- Home Care & Utilities

- Candle Jar Market

Candle Jar Market Size, Share, and Growth Forecast, 2026 - 2033

Candle Jar Market by Material (Glass, Ceramic, Others), Product Type (Straight Sided Jars, Mason Jars, Others), Capacity, and Regional Analysis for 2026 - 2033

Candle Jar Market Size and Trends Analysis

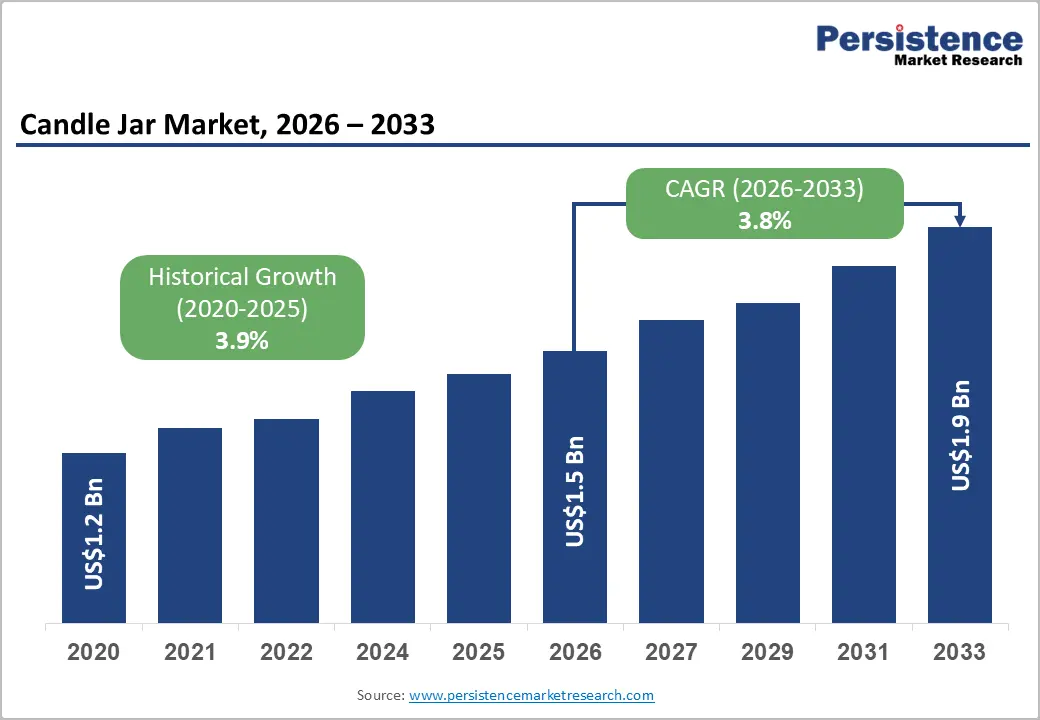

The global candle jar market size is likely to be valued at US$1.5 billion in 2026 and is expected to reach US$ 1.9 billion by 2033, growing at a CAGR of 3.8% between 2026 and 2033, driven by the rising demand for premium and scented jar candles, increased spending on home fragrance and wellness products, and a shift toward sustainable packaging solutions such as glass and ceramic jars.

Expansion is driven by innovations in jar design, e-commerce growth, and increased use in hospitality and wellness. Premium gifting demand and luxury collections boost average selling prices and repeat purchases. Sustainable materials such as recycled glass and ceramic are gaining traction due to consumer preference and regulations. Key challenges include securing glass supply, managing cost volatility, and scaling D2C and omnichannel distribution for higher-margin growth.

