- Hardware & Software IT Services

- AI Governance Market

AI Governance Market Size, Share, and Growth Forecast, 2026 - 2033

AI Governance Market by Governance Layer (Policy & Strategy Governance, Model Lifecycle Management, Risk Management & Regulatory Compliance, Monitoring & Auditing, Transparency & Explainability, Data Governance for AI, Ethics & Responsible AI, AI Security & Resilience Governance), Delivery Models (Software platforms, Managed governance services, Professional and consulting services), Organisation Size, Deployment Mode, Industry), and Regional Analysis for 2026 - 2033

AI Governance Market Size and Trends Analysis

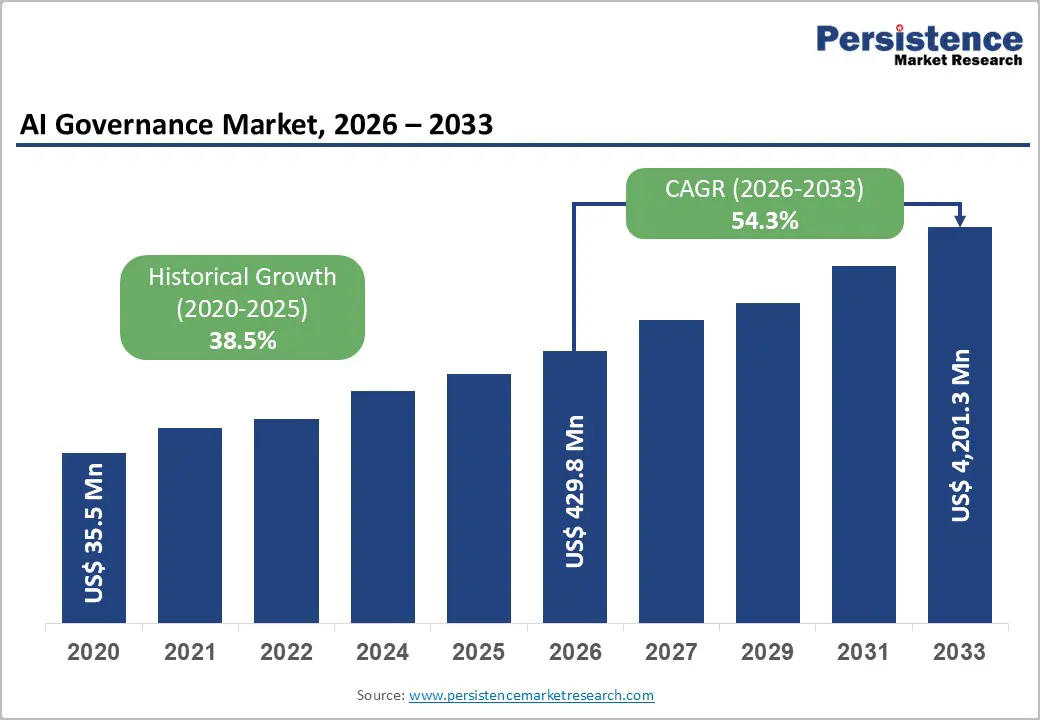

The global AI governance market size is likely to be valued at US$ 429.8 million in 2026 and is projected to reach US$ 4,201.3 million by 2033, growing at a CAGR of 38.5% between 2026 and 2033. This expansion reflects an extraordinary acceleration from historical performance, with the market demonstrating a significant CAGR between 2020 and 2026, evidencing rapid maturation of governance frameworks across enterprises globally.

The market's substantial growth trajectory is driven by escalating regulatory mandates, particularly the EU AI Act's enforcement provisions that impose penalties up to €35 million or 7% of global turnover, compounded by rising enterprise AI adoption requiring robust governance infrastructure, and the emergence of autonomous AI agents demanding sophisticated risk management and lifecycle oversight capabilities.

