- Advanced Materials

- Polybutylene Adipate Terephthalate Market

Polybutylene Adipate Terephthalate Market Size, Share, and Growth Forecast, 2026 - 2033

Polybutylene Adipate Terephthalate Market by Grade (Extrusion grade, thermoforming grade, and miscellaneous), Application (Flexible packaging, compostable bags (shopping, garbage, industrial), agricultural mulch films, compostable food service ware, fibres & non-wovens, and miscellaneous products), and Regional Analysis for 2026 - 2033

Polybutylene Adipate Terephthalate Market Size and Trends Analysis

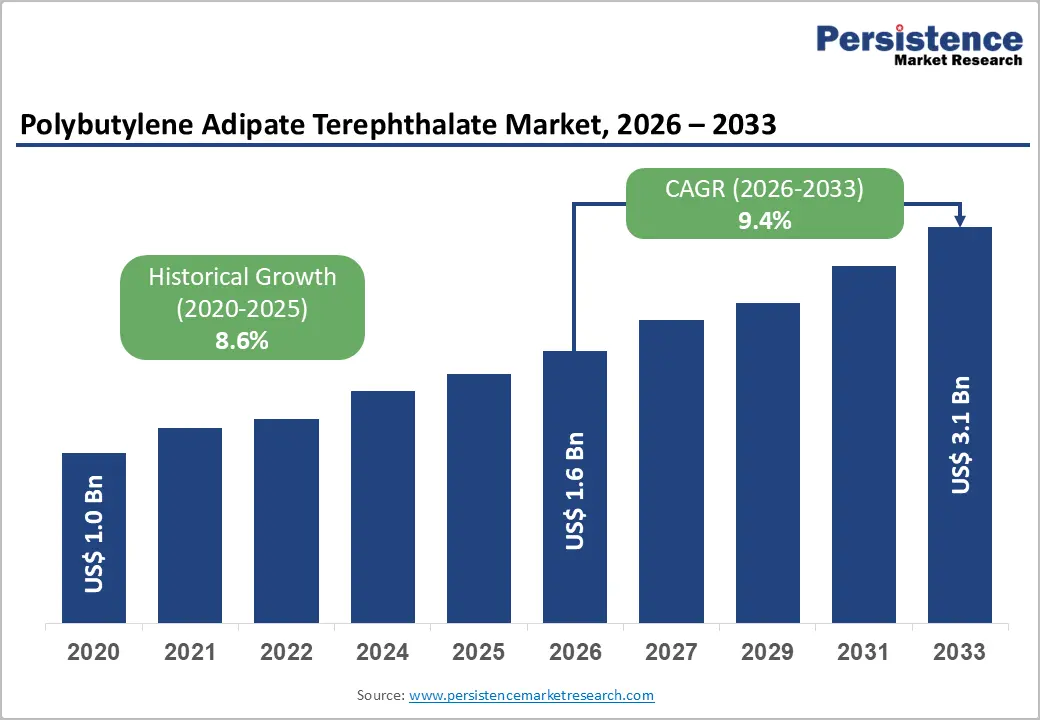

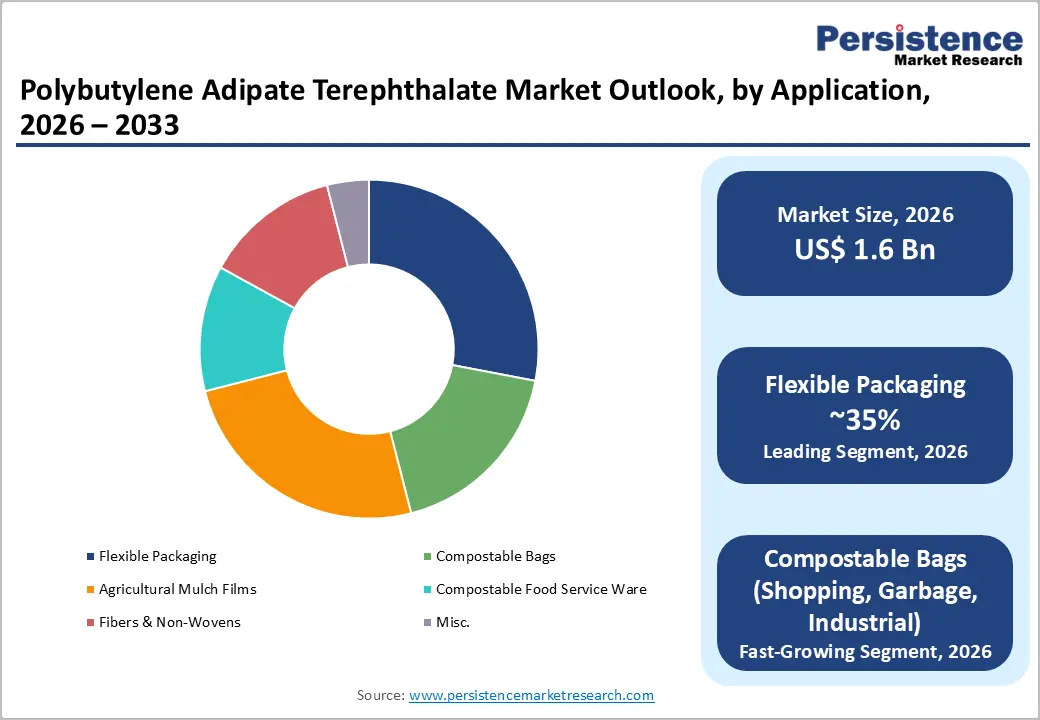

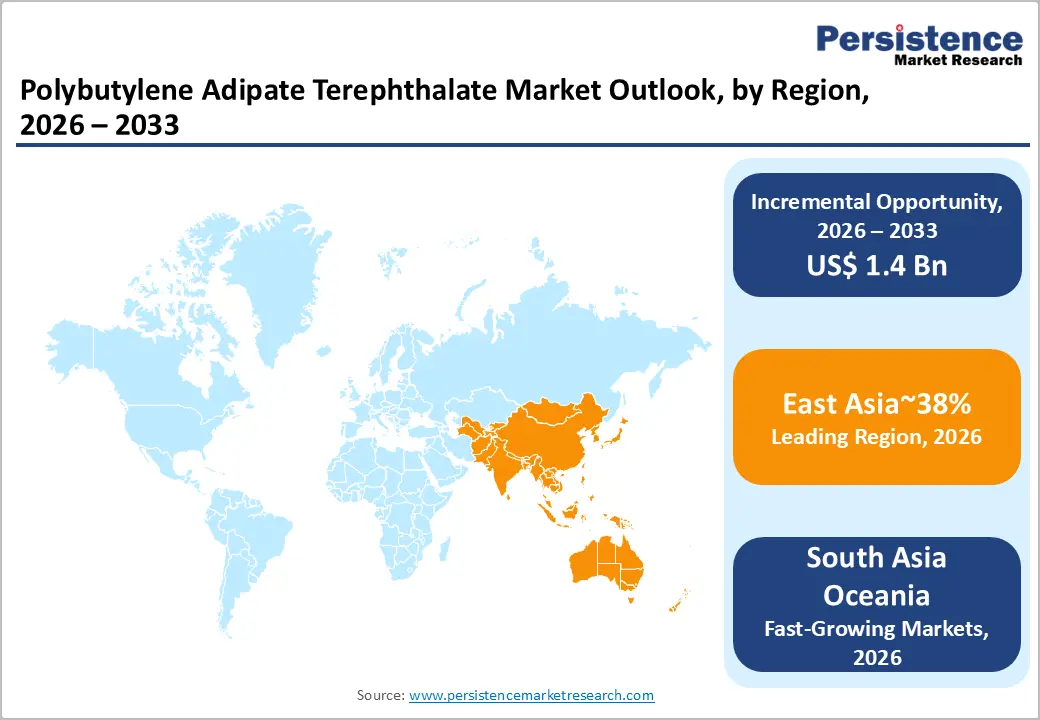

The global polybutylene adipate terephthalate market size is likely to be valued at US$ 1.6 billion in 2026 and is projected to reach US$ 3.1 billion by 2033, growing at a CAGR of 9.4% between 2026 and 2033.