Key Industry Highlights

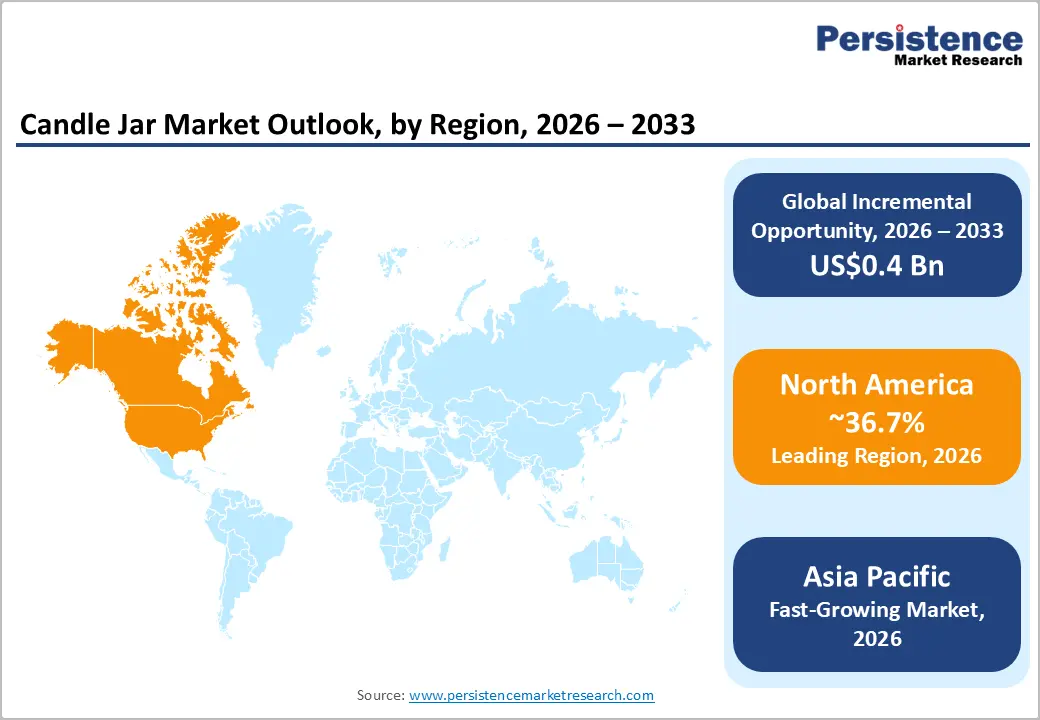

- Leading Region: North America is projected to lead the market, accounting for approximately 36.7% of revenue, supported by strong U.S. household spending on home fragrance, seasonal gifting demand, and advanced omnichannel retail infrastructure.

- Fastest-growing Region: Asia Pacific is the fastest-growing region, projected to expand at a CAGR exceeding the global average, driven by rapid urbanization, rising disposable incomes, and premium candle adoption across China, India, Japan, and ASEAN markets.

- Investment Plans: Industry investments are concentrated in refill-compatible glass and ceramic jars, recycled-content integration, and D2C logistics expansion. Private equity participation and vertical integration into jar supply chains are increasing, particularly in North America and Europe, to enhance margin control and sustainability compliance.