Key Industry Highlights:

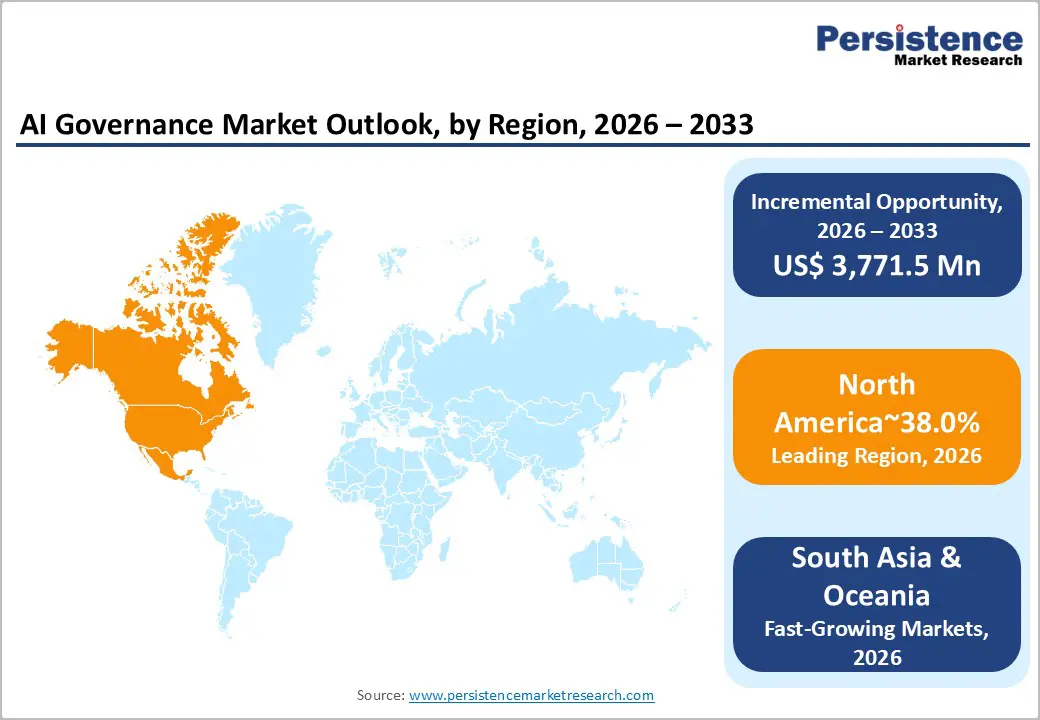

- Regional Dominance: North America leads the global AI Governance Market with ~38% share in 2026, driven by strong enterprise AI adoption, substantial regulatory oversight, and the presence of technology giants like IBM, Microsoft, and Google, while Europe (28%) and East Asia (15%) hold significant positions supported by prescriptive AI regulations and proactive national frameworks.

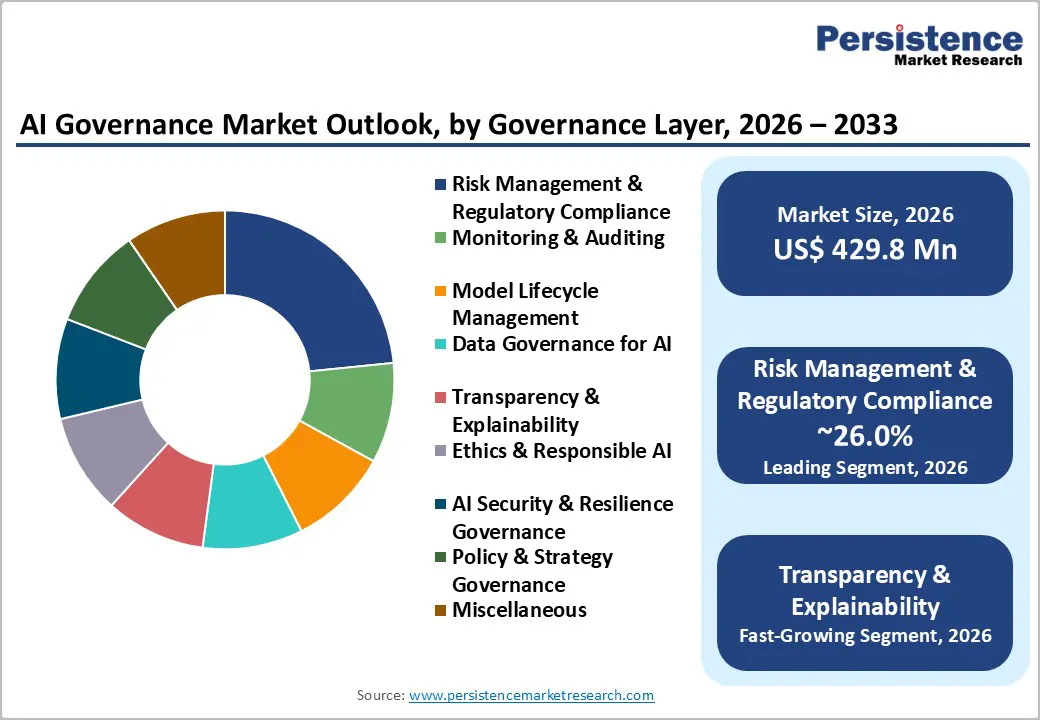

- Leading Governance Layer: Risk Management & Regulatory Compliance captures the largest market share at ~26% in 2026, reflecting enterprises’ focus on audit, compliance monitoring, and cross-jurisdiction regulatory validation, whereas Transparency & Explainability emerges as the fastest-growing segment due to rising demand for algorithmic accountability and stakeholder trust.

