- Specialty & Fine Chemicals

- Butyl Acetate Market

Butyl Acetate Market Size, Share, and Growth Forecast, 2026 - 2033

Butyl Acetate Market by Product Type (Normal-Butyl Acetate, Isobutyl Acetate, Sec-Butyl Acetate, Tert-Butyl Acetate), Application (Paints & Coatings, Adhesives & Sealants, Pharmaceutical, Cosmetics & Personal Care), End-User (Automotive, Construction, Packaging), and Regional Analysis for 2026-2033

Butyl Acetate Market Share and Trends Analysis

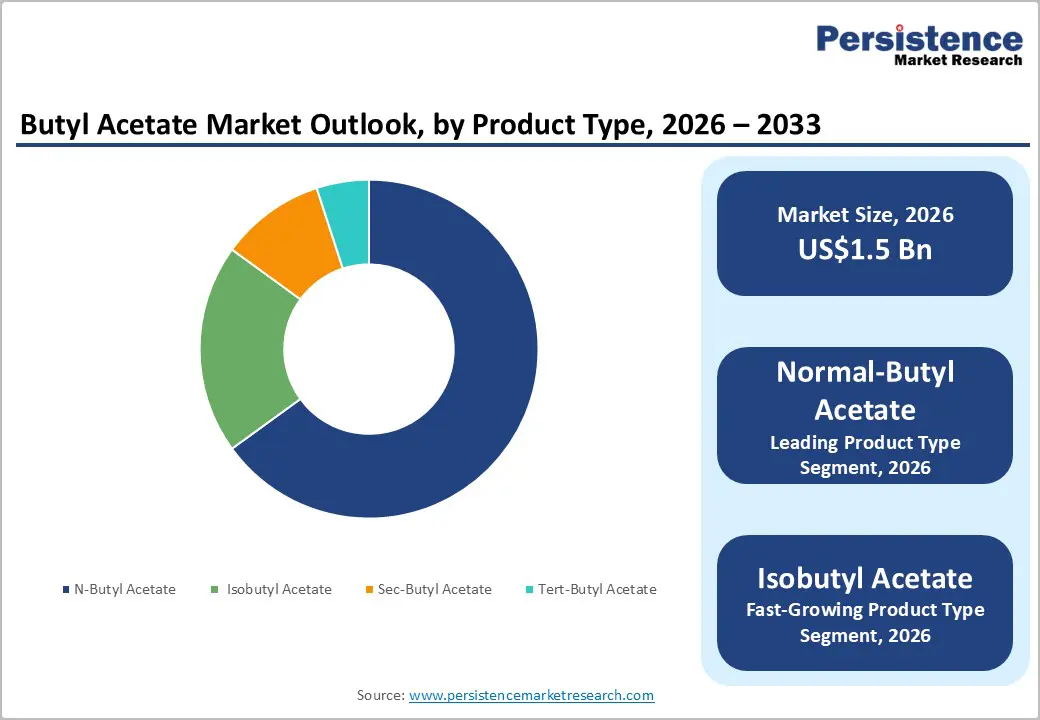

The global butyl acetate market size is likely to be valued at US$ 1.5 billion in 2026, and is projected to reach US$ 2.0 billion by 2033, growing at a CAGR of 3.0% during the forecast period 2026−2033.

Growth is occurring primarily because the coatings and paints sector is relying on butyl acetate for its balanced evaporation rate, strong solvency power, and relatively low toxicity profile. Manufacturers in automotive refinishing, wood finishing, and architectural applications are using this solvent to achieve smooth film formation and consistent surface performance.

Emerging economies are accelerating construction and industrial output, which is further supporting consumption across infrastructure and manufacturing value chains. Regulatory developments are also influencing purchasing decisions. Governments are enforcing stricter limits on volatile organic compound (VOC) emissions, and formulators are responding by adopting lower emission alternatives such as butyl acetate. This transition is encouraging companies to redesign product formulations to meet environmental standards while maintaining application efficiency. At the same time, producers are optimizing production processes to improve cost stability and supply reliability. Organizations that are aligning regulatory compliance, performance attributes, and supply chain resilience will have strengthened their competitive positioning within the evolving solvent landscape.

Key Industry Highlights

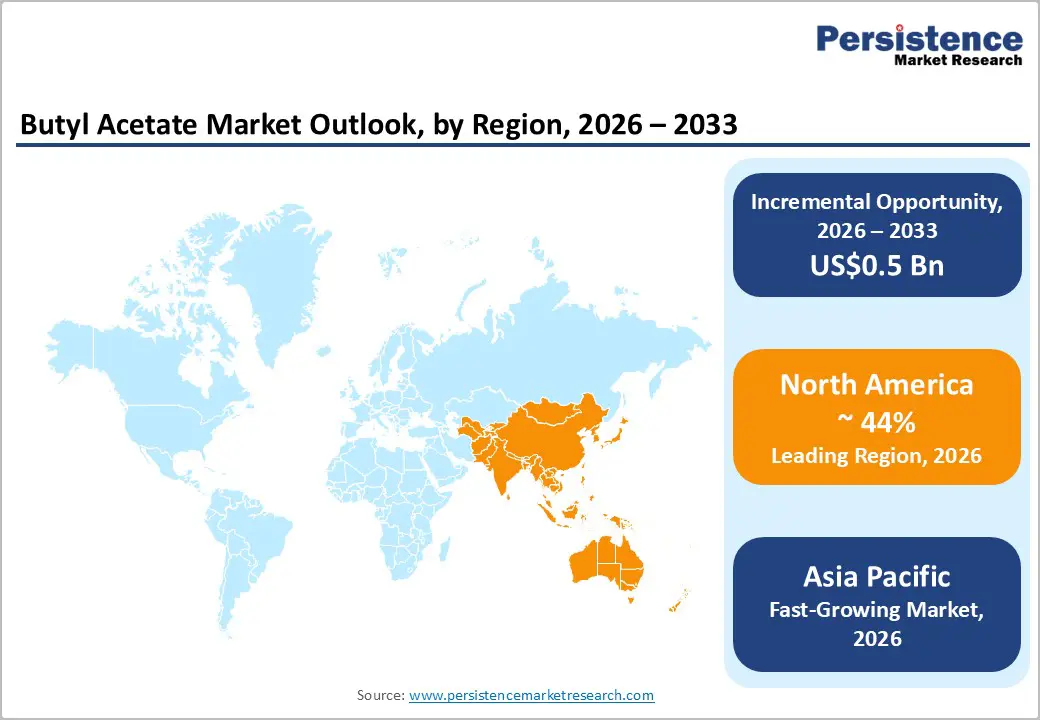

- Regional Dominance: Asia Pacific is likely to be both the dominant and fastest-growing market through 2033, holding around 44% share in 2026, supported by rapid industrialization that has transformed economies into manufacturing powerhouses.

- Leading & Fastest-growing Product Type: Normal-butyl acetate is set to lead by commanding approximately 85% of the revenue share in 2026, while isobutyl acetate is likely to be the fastest-growing segment during the 2026-2033 forecast period.

- Application Dynamics: Paints & coatings are poised to capture roughly 68% of the market revenue share in 2026, whereas adhesives & sealants are expected to grow the fastest between 2026 and 2033.

- Market Driver: The thriving global paints and coatings market drives the demand for butyl acetate, as this sector depends on the solvent due to its several standout properties.

- Market Opportunity: Innovation in coating formulations has opened the doors for specialty-grade butyl acetate, with developers engineering this variant with superior purity levels and tailored performance traits.

| Key Insights | Details |

|---|---|

| Butyl Acetate Market Size (2026E) | US$ 1.5 Bn |

| Market Value Forecast (2033F) | US$ 3.0 Bn |

| Projected Growth (CAGR 2026 to 2033) | 3% |

| Historical Market Growth (CAGR 2020 to 2025) | 2.8% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Expanding Coatings and Paints Industry

The global paints and coatings industry is serving as the central demand engine for butyl acetate. Manufacturers are selecting this solvent because it is delivering a controlled evaporation rate that minimizes surface defects during application. It is blending effectively with resins such as nitrocellulose and acrylic systems while providing strong solvency for pigments and functional additives. Formulators are incorporating it into architectural coatings designed for residential and commercial buildings, and they are deploying it in industrial formulations that safeguard equipment and structural assets. These performance attributes are ensuring uniform film formation under varied environmental conditions, including elevated humidity and temperature fluctuations.

Asia Pacific is accelerating consumption as construction activity is expanding across urban and infrastructure segments. Countries such as China and India are advancing housing developments and public works projects, which are increasing requirements for decorative and protective finishes. The automotive sector is also supporting incremental demand as vehicle production and refinishing services are progressing. In this context, butyl acetate is enabling strong adhesion and sustained color stability in repair and customization applications.

End users are benefiting from dependable sourcing channels and adaptable formulation options. Key market players are negotiating structured supply agreements and pursuing product optimization strategies to secure long term value within this evolving solvent landscape.

