- Automotive Components & Materials

- Automotive Condenser Market

Automotive Condenser Market Size, Share, and Growth Forecast 2026 - 2033

Automotive Condenser Market by Vehicle Type (Passenger Cars, Light Commercial Vehicles and Heavy Commercial Vehicles), by Design (Serpentine, Parallel flow, and Tube and Fin), by Material (Aluminum, Copper, and Nickel-Plated Steel), by Sales Channel (OEM and Aftermarket) and Regional Analysis for 2026 - 2033

Automotive Condenser Market Share and Trends Analysis

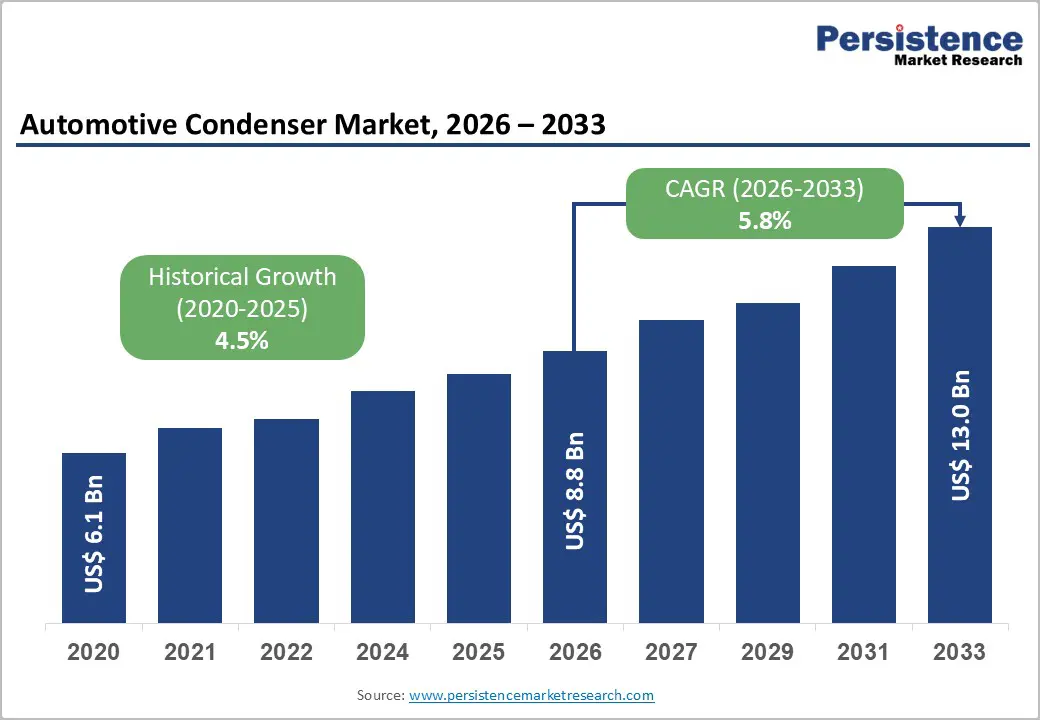

The global automotive condenser market size is likely to be valued at US$ 8.8 billion in 2026 and is projected to reach US$ 13.1 billion by 2033, growing at a CAGR of 5.8% between 2026 and 2033.

The market's expansion reflects accelerating automotive production, rising demand for efficient air-conditioning systems, and the widespread adoption of advanced thermal management technologies across passenger and commercial vehicle segments. The broader automotive HVAC market, which includes condenser systems as critical components, reached approximately US$ 60.27 billion in 2026, with condensers representing the fastest-growing component segment, growing at 6.3% annually, supported by integration with smart features and the adoption of lightweight, compact designs.