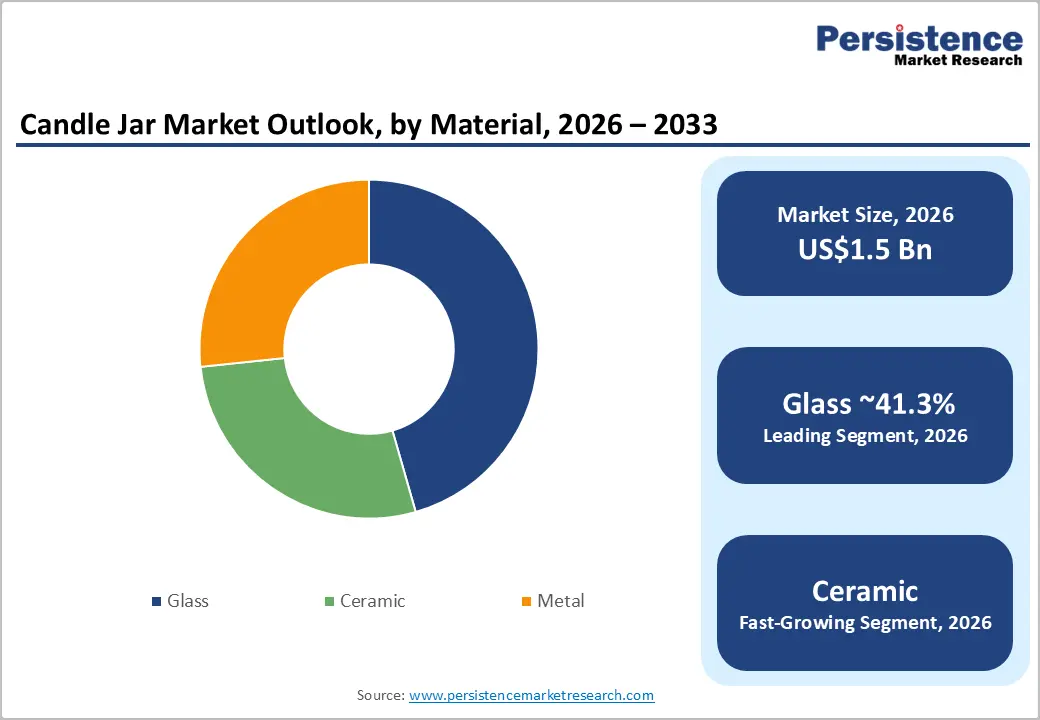

- Dominant Material: Glass jars dominate the market with an anticipated 41.3% revenue share, supported by recyclability, visual merchandising advantages, cost efficiency, and compatibility with both premium and mass-market candle formats.

- Leading Product Type: Straight-sided jars hold the largest share at approximately 35.7%, driven by manufacturing standardization, tooling efficiency, consistent shelf presentation, and strong adoption across private-label and branded SKUs.

| Key Insights | Details |

|---|---|

| Candle Jar Market Size (2026E) | US$1.5 Bn |

| Market Value Forecast (2033F) | US$1.9 Bn |

| Projected Growth (CAGR 2026 to 2033) | 3.8% |

| Historical Market Growth (CAGR 2020 to 2025) | 3.9% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Premiumization & Wellness-led Demand

Consumers in developed markets are increasingly trading up to premium scented and decorative candle jars, integrating them into home fragrance and wellness routines. Premium products, including larger-capacity jars with designer finishes, command higher average selling prices (ASPs) and increase repeat purchases, raising overall market value despite modest unit growth. Seasonal gifting, boutique hotels, and spa procurement amplify demand. Premium scented and decorative jars outperform commodity paraffin containers in value growth, demonstrating the financial impact of product differentiation and lifestyle positioning. Brands that integrate signature fragrances with visually distinctive jars benefit from higher margins and improved customer lifetime value.

Sustainability & Material Shifts

Sustainability strongly influences container selection. Glass jars, recyclable and chemically inert, dominate the market with roughly 41.3% share, offering visual appeal, premium perception, and refill potential. Regulatory frameworks emphasizing extended producer responsibility (EPR) and packaging waste reduction increase the commercial value of recyclable formats and push brands toward recycled-content glass and ceramic innovation. Take-back programs, refill initiatives, and lightweighting strategies enhance brand positioning, allow price premiums, and mitigate regulatory risks. Adoption of sustainable materials strengthens long-term supply chain resilience while appealing to environmentally conscious consumers.

Channel Expansion & D2C Acceleration

E-commerce and branded direct-to-consumer channels are expanding rapidly, leveraging visual merchandising, subscription models, and personalization options. Online platforms allow efficient testing of jar designs and limited editions, reducing promotional costs and time-to-market. Partnerships with lifestyle retailers and subscription services improve recurring revenue and inventory turnover. Success in omnichannel markets requires integrated inventory systems, premium fulfillment, and effective digital storytelling for jar design and sustainability credentials. The increasing online penetration of decorative candle channels contributes to overall market value growth.

Barrier Analysis - Raw-Material & Glass Supply Constraints

Glass feedstock and container capacity can become bottlenecks during cyclical demand surges or energy-price volatility. Glassmaking is energy-intensive, and maintenance cycles can cause temporary shortages, leading to double-digit spot price increases for specialty jars. Mid-market manufacturers unable to pass on cost increases face compressed margins, particularly for seasonal launches. These supply constraints necessitate proactive sourcing agreements and production scheduling to maintain SKU availability.

Regulatory & Compliance Costs

Evolving packaging regulations, including recycled content minimums and labeling requirements, raise compliance costs, particularly for artisanal and small-scale manufacturers. Multi-market rollouts require adherence to EPR schemes and chemical disclosure rules, imposing operational complexity. Non-compliance risks include fines and restricted retail access. These regulatory pressures create measurable operational and financial constraints, emphasizing the importance of proactive planning and centralized compliance management.