Competition from Bio-Based and Alternative Solvents

Bio-based solvents are creating a measurable substitution risk for butyl acetate as sustainability priorities are reshaping procurement criteria. Producers are sourcing alternatives such as ethyl acetate and propyl acetate from renewable feedstock derived from agricultural residue and bio processing streams. Coating manufacturers are adopting these options to meet carbon reduction objectives and demonstrate environmental accountability across production cycles. Formulators are testing these substitutes within established recipes to maintain application performance while lowering lifecycle emissions.

Buyers are increasingly requesting validated sustainability credentials, which is compelling traditional solvent suppliers to refine portfolios. In response, companies are developing optimized blends that preserve solvency strength and drying characteristics while reducing environmental impact.

Water-based coating technologies are further reducing reliance on organic solvents across several applications. These systems are gaining traction in architectural projects because they are supporting improved indoor air quality standards. Industrial facilities are implementing them to comply with tightening environmental regulations. Although certain constraints remain in areas such as durability and surface finish, adoption is progressing steadily in mature markets.

Forward-looking organizations are investing in research partnerships and diversifying raw material sourcing to strengthen resilience. Through early adaptation and technical collaboration, companies are positioning themselves to sustain competitiveness in a market that is steadily transitioning toward lower emission solutions.

Technological Advancements in Formulation Chemistry

Advances in coating science are creating new opportunities for specialty grade butyl acetate with enhanced purity and application specific attributes. Developers are engineering refined variants that support high solid formulations designed to reduce VOC emissions while maintaining workable viscosity during application. These systems are preserving ease of handling without compromising surface finish. Butyl acetate is enabling precise solvent balance within complex resin matrices and is stabilizing advanced polymer combinations used in performance driven coatings.

Manufacturers are targeting specialized segments where commodity grades cannot meet stringent technical specifications for gloss retention, film integrity, and chemical resistance.

Hybrid coating platforms are expanding this addressable scope by combining conventional chemistries with emerging material technologies. Researchers are designing systems that require solvents capable of interacting effectively with diverse resin families across multiple application methods, including spraying and dipping. In certain powder coating workflows that incorporate liquid components, butyl acetate is fulfilling specific functional requirements related to dispersion and adhesion.

Suppliers are positioning themselves as formulation partners by offering customized blends aligned with evolving performance benchmarks. Strategic players are investing in collaborative development programs to ensure solvent compatibility with next generation coatings. Buyers are prioritizing innovation focused suppliers to secure adaptable solutions that will have strengthened operational resilience in increasingly competitive markets.

Category-wise Analysis

Product Type Insights

Normal butyl acetate is poised to be the leading product type in 2026 with an estimated 85% revenue share, owing to its balanced performance profile. This variant is delivering an optimal evaporation rate, strong solvency strength, and cost efficiency, which is making it the preferred option for general purpose coating applications. Its dominance is supported by established production infrastructure, mature supplier networks, and broad regulatory acceptance across key regions. Producers are benefiting from scale efficiencies in normal butyl acetate manufacturing, which is enabling competitive pricing and supporting penetration in cost sensitive end use industries.

Isobutyl acetate is expected to be the fastest expanding segment during the 2026-2033 forecast period, as its demand is rising in specialized applications. Industries such as coatings, cosmetics, and personal care are adopting this variant for targeted formulations. Isobutyl acetate offers lower viscosity and a mild fruity odor, which is making it suitable for perfumes, fragrances, nail care products, and other beauty applications. Premium product positioning within the cosmetics sector is driving incremental uptake as consumers are prioritizing refined sensory attributes.

Formulators are selecting isobutyl acetate to achieve desired texture and scent performance, while suppliers are aligning capacity and distribution strategies to capture growth emerging from evolving beauty and personal care trends.

Application Insights

Paints and coatings are likely to dominate in 2026, capturing approximately 68% of the butyl acetate market revenue share, fueled by a consistent demand from the construction and automotive industries for high performance surface treatments. Infrastructure projects are requiring durable finishes that resist weathering and mechanical wear, while vehicle manufacturers are applying long lasting refinish layers that preserve color depth and surface integrity. Butyl acetate is supporting these needs through strong solvency strength that dissolves resins efficiently and promotes uniform film formation.

It is accelerating drying cycles to improve throughput and is enhancing gloss and visual appeal. Formulators are incorporating it into nitrocellulose and acrylic systems to achieve smooth flow, stable adhesion, and dependable results under demanding service conditions.

