- Automotive

- Africa Passenger Car Market

Africa Passenger Car Market Size, Trends, Share, and Growth Forecast, 2026 - 2033

Africa Passenger Car Market by Category of Vehicle (Sedans, SUVs, MPVs, Hatchbacks), Fuel Type (Petrol, Diesel, Hybrid/Electric), Price Category (Economy, Mid-Range, Premium/Luxury), Type of Vehicle (Used Passenger Car, New Passenger Car), and Countrywise Analysis for 2026 - 2033

Africa Passenger Car Market Size and Trends Analysis

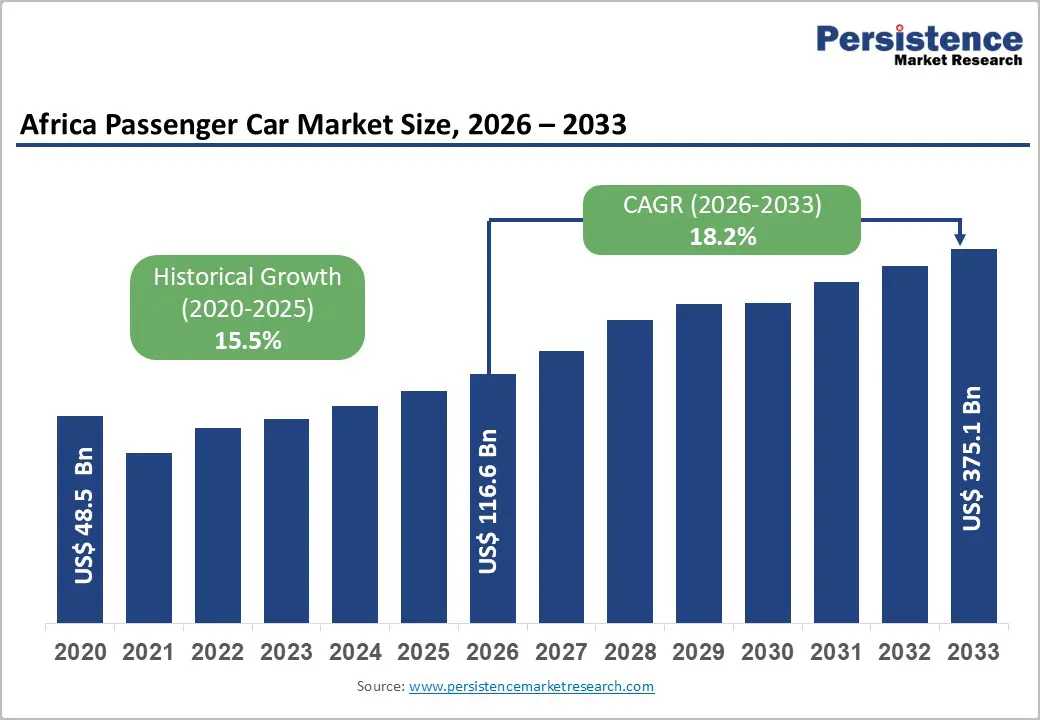

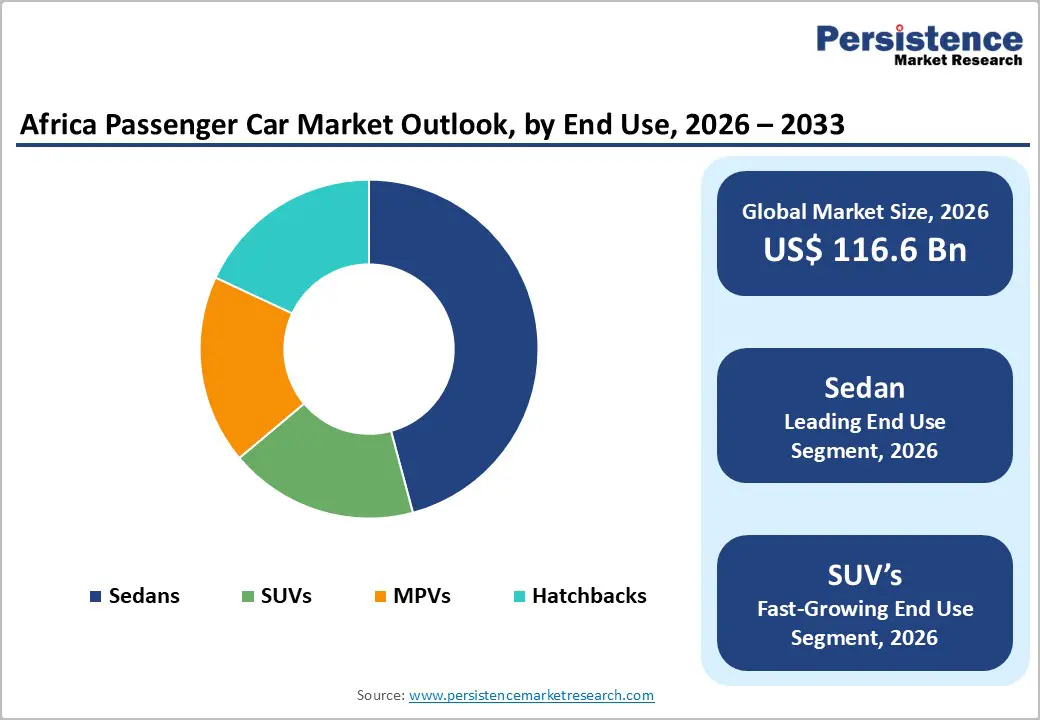

Africa passenger car market size is likely to be valued at US$ 116.6 billion in 2026, and is reach US$ 375.1 billion by 2033, expanding at a CAGRof 18.2% during the forecast period 2026 - 2033.

This substantial market expansion reflects structural shifts across the African continent, driven primarily by an expanding middle-class population, accelerating urbanization, and improved access to vehicle financing. The region's motorization rate remains significantly below global averages-approximately 45 vehicles per 1,000 people in Nigeria compared to the global average of 180-indicating substantial untapped demand potential. Government incentives supporting