Opportunity Analysis - Refill & Reuse Business Models

Refill stations, modular jar systems, and return-for-discount programs present a structurally attractive pathway for revenue diversification and margin expansion. By separating the decorative vessel from the consumable wax refill, brands reduce recurring packaging costs while encouraging repeat purchases at a higher lifetime value per customer. Refill pods and insert systems also optimize logistics by lowering shipping weight and breakage risk compared to fully assembled jars. In urban pilot markets, in-store refill bars and subscription-based refill deliveries allow brands to test demand elasticity and operational feasibility before broader rollout. These models strengthen sustainability credentials, align with retailer recycled-content mandates, and enhance customer loyalty through incentive-based repurchase programs.

Design & Material Innovation for Premium Channels

Advanced jar design and material innovation support differentiation in luxury retail, boutique hospitality, and high-end gifting segments. Double-walled glass improves thermal performance and visual depth, while hand-applied ceramic glazes and textured specialty finishes elevate perceived craftsmanship. Limited-edition collaborations with glassmakers, ceramic ateliers, and lifestyle designers generate collectible appeal and justify premium pricing strategies. Seasonal launches featuring embossed detailing, metallic accents, or sculptural silhouettes enable brands to command higher average selling prices and strengthen brand storytelling. Investment in proprietary jar molds and design intellectual property enhances exclusivity and reduces imitation risk in competitive markets. Premium channels such as department stores, concept boutiques, and upscale hotels increasingly favor distinctive jar formats that function as décor objects beyond the candle lifecycle, extending product utility and reinforcing long-term brand equity.

High-Growth Market Expansion Strategies

Rapid urbanization, expanding middle-class populations, and increasing exposure to global lifestyle trends position Asia Pacific and selected Middle Eastern markets as high-potential growth corridors. Tiered pricing strategies that combine entry-level glass jars with premium ceramic collections allow brands to address diverse income segments without diluting positioning. Localized fragrance profiles tailored to cultural preferences improve early adoption rates, while partnerships with regional distributors and co-packers reduce initial capital intensity. E-commerce marketplaces accelerate brand entry, enabling targeted marketing campaigns and data-driven SKU optimization before physical retail expansion. Over time, establishing localized supply partnerships for glass and ceramic jars supports cost efficiency and regulatory compliance. Strategic penetration of emerging markets offers scalable volume growth, stronger geographic diversification, and long-term brand establishment in regions with above-average consumption growth trajectories.

Category-wise Analysis

Material Insights

Glass jars are anticipated to account for approximately 41.3% of market revenue in 2026, maintaining leadership due to recyclability, aesthetic flexibility, and premium perception. They are widely adopted across both mass-market and premium candle SKUs, supporting diverse shapes, finishes, embossing, frosting, and decorative coatings that enhance shelf differentiation. Transparent glass allows visible wax levels and flame presentation, which strengthens in-store merchandising and e-commerce appeal. Major home fragrance brands such as Yankee Candle and Bath & Body Works standardize glass containers across core and seasonal collections to maintain brand consistency and scalability. Glass also integrates well with refill systems and recycled-content initiatives, reinforcing its dominant position.

Ceramic and specialty jars, including stoneware, porcelain, and hand-glazed formats, are projected to register the highest CAGR over the forecast period. Growth is driven by premiumization trends, sustainability storytelling, and rising consumer preference for reusable décor-oriented containers. Ceramic vessels enable higher average selling prices and extended product life cycles, as consumers often repurpose them for storage or decorative use. Premium fragrance houses such as Diptyque and Jo Malone London frequently introduce limited-edition ceramic collections to reinforce exclusivity. The segment also benefits from collaborations with craft studios and lifestyle designers, appealing strongly to gifting and boutique retail channels. Regulatory momentum around recyclable and reusable packaging further supports ceramic and high-recycled-content specialty materials.