- Leading Industry: Banking, Financial Services & Insurance holds the largest revenue share at ~28% in 2026, while Healthcare & Life Sciences stands out as the fastest-growing sector, driven by clinical AI adoption, FDA regulations, and the need for domain-specific governance frameworks ensuring patient safety and regulatory compliance.

- Regulatory Landscape: The EU AI Act, U.S. AI Research, Innovation, and Accountability Act, and East Asian AI governance initiatives are fueling demand for AI governance solutions that ensure compliance, ethical use, and secure deployment of autonomous systems across enterprises.

- Sovereign Cloud & Data Residency Opportunity: SAP’s EU AI Cloud and Capgemini partnerships enable enterprises to maintain data sovereignty, regulatory compliance, and controlled AI deployment, presenting growth potential in regulated sectors and cross-border AI applications

- Enterprise Platform Integration Trend: IBM’s watsonx. governance integration and SAP’s role-aware AI assistants embed AI governance directly into enterprise workflows, reducing implementation complexity and accelerating adoption across large organizations.

| Key Insights | Details |

|---|---|

| AI Governance Market Size (2026E) | US$ 429.8 Mn |

| Market Value Forecast (2033F) | US$ 4,201.3 Mn |

| Projected Growth (CAGR 2026 to 2033) | 54.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 38.5% |

Market Dynamics

Growth Drivers

Escalating Regulatory and Compliance Requirements Across Global Jurisdictions

Regulatory frameworks governing AI development and deployment have emerged as the most consequential driver of the AI Governance Market. The European Union's AI Act, effective February 2025, established the first comprehensive regulatory framework with categorical risk classifications and stringent requirements for high-impact AI systems, creating immediate compliance obligations for multinational enterprises.

The United States proposed Artificial Intelligence Research, Innovation, and Accountability Act (S. 3312) seeks to establish federal oversight with civil fines up to $300,000 or twice the value of non-compliant AI systems for violations. India's MeitY unveiled the India AI Governance Guidelines under the IndiaAI Mission in November 2025, establishing a comprehensive framework for safe, inclusive, and responsible AI adoption with governance pillars and phased action plans.

Japan continues leading through the Hiroshima AI Process and AI Guidelines for Business, combining soft-law frameworks with sector-specific hard-law measures to ensure safe, ethical, and human-centric AI deployment. South Korea advanced its national "Digital Bill of Rights," establishing Responsible, Inclusive, and Sustainable AI as guiding principles. The regulatory patchwork necessitates organizations implement sophisticated AI Governance Market solutions that validate compliance across multiple jurisdictions simultaneously, directly fueling demand for governance platforms, risk management tools, and regulatory monitoring services that address cross-border complexities and conflicting requirements.

Enterprise AI Adoption Acceleration and Autonomous Agent Complexity

Enterprise AI adoption has reached mainstream status with 87% of large enterprises implementing AI solutions and annual investments averaging $6.5 million per organization. The market is experiencing accelerated deployment of generative AI and autonomous agents, with 23% of enterprises already scaling agentic AI systems and another 39% actively experimenting with multi-step workflow automation. This proliferation of AI agents across business functions fundamentally increases governance complexity, as autonomous systems require continuous monitoring, risk assessment, model lifecycle management, and real-time compliance validation.

The IBM Institute for Business Value study highlighted that AI leaders centralize governance, formalize oversight, and empower Chief AI Officers to manage risk, align innovation with strategy, and ensure ethical, compliant AI deployment. As enterprises embed AI into mission-critical functions spanning finance, healthcare, supply chain, and customer operations, the AI Governance Market expands to address model validation, bias detection, performance monitoring, and algorithmic accountability capabilities essential for scaling AI responsibly across organizational hierarchies and functional domains.