local manufacturing, combined with the African Continental Free Trade Area (AfCFTA) tariff harmonization framework, are systematically lowering barriers to new-vehicle adoption while catalyzing regional supply-chain integration and competitive market dynamics.

Key Industry Highlights:

- Vehicle Type: Sedans maintain dominance with 40%+ revenue share; however, SUVs capture fastest growth at 19.5% CAGR, with crossovers/compact SUVs reaching 37.7% of new-vehicle sales in South Africa.

- Fuel Type: Petrol vehicles command 70%+ revenue share; electric/hybrid powertrains accelerate at 23% CAGR, with EV adoption varying from 60% (Ethiopia) to 1-2% (South Africa) by geography and regulatory environment.

- Price Category: Economy segment dominates (55%+ share), while mid-range vehicles grow fastest at 20% CAGR, capturing aspirational consumers transitioning from used-vehicle purchases toward premium safety and technology features.

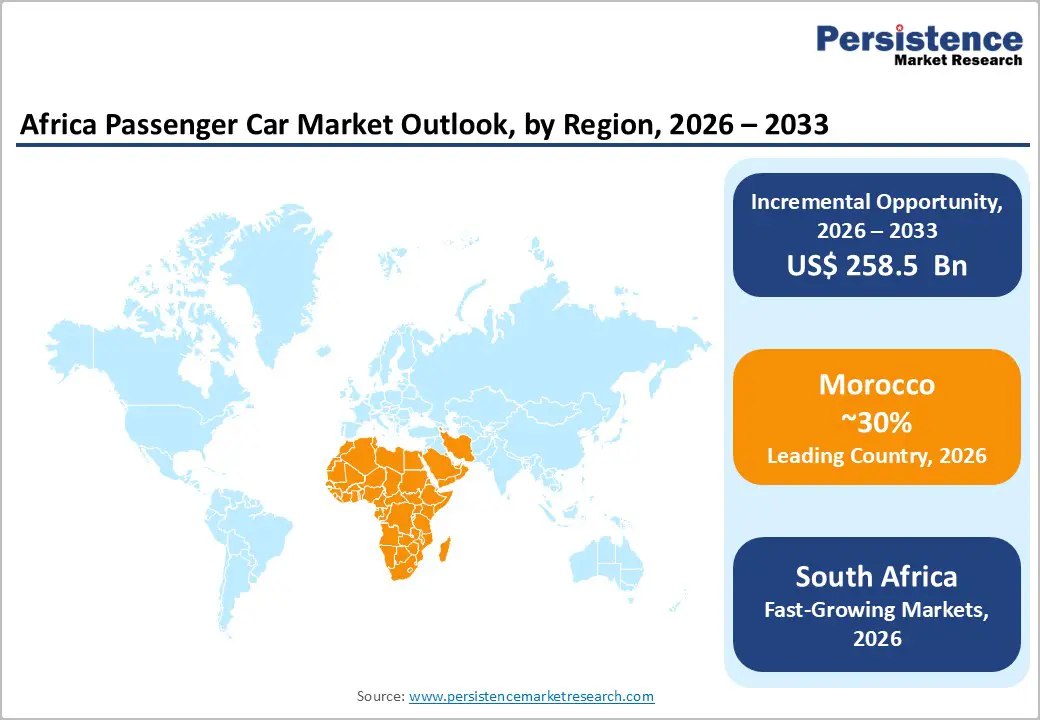

- Country-wise Growth Leaders: Morocco emerges as a continental leader commanding 60%+ market share, positioning as Africa's manufacturing hub through Renault, Stellantis, and BYD manufacturing investments totaling US$ 2.8+ billion.