Product Type Insights

Straight-sided jars are anticipated to capture roughly 35.7% of market share in 2026, supported by manufacturing efficiency, cost optimization, and versatile aesthetics. Their clean cylindrical silhouette accommodates both single- and multi-wick configurations while ensuring uniform heat distribution and burn performance. Tooling standardization lowers production complexity and simplifies label application, enabling scalable private-label manufacturing. Leading candle manufacturers and private-label suppliers distribute straight-sided formats through major retailers such as Target and Walmart, where consistent shelf presentation enhances visibility. The format’s stackability and shipping efficiency also make it highly suitable for direct-to-consumer e-commerce fulfillment.

Mason jars and artisanal formats are witnessing rapid expansion, driven by craft-brand positioning, nostalgia-inspired aesthetics, and strong social-media engagement. Embossed glass, metal lids, rope handles, and hand-applied labels elevate perceived authenticity and enable premium pricing strategies. Independent and digitally native brands leverage platforms such as Etsy and curated lifestyle retailers to promote limited-edition, small-batch collections. These formats resonate particularly with urban consumers seeking personalized or gift-oriented products. The combination of storytelling, visual distinctiveness, and refill compatibility positions mason and artisanal jars as high-growth contributors within specialty and boutique distribution channels.

Regional Insights

North America Candle Jar Market Trends - Premiumization, Seasonal Retail Peaks & Refill Adoption

North America is projected to account for approximately 36.7% of the market share in 2026, positioning the region as the largest consumption hub worldwide. The U.S. represents the dominant share, supported by high per-capita expenditure on home fragrance, an established gifting culture, and well-developed specialty retail networks. Seasonal peaks during Thanksgiving and Christmas materially influence annual performance, with retailers expanding exclusive jar designs and limited-edition packaging to capture premium spending. Canada complements regional growth with strong demand for wellness-oriented and décor-driven candles, particularly in urban centers such as Toronto and Vancouver.

Premiumization remains a central growth lever. Brands such as Yankee Candle and Bath & Body Works continue to expand seasonal collections in differentiated glass formats, reinforcing higher average selling prices and repeat purchases. In 2023 and 2024, several North American premium labels accelerated refill initiatives, reflecting sustainability preferences and retailer mandates for recycled content. Nest Fragrances expanded its refillable glass candle program across department store channels, supporting circular consumption models and influencing jar design standardization.

Retail and omnichannel integration strongly shape regional performance. Mass retailers, including Target and Walmart, collaborate with private-label suppliers on exclusive straight-sided and seasonal jar SKUs to optimize shelf presentation and logistics efficiency. Direct-to-consumer brands leverage social media and subscription models to introduce artisanal and limited-edition jars, intensifying SKU innovation cycles. Regulatory oversight in North America centers on labeling compliance, product safety standards, and voluntary sustainability commitments. State-level packaging initiatives, particularly in California, encourage recycled glass adoption and influence sourcing strategies. Investment activity has increased as private equity firms target vertically integrated fragrance brands to secure margin control across wax, vessel, and distribution channels.

Europe Candle Jar Market Trends - Sustainability-Driven Design & Regulatory-Led Packaging Innovation

Europe demonstrates strong demand for premium and artisanal candle jars, supported by a mature home décor culture and sustainability-driven consumer preferences. Germany, the U.K., France, and Spain collectively anchor regional demand. Ceramic, stoneware, and high-recycled-content glass jars gain traction due to environmental awareness and regulatory compliance requirements. Germany stands out for its manufacturing base and emphasis on sustainable packaging, while the United Kingdom exhibits high penetration of premium SKUs supported by advanced e-commerce infrastructure. Luxury and design orientation significantly influence product formats. French fragrance house Diptyque continues to introduce limited-edition ceramic and decorative glass jars through flagship boutiques in Paris and London, reinforcing the premium gifting segment. Similarly, Jo Malone London emphasizes minimalist glass aesthetics and seasonal collector editions, sustaining premium price positioning across department stores such as Harrods. These launches stimulate innovation among regional glassmakers and ceramic ateliers, strengthening the specialty supply chain.

