- Specialty & Fine Chemicals

- P-Tert-Butylphenol Market

P-Tert-Butylphenol Market Size, Share, and Growth Forecast, 2025 - 2032

P-Tert-Butylphenol Market by Form Type (Liquid, Solid), Application (Resins, Pharmaceuticals, Agricultural Chemicals, Personal Care Products, Industrial Manufacturing), End-use (Chemical Industry, Construction, Automotive Industry, Consumer Goods, Aerospace), and Regional Analysis for 2025 - 2032

P-Tert-Butylphenol Market Size and Trend Analysis

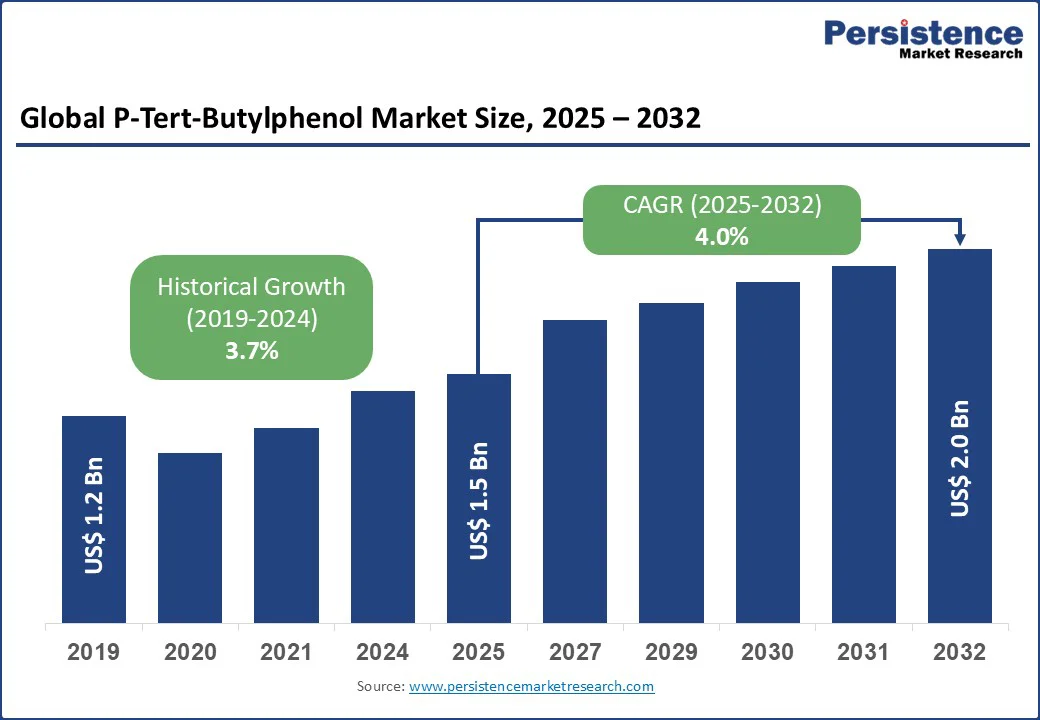

The global P-tert-butylphenol market size is likely to be valued at US$1.5 bn in 2025 and is expected to reach US$2.0 bn by 2032, growing at a CAGR of 4.0% during the forecast period from 2025 to 2032.

This growth is driven by the increasing demand for phenolic resins and high-performance coatings across industries. PTBP’s role in enhancing resin durability, heat resistance, and chemical stability makes it indispensable for coatings, adhesives, and polycarbonate applications.

Key Industry Highlights:

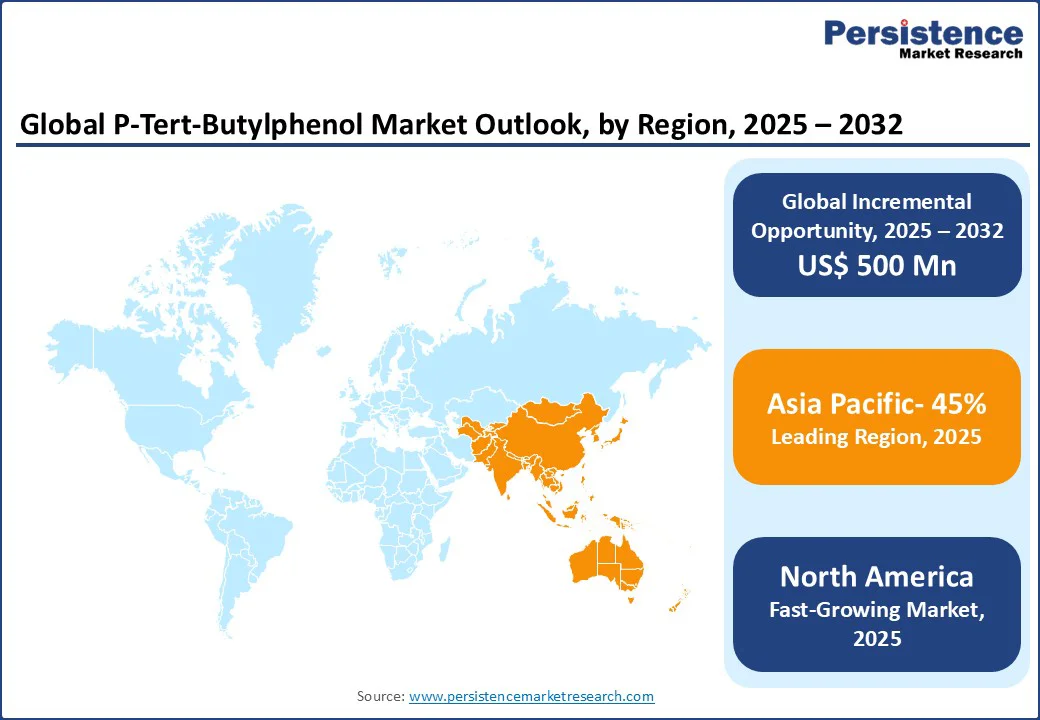

- Leading Region: Asia Pacific holds a 45% global P-tert-butylphenol market share in 2025, driven by China’s strong chemical production and industrial base, supporting high demand for PTBP in resins, coatings, and adhesives.

- Fastest-growing Region: North America is the fastest-growing market due to rising industrial manufacturing, expansion of chemical intermediate production, and increased adoption of PTBP in high-performance resins and coatings.

- Dominant Form Type: Solid PTBP leads with a 60% share, preferred for its stability, ease of storage, and extensive use in phenolic resins, adhesives, and coating applications.

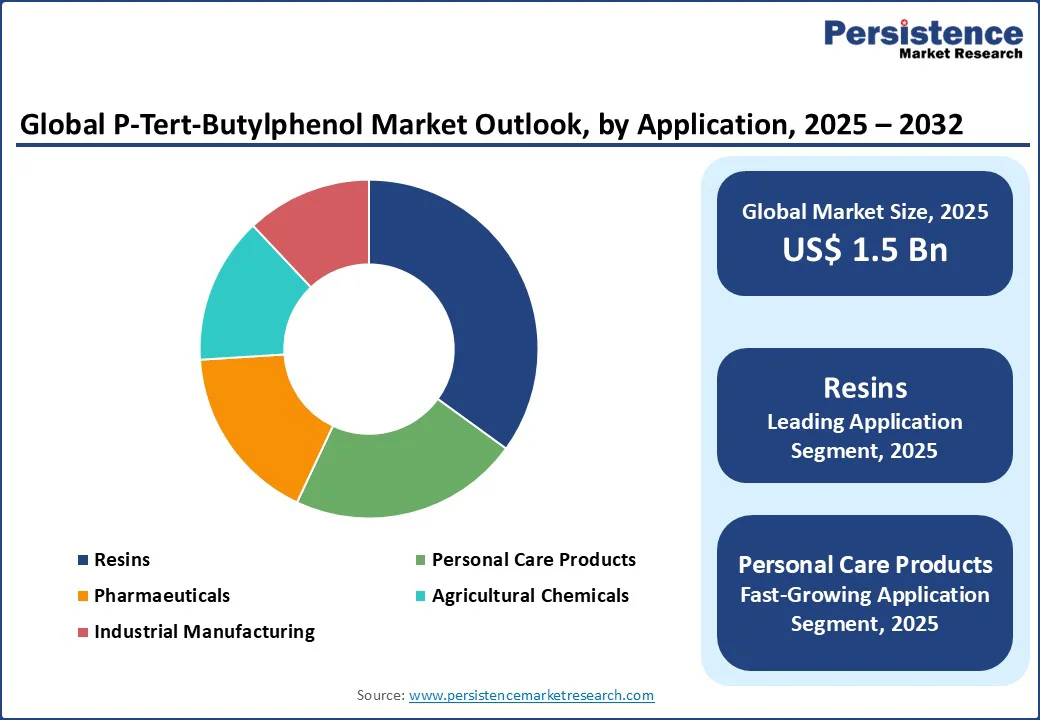

- Leading Application: Resins account for a 35% share, supported by demand in coatings, adhesives, and polycarbonate products, where PTBP enhances durability, heat resistance, and overall performance.

- Leading End-use: The chemical industry dominates with a 45% share, leveraging PTBP as a key intermediate in antioxidants, stabilizers, and other industrial chemical applications.

- Key Developments: In 2024-2025, SI Group showcased polymer additive innovations at Chinaplas 2024, while Sasol achieved first gas flow from Mozambique to South Africa; DIC Corporation terminated its PTBP facility operations.

|

Global Market Attribute |

Key Insights |

|

P-Tert-Butylphenol Market Size (2025E) |

US$1.5 Bn |

|

Market Value Forecast (2032F) |

US$2.0 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

4.0% |

|

Historical Market Growth (CAGR 2019 to 2024) |

3.7% |

Expanding chemical manufacturing in the Asia Pacific, particularly in China and India, along with use in automotive, industrial, and personal care sectors, further supports market growth. Additionally, the stability and ease of handling of solid PTBP facilitate its widespread adoption in resin-based applications, reinforcing sustained growth.

Market Dynamics

Driver: Growing Demand for Phenolic Resins and High-Performance Coatings

The P-tert-butylphenol market is witnessing significant growth driven by the rising demand for phenolic resins in high-performance coatings. These resins are prized for their exceptional heat resistance, mechanical strength, and chemical stability, making them ideal for automotive, aerospace, electrical, and construction applications.

Industries increasingly prefer phenolic resins in coatings for metal, wood, and composite surfaces, as they enhance durability, corrosion resistance, and fire retardancy. The performance characteristics of phenolic-based coatings directly align with evolving industrial standards for safety and longevity, positioning P-Tert-Butylphenol as a critical raw material.

Government regulations and initiatives promoting fire safety further stimulate market growth. For instance, the U.S. National Fire Protection Association (NFPA) 285 standard requires fire-resistant building materials in commercial construction, including coatings and laminates with high thermal stability. Compliance with such standards drives the adoption of phenolic resins in high-performance coatings, thereby increasing the demand for P-Tert-Butylphenol in multiple industrial sectors.

Restraint: Regulatory Pressures and Raw Material Volatility

The P-tert-butylphenol market faces significant restraints due to strict regulatory requirements governing chemical production and safety. Environmental regulations related to hazardous chemicals, emissions, and waste management increase compliance costs and operational complexity for manufacturers. Meeting these standards often requires additional investment in safety protocols and process adjustments, which can limit market expansion, particularly for smaller producers.

Raw material volatility further constrains growth. Prices of phenols, alkylating agents, and other intermediates are susceptible to fluctuations caused by supply-demand imbalances, geopolitical factors, and raw material scarcity. These uncertainties can impact production costs and profit margins, making large-scale adoption in high-performance applications more challenging. Companies must carefully manage sourcing and production strategies to mitigate these risks and sustain competitiveness.

Opportunity: Emerging Markets and Sustainable Formulations

The P-tert-butylphenol market is poised for growth through expanding opportunities in emerging markets. Rapid industrialization, increasing automotive production, and urban infrastructure development in regions such as the Asia Pacific, Latin America, and the Middle East are driving demand for high-performance coatings, adhesives, and resins. Rising disposable incomes and industrial investments in these regions create new avenues for P-tert-butylphenol adoption, particularly in construction, electronics, and automotive applications.

In addition, there is a growing industry focus on sustainable and eco-friendly formulations. Manufacturers are increasingly developing low-VOC and bio-based phenolic resins to meet stringent environmental standards and consumer preferences for greener products.

This trend not only aligns with global sustainability initiatives but also opens opportunities for differentiation and innovation. Companies investing in sustainable P-tert-butylphenol derivatives can capitalize on rising demand in both mature and emerging markets.

Category-wise Analysis

Form Type Insights

Solid P-tert-butylphenol (PTBP) is projected to remain the dominant type in 2025, accounting for approximately 60% market share. Its stability and extensive use in resin and coating applications make it the preferred choice for manufacturers. The solid form ensures ease of storage and handling, and a significant portion of phenolic resin production continues to rely on solid PTBP, reflecting its critical role across construction, automotive, and electrical sectors.

Liquid PTBP is emerging as the fastest-growing segment, driven by its ease of incorporation into lubricants, adhesives, and personal care formulations. Rising industrial manufacturing and the demand for versatile formulations are supporting increased adoption of liquid PTBP, complementing the continued dominance of the solid variant in various end-use applications.

Application Insights

Resins continue to lead the P-tert-butylphenol (PTBP) market, accounting for approximately 35% of global demand in 2025. Their extensive use in coatings, adhesives, and polycarbonate production underscores their importance across multiple industries.

In particular, around 60% of phenolic resin consumption is attributed to automotive and construction applications, where PTBP enhances durability, thermal stability, and chemical resistance, making it a preferred additive for high-performance industrial products.

Personal care products represent the fastest-growing application segment. Rising demand for fragrances and cosmetics, especially in the Asia Pacific region, is driving increased PTBP adoption in perfumes, lotions, and other personal care formulations. The growing preference for high-quality, stable, and long-lasting ingredients in cosmetics further supports the expansion of PTBP use in this sector.