- South Africa maintains 38% of market volume with 7-9% CAGR and a mature 100,000+ job automotive sector; however, faces production constraints and competitive pressure from Morocco's manufacturing expansion and Chinese brand market entry.

- Critical Market Developments: EV adoption accelerating with Africa's electric-vehicle market projected to reach US$ 4.2 billion by 2033 (56.3% CAGR), driven by government ICE-import bans (Ethiopia), zero-duty schemes (Ghana), and battery-cost reductions of 12-15% annually.

- Chinese OEM market entry (BYD, GWM, Chery) capturing 8-10% market share since 2022, introducing 25-30% price-discounted models and challenging incumbent profitability margins while expanding the addressable market toward price-sensitive consumer segments.

| Key Insights | Details |

|---|---|

| Passenger Car Market Size (2026E) | US$ 116.6 Bn |

| Market Value Forecast (2033F) | US$ 375.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 18.2% |

| Historical Market Growth (CAGR 2020 to 2025) | 15.5% |

Market Dynamics

Drivers - Rising Middle-Class Expansion and Enhanced Consumer Purchasing Power

Africa's middle-class population reached an estimated 460 million individuals in 2023 and is projected to expand toward 1.1 billion by 2060, according to the African Development Bank. This demographic transformation directly correlates with increased vehicle ownership aspirations, as rising disposable incomes elevate personal mobility from a luxury to an attainable priority. Urban centers, including Cape Town, Nairobi, and Casablanca, have experienced disproportionate concentration of income growth, with corresponding vehicle demand reflecting consumer preference for entry-level sedans and compact SUVs that balance affordability with functional versatility.

Financial innovation has amplified this demand trajectory: major banking institutions across South Africa, Kenya, and Morocco now offer auto loan tenors extending 72-84 months with down-payment reduction schemes, effectively lowering monthly payment burdens and broadening the addressable consumer base. Ride-hailing services such as Uber and Bolt, now operational in 15+ African nations, have created an ancillary market for fleet acquisition demand, in which operators systematize vehicle procurement through institutional financing mechanisms. This structural credit expansion is forecast to drive new passenger-car registrations at a 19.8% CAGR through 2033, substantially outpacing the growth of used-vehicle imports.

Restraint - Currency Volatility and Import Dependency for Advanced Components

The African passenger-car sector remains structurally dependent on imported advanced components, including powertrains, electronic control systems, and battery packs, exposing manufacturers and consumers to currency fluctuation and foreign-exchange volatility. Depreciation cycles in the South African rand, Nigerian naira, and Moroccan dirham have increased vehicle import costs by 15-22% during periods of acute currency weakness, directly constraining consumer purchasing power and new-vehicle affordability. Battery-pack imports from Asia account for 40-55% of EV production costs, making regional EV competitiveness highly sensitive to currency movements and global supply-chain disruptions. Local assemblers lack vertical integration capacity to manufacture high-specification components domestically, necessitating reliance on global suppliers and exposing profit margins to hedging costs and working-capital volatility. This structural constraint limits new-vehicle price competitiveness relative to grey-market used imports, which remain popular due to lower perceived total cost of ownership, potentially capping new-vehicle market penetration growth at 35-40% through 2033.

Opportunity - Battery Manufacturing Localization and Mineral Value-Chain Integration

Africa controls 92% of global platinum reserves, 56% of global cobalt, and substantial lithium, graphite, and nickel deposits essential for battery manufacturing. The DRC-Zambia copper-cobalt corridor, combined with Zimbabwe's lithium capacity and Madagascar's graphite resources, positions the continent to establish battery-cell manufacturing hubs capturing downstream value in the EV supply chain.

Current market projections indicate that localized battery manufacturing could reduce EV production costs by 20-28%, making African-assembled vehicles globally competitive while preserving profit margins within regional value chains. Governments in Rwanda, Ethiopia, and Kenya are actively negotiating foreign direct investment (FDI) agreements with battery manufacturers, including CATL and BYD, with public commitments totaling US$1.2 billion through 2027. Successful battery localization could transform Africa from a component-import-dependent to an EV-manufacturing exporter, supporting domestic assembly volumes of 500,000-800,000 units annually by 2030 and generating an estimated 85,000-120,000 skilled manufacturing jobs.

Category-wise Analysis

Product Type Insights - Sedans Dominate Africa Passenger Car Revenues While SUVs Drive Rapid Growth

Sedans remain the dominant vehicle category in the Africa passenger car market, accounting for over 40% of total revenue and maintaining a strong presence across diverse income groups. Entry-level and mid-range models such as the Toyota Corolla, Volkswagen Polo, Renault Clio, and Hyundai i20 continue to attract urban buyers due to their fuel efficiency, affordable maintenance, and proven reliability. Sedans generate the highest sales volumes across both new and used vehicle segments, supported by well-established dealer networks, widespread spare-parts availability, and long-standing consumer familiarity. Their suitability for daily commuting and intercity travel reinforces sustained demand, although competitive pressure is increasing as buyer preferences gradually shift.

In contrast, SUVs represent the fastest-growing vehicle segment, expanding at a robust CAGR of 19.5% and significantly outpacing overall market growth. Compact SUVs and crossovers are gaining rapid acceptance, driven by preferences for higher ground clearance, perceived safety, and versatility across varying road conditions. In markets such as South Africa, SUVs already account for 37.7% of new vehicle sales, with strong momentum across Kenya, Nigeria, and Morocco. Expanded offerings from global OEMs and emerging Chinese brands are accelerating this transition, positioning SUVs as a key long-term growth engine.

Fuel Type Insights - Petrol Dominates Africa Passenger Cars While Hybrid-Electric Vehicles Drive Growth

Petrol-powered vehicles continue to dominate the African passenger car market, accounting for over 70% of total revenue, reflecting the maturity of petrol fuel-distribution infrastructure, strong consumer familiarity with petrol engines, and favorable pricing compared with diesel alternatives. Petrol powertrains underpin the majority of entry-level and mid-range passenger cars, as manufacturers prioritize cost optimization and adaptability to varying regional fuel-quality standards. Well-established service ecosystems and widespread spare-parts availability further strengthen consumer confidence, particularly across rural and semi-urban areas where diesel supply chains remain inconsistent, and maintenance capabilities are limited. As a result, petrol vehicles remain the most practical and economically viable mobility solution across much of the continent.

At the same time, hybrid and electric vehicles represent the fastest-growing fuel-type segment, expanding at an estimated CAGR of 23.0%, supported by government-led electrification initiatives, declining battery costs, and the gradual expansion of charging infrastructure. Policy interventions such as Ethiopia’s ban on ICE vehicle imports, Kenya’s VAT exemptions, and Ghana’s zero-tariff framework are materially improving EV affordability. Ongoing battery-pack cost reductions of 12-15% annually are narrowing price gaps, enabling select EV models from BYD, Citroën, and Volkswagen to approach economy-segment parity. Hybrid vehicles are also gaining traction as transitional solutions, delivering 15-20% fuel savings while mitigating charging constraints, with market penetration projected to reach 3-5% by 2028.

Price Category Insights - Economy Cars Dominate Africa While Mid-Range Segment Drives Rapid Growth

The economy price category remains the dominant segment in the African passenger car market, accounting for over 55% of total revenue, reflecting the continent’s income distribution and strong preference for affordability among first-time vehicle buyers. Entry-level models priced between US$ 8,000 and US$ 15,000 form the largest addressable customer base, as they minimize upfront costs and financing burdens while meeting essential mobility needs. The segment’s leadership is further reinforced by the gradual expansion of auto-loan availability and improving access to formal financing in key urban markets. Automotive manufacturers such as Renault, Dacia, Hyundai, Chery, and GWM have strategically positioned economy vehicles as core volume and revenue drivers, with unit sales in this category exceeding those of premium segments by four to six times across major African markets.

In contrast, mid-range vehicles priced between US$ 15,000 and US$ 30,000 represent the fastest-growing price segment, expanding at a robust 20.0% CAGR. Growth is driven by rising consumer confidence, improving credit terms, and a growing base of aspirational buyers upgrading from used or entry-level vehicles. This segment includes compact SUVs, mid-size sedans, and crossovers that offer enhanced comfort, safety features, and in-vehicle technology while remaining relatively affordable. Manufacturers such as Hyundai, Kia, Volkswagen, and leading Chinese brands are aggressively expanding their mid-range portfolios, accelerating category penetration and reshaping Africa’s passenger car pricing landscape.

Vehicle Type Insights - Used Cars Dominate Revenue While New Vehicles Drive Africa’s Fastest Growth

Used passenger cars continue to dominate the African passenger car market, accounting for over 65% of total revenue, reflecting the region’s structural reliance on pre-owned vehicles driven primarily by affordability, proven reliability, and limited financing requirements. Large volumes of grey-market imports from developed economies underpin market supply, with countries such as Kenya and Uganda together importing more than 19,800 used vehicles annually. Despite this dominance, the used-car ecosystem faces structural constraints, including vehicle age restrictions typically capped between 7 and 10 years, limited transparency around vehicle history, