- Electric Mobility

- Bike and Scooter Rental Market

Bike and Scooter Rental Market Size, Share, and Growth Forecast 2026 - 2033

Bike and Scooter Rental Market by Vehicle Type (Bike, Scooter), Propulsion Outlook (Pedal, Electric, Gasoline), Service Outlook (Pay-as-you-go, Subscription Based, Others), and Regional Analysis for 2026 - 2033

Bike and Scooter Rental Market Size and Trend Analysis

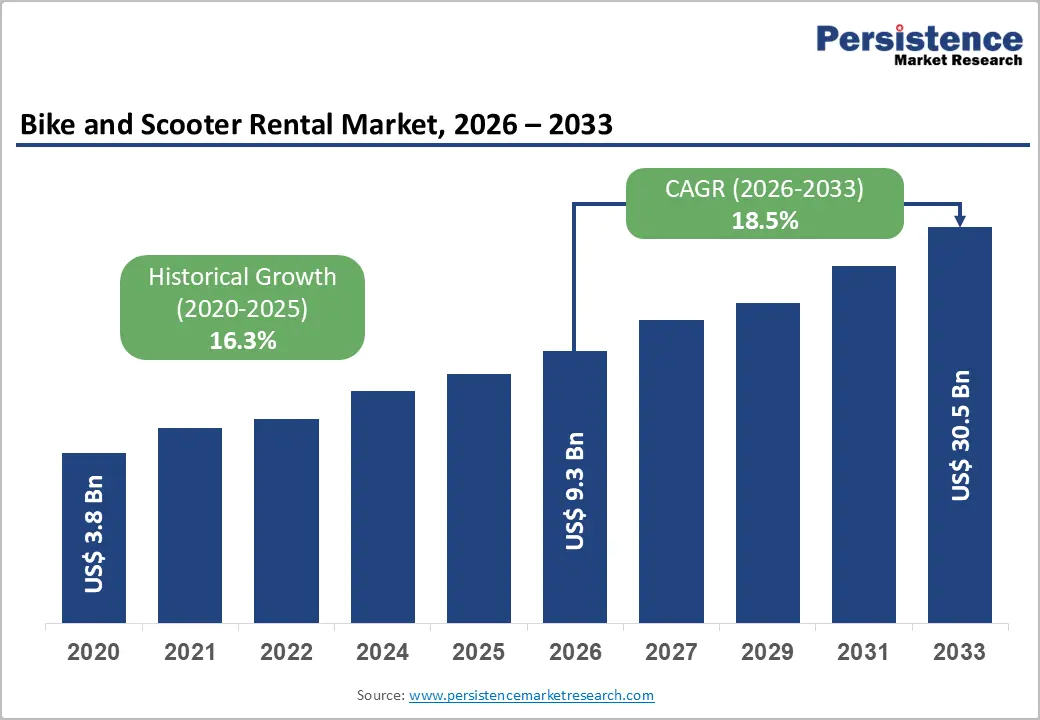

The global bike and scooter rental market size is valued at US$ 8.9 billion in 2026 and is projected to reach US$ 30.5 billion by 2033, growing at a CAGR of 18.5% between 2026 and 2033.

Rapid urbanization, mounting traffic congestion in metropolitan areas, and heightened environmental consciousness are collectively propelling the adoption of shared micro-mobility solutions worldwide. Governments across North America, Europe, and Asia Pacific are channelling investments into dedicated cycling infrastructure and last-mile connectivity programs, which directly expands the user base for bike and scooter rental services.

Key Industry Highlights:

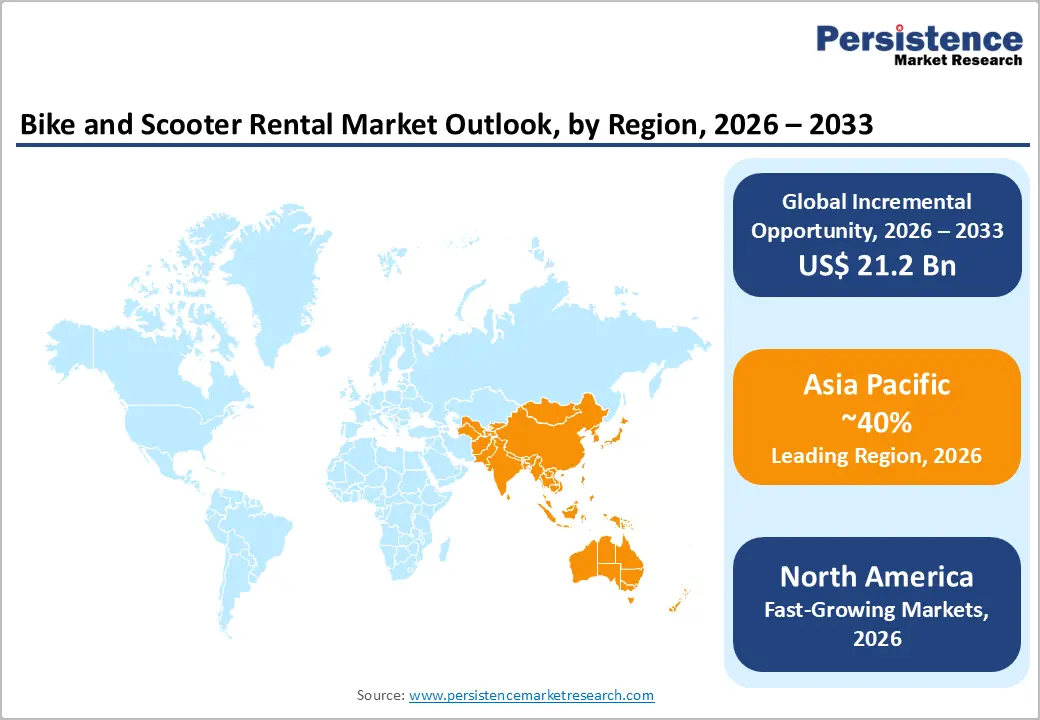

- Leading Region: Asia Pacific leads the global bike and scooter rental market, driven by China's massive fleet deployments, high urban density, and deep cultural adoption of two-wheeled transport, collectively accounting for over 40% of global rental trip volume.

- Fast-Growing Market: North America represents one of the most developed micro-mobility markets globally, driven by progressive urban transport policies, high smartphone penetration, and well-established cycling infrastructure in major cities.

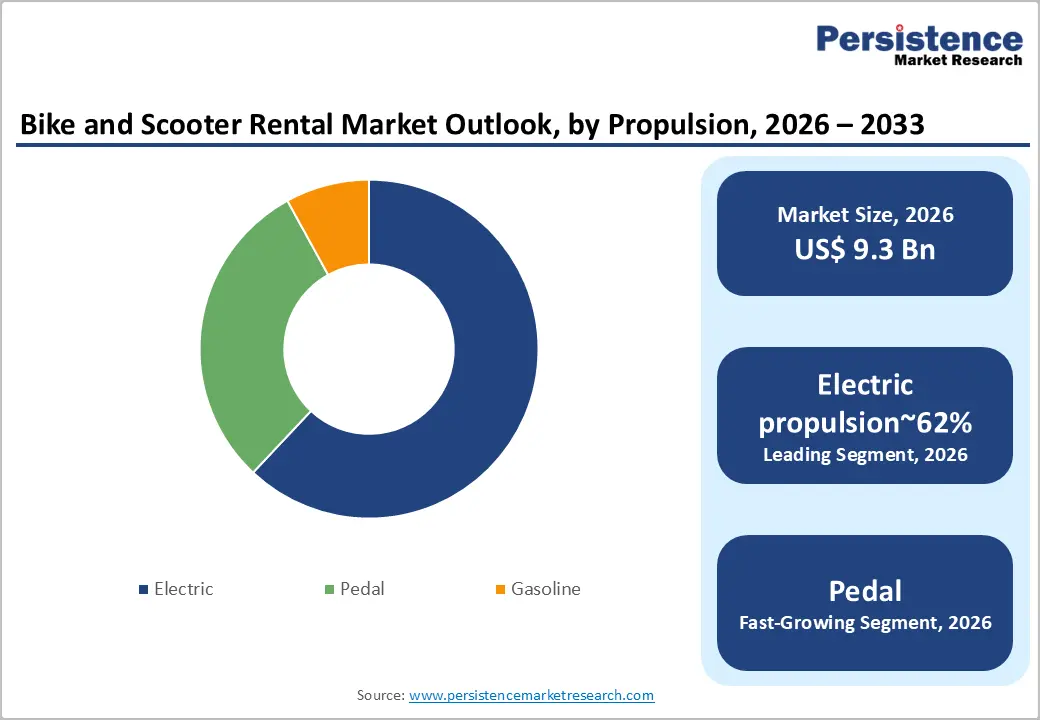

- Dominant Propulsion Type: Electric propulsion is dominant likely to register approximately 62% revenue share, driven by battery cost declines, zero-emission regulatory mandates, and strong rider preference for effortless, motorized mobility in urban environments.

- Fast-Growing Service Segment: Subscription-based service models are the fast-growing, as daily commuters seek cost-predictable plans, boosting operator revenues through improved customer lifetime value and enhanced fleet utilization rates.

- Key Opportunity: Integration with Mobility-as-a-Service (MaaS) platforms presents the most significant growth opportunity, enabling rental operators to tap into a global base of over 1.6 Bn daily public transit users and unlocking new revenue streams through transit partnerships and data monetization.

DRO Analysis

Drivers - Surging Urban Demand for Sustainable Last-Mile Mobility

The global push toward decarbonizing urban transport systems is a primary catalyst for the bike and scooter rental market. According to the International Energy Agency (IEA), urban transport accounts for nearly 40% of global energy-related CO2 emissions, prompting city planners to aggressively incentivize shared micro-mobility as a cleaner alternative.

Municipalities in the European Union have committed over €1 Bn to cycling infrastructure since 2021 under the EU Green Deal. In the United States, the Bipartisan Infrastructure Law (2021) allocated US$ 233 Mn specifically for active transportation and micro-mobility infrastructure. These policy tailwinds, combined with rapid urbanization where the United Nations projects 68% of the global population will reside in cities by 2050 create a supportive environment for a sustained rental market expansion.

Proliferation of Electric Vehicles and Smart Fleet Technology

The rapid commercialization of affordable lithium-ion battery packs has dramatically lowered the total cost of ownership for electric bikes and scooters, enabling rental operators to scale fleets profitably. Data from the World Economic Forum (WEF) indicate that battery pack costs declined by approximately 89% between 2010 and 2023.

Simultaneously, the adoption of IoT-enabled smart locks, predictive maintenance algorithms, and AI-driven demand forecasting has reduced fleet downtime and improved asset utilization rates for major operators. Companies such as Lime and Bird report utilization improvements of up to 25% following deployment of next-generation fleet management software.

Restraints - Regulatory Fragmentation and Restrictive Municipal Policies

Highly inconsistent regulatory environment across cities and countries restricts market expansion. Several municipalities have imposed strict fleet-size caps, mandatory parking zones, and speed limitations that constrain operator scalability. For instance, Paris voted in a 2023 referendum to ban free-floating rental scooters, resulting in operators losing access to an estimated 15,000 vehicle permits overnight.

Regulatory unpredictability increases the cost of capital for operators and deters long-term infrastructure investment. Compliance costs associated with obtaining permits, managing geo-fencing requirements, and adhering to insurance mandates in multiple jurisdictions materially erode profit margins, especially for smaller and mid-sized rental operators.

High Capital Expenditure and Fleet Maintenance Burden

The bike and scooter rental business model demands significant upfront capital investment in vehicle procurement, technology infrastructure, and station setup. Industry estimates suggest that deploying and maintaining a fleet of 1,000 e-scooters can cost between US$ 1 Mn and US$ 1.5 Mn annually when factoring in vandalism losses, battery replacements, and logistics.

High churn rates among vehicles particularly in regions with inadequate road infrastructure shorten vehicle lifespans and compress return on investment timelines. These economic pressures are particularly challenging in developing markets where lower average revenue per ride constrains the viability of sustainable fleet operations, acting as a natural barrier to entry and expansion.

Opportunities - Integration with Public Transit Ecosystems and MaaS Platforms

The evolution of Mobility-as-a-Service (MaaS) platforms presents a transformational growth opportunity for bike and scooter rental operators. Governments and transit authorities in Finland, Singapore, and Japan are actively piloting integrated transit apps that enable users to plan, book, and pay for multi-modal journeys including bike rentals within a single digital interface.

The European Commission's Urban Mobility Framework explicitly supports MaaS integration to reduce private car dependency. As public transit agencies increasingly look to micro-mobility for bridging first- and last-mile gaps, rental operators that forge formal partnerships with metro networks, bus rapid transit systems, and ride-hailing platforms will access a captive, transit-dependent user base estimated at over 1.6 Bn daily public transit users globally, according to the International Association of Public Transport (UITP).

Untapped Growth in Emerging Markets and Tourism Corridors

Emerging economies across Southeast Asia, Latin America, and Africa represent a largely underpenetrated opportunity for the bike and scooter rental industry. According to the World Bank, urban population growth in Sub-Saharan Africa is expected to reach 1.5 Bn by 2050, with many emerging cities lacking adequate public transport infrastructure creating natural demand for affordable micro-mobility alternatives.