Key Market Highlights

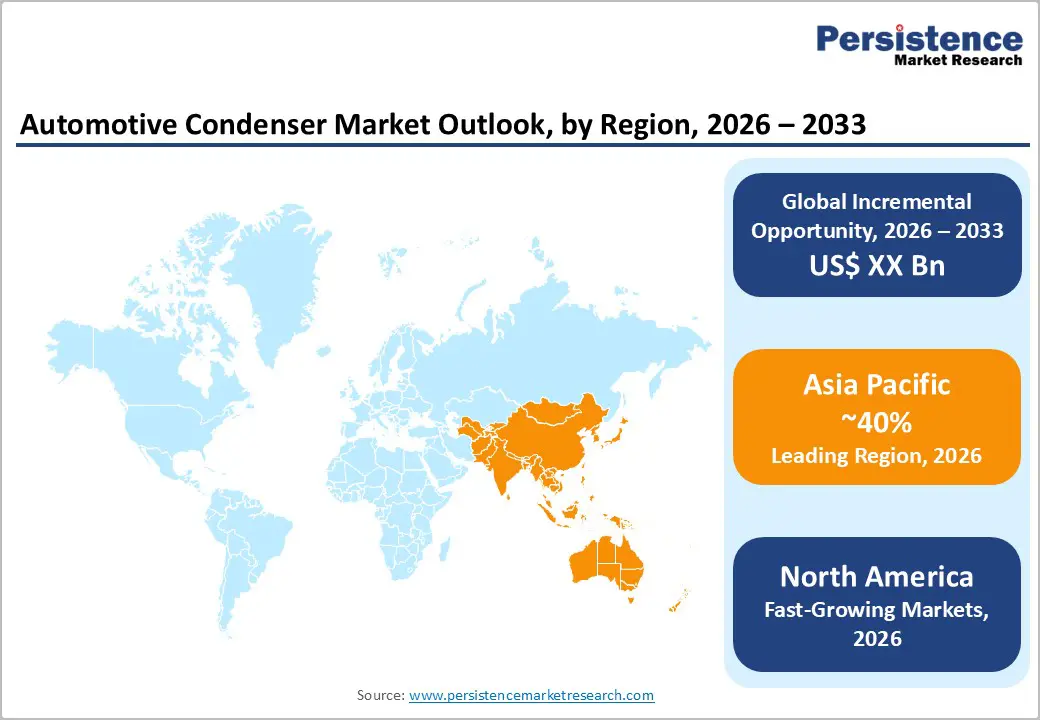

- Leading Region: Asia-Pacific dominates with a 40% global market share. China's new energy vehicle sales are expected to exceed 12 million units in 2024. India's heavy-duty vehicle electrification mandate, and Southeast Asian manufacturing expansion drive regional market dominance through 2033.

- Fastest-growing Region: Passenger Cars fastest-growing at 6.1% CAGR Rising consumer demand for advanced climate control, electric vehicle thermal management optimization, and autonomous vehicle technology integration drives passenger car condenser expansion.