Restraint - High Implementation Costs and Resource Intensity

Establishing comprehensive AI governance frameworks requires substantial capital investment in technology platforms, specialized talent, and organizational restructuring. Only around 43% of surveyed organizations possess formal AI governance policies, with many organizations delaying implementation due to cost considerations, implementation complexity, and competing budget priorities.

Organizations must invest in governance platforms, hire or train governance specialists, establish oversight committees, and integrate governance tools with existing IT infrastructure investments that smaller and mid-market organizations struggle to justify when facing resource constraints and uncertain ROI calculations.

The complexity of governance requirements across multiple regulatory jurisdictions compounds implementation costs, as organizations require solutions capable of validating compliance with EU AI Act provisions, U.S. state-level regulations, and sector-specific requirements simultaneously. This cost barrier disproportionately impacts smaller enterprises, potentially fragmenting the AI Governance Market and limiting market penetration in price-sensitive segments.

Opportunity - Sovereign Cloud and Data Residency Governance Solutions

National governments are mandating data sovereignty and establishing requirements for controlled AI deployment within geographically bounded cloud environments. Europe's regulation establishing AI gigafactories through the EuroHPC Joint Undertaking aims to strengthen Europe's AI infrastructure, technological autonomy, and innovation while ensuring data remains within European boundaries. SAP's launch of EU Cloud in November 2025 created a sovereign AI and cloud framework ensuring data residency and regulatory compliance for European enterprises. The European Commission's Regulation (EU) 2024/1689 and Code of Practice for General-Purpose AI require AI providers to detect and respect copyright reservations, creating governance requirements that extend to content management and intellectual property protection.

The AI governance market is expanding to address sovereign cloud governance, data residency validation, cross-border data compliance, and controlled AI deployment frameworks. Enterprises in regulated sectors, government agencies, and financial institutions require governance solutions enabling them to maintain data sovereignty while deploying AI agents and autonomous workflows.

Capgemini and SAP partnership announced in November 2025 emphasizes AI governance, data sovereignty, and compliance, enabling organizations in regulated sectors to deploy trusted, secure, and autonomous AI workflows while maintaining strict control over sensitive data and operations. This opportunity extends across European enterprises, Asian governments establishing sovereign AI ecosystems, and regulated industries worldwide requiring governance solutions that integrate data residency, compliance validation, and controlled AI deployment.

AI Governance Integration Within Enterprise Platforms and Development Workflows

Embedding AI governance directly into enterprise application platforms, development environments, and business technology platforms represents a significant market opportunity. OpenText's SAP S/4HANA Cloud Public Edition certification for Core Content Management enables enterprises to securely manage structured and unstructured content while embedding compliance and governance into AI-driven workflows. SAP's expansion of Joule and introduction of role-aware AI assistants enables enterprises to scale AI applications responsibly by ensuring data integrity, compliance, and oversight in AI-driven workflows. IBM's announcement of role-aware AI assistants in Joule and expansion of SAP Business Data Cloud Connect strengthens AI governance by enabling secure, governed access to trusted data across platforms.

The opportunity extends to enterprises seeking to integrate governance capabilities within development platforms, enterprise resource planning systems, and customer relationship management platforms, rather than implementing governance as a standalone tool requiring separate infrastructure and change management.

Developers require governance frameworks embedded directly in their development workflows, enabling them to validate compliance during model development, test for bias and performance drift automatically, and document governance decisions within existing development processes. The Market is expanding as enterprise platform vendors, technology infrastructure companies, and systems integrators deliver integrated governance capabilities within their platforms, reducing implementation complexity and accelerating governance adoption across organizational hierarchies.

Category-wise Analysis

Component Insights

Risk Management & Regulatory Compliance represents the largest AI Governance Market segment, capturing approximately 26% of market share in 2026. Organizations prioritize risk management and regulatory compliance due to escalating regulatory requirements, enforcement actions, and potential financial penalties for non-compliance.

This segment encompasses risk assessment frameworks, regulatory compliance validation, audit trail management, regulatory reporting automation, and compliance monitoring solutions that help organizations validate adherence to regulatory requirements across multiple jurisdictions. Financial services organizations, healthcare providers, and government agencies drive demand for risk management and regulatory compliance solutions, as these sectors face stringent regulatory oversight and significant potential fines for governance failures.