The regulatory environment is a defining market factor. European Union packaging directives and Extended Producer Responsibility (EPR) frameworks impose cost implications on non-recyclable materials while incentivizing recycled glass and reusable formats. This has prompted collaborations between candle brands and established packaging producers such as Verallia to develop lighter-weight, recycled-content vessels. Retail and boutique channels remain instrumental in driving premium trials, especially in Germany and France, where department stores and specialty décor outlets curate artisanal candle selections. Strategic investments focus on pan-European logistics optimization and artisanal consolidation, enabling small producers to scale across borders. Limited-edition jar ranges and experiential flagship store concepts launched by premium fragrance houses reinforce Europe’s position as a design-led and sustainability-focused market.

Asia Pacific Candle Jar Market Trends - Rapid Urban Growth, Luxury Expansion & Localized Manufacturing Advantage

Asia Pacific represents the fastest-growing regional market for candle jars, supported by rapid urbanization, expanding middle-class populations, and evolving lifestyle aspirations. Growth outpaces North America and Europe, offering significant headroom for premium and specialty jar penetration. China leads regional demand, particularly in tier-1 cities such as Shanghai and Beijing, where consumers increasingly adopt luxury home fragrance products. Japan emphasizes minimalist, high-quality glass and ceramic formats aligned with design sensibilities, while India and ASEAN markets demonstrate rising gifting and festival-driven consumption.

Premiumization and e-commerce expansion are central drivers. International brands such as Bath & Body Works have expanded store footprints and digital channels across India and Southeast Asia, increasing the availability of standardized glass jar collections. In China, premium labels, including Diptyque, strengthened retail presence through partnerships with high-end malls and online luxury platforms, elevating demand for decorative and refill-compatible jars. These brand expansions stimulate localized sourcing of glass and ceramic vessels to manage costs and regulatory compliance.

Manufacturing proximity provides APAC with structural advantages. China and India host extensive glass and ceramic production ecosystems, enabling cost-efficient supply of straight-sided and artisanal jars to both domestic and export markets. Compliance requirements vary across countries, with emerging chemical disclosure standards influencing labeling practices. Investment trends center on co-packing arrangements, regional licensing agreements, and private-label growth across online marketplaces. Partnerships between international fragrance houses and local suppliers for customized jar designs indicate long-term strategic commitment to APAC expansion.

Competitive Landscape

The global candle jar market is moderately fragmented at the brand level and more concentrated at the jar-glass supplier level. Global fragrance and retail brands dominate large-scale distribution, while artisanal and regional players capture niche markets. Glass and ceramic supply is capital-intensive, favoring vertically integrated strategies to secure supply and margins. Market concentration supports premium positioning, limited-edition collections, and supply-chain negotiation leverage.

Core strategies include premiumization, vertical supply agreements, and omnichannel expansion. Emerging models emphasize refill programs, limited-edition collaborations, and sustainability certification as differentiators.

Key Industry Developments:

- In April 2025, Bolsius International BV completed the acquisition of Boca Candles, expanding its production footprint in the U.S. and enhancing its devotional and jar candle portfolio.

- In March 2025, NEST New York introduced the VOYAGES by NEST line, premium eau de parfums, perfume oils, diffusers, and large-format candles, launching exclusively at Harrods and boosting its luxury candle segment expansion in Europe.

Companies Covered in Candle Jar Market

- Yankee Candle

- Bath & Body Works

- Diptyque

- Jo Malone London

- Nest Fragrances

- Lafco

- Paddywax

- Village Candle

- Colonial Candle

- BISPOL

- Bolsius

- Gala Candles

- Verallia

- Ardagh Group

- Gerresheimer

- Libbey

- Anchor Hocking

- Berlin Packaging

Frequently Asked Questions

The global candle jar market size is estimated at US$1.5 billion.

By 2033, the candle jar market is projected to reach US$1.9 billion.

Key trends include rising demand for recyclable and refillable glass jars, growing adoption of ceramic and artisanal vessels, premium limited-edition collections, expansion of direct-to-consumer (D2C) channels, and integration of sustainability mandates across packaging supply chains.

Glass jars remain the leading material segment, accounting for the highest revenue share due to recyclability, transparency, cost efficiency, and compatibility with both mass-market and premium candle formats.

The candle jar market is expected to grow at a CAGR of 3.8% through 2033.

Major players include Yankee Candle, Bath & Body Works, Diptyque, Jo Malone London, and Verallia.