Adhesives and sealants are expected to register the fastest expansion over the 2026-2033 forecast period, driven by the growing focus of manufacturers on developing advanced bonding solutions. This solvent is dissolving polymers and resins to create homogeneous blends that improve spreadability and bonding strength. Packaging producers are requiring flexible seals that withstand moisture and mechanical stress, automotive assemblers are depending on resilient joints that tolerate vibration, and construction firms are adopting weather resistant gap fillers.

Product developers are engineering high strength formulations that respond to these performance demands. In such systems, butyl acetate is enhancing tack development and supporting efficient curing, thereby reinforcing its relevance in next generation adhesive technologies.

End-User Insights

The construction sector is slated to be the leading end user, accounting for an estimated 42% of the butyl acetate market share in 2026. Builders are applying the solvent in paints, coatings, and adhesive systems that protect structures from moisture, corrosion, and environmental stress. Rapid urbanization in developing economies is accelerating residential and infrastructure projects, which is increasing the need for durable and visually appealing finishes across housing, commercial complexes, and industrial facilities.

Contractors are selecting butyl acetate because it is dissolving resins uniformly, enabling smooth film formation and reliable surface coverage. Its evaporation profile is also supporting faster drying, which is helping reduce project timelines and improve on site efficiency.

The automotive industry is projected to record the highest CAGR from 2026 to 2033, as vehicle production and refinishing activities are advancing globally. Manufacturers are using this solvent in coating formulations that deliver deep gloss, color stability, and resistance to ultraviolet radiation and road contaminants. Assembly operations are incorporating it into sealants and bonding agents that must withstand heat exposure and vibration stress. Rising consumer expectations for long term durability and premium aesthetics are reinforcing this demand.

Formulators are relying on butyl acetate to dissolve complex resin systems and create homogeneous mixtures, while its rapid evaporation is enabling efficient curing cycles within high throughput production environments.

Regional Insights

Asia Pacific Butyl Acetate Market Trends

Asia Pacific is positioned as both the largest and fastest-growing regional market for butyl acetate through 2033, accounting for nearly 44% of the global demand. China, India, and several Southeast Asian economies are driving this momentum through rapid industrialization and sustained urban development. Manufacturing growth is strengthening consumption across automotive, construction, packaging, and general industrial applications. Vehicle production is requiring high performance refinish coatings and assembly adhesives, while infrastructure expansion is increasing the need for durable architectural finishes.

Broader manufacturing activity is also utilizing solvents in inks, sealants, and surface treatment processes, thereby creating diversified demand streams that extend into specialty sectors such as pharmaceuticals.

China is serving as both a major producer and a primary consumer, supported by integrated production facilities that benefit from domestic raw material availability. Policy initiatives are encouraging chemical sector expansion to reinforce export competitiveness and domestic supply resilience. At the same time, regulatory frameworks are tightening to align with international environmental standards, prompting formulators to transition toward compliant solvent blends. Japan is emphasizing high purity grades tailored for advanced technology and healthcare applications.

Competitive dynamics are combining multinational participation with strong regional manufacturers that are expanding capacity and strengthening upstream integration. Global and regional players operating in Asia Pacific need to monitor capacity additions, regulatory evolution, and regional supply hubs to better position themselves to secure stable sourcing and long-term commercial advantages.

Europe Butyl Acetate Market Trends

Europe is expected to maintain a solid position in the global market for butyl acetate through 2033, on the back of a technologically advanced coatings industry and stable industrial demand. Countries such as Germany, United Kingdom, France, and Spain are leading regional consumption across industrial finishes, automotive refinish systems, and architectural paints. Mature manufacturing ecosystems are prioritizing technical performance and environmental responsibility.

Machinery producers in Central Europe are applying protective coatings to safeguard equipment, while automotive assemblers are specifying premium finishes that enhance gloss retention and durability. Furniture manufacturers across northern and southern markets are also relying on wood coatings that combine aesthetic quality with surface protection.

Regulatory governance is shaping strategic decisions through harmonized compliance requirements. The Registration, Evaluation, Authorisation and Restriction of Chemicals (REACH) framework and the Industrial Emissions Directive (IED) are requiring comprehensive safety documentation and cleaner production practices. Producers are maintaining detailed substance profiles to secure approvals and ensure formulation compatibility with evolving standards. Competitive dynamics include multinational chemical companies with extensive distribution networks alongside specialized traders serving cross border niches.

Investment is flowing toward renewable feedstock sources and sustainable chemistry initiatives to reduce lifecycle emissions. Market stakeholders are benefiting from access to verified low impact solvent options, while strategic planners are aligning with suppliers that actively monitor regulatory updates and invest in continuous compliance adaptation.