Transparency and Explainability represents the fastest-growing governance layer segment within the AI Governance Market, reflecting enterprises' recognition that algorithmic accountability and explainability are fundamental to building stakeholder trust and managing organizational reputation. As AI systems increasingly drive decisions affecting customers, employees, and business outcomes, organizations recognize the need to understand and explain AI decision-making processes to stakeholders, regulators, and affected individuals.

Industry Insights

The Banking, Financial Services & Insurance sector represents the largest industry segment within the AI Governance Market, commanding approximately 28% of market share in 2026. Financial institutions deploy AI extensively across lending decisions, fraud detection, algorithmic trading, customer service, and risk management, but face stringent regulatory oversight from financial regulators, central banks, and sectoral compliance bodies.

Financial services organizations must comply with GDPR, PCI DSS, Anti-Money Laundering regulations, and emerging AI-specific requirements, creating substantial governance requirements. IBM's integration of watsonx. governance with IBM Guardium AI Security in June 2025 demonstrates the market's focus on financial services governance, enabling financial institutions to govern and secure AI systems while validating compliance across multiple regulatory frameworks including the EU AI Act and ISO 42001.

Healthcare and Life Sciences represent the fastest-growing industry segment within the AI Governance Market, driven by exponential growth in clinical AI adoption, FDA regulatory requirements for AI medical devices, and life sciences enterprises' use of AI in drug discovery and development. Healthcare organizations are deploying AI for diagnostic imaging analysis, patient risk stratification, treatment recommendations, and drug discovery at unprecedented scale, creating governance requirements for clinical validation, patient safety monitoring, adverse event reporting, and regulatory compliance.

The NTT DATA 2026 Global AI Report emphasizes that top-performing enterprises embedding AI governance at the enterprise level scale AI responsibly, with healthcare organizations increasingly recognizing governance as essential for scaling clinical AI safely and managing liability exposure. Healthcare enterprises require specialized governance solutions addressing clinical validation, algorithmic accountability for treatment decisions, bias detection across patient populations, FDA compliance for AI medical devices, and integration with clinical governance and quality assurance processes.

Regional Insights and Trends

North America AI Governance Market Trends

North America commands approximately 38% of the global AI Governance Market and represents the largest regional market, driven by substantial regulatory activity, high enterprise AI adoption rates, and significant investment in governance infrastructure. The proposed Artificial Intelligence Research, Innovation, and Accountability Act (S. 3312) signals federal commitment to establishing comprehensive AI oversight with civil penalties reaching $300,000 or twice non-compliant AI system values.

The U.S. Federal Trade Commission has emerged as an active AI governance regulator, with enhanced enforcement authority and FTC expectations influencing platform feature development and governance capabilities. Canada has demonstrated proactive governance initiatives through AI guidelines and collaboration with industry leaders to promote responsible AI use, while the presence of major technology firms including IBM, Microsoft, Amazon, Google, and Salesforce in North America accelerates governance solution innovation and implementation.

North American enterprises invest substantially in governance infrastructure, with organizations recognizing governance as essential for managing reputational risk, avoiding regulatory penalties, and maintaining stakeholder confidence. The region's financial services sector, concentrated in New York, Toronto, and major U.S. financial centers, drives demand for governance solutions addressing algorithmic trading, lending discrimination, fraud detection, and customer treatment.

East Asia AI Governance Market Trends

East Asia commands approximately 15% of the global AI Governance Market and represents a rapidly evolving governance landscape characterized by divergent policy approaches reflecting regional ambitions and strategic priorities.

China has emerged as a proactive AI governance leader, announcing the Artificial Intelligence Global Governance Action Plan in July 2025 at the World AI Conference, positioning itself as a global AI rulemaker and emphasizing international collaboration on technical standards through organizations including the International Telecommunication Union, International Organization for Standardization, and International Electrotechnical Commission. China's action plan highlights infrastructure development, sectoral AI applications, high-quality data sharing, security, sustainability, and capacity-building for developing countries, reflecting China's strategic priority to shape the global AI framework. The plan aligns with China's regulatory framework including the Data Security Law, Cybersecurity Law, and Personal Information Protection Law, establishing comprehensive governance requirements for Chinese enterprises and foreign companies operating in China.

South Korea advanced its "Digital Bill of Rights" with governance principles emphasizing Responsible, Inclusive, and Sustainable AI development and deployment. Microsoft's alignment with South Korea's governance framework demonstrates multinational technology companies' commitment to supporting national governance initiatives while maintaining regulatory compliance.

