position Asia Pacific as both a production powerhouse and a rapidly expanding consumption-driven market.

Competitive Landscape

The global candle box market is moderately fragmented, combining global converters serving multinational brands and regional specialists serving DTC and artisan brands. Leading converters dominate high-volume categories, while specialists achieve higher margins through premium finishing, structural engineering, and short-run capabilities. Market concentration is higher in premium rigid boxes, whereas mass boxes remain highly competitive and price-sensitive. Key strategies include product differentiation via finishing and inserts, cost leadership through scale procurement, and service integration encompassing design, digital print, and fulfillment. Emerging models include converter-brand partnerships and subscription packaging for DTC candle brands.

Key Industry Developments:

- In March 2025, Yankee Candle completed the acquisition of Chesapeake Bay Candle, consolidating premium candle brands and expanding its boxed packaging portfolio to meet rising demand for luxury candle boxes.

Companies Covered in Candle Box Market

- WestRock

- Smurfit Kappa

- International Paper

- DS Smith

- Mondi Group

- Graphic Packaging International

- Packaging Corporation of America

- Stora Enso

- Sappi Limited

- Nippon Paper Industries

- Nine Dragons Paper

- Oji Holdings

- Mayr-Melnhof Karton

- Cascades Inc.

- Clearwater Paper Corporation

- Sonoco Products Company

- Georgia-Pacific

- AR Packaging

Frequently Asked Questions

The global candle box market is estimated to be valued at approximately US$3.9 billion in 2026.

By 2033, the candle box market is projected to reach around US$5.6 billion, driven by structural packaging upgrades, sustainability mandates, and growth in artisan and DTC candle brands.

Key trends include rising adoption of lock-bottom and reinforced cartons for e-commerce durability, increased use of FSC-certified and recyclable paperboard, elimination of plastic window films in favor of fiber-based alternatives, growth of short-run digital printing for artisan brands, and premium finishing enhancements such as embossing, foil stamping, and rigid box formats for gifting.

By box type, mass candle boxes lead with an anticipated 62.1% share, driven by high-volume retail supply. By candle type, container/jar candles account for approximately 36.8% share, due to higher protective and branding requirements.

The candle boxes market is projected to grow at a CAGR of approximately 5.3% through 2033.

Major players include WestRock, Smurfit Kappa, International Paper, DS Smith, and Mondi Group.