Simultaneously, the global tourism sector, which welcomed over 1.3 Bn international arrivals in 2023 (per the UNWTO), is driving rental demand in high-traffic destinations such as Amsterdam, Barcelona, and Bangkok. Operators deploying lightweight, low-cost, non-electric bikes targeted at tourist corridors and informal urban settlements can unlock significant revenue streams in markets previously considered too price-sensitive for shared mobility services.

Category-wise Analysis

Vehicle Type Insights

The scooter segment dominates the vehicle type category, likely to command approximately 58% of the global bike and scooter rental market revenue in 2026. This leadership is underpinned by scooters' superior versatility for navigating dense urban traffic, higher average speeds compared to conventional bicycles, and the growing fleet of electric variants that offer zero-emission appeal.

Data from the National Association of City Transportation Officials (NACTO) in the United States confirms that shared e-scooter trips surpassed 100 million in 2022 alone, reflecting robust user adoption. Additionally, scooters command a higher revenue-per-trip compared to traditional bike rentals due to their motorized capability and broader demographic appeal, including commuters and tourists, which makes the segment the revenue engine of the overall market.

Propulsion Outlook Insights

The electric propulsion accounts for the largest share within the propulsion outlook category, accounting for approximately 62% of total market revenue. The dominance of electric propulsion is driven by rider preference for effortless mobility, zero direct emissions, and the favorable economics enabled by declining battery costs.

The International Energy Agency (IEA) reports that the global stock of electric two-wheelers exceeded 300 million units in 2023, with China alone accounting for over 90% of the fleet. Rental operators are rapidly transitioning legacy gasoline and pedal fleets to electric alternatives to meet both user demand and increasingly stringent urban emission regulations, further cementing the electric segment's commanding position in the rental value chain.

Service Outlook Insights

The Pay-as-you-go service model leads the service outlook category with an estimated share of approximately 55% of total market revenue in 2026. This model's dominance stems from its low-commitment, frictionless nature that appeals to occasional riders, tourists, and infrequent commuters who do not wish to commit to fixed subscription fees. The simplicity of scanning a QR code and unlocking a vehicle for a per-minute charge facilitated by app-based platforms has been transformative in lowering user adoption barriers.

Subscription-Based models are gaining traction among daily urban commuters, offering cost predictability. Operators such as Citi Bike have demonstrated that annual membership conversions significantly improve fleet utilization rates and customer lifetime value, establishing subscription as the fastest-growing service segment.

Regional Analysis

North America Bike and Scooter Rental Market Trends & Analysis

North America represents one of the most developed micro-mobility markets globally, driven by progressive urban transport policies, high smartphone penetration, and well-established cycling infrastructure in major cities. The United States accounts for the lion's share of regional revenue, supported by federal investments in active transportation under the Bipartisan Infrastructure Law and the rapid expansion of dock-based and dockless rental networks in cities such as New York, Chicago, San Francisco, and Washington D.C.

U.S. Bike and Scooter Rental Market Size

The U.S. bike and scooter rental market is estimated at approximately US$ 2.1 Bn in 2026, growing at a CAGR of ~17.2% through 2033, fueled by continued infrastructure investment, regulatory clarity in key cities, and the expansion of e-scooter services into suburban corridors.

Europe Bike and Scooter Rental Market Trends, Drivers, & Insights

Europe holds the second-largest market share in the global bike and scooter rental industry and is characterized by strong government support, mature cycling cultures, and comprehensive urban mobility regulations. The European Union's Sustainable and Smart Mobility Strategy targets a 50% reduction in car use in cities by 2030, directly incentivizing shared micro-mobility solutions. Countries such as Germany, France, the Netherlands, and the U.K. are frontrunners, with extensive cycling lane networks and forward-thinking municipal mobility frameworks.

The continent is also witnessing accelerated adoption of e-cargo bikes for last-mile delivery, a segment increasingly served through rental and subscription models.

Germany Bike and Scooter Rental Market Size

Germany's market is estimated at approximately US$ 620 Mn in 2026, supported by over 1.6 million km of cycling infrastructure and the national government's active promotion of e-mobility for urban transport.

U.K. Bike and Scooter Rental Market Size

The U.K. market is estimated at approximately US$ 410 Mn in 2026, driven by the Active Travel England initiative, urban congestion charge zones in London, and the rollout of e-scooter rental trials sanctioned by the Department for Transport.

France Bike and Scooter Rental Market Size

France's market is estimated at approximately US$ 390 Mn in 2026. Despite the Paris scooter ban, growth continues in Lyon, Bordeaux, and other cities, underpinned by the national Plan Vélo cycling investment program allocating €2 Bn through 2027.