End-use Insights

The chemical industry remains the dominant end-user of P-tert-butylphenol (PTBP), accounting for approximately 45% market share in 2025. PTBP is widely used as a chemical intermediate in the production of antioxidants, stabilizers, and other specialty chemicals. In 2024, nearly 70% of PTBP production supported chemical manufacturing, highlighting its critical role in ensuring product stability, performance, and long-term durability across various industrial applications.

The automotive industry is emerging as the fastest-growing end-use segment. Increasing global automotive production, particularly for polycarbonate components, is driving PTBP demand in coatings, adhesives, and high-performance materials. The industry’s focus on lightweight, durable, and heat-resistant materials creates new growth opportunities for PTBP, supporting its adoption in advanced automotive manufacturing and related applications.

Regional Insights

North America P-Tert-Butylphenol Market Trends

North America is emerging as the fastest-growing region for P-tert-butylphenol (PTBP), driven by increasing industrial manufacturing and demand for high-performance coatings, adhesives, and resins. The region’s well-established automotive, construction, and chemical industries are adopting PTBP for its stability, durability, and versatility in phenolic resin formulations.

Rising investments in advanced manufacturing, infrastructure development, and environmentally compliant production processes further support market growth. Additionally, stringent regulatory standards for fire-resistant and durable materials encourage the use of PTBP in coatings and composites, making North America a key growth hub for both solid and liquid PTBP across industrial and consumer applications.

Europe P-Tert-Butylphenol Market Trends

Europe holds a significant share of the P-tert-butylphenol (PTBP) market, driven by the region’s strong chemical, automotive, and construction industries. The demand for PTBP in phenolic resins, coatings, adhesives, and stabilizers is supported by strict regulatory standards for safety, durability, and environmental compliance.

Well-established manufacturing infrastructure, coupled with increasing adoption of high-performance and sustainable formulations, reinforces Europe’s position as a key market. The region’s focus on technological innovation, energy-efficient construction, and advanced automotive components continues to sustain steady demand for both solid and liquid PTBP, ensuring Europe remains a crucial contributor to global market dynamics.

Asia Pacific P-Tert-Butylphenol Market Trends

Asia-Pacific dominates the P-tert-butylphenol (PTBP) market, accounting for approximately 45% of the global share in 2025. Rapid industrialization, expanding automotive and construction sectors, and growing chemical manufacturing drive the region’s strong demand. PTBP is widely used in phenolic resins, coatings, adhesives, and stabilizers, supporting applications that require durability, heat resistance, and chemical stability.

Rising consumer demand for personal care products and increasing infrastructure investments further fuel adoption. Coupled with supportive government initiatives and the presence of major manufacturers, the Asia Pacific continues to lead the global PTBP market, making it a central hub for both solid and liquid PTBP consumption.

Competitive Landscape

The global P-tert-butylphenol market is highly competitive, driven by continuous innovation and expansion in production capacities. Manufacturers are focusing on developing high-purity and sustainable PTBP variants to meet growing demand across resins, coatings, and personal care applications.

Strategic initiatives such as capacity enhancements, technological advancements, and regional expansions are shaping market dynamics. Companies are also investing in research for environmentally friendly formulations and efficient production processes, enabling them to strengthen their market presence and cater to evolving industrial and consumer requirements globally.

Key Developments

- July 2024: SI Group showcased its latest innovations in polymer additive technologies at Chinaplas 2024, held in Shanghai, China. While the company did not announce a high-purity PTBP line for polycarbonate applications, their participation in the event highlights their ongoing commitment to advancing polymer additives.

- October 2023: DIC Corporation announced the termination of operations at its PTBP production facility, indicating a strategic shift away from PTBP manufacturing.

Companies Covered in P-Tert-Butylphenol Market

- SI Group (UK)

- Sasol (South Africa)

- Sanors (Russia)

- Tasco Group (Malaysia)

- Nainkaware Chemicals (India)

- Songwon Industrial (South Korea)

- Anshan Wuhuan Chemical (China)

- Sigma-Aldrich (USA)

- Merck Millipore (USA)

- DIC Chemical (Japan)

- Cambridge Chemical Company (UK)

- AbovChem LLC (USA)

- Aurora Fine Chemicals LLC (USA)

- Others

Frequently Asked Questions

The P-tert-butylphenol market is projected to reach US$1.5 bn in 2025, driven by resin and automotive demand.

Rising demand for phenolic resins, coatings, and sustainable formulations fuels market growth.

The P-tert-butylphenol market will grow from US$1.5 bn in 2025 to US$2.0 bn by 2032, with a CAGR of 4.0%.

Sustainable formulations and emerging market expansion drive growth in industrial applications.

Leading players include SI Group, Sasol, DIC Chemical, Songwon Industrial, and Tasco Group.