The market growth recorded a valuation of US$1.0 billion in 2020, underpinned by the accelerating global shift away from conventional petroleum-based plastics toward certified compostable and biodegradable polymer alternatives. This expansion is primarily driven by stringent single-use plastic regulations across more than 100 countries, robust demand for compostable flexible packaging and agricultural mulch films, and continued innovations in PBAT-grade formulations. The growing penetration of PBAT-based compostable solutions across food packaging, agricultural films, and fiber applications, combined with rising regulatory enforcement, forms the core growth engine of this market.

Key Industry Highlights:

- Asia Pacific emerges as a leader contributing approximately 38% of global PBAT revenues, with China dominating production and policy-driven demand for biodegradable plastics.

- North America holds around 22% share, driven by a mature flexible packaging sector, state-level single-use plastic bans and corporate sustainability mandates.

- Europe accounts for about 20% share underpinned by the EU Single-Use Plastics Directive and binding food waste reduction targets, supporting PBAT adoption in compostable packaging.

- Flexible packaging is the leading application, capturing 35% of market demand, benefiting from PBAT’s combination of flexibility, strength, and certified compostability.

- Extrusion-grade PBAT dominates the product segment, representing 48% of the market due to its suitability for films, liners, and agricultural applications, while thermoforming grade grows fastest for rigid foodware.

- Regulatory bans on conventional plastics and validated biodegradability drive structural demand, particularly in food service, produce bags, and agricultural film

- Opportunities exist in bio-based PBAT grades and composting infrastructure expansion, yhjwith innovations such as BASF’s biomass-balanced ecoflex F Blend enabling carbon footprint reduction and circular economy compliance.

| Key Insights | Details |

|---|---|

| Polybutylene Adipate Terephthalate Market Size (2026E) | US$ 1.6 Bn |

| Market Value Forecast (2033F) | US$ 3.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 9.4% |

| Historical Market Growth (CAGR 2020 to 2025) | 8.6% |

Market Dynamics

Drivers - Global Regulatory Mandates Against Conventional Single-Use Plastics

Governments worldwide have enacted sweeping legislative measures to restrict single-use plastics, creating a powerful and sustained demand signal for PBAT-based biodegradable alternatives. These regulations operate as structural market compulsions rather than voluntary adoption incentives, directly redirecting procurement decisions across packaging and agriculture supply chains.

Over 100 countries have implemented single-use plastic restrictions since 2020, including the European Union's Single-Use Plastics Directive (effective 2021), which explicitly mandates compostable alternatives for regulated item categories such as cutlery, food containers, and carry bags.

In China, a phased national plastic ban launched in 2020 prohibits non-degradable plastic bags and food delivery packaging in major urban centres, stimulating a domestic biodegradable plastics market. In India, a 2022 ban covering 19 categories of single-use plastic items triggered a 28% surge in PBAT imports and, per the Central Pollution Control Board's 2023 approval, certified PBAT products received formal exemptions for single-use applications under the Plastic Waste Management Rules, prompting a 19% surge in procurement by quick-service restaurant chains. These legislative actions directly support the Polybutylene Adipate Terephthalate Market by making PBAT the material of choice in applications where product lifespan is short and compostable disposal is mandated.

Scientifically Validated Biodegradability and Circular Economy Alignment

The credibility of PBAT as a genuinely compostable material, validated by independent scientific institutions and aligned with internationally recognised standards, constitutes a foundational demand drive in both consumer and industrial markets. Unlike legacy greenwashing claims, PBAT's biodegradability credentials are underpinned by peer-reviewed science and certified performance benchmarks.

A landmark study by ETH Zürich confirmed that PBAT is metabolised by soil microbes, forming CO2, water, and biomass, proving for the first time that PBAT does not persist as microplastic. European performance standards such as EN 13432 and EN 17033, developed by European standardisation bodies, provide a regulatory framework that formally validates PBAT for home and industrial composting conditions. BASF's ecoflex® PBAT biopolymer, which celebrated its 25th anniversary in October 2023, has served as the foundational compostable polymer in certified applications since 1998, establishing long-term market credibility. In the Polybutylene Adipate Terephthalate Market, the material's ability to degrade under soil, industrial, and home composting conditions positions it as a proven circular economy enabler, directly addressing global food waste challenges where, according to the European Parliament, roughly 60 million tonnes of food are wasted annually in the EU, much of which requires compostable packaging solutions to facilitate organic waste separation and recycling.

