- Specialty & Fine Chemicals

- Calcium Sulfate Market

Calcium Sulfate Market Size, Share, and Growth Forecast 2025 - 2032

Calcium Sulfate Market by Grade (Food, Technical, Pharmaceutical), Application (Cement, Plasterboard, Paints & Coatings, Others), End-Use Industry (Construction, Agriculture, Food & Beverages, Chemical, Water Treatment, Others), and Regional Analysis for 2025 - 2032

Calcium Sulfate Market Share and Trends Analysis

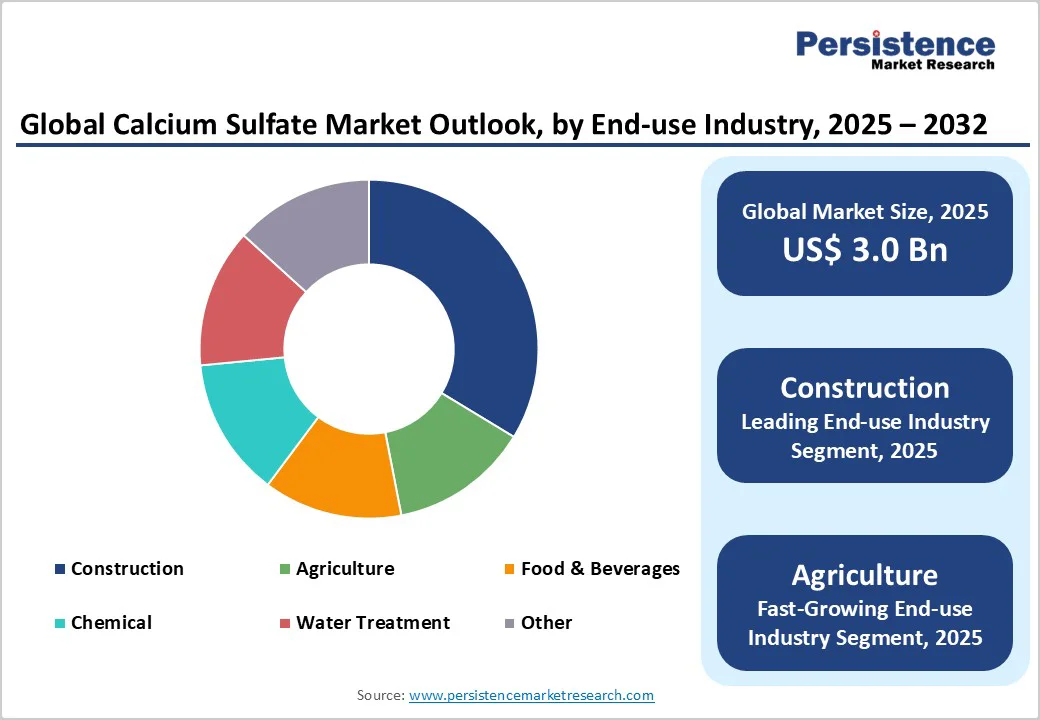

The global calcium sulfate market size is likely to be valued at US$3.0 billion in 2025, and is projected to reach US$4.8 billion by 2032, growing at a CAGR of 7.1% during the forecast period 2025-2032. The market is experiencing robust growth driven by surging demand for this compound in the construction and agriculture sectors.

Rapid urbanization and infrastructure development worldwide are key catalysts, as calcium sulfate serves as a vital component in cement and plasterboard production, enhancing material strength and durability. Furthermore, its role in soil conditioning for improved crop yields supports agricultural expansion amid global food security needs. These factors are backed by increasing investments in sustainable building practices and eco-friendly farming techniques, positioning the market for accelerated expansion through technological advancements and regulatory support for green materials.

Key Industry Highlights

- Regional Leader: Asia Pacific is poised to lead the calcium sulfate market share in 2025, driven by China's manufacturing scale and India's rapid urbanization.

- Leading End-Use Industry: Construction is set to dominate in 2025, with a substantial market share, driven by calcium sulfate's role in gypsum boards and cement for building projects.

- Fastest-growing Regional market: Europe is slated to be the fastest-growing regional market from 2025 to 2032, on account of an increasingly strong emphasis on the use of sustainable construction materials under the Green Deal of the European Union (EU)

- Growth Opportunity: Key market opportunity lies in expanding synthetic gypsum applications, leveraging policies such as the EU Green Deal for eco-friendly construction and generating revenue in emerging green building sectors.

| Key Insights | Details |

|---|---|

|

Calcium Sulfate Market Size (2025E) |

US$3.0 Bn |

|

Market Value Forecast (2032F) |

US$4.8 Bn |

|

Projected Growth CAGR (2025-2032) |

7.1% |

|

Historical Market Growth (2019-2024) |

4.4% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Massive Growth of the Construction Industry to Boost Market Expansion

The exponential growth of the construction sector is a primary driver of the calcium sulfate market, fueled by global urbanization. According to the United Nations, urban populations are projected to reach 68% by 2050, driving massive infrastructure projects that rely on calcium sulfate for plasterboard and cement applications. This mineral enhances material binding and fire resistance, making it indispensable for residential and commercial buildings. Furthermore, its cost-effectiveness compared to alternatives reduces overall project expenses, encouraging wider adoption. The integration with sustainable building practices, such as those promoted by the U.S. Green Building Council, further amplifies its positive impact, ensuring steady demand growth.