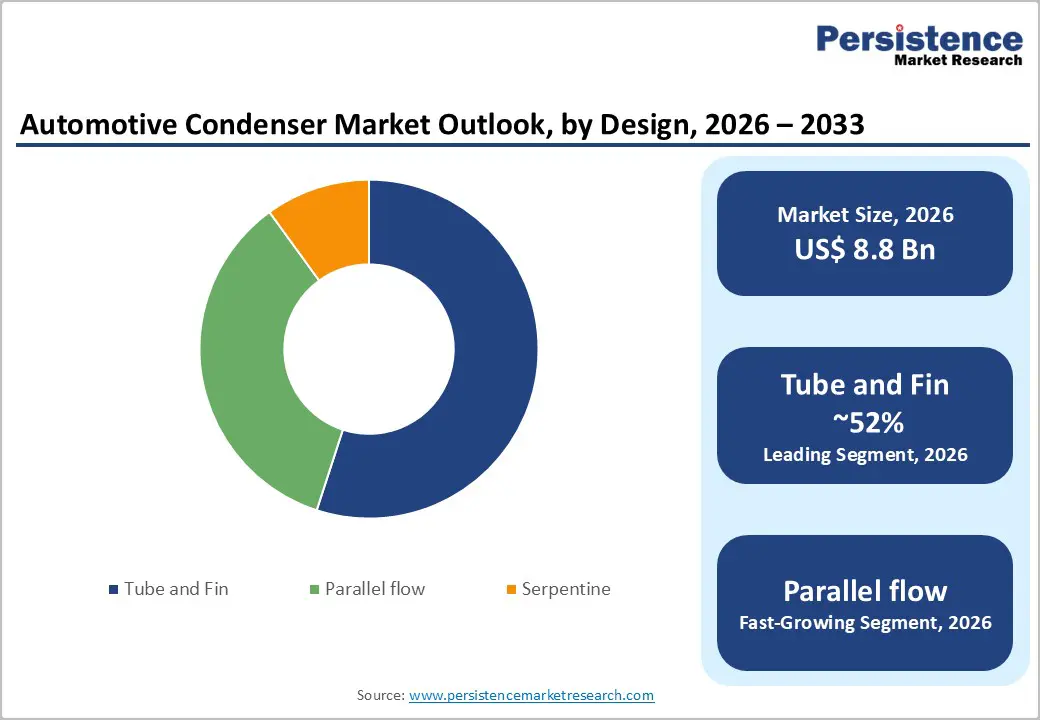

- Leading Segment: Tube-and-Fin design dominates with 52% market share. Established manufacturing processes, cost-effectiveness, and proven performance across diverse vehicle applications maintain traditional design dominance in automotive condenser specifications.

- Fastest-growing Segment: OEM sales channels account for 71% of the market. Long-term OEM supplier contracts, integrated vehicle development programs, and collaborative technology partnerships establish a foundation for market demand that supports manufacturing capacity investments.

- Opportunity: Advanced Material Integration and Microchannel Technology represent major market opportunities. Lightweight material innovation, enhanced thermal performance, and emerging EV thermal management requirements establish high-value market segments that support premium pricing and competitive differentiation.

| Key Insights | Details |

|---|---|

| Automotive Condenser Market Size (2026E) | US$ 8.8 Bn |

| Market Value Forecast (2033F) | US$ 13.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.8% |

| Historical Market Growth (CAGR 2020 to 2024) | 4.5% |

Market Dynamics

Drivers - Rising Electric Vehicle Adoption and Advanced Thermal Management System Requirements

Unprecedented global expansion of the electric vehicle market and the increasing complexity of thermal management requirements are driving substantial demand for specialized condenser systems that support battery cooling, motor heat dissipation, and cabin climate control optimization. Global electric vehicle sales exceeded 14 million units in 2024, representing approximately 18% of total global automotive production, and a continued acceleration toward 50% electric vehicle market penetration is projected by 2033. Electric vehicle thermal management demands sophisticated condenser architectures that manage concentrated battery heat loads exceeding those in traditional internal combustion engine applications, requiring specialized cooling systems and advanced materials to ensure operational reliability. China's new energy vehicle production mandate, targeting 40% electrification by 2033, is driving substantial procurement of automotive condensers by domestic and tier-1 global suppliers.

Stringent Environmental Regulations and Refrigerant Transition Requirements

Accelerating global environmental regulations mandating refrigerant transition from high global warming potential alternatives toward low-GWP options are establishing structural demand for advanced condenser redesign supporting compliance objectives. European Union refrigerant directive phasing down HFC (hydrofluorocarbon) refrigerants by 2030 and Asia Pacific regulatory harmonization toward low-GWP alternatives create a synchronized global market transformation. CO2 refrigerant systems utilizing trans critical refrigeration cycles deliver 25-30% fuel consumption reduction compared to R134a alternatives, directly supporting vehicle efficiency targets established by global emissions regulations.

Alternative refrigerant compatibility requires a fundamental redesign of the condenser, addressing system pressure requirements, optimizing heat transfer, and enhancing corrosion resistance, necessitating substantial investment in manufacturer research and development. Government vehicle emissions standards, including Euro 7, China 6b, and U.S. EPA regulations establishing increasingly stringent fleet-average carbon dioxide emission targets, force automotive manufacturers to prioritize thermal management efficiency, differentiating vehicle competitiveness.