Asia Pacific Bike and Scooter Rental Market Drivers & Analysis

Asia Pacific is the fastest-growing regional market and the largest by volume, accounting for over 40% of global rental trips. The region benefits from extremely dense urban populations, a well-entrenched cultural affinity for two-wheeled transport, and massive government investments in smart city infrastructure.

China Bike and Scooter Rental Market Size

China accounts for the largest share in Asia Pacific, with the market estimated at approximately US$ 2.8 Bn in 2026, expanding on the back of platform-driven shared micro-mobility ecosystems and aggressive municipal e-mobility mandates.

China dominates the regional market, with platforms such as Meituan Bike and Hello Bike operating fleets exceeding 10 million vehicles. India's market is accelerating following the government's National Electric Mobility Mission Plan and policy incentives under the FAME II scheme, which have catalysed investment in electric two-wheeler infrastructure. Japan presents a unique market with high tourism density and mature urban mobility ecosystems, positioning docked bike rental systems as vital transport supplements for both residents and international visitors.

India Bike and Scooter Rental Market Size

India's bike and scooter rental market is estimated at approximately US$ 580 Mn in 2026, underpinned by surging EV adoption, rapid urbanization, and the proliferation of app-based micro-mobility startups such as Yulu and Bounce in tier-1 and tier-2 cities.

Japan Bike and Scooter Rental Market Size

Japan's market is estimated at approximately US$ 310 Mn in 2026, driven by inbound tourism recovery, smart city pilot programs in Tokyo and Osaka, and government-backed initiatives promoting cycling for urban commuting under Japan's Green Growth Strategy.

Competitive Landscape

The global bike and scooter rental market exhibits a moderately fragmented competitive structure, characterized by a mix of global platform operators, regional champions, and municipal-backed schemes.

Leading companies such as Lime, Bird, Lyft (Citi Bike / Bay Wheels), and Hellobike command significant market shares through extensive city partnerships and technology-driven fleet optimization. Key differentiators include mobile app user experience, fleet electrification pace, and public-private partnership capabilities.

Key Developments:

- In March 2025, Lime announced an expanded partnership with Transport for London (TfL) to integrate its e-bike rental fleet into the official TfL Journey Planner app, enabling seamless multi-modal travel booking for over 5 million daily London commuters.

- In November 2024, Hellobike (Hello Inc.) secured a US$ 400 Mn funding round to accelerate international expansion across Southeast Asia and develop next-generation battery-swap infrastructure for its growing e-scooter fleet in China and beyond.

Companies Covered in Bike and Scooter Rental Market

- Lime (Neutron Holdings Inc.)

- Lyft Inc. (Citi Bike / Bay Wheels)

- Hello Inc. (Hellobike)

- Bird Rides Inc.

- Tier Mobility SE

- Voi Technology AB

- Dott

- Spin (Ford Motor Company)

- Zagster Inc.

- Nextbike by TIER

- Ofo Inc.

- Mobike (Meituan Bike)

- Yulu Bikes Pvt. Ltd.

- Bounce Infinity (Wicked Ride Adventures)

- Citi Bike (operated by Lyft)

- Jump Bikes (Uber)

- Zipp Mobility

- Superpedestrian Inc.

- UFI Filters S.p.A.

Frequently Asked Questions

The global Bike and Scooter Rental market is valued at approximately US$ 8.9 Bn in 2026 and is projected to reach US$ 30.5 Bn by 2033, expanding at a CAGR of 18.5% during the forecast period of 2026 - 2033.

The primary demand drivers include rapid urbanization (the UN projects 68% of the global population will live in cities by 2050), growing environmental consciousness pushing cities to reduce carbon emissions, government investments in cycling and micro-mobility infrastructure (such as the US$ 233 Mn allocated under the U.S.

The Electric propulsion segment leads the Propulsion Outlook category with approximately 62% revenue share. This dominance is driven by rider preference for effortless, zero-emission travel, the dramatic decline in lithium-ion battery costs (down ~89% between 2010 and 2023 per the IEA), and stringent urban emission regulations mandating operators to transition away from gasoline-powered vehicles, making electric the most commercially and environmentally viable propulsion option.

Asia Pacific is the leading region, accounting for over 40% of global rental trip volume. China is the dominant national market, with platforms such as Meituan Bike and Hello Bike deploying fleets exceeding 10 million vehicles.

The leading players in the global Bike and Scooter Rental Market include Lime (operating 250,000+ vehicles in 280+ cities across 30+ countries), Lyft Inc. through its Citi Bike (New York's largest bike share system with 30,000+ bikes) and Bay Wheels networks, Hello Inc. (Hellobike).