The role of calcium sulfate in agriculture as a soil amendment is driving market growth, as the compound addresses nutrient deficiencies and improves soil structure. This leads to higher crop yields, with studies in agricultural journals showing up to a 25% improvement in root development for crops such as corn and soybeans. In emerging economies, where fertile land is under pressure, the use of calcium sulfate supports sustainable farming by reducing erosion and promoting water retention. Regulatory bodies such as the European Commission (EC) also endorse such amendments for eco-friendly practices, fostering market expansion through increased adoption in precision agriculture.

Fluctuations in Raw Material Prices to Hamper Market Stability

Volatile raw-material prices, particularly for natural gypsum, pose a significant restraint on the calcium sulfate market, disrupting supply chains and increasing production costs. Data from the U.S. Geological Survey (USGS) indicates that gypsum prices have fluctuated annually over the last few years due to mining disruptions and geopolitical tensions that have affected global trade. This instability forces manufacturers to pass on costs to end users, potentially reducing demand in price-sensitive sectors such as construction. In regions reliant on imports, such as Europe, supply shortages have led to a notable drop in production efficiency. Besides this, competition from synthetic alternatives, while beneficial, has added complexity to pricing strategies, leading stakeholders to conclude that it has a negative impact on long-term market predictability and investment.

Furthermore, environmental regulations on mining activities are a major barrier, restricting access to natural gypsum deposits and increasing compliance costs. The European Environment Agency (EEA) reports that stricter emission standards have reduced mining output, owing to requirements for land rehabilitation and pollution control. This has negatively affected supply, leading to higher prices and potential shortages for industries dependent on calcium sulfate. In North America, similar policies by the U.S. Environmental Protection Agency (EPA) have delayed projects, leading to a tangible decline in operational mines in recent years. These constraints convince market participants of reduced profitability and innovation hurdles, as resources are diverted to regulatory adherence rather than expansion.

The shift toward synthetic gypsum presents substantial opportunities for market participants, driven by environmental policies favoring sustainable alternatives. The Synthetic Gypsum Market is expanding as flue gas desulfurization processes in power plants generate high-quality byproducts, with production reaching 15.4 million tons in the U.S. alone, per USGS data. This creates demand for eco-friendly plasterboard in construction, which is expected to grow significantly with global decarbonization efforts. Companies can capitalize by investing in recycling technologies, as recent developments show synthetic variants that reduce carbon footprints. Policies such as the EU Green Deal support this transition, positioning firms to tap into the fastest-growing segments such as green building materials and generate revenue through premium pricing for certified sustainable products.

Category-wise Analysis

Grade Insights

The technical grade is expected to dominate, holding approximately 60% of the calcium sulfate market share in 2025. This is mainly on account of the widespread use of technical grade of the compound in industrial applications requiring high purity and consistency. This leadership is further justified by its cost-effectiveness and versatility in construction materials such as cement and plaster, where it acts as a setting regulator. Moreover, its superior properties, such as low solubility and thermal stability, make it preferable over food and pharmaceutical grades for large-scale manufacturing. This prominence of the segment finds additional support from regulatory standards established by bodies such as ASTM International, ensuring quality in technical applications and sustaining its market position.

Application Insights

Plasterboard is likely to emerge as the leading application segment, capturing roughly 40% of the market in 2025, driven by its essential role in modern construction for interior walls and ceilings. This position is supported by UN statistics on urbanization, which project a 68% urban population by 2050, boosting demand for lightweight, fire-resistant materials. Industry developments, such as enhanced formulations for acoustic performance, further justify this segment's leading position, with associations across Europe noting a significant rise in plasterboard usage in sustainable buildings. Its advantages over cement or paints include faster installation and recyclability, making it ideal for high-volume projects.

End-Use Industry Insights

Construction is slated to be the dominant end-use industry, with an estimated 50% market share in 2025, owing to calcium sulfate's integral functionality in building materials such as gypsum boards and cement. This is backed by global infrastructure investments, where the World Bank (WB) reports annual spending exceeding US$ 2 trillion, necessitating reliable additives for strength and durability. Its adoption is further justified by performance data showing 20% improved fire resistance in structures, as per safety standards from the National Fire Protection Association (NFPA). The growth of the segment is also propelled by the unprecedented scale of urbanization in developing economies, ensuring sustained demand over alternatives in the agriculture or food sectors.