Restraints - Rising Raw Material Costs and Supply Chain Volatility Constraining Profitability

Volatile pricing for volatile precious metals, aluminum, and specialty alloys, combined with persistent supply chain disruptions, create substantial cost pressures that undermine profitability and constrain market growth, particularly among lower-margin aftermarket condenser providers. Fluctuations in aluminum market prices within 25% annual ranges directly increase condenser manufacturing costs, with aluminum accounting for 40% of traditional tube-and-fin condenser material costs. Copper pricing volatility affecting thermal management component specifications and nickel alloy availability for specialized corrosion-resistant applications create procurement complexity and cost unpredictability. Supply chain disruptions extending semiconductor component lead times for electronic temperature sensors and control modules integrated into advanced condenser systems cascade through manufacturing schedules extending 16-24 weeks.

Intense Price Competition and Margin Compression from Regional Manufacturers

Extreme competitive intensity across condenser markets, driven by the proliferation of regional manufacturers from China, India, and Southeast Asia, is substantially constraining margins for established global suppliers. Chinese condenser manufacturers, including Linazheng and emerging competitors, are capturing 35% cost advantages through domestic material sourcing and labor efficiencies, compressing pricing across all geographic markets. Consolidation among global suppliers, including Hanon Systems' acquisition and Modine Manufacturing's portfolio expansion, creates pricing pressure as suppliers pursue volume-based market share expansion. Aftermarket condenser pricing declines 10-15% annually as independent remanufacturers and regional suppliers capture share from premium original equipment manufacturer suppliers. Condenser commoditization across standard tube-and-fin designs establishing minimal product differentiation and driving price-per-unit declines of 6-8% annually across OEM procurement.

Opportunity - Advanced Condenser Design Integration Supporting Autonomous Vehicle and Connected Mobility Requirements

Emerging autonomous vehicle architectures and sophisticated connected-car technologies that require enhanced computing-infrastructure thermal management represent exceptional market opportunities for condenser manufacturers developing specialized high-performance cooling solutions. Advanced driver-assistance systems (ADAS), including sophisticated sensor arrays, computing platforms, and real-time data processing, require robust thermal management to prevent computational performance degradation during extended operation. Data center integration in autonomous vehicles, necessitating continuous thermal management of graphics processing units, artificial intelligence accelerators, and communication infrastructure, is creating emerging high-value condenser applications. Distributed computing architectures across autonomous vehicle platforms, which require localized thermal management near processing clusters, create opportunities for specialized condenser development. Thermal domain controller integration, enabling centralized optimization of condenser operation coordinated with vehicle propulsion systems, battery management, and cabin climate, creates software-differentiated market opportunities.

Lightweight Material Innovation and Microchannel Condenser Technology Development

Integration of advanced lightweight materials, including graphene-enhanced composites, aluminum-titanium alloys, and ceramic matrix composites, combined with microchannel condenser geometry optimization, represents a transformative market opportunity, enabling performance differentiation and cost reduction. Microchannel condenser technology delivering 35% improved heat transfer efficiency compared to traditional tube-and-fin designs while reducing weight by 20% creates compelling value proposition supporting premium pricing justified by vehicle fuel economy improvements. Graphene-enhanced thermal conductivity enables improved condenser performance with reduced size and weight, establishing opportunities for emerging technology differentiation, particularly valuable for electric vehicle thermal management optimization. High-performance aluminum alloy development customized for automotive condenser applications, combining superior corrosion resistance with lightweight benefits, supports electric vehicle efficiency objectives.

Category-wise Analysis

Vehicle Type Insights

Passenger cars maintain market dominance with approximately 58% market share, reflecting higher vehicle production volumes and sophisticated climate control system adoption across global automotive markets. Passenger vehicle air conditioning represents standard equipment across developed markets and increasingly widespread adoption in emerging economies with rising consumer affluence supporting premium comfort features. Passenger-car thermal management requirements emphasize optimizing cabin climate comfort, improving fuel efficiency, and integrating advanced sensors to support the development of autonomous-vehicle technology. The commercial vehicle segment accounts for approximately 42% of the market, expanding at an accelerating 6.8% annual growth rate, driven by increasing heavy-duty vehicle electrification, regulatory emphasis on fleet efficiency, and operator demand for enhanced driver comfort during extended operational periods.