Japan continues advancing the Hirashima AI Process and AI Guidelines for Business, emphasizing transparency, accountability, privacy, and fairness across AI applications. Tokio Marine Holdings established the Basic Policy for AI Governance in June 2025, addressing risks in insurance and solutions businesses while complying with Japanese guidelines from the Ministry of Economy, Trade and Industry and the Financial Services Agency.

Europe AI Governance Market Trends

Europe commands approximately 28% of the global AI Governance Market and represents the most advanced and prescriptive regulatory environment globally. The EU AI Act's February 2025 enforcement of prohibited practices provisions with penalties reaching €35 million or 7% of global turnover established the global governance standard against which other regulatory frameworks are measured.

The European Union finalized the Code of Practice for General-Purpose AI in 2025, establishing transparency, safety, and copyright compliance requirements for general-purpose AI providers and creating enforcement mechanisms through the European Commission and national competent authorities.

European enterprises accelerated governance policy adoption ahead of formal compliance requirements, with governance policies emerging across European boards in 2025 as directors recognized governance obligations and organizational risk management imperatives. The European Council adopted updated regulations under the EuroHPC Joint Undertaking to establish AI gigafactories across Europe in December 2025, combining high-performance computing with AI-driven automation while introducing safeguards for third-country participation and establishing governance requirements for public-private partnerships.

Competitive Landscape

The global AI governance market exhibits an oligopolistic structure, characterized by the strong presence of a limited number of large, well-established technology companies that command a significant share through broad platform capabilities, deep enterprise penetration, and integrated AI lifecycle governance offerings. IBM Corporation, Microsoft Corporation, Google LLC (Alphabet), SAP SE, Salesforce Inc., and SAS Institute Inc. collectively shape the competitive direction of the market by offering end-to-end AI governance frameworks spanning policy management, model risk management, compliance, monitoring, and explainability.

Alongside these leaders, a growing set of specialized players such as FICO Inc., DataRobot Inc., Credo AI Inc., Truera Inc., Arthur AI Inc., and Aporia Technologies Ltd. operate in focused niches, enhancing innovation but not yet diluting the dominance of the top players. This combination results in a market that is oligopolistic with selective fragmentation at the niche level, where scale, trust, regulatory alignment, and enterprise relationships act as high entry barriers.

Key Industry Developments:

- June 18, 2025 - IBM Corporation announced an industry-first AI governance and security integration by unifying watsonx. governance with IBM Guardium AI Security, providing enterprises with a single, consolidated view of AI risk posture. The solution enables organizations to govern and secure AI systems and autonomous agents at scale while validating compliance across multiple regulatory frameworks, including the EU AI Act and ISO 42001. This development strengthens enterprise-grade AI governance by embedding security, risk management, and compliance directly into the AI lifecycle.

- November 27, 2025 - SAP SE launched EU AI Cloud, a sovereign AI and cloud framework designed to support European digital sovereignty by ensuring data residency, regulatory compliance, and controlled AI deployment. The offer enables enterprises to build, deploy, and govern AI applications within EU-compliant environments, addressing governance requirements tied to data protection and operational sovereignty. Through partnerships with Cohere and other AI model providers, SAP strengthens AI governance, compliance assurance, and sovereign control across the AI lifecycle for regulated European enterprises.

Companies Covered in AI Governance Market

- IBM Corporation

- Microsoft Corporation

- Google LLC (Alphabet)

- SAP SE

- SAS Institute Inc.

- Salesforce Inc.

- Oracle Corporation

- ServiceNow Inc.

- FICO Inc.

- DataRobot Inc.

- H2O.ai Inc.

- Arthur AI Inc.

- Credo AI Inc.

- Truera Inc.

- Aporia Technologies Ltd.

Frequently Asked Questions

The global AI Governance market is projected to be valued at US$ 429.8 Mn in 2026.

The Risk Management & Regulatory Compliance segment is expected to account for approximately 26.0% of the global AI Governance market by Governance Layer in 2026.

The market is expected to witness a CAGR of 38.5% from 2026 to 2033.

The Global AI Governance Market growth is driven by escalating global regulatory and compliance requirements, mainstream enterprise AI adoption, and the increasing complexity of autonomous AI systems.

Key market opportunities in the Global AI Governance Market lie in sovereign cloud and data residency solutions, and embedding governance directly into enterprise platforms and development workflows.

The key players in the AI Governance market include Microsoft Corporation, Google LLC (Alphabet), SAP SE, Oracle Corporation, Salesforce Inc., Truera Inc.