Structural Demand from Sustainable Agricultural Applications

Agricultural plastics represent one of the most critical and structurally embedded end-use segments for PBAT, driven by the material's ability to eliminate the environmental liabilities associated with conventional polyethylene mulch films without compromising crop productivity. Globally, approximately 15.6 million tonnes of plastics were used in agricultural applications in 2021, with films for mulching, silage, and greenhouse coverings accounting for approximately 63% of non-packaging agricultural plastic use in Europe, according to the Food and Agriculture Organisation of the United Nations and Plastics Europe. FAO projections further indicate that demand for greenhouse, mulch, and silage films could increase by 50% between 2018 and 2030, reflecting the structural requirement for high-performance agricultural films and the compounding pressure to replace conventional films with certified biodegradable alternatives.

China's Jiangsu province alone allocated US$ 147 million in 2023 specifically for PBAT-modified agricultural film R&D, targeting both soil pollution mitigation and carbon emission reduction targets under the national Dual Carbon policy. Within the Polybutylene Adipate Terephthalate Market, PBAT-based mulch films such as BASF's ecovio® M 2351 eliminate post-harvest collection needs entirely, making agriculture more sustainable while simultaneously supporting food security objectives aligned with international climate frameworks.

Restraint - High Production Costs Relative to Conventional Plastics

PBAT production costs remain materially higher than those of conventional petroleum-based polymers such as polyethylene and polypropylene, limiting widespread adoption, particularly in price-sensitive markets and developing economies.

The cost differential is rooted in complex multi-step synthesis processes, the premium on bio-based or certified feedstocks, and the capital intensity of purpose-built PBAT manufacturing lines. Only 23% of India's urban composting facilities currently meet ISO 14855 standards for PBAT degradation, limiting end-of-life value realisation even where adoption occurs. In Southeast Asia, unregulated landfills account for 88% of plastic waste disposal in countries such as Indonesia and Thailand, further reducing the economic incentive for PBAT-based product lines. The combination of higher material costs and inadequate composting infrastructure constrains market penetration in high-volume, low-margin packaging applications.

Fragmented Certification Frameworks and Inconsistent Regulatory Enforcement

Despite broad regulatory intent, the absence of harmonised global certification standards creates significant compliance complexity for PBAT producers and downstream converters operating across multiple jurisdictions. While the EU harmonises standards through EN 13432, countries such as Indonesia and Brazil maintain divergent local certifications (SNI 7188.7:2023 and ABNT NBR 15448-1, respectively), forcing manufacturers to optimise formulations for regional compliance at added cost and complexity.

In the United States, plastic recycling rates remain below 6%, and inconsistent labelling regulations complicate consumer-facing compostability claims. This regulatory fragmentation slows product commercialisation timelines, increases market entry barriers, and undermines the commercial case for PBAT adoption in markets where enforcement of single-use plastic bans remains inconsistent or incomplete.

Opportunities - Bio-Based and Biomass-Balanced PBAT Grades

The development and commercialisation of bio-based and biomass-balanced PBAT grades represents a structurally significant opportunity, enabling manufacturers to address both carbon footprint reduction mandates and circular economy compliance requirements simultaneously. This opportunity is driven by converging pressures from corporate ESG commitments, mandatory product carbon footprint disclosure frameworks, and consumer demand for verifiably lower-emission packaging materials.