Design Insights

Tube-and-Fin condenser designs command market dominance with approximately 52% market share, representing proven technology across diverse vehicle applications with established manufacturing processes and established cost structures. Traditional tube-and-fin technology offers cost-effective performance delivering reliable heat transfer across temperature operating ranges supporting widespread OEM adoption. Serpentine design configurations account for approximately 31% of the market, optimized for compact engine compartments and for specialized vehicle architectures that require space-efficient thermal solutions. Parallel flow condenser designs account for approximately 17% market share, expanding at accelerating 7.2% annual growth rates driven by electric vehicle integration requiring optimized thermal performance within constrained vehicle compartments.

Material Insights

Aluminum construction dominates automotive condenser specifications, with approximately 56% market share, owing to its superior thermal conductivity, lightweight, and cost-effectiveness, which support fuel-economy objectives. Aluminum alloy selection, increasingly emphasizing corrosion resistance, fatigue performance, and optimization of extended service life, addresses rising durability requirements across diverse vehicle and environmental operating conditions. Copper materials command approximately 27% market share, valued for exceptional thermal properties and specialized high-performance applications including premium electric vehicle thermal management and specialized commercial applications. Nickel-plated steel accounts for approximately 17% of the market, used in specialized heavy-duty vehicles and marine applications that require enhanced corrosion resistance and operational durability under extreme environmental conditions. Advanced material integration including graphene-enhanced composites and ceramic-matrix materials expanding at 9.3% annual growth rates reflects emerging technology adoption addressing weight reduction and thermal performance optimization supporting electric vehicle adoption.

Sales Channel Analysis

OEM (Original Equipment Manufacturer) channels command approximately 71% of the market, reflecting automotive manufacturers' direct procurement supporting new-vehicle production and integrated vehicle program development. OEM supplier relationships that emphasize long-term contracts, volume commitments, and collaborative technology development establish a foundation for market demand that supports manufacturing capacity investments and research initiatives. Aftermarket sales account for approximately 29% of the market, driven by replacement demand from maintenance of aging vehicle fleets, component failure recovery, and performance upgrades. Aftermarket channel expansion at 6.4% annual growth rates reflects growing vehicle population maintenance requirements, regulatory compliance support, and independent repair facility consolidation, establishing distributed distribution networks. Online aftermarket condenser sales are expanding at 12.3% annual growth rates, driven by e-commerce platform proliferation, including Amazon Automotive, RockAuto, and specialized automotive parts retailers, reaching geographically dispersed independent repair facilities.

Regional Insights

North America Automotive Condenser Market Trends

North America maintains a strong market position with approximately 30% global automotive condenser market share, anchored by the United States automotive production leadership and sophisticated thermal management technology adoption across passenger and commercial vehicles. United States light-duty vehicle production reached approximately 10.8 million units in 2024, with thermal management systems integration standardized across all manufacturer platforms. EPA environmental regulations establishing increasingly stringent fleet-average CO2 emission standards drive automotive manufacturer investment in advanced condenser technology supporting vehicle efficiency optimization.

Heavy-duty vehicle emissions standards requiring integrated thermal management systems for Class 8 truck applications create substantial OEM procurement supporting specialized condenser development. North American aftermarket condenser market expansion is driven by an aging vehicle fleet, averaging 12.3 years of operational life, which creates recurring replacement demand supporting independent repair facility requirements.

Europe Automotive Condenser Market Trends

Europe represents approximately 26% global automotive condenser market share, characterized by stringent environmental regulations, advanced technology adoption, and premium vehicle production emphasis driving sophisticated thermal management system development. Euro 7 environmental regulation establishes comprehensive emissions control requirements, including CO2 limits and real-world driving emissions testing mandates, automotive manufacturer investment in advanced thermal management.