Regional Insights

North America Calcium Sulfate Market Trends

The North American calcium sulfate market is characterized by strong leadership from the U.S., where regulatory frameworks such as those from the EPA promote sustainable mining and synthetic production. Innovation ecosystems, including partnerships with tech firms, have enabled advanced applications in construction, with USGS data showing a 2024 gypsum supply of 42.8 million tons. This supports eco-friendly building trends, enhancing market dynamics. Apart from this, the focus of the stakeholders in the regional market on high-purity grades for pharmaceuticals and food has further stimulated novel trends, with recent developments in soil amendments improving agricultural efficiency, as noted in several agrarian journals. These factors underscore North America's role in fostering innovation and compliance-driven growth.

Europe Calcium Sulfate Market Trends

In Europe, market trends highlight strong performance in Germany, the U.K., France, and Spain, with regulatory harmonization under the EU Green Deal emphasizing the sustainable use of essential construction materials such as gypsum. Germany's manufacturing processes have been integrating more calcium sulfate into paints and coatings, per industry news, boosting efficiency. In the U.K. and France, on the other hand, the positive recovery of the construction industry in the post-pandemic period has driven demand, while the Spanish market mainly benefits from agricultural applications. Harmonized standards across these countries facilitate cross-border trade, with the European Environment Agency reporting reduced emissions through synthetic alternatives, supporting overall market resilience.

Asia Pacific Calcium Sulfate Market Trends

The market in the Asia Pacific is primarily dominated by the vast manufacturing ecosystem of China and the rapid infrastructure growth of India, complemented by ASEAN countries, where economies have been exhibiting dynamic expansion. According to UN data, China's production capacity supports a 20% rise in construction materials, leveraging low-cost natural gypsum. In Japan and India, the focus has been on agricultural innovation, with scientific and technological advances significantly improving soil quality. More importantly, the cost efficiencies and government incentives for urbanization across the region has positioned it well for continued growth, aligning with global sustainability goals.

Competitive Landscape

The global calcium sulfate market exhibits a consolidated structure, with major players such as Saint-Gobain Group and Knauf Gips KG controlling a significant portion of the market share through vertical integration and global supply chains. Companies are aggressively employing expansion strategies, such as mergers and capacity upgrades, to tap opportunities in emerging markets. Research and development trends have focused on sustainable synthetic production, while key differentiators include high-purity offerings and eco-certifications. Upcoming business models emphasize circular economy practices, recycling byproducts for cost efficiency and environmental compliance, fostering competitive edges in regulated industries.

Key Industry Developments

- In October 2025, in a New Zealand-first initiative, Hawke’s Bay piloted a plasterboard recycling trial to tackle construction waste more sustainably. The program, led by Hastings District and Napier City councils in partnership with Winstone Wallboards and local building suppliers, collects clean GIB® plasterboard offcuts in pre-labeled bags for easy on-site separation. Since May 2025, nearly 14,000 kilograms of plasterboard waste have been diverted from landfills, with the gypsum and paper components separated, recycled, and remanufactured into new plasterboard.

- In June 2025, Louisiana began considering a bill to repurpose gypsum waste from the phosphate industry into a valuable agricultural resource. The legislation aims to encourage the use of gypsum waste as a soil amendment, improving soil structure, reducing erosion, and enhancing nutrient availability for crops. This initiative promotes sustainable waste management by diverting industrial byproducts from landfills and supporting farmers with a cost-effective solution to improve soil health. If passed, the bill could foster collaboration between industry and agriculture, boosting environmental benefits and farm productivity across the state.

- In April 2025, a new calcium sulfate fertilizer plant opened in Illinois, enhancing the supply of this essential soil amendment for agriculture. The facility produces high-quality calcium sulfate, which improves soil structure, nutrient availability, and crop yields by supplying calcium and sulfur. This plant supports regional farmers by providing a locally sourced, sustainable fertilizer option to optimize soil health and agricultural productivity. The new operation signals growth in demand for specialty fertilizers that address specific soil nutrient needs while promoting sustainable farming practices.

Companies Covered in Calcium Sulfate Market

- Saint-Gobain Group

- Knauf Gips KG

- USG Corporation

- Georgia-Pacific

- Etex Group

- ACG Materials

- American Gypsum

- National Gypsum Company

- Xiamen Huilong Chemical Co.

- Boral Limited

Frequently Asked Questions

The global calcium sulfate market is projected to reach US$ 3.0 billion in 2025.

Rising intensity of construction activities and rapid urbanization in emerging economies are driving the market.

The market is poised to witness a CAGR of 7.1% from 2025 to 2032.

The expansion in synthetic gypsum production offers multiple opportunities, aligning with environmental policies for eco-friendly alternatives in construction.

Some of the key market players include Saint-Gobain Group, Knauf Gips KG, and USG Corporation.