In June, 2024, BASF SE introduced the industry-first biomass-balanced ecoflex F Blend C1200 BMB, a PBAT grade with a 60% lower product carbon footprint compared to the standard fossil-based variant, achieved by replacing fossil feedstocks with renewable alternatives from waste biomass through a certified biomass approach. This represents a drop-in solution with identical performance characteristics and certifications, meaning converters can adopt it without process modifications. Within the Polybutylene Adipate Terephthalate Market, this development opens a premium product tier in which carbon-intensity reduction serves as a primary purchasing criterion for multinational retailers and food service operators, particularly in the European market where, according to Plastics Europe, non-fossil-based plastics reached 12.4% of European plastics production in 2021, with an EU target of 20% non-fossil carbon in plastics by 2030.

Composting Infrastructure Development in High-Growth Economies

The accelerating build-out of industrial and community composting infrastructure across high-growth economies in Asia and South Asia constitutes a tangible demand-side opportunity for PBAT market participants, as material adoption rates are directly correlated with the availability of certified end-of-life processing systems. Without functional composting infrastructure, the value proposition of compostable PBAT is structurally limited, making infrastructure investment a critical demand catalyst.

India's packaging industry was valued at US$84 billion in 2024 and is projected to reach Rs. US$ 143 Billion by 2029, reinforcing the scale of opportunity for sustainable packaging materials. In 2024, the Council of Scientific and Industrial Research launched the National Mission on Sustainable Packaging Solutions (led by CSIR-NIIST), focusing on recyclable materials, biodegradable alternatives, and advanced testing capabilities.

For the Polybutylene Adipate Terephthalate Market, this government-backed institutional commitment signals infrastructure investment that will progressively validate compostable materials on a scale. Furthermore, Swiss packaging firm SIG Group committed US$ 106 million for 2023 to 2025 and an additional US$ 50 million for Phase 2 by 2027 in sustainable packaging facilities in India, illustrating the level of private capital aligned with this infrastructure-driven opportunity.

Food Waste Reduction and Compostable Food Service Applications

Growing regulatory focus on food waste reduction creates a structurally aligned demand opportunity for PBAT-based compostable food service ware, produce bags, and food packaging formats that facilitate organic waste separation and composting at the household and institutional level. In the EU, approximately 60 million tonnes of food are wasted annually, equivalent to around 130 kg per person, with households responsible for 53% of this waste, and food waste costs estimated at approximately €132 billion annually in market value.

In September 2025, the European Parliament approved new binding food waste reduction targets for EU member states to be achieved by 2030, creating formal policy scaffolding for composting-aligned packaging solutions. PBAT-based produce bags, such as those demonstrated by BASF's ecovio® product line, have shown the ability to extend produce shelf life by up to four times compared to conventional polyethylene bags, while functioning simultaneously as organic waste collection bags to facilitate composting. In the Polybutylene Adipate Terephthalate Market, this dual functionality addressing both food waste reduction and organic waste management positions PBAT-based food service applications as directly policy-responsive, enabling material suppliers to align product development with binding legislative timelines.

Category-wise Analysis

Grade Insights

The extrusion grade segment commands the leading position in the polybutylene adipate terephthalate market, accounting nearly for 48% total grade-based market share. Extrusion-grade PBAT benefits from excellent thermal stability, consistent melt flow properties, and compatibility with standard industrial extrusion equipment, enabling manufacturers to adopt PBAT without significant capital expenditure on new processing lines. These properties make extrusion grade the preferred choice for producing compostable films, mulch films, compostable liners, and flexible packaging substrates at scale. The segment's commanding share is reinforced by the fact that the film extrusion process is the most widely deployed conversion technology across packaging and agricultural film applications, both of which represent structurally high-demand end-use categories in the PBAT value chain

The thermoforming grade segment is emerging as the fastest-growing category within the grade-based segmentation of the Polybutylene Adipate Terephthalate Market, driven by expanding demand for rigid and semi-rigid compostable food service ware, trays, and containers across the food service, retail, and institutional sectors. Thermoforming-grade PBAT is formulated to maintain dimensional stability and sufficient rigidity under controlled heating conditions, enabling the production of compostable containers, trays, and food packaging items that directly substitute single-use plastic alternatives targeted by regulatory bans.

Application Insights

Flexible packaging holds the leading application-level market share of approximately 35% in 2026, reflecting PBAT's superior combination of flexibility, toughness, and certified compostability that makes it uniquely suited to replace conventional polyethylene-based flexible formats. The U.S. flexible packaging industry recorded sales of US$ 41.5 Billion in 2022, representing approximately 21% of the total U.S. packaging market valued at US$ 180.3 Billion, illustrating the scale of the addressable conversion opportunity for PBAT-based flexible formats. A 2024 survey by Flexible Packaging Europe across 6,000 consumers in France, Germany, Italy, Spain, the United Kingdom, and Poland confirmed that lightweight convenience was valued by 42% of respondents, reinforcing the structural fit between PBAT-based flexible formats and established consumer preference patterns.

The compostable bags segment, encompassing shopping bags, garbage liners, and industrial waste bags, is the fastest-growing application category within the Polybutylene Adipate Terephthalate Market, propelled directly by legislative bans on conventional plastic carrier bags and the scalable substitution dynamic they create. EU data indicates that average consumption of lightweight plastic carrier bags fell to 65 bags per person in 2023, down 30 bags from 2018, reflecting enforcement of EU waste and plastic reduction directives. Countries including Belgium, Poland, and Austria have already met the 2025 target of fewer than 40 bags per capita, demonstrating the policy trajectory driving conversion to PBAT-based compostable alternatives.

Regional Insights and Trends

East Asia Polybutylene Adipate Terephthalate Market Trends

Asia Pacific commands the largest regional share of the Global Polybutylene Adipate Terephthalate Market, accounting for approximately 38% of global market revenues, with China serving as the world's largest PBAT manufacturing hub, contributing over 60% of total global PBAT production capacity. China's 2020 national plastic ban created the world's most consequential single-country demand stimulus for biodegradable plastics, generating a domestic market for biodegradable alternatives. With 18 new PBAT production lines commissioned in 2023 alone and Beijing enforcing non-compliance penalties on retailers in the first quarter of 2024. Jiangsu province allocated US$ 147 million in 2023 for PBAT-modified agricultural film research and development, demonstrating state-level investment commitment. The regional competitive landscape reflects a combination of large-scale domestic manufacturers and multinational PBAT producers establishing local production to serve China's, India's, and Southeast Asia's growing compostable materials markets.

North America Polybutylene Adipate Terephthalate Market Trends

North America holds approximately 22% of the global polybutylene adipate terephthalate market, representing a high-value, innovation-led market driven by corporate sustainability commitments, state-level legislative action, and a mature flexible packaging industry. The U.S. flexible packaging sector recorded sales of US$ 41.5 billion in 2022, with food packaging accounting for approximately 50% of shipments and the sector directly supporting over 85,000 jobs, underscoring the scale of the conversion opportunity for PBAT-based materials. In 2024, the World Bank introduced a seven-year, US$ 100 million principal-protected bond to finance plastic waste reduction projects, signalling institutional commitment to biodegradable alternatives at a systemic level.

The U.S. Plastics Industry Association launched its "Recycling Is Real" campaign in September 2023, though critics note that plastics recycling rates remain below 6% in the country, creating a policy and market environment increasingly favourable to certified compostable PBAT formats that provide verifiable end-of-life solutions. Regulatory momentum at the state level, including California's SB 54 mandating the reduction of single-use plastic packaging, and growing food service sector adoption of compostable ware, constitute the primary near-term demand drivers in the region.

Europe Polybutylene Adipate Terephthalate Market Trends

Europe holds approximately 20^% of the global Polybutylene Adipate Terephthalate market, with demand structurally shaped by the most comprehensive biodegradable polymer regulatory framework in the world. The EU's Single-Use Plastics Directive (2021) has directly driven PBAT capacity in Europe up by 34% since implementation, reaching 280,000 tonnes annually in 2023. Eurostat data confirms that the EU generated 79.7 million tonnes of packaging waste in 2023 at 177.8 kg per capita, with plastic packaging waste at 15.8 million tonnes, yet only Belgium and Latvia exceeded the 55% plastic packaging recycling target for 2030. This structural recycling gap directly reinforces the policy case for compostable PBAT formats as a complementary waste management solution.

Seven EU member states have already surpassed the overall 70% packaging recycling target for 2030, including Belgium, the Netherlands, Italy, Czechia, Slovenia, Slovakia, and Spain, reflecting the maturity of waste management infrastructure that validates compostable material end-of-life claims. EU food waste legislation adopted in September 2025, establishing binding food waste reduction targets for 2030, further embeds PBAT-aligned packaging solutions in European food system policy. BASF's October 2023 celebration of ecoflex®'s 25th anniversary as the world's first certified compostable PBAT biopolymer underscores Europe's position as the historic innovation center of the global PBAT market.

Competitive Landscape

The global Polybutylene Adipate Terephthalate (PBAT) market exhibits a consolidated to moderately oligopolistic competitive landscape, with a handful of large established players holding significant market share and driving innovation while numerous smaller regional producers contribute to capacity growth. Major multinational manufacturers such as BASF SE, Novamont S.p.A, Chang Chun Group, Kingfa Sci. & Tech. Co., Ltd., and GO YEN Chemical Industrial Co., Ltd. command strong positions through advanced R&D, broad product portfolios, and global distribution networks focused on biodegradable polyester solutions.

These leaders are complemented by other significant players such as Anhui Jumei Biological Technology Co., Ltd., Hangzhou Peijin Chemical Co., Ltd., and Jin Hui Zao Long High Tech Co., Ltd., particularly in Asia, where capacity expansion and cost-competitive production are shaping market dynamics. Together, these companies dominate global PBAT supply and set industry standards for performance, sustainability and compliance with biodegradability regulations, while engaging in strategic partnerships, capacity expansions and product innovations to meet rising demand. Although several India-based and other regional suppliers such as Easy Flux Polymers Private Limited, produce PBAT granules, their scale relative to global leaders remains smaller, underscoring the concentrated nature of the competitive landscape.

Key Developments:

- On November 13, 2025, BASF expanded its Polybutylene Terephthalate (PBT) portfolio in India by localizing production of Ultradur® specialty grades, including flame-retardant (FR) and hydrolysis-resistant (HR) variants, enhancing supply reliability and supporting applications in automotive, electronics, and industrial sectors with improved performance and faster delivery.

Companies Covered in Polybutylene Adipate Terephthalate Market

- BASF SE

- Chang Chun Group

- Kingfa Sci. & Tech. Co., Ltd.

- Novamont S.p.A.

- GO YEN Chemical Industrial Co., Ltd.

- Anhui Jumei Biological Technology Co., Ltd.

- Hangzhou Peijin Chemical Co., Ltd.

- Jin Hui Zao Long High Tech Co., Ltd.

- TEN Zimmer GmbH

- Mitsui Plastics, Inc.

- Zhejiang Biodegradable Biomaterials Co., Ltd.

- Hengli Group Co., Ltd.

- Junyuan Petroleum Group

- Qingdao Zhoushi Plastic Packaging Co., Ltd.

- Red Avenue New Materials Group Co., Ltd.

- CSPA Polychem Pvt. Ltd.

- Xinjiang Blue Ridge Tunhe Sci & Tech Co., Ltd.

- Tarpath Elastomers LLP

- Easy Flux (India)

Frequently Asked Questions

The global Polybutylene Adipate Terephthalate Market is projected to be valued at US$ 1.6 Bn in 2026.

The Extrusion Grade segment is expected to account for approximately 59% of the Global Polybutylene Adipate Terephthalate Market by Grade in 2026.

The market is expected to witness a CAGR of 9.4% from 2026 to 2033.

The Polybutylene Adipate Terephthalate (PBAT) market is primarily driven by global regulatory bans on single-use plastics, scientifically validated biodegradability, circular economy alignment, and structural demand from sustainable agricultural and compostable packaging applications.

Key market opportunities in the Polybutylene Adipate Terephthalate market include bio-based and biomass-balanced PBAT grades, expansion of composting infrastructure in high-growth economies, and PBAT-based compostable food service and packaging solutions aligned with food waste reduction policies.

Key players in the BASF SE, Novamont S.p.A, Chang Chun Group, Kingfa Sci. & Tech. Co., Ltd., and GO YEN Chemical Industrial Co., Ltd.