North America Butyl Acetate Market Trends

North America is poised to secure a meaningful share of the global butyl acetate consumption, with the United States spearheading regional demand through its established coatings and industrial manufacturing base. Applications are spanning architectural paints for residential and commercial buildings, automotive refinishing for aging vehicle fleets, and specialty coatings for aerospace components. Construction activity is sustaining solvent use as builders are applying weather resistant finishes across housing developments, particularly in high growth southern states.

Automotive repair centers are requiring consistent refinishing materials, while aerospace manufacturers are specifying high purity grades for precision parts. Formulators are selecting butyl acetate because it is delivering dependable solvency strength across these performance driven applications.

Regulatory oversight is shaping competitive positioning through stringent emission standards. The U.S. Environmental Protection Agency (EPA) is enforcing VOC limits, and state level authorities such as the South Coast Air Quality Management District (SCAQMD) are advancing tighter regional requirements. Producers are responding by developing lower emission blends that maintain application efficiency and surface quality. Vertically integrated suppliers are leveraging upstream control to stabilize input costs, particularly along the Gulf Coast where feedstock availability and logistics infrastructure provide structural advantages.

Buyers are negotiating long term agreements with compliant producers to secure supply continuity and mitigate regulatory risk in an evolving policy environment.

Competitive Landscape

The global butyl acetate market structure is moderately consolidated, with leading multinational producers shaping competitive intensity and pricing dynamics. Key participants include BASF SE, Celanese Corporation, Eastman Chemical Company, and INEOS Group. These corporations are competing alongside regional manufacturers, creating a landscape marked by strong rivalry and strategic positioning. Market leaders are strengthening their portfolios through development of differentiated solvent grades tailored to specific performance requirements in coatings, adhesives, and specialty applications. At the same time, partnerships and collaborative agreements are enabling technology exchange and broader geographic reach.

Consolidation efforts, including mergers and acquisitions, are supporting scale efficiencies and operational integration. Producers are expanding production facilities to enhance capacity utilization and are investing in research and development to improve process efficiency and cost optimization. Distribution network enhancements are ensuring faster and more reliable supply to downstream industries. Although the market retains elements of fragmentation, top players are capturing a substantial share of overall sales through integrated value chains and global logistics capabilities. Buyers are benefiting from multiple sourcing avenues, while strategic planners are closely monitoring expansion strategies and innovation pipelines to align with stable and performance focused supply partners.

Key Industry Developments

- In February 2026, Godavari Biorefineries Limited (GBL) entered into a strategic partnership with Synthomer to develop and commercialize bio-based alternatives to conventional fossil-based monomers, including bio-based butyl acrylate produced from bio-based butanol supplied by GBL. This collaboration is supporting the chemical industry’s shift toward renewable feedstock and lower-carbon raw materials.

- In December 2025, the SOLRESS initiative advanced an integrated biorefinery project in Valencia, Spain, to produce five key industrial solvents, including bio-based butyl acetate, from second-generation biomass waste such as coffee grounds and lignocellulosic feedstock to support safer and greener chemical alternatives.

- In July 2025, BASF SE reached mechanical completion of its glacial acrylic acid and butyl acrylate plants at its new Zhanjiang Verbund site in Zhanjiang, marking a key construction milestone. This development strengthens BASF’s integrated production capacity for essential intermediates used in adhesives, coatings, and other industrial materials across Asia Pacific.

Companies Covered in Butyl Acetate Market

- BASF SE

- Celanese Corporation

- Eastman Chemical Company

- INEOS Group

- Mitsubishi Chemical Corporation

- Sasol Limited

- Jiangsu Ruijia Chemistry Co., Ltd.

- Yankuang Group

- Oxea GmbH

- KH Neochem Co., Ltd.

- Saudi International Petrochemical Company

(Sipchem) - Chemicals Incorporated

- Yip's Chemical Holdings Limited

- Novasol Chemicals

- Hefei TNJ Chemical Industry Co., Ltd.

Frequently Asked Questions

The global butyl acetate market is projected to reach US$ 1.5 billion in 2026.

Skyrocketing demand from paints, coatings, adhesives, and construction, led by the massive industrialization scale of Asia Pacific, is driving the market.

The market is poised to witness a CAGR of 3% from 2026 to 2033.

Formulation of bio-based variants, electronics adhesives, and emerging market infrastructure projects offer strong opportunities.

BASF SE, Celanese Corporation, Eastman Chemical Company, and INEOS Group are some of the key players in the market.