European Union refrigerant directive phasing down HFC compounds establishes synchronized regional market transformation toward low-GWP alternatives including HFOs and CO2. German automotive manufacturers, including BMW, Mercedes-Benz, and Volkswagen, are emphasizing precision engineering and advanced technology integration, driving condenser technology innovation and establishing regional leadership. United Kingdom post-Brexit automotive supply chain reconfiguration creates opportunities for regional condenser suppliers establishing manufacturing footprints supporting European vehicle production.

Asia Pacific Automotive Condenser Market Trends

Asia Pacific dominates automotive condenser markets with approximately 40% global market share, driven by extraordinary automotive production volumes, rapid electrification acceleration, and emerging market vehicle demand expansion. China represents approximately 55% of the regional market share, supported by new energy vehicle sales exceeding 12 million units in 2024 and a mandate establishing 40% electric vehicle penetration by 2033. Chinese automotive manufacturer's emphasis on integrated thermal management, supporting battery efficiency and extended vehicle driving range, drives substantial condenser procurement, supporting regional supplier dominance. India's automotive production expansion, coupled with heavy-duty vehicle electrification and a blanket air-conditioning mandate for commercial vehicles, is creating exceptional demand for thermal management systems. Japanese and South Korean automotive manufacturers maintain technology leadership in thermal management component development, supporting regional export positioning.

Competitive Landscape

The automotive condenser market exhibits significant consolidation among global tier-one suppliers Denso, Valeo, Hanon Systems, MAHLE, Sanden, and Keihin collectively commanding approximately 58% aggregated market share through comprehensive product portfolios, established OEM relationships, and substantial research and development investment. Market leaders pursue expansion through strategic acquisition of regional manufacturers, integration of advanced materials and design technologies, and research partnerships advancing thermal management innovation.

Denso maintains market leadership through comprehensive automotive thermal management portfolio, advanced manufacturing processes, and innovation emphasis supporting electric vehicle thermal requirements. Valeo emphasizes innovative condenser designs including microchannel technology development and alternative refrigerant system optimization supporting emerging market demands.

Key Developments:

- In June 2025, German supplier ZF unveiled its TherMaS electric-vehicle thermal management system using propane as a refrigerant, offering better cooling efficiency in a compact design. This innovation highlights the trend toward environmentally friendly, high-performance condensers tailored for EVs.

- In May 2025, MAHLE introduced an intelligent thermal management solution for Mahindra’s XEV BEV platforms. It features smart control, corrosion-resistant materials, and multi-source cooling capabilities, demonstrating advanced condenser integration in EVs.

Companies Covered in Automotive Condenser Market

- Calsonic Kansei

- Delphi Technologies

- Denso

- Hanon Systems

- Keihin

- MAHLE

- Modine Manufacturing Company

- Sanden Holdings

- Tata AutoComp

- Valeo

- Other Key Players

Frequently Asked Questions

The global Automotive Condenser market was valued at US$ 8.8 billion in 2026 and is projected to reach US$ 13.1 billion by 2033, expanding at a 5.8% CAGR.

Primary growth drivers include unprecedented electric vehicle adoption with global sales exceeding 14 million units in 2024 requiring advanced thermal management systems, stringent environmental regulations including refrigerant transition toward low-GWP alternatives mandating condenser redesign and rising automotive production volumes supporting sustained OEM procurement expansion.

Passenger Cars dominate with approximately 58% market share, reflecting higher vehicle production volumes and sophisticated climate control system adoption. Commercial Vehicles represent 42% market share, expanding at accelerating 6.8% annual growth rates driven by heavy-duty vehicle electrification, regulatory compliance emphasis, and operator demand for enhanced thermal comfort supporting extended operational periods.

Asia Pacific maintains market dominance with approximately 40% global market share, driven by China's new energy vehicle sales exceeding 12 million units and government mandate establishing 40% electric vehicle penetration by 2033.

Market leaders include Denso Corporation, Valeo SE, Hanon Systems, MAHLE International, Sanden Holdings, and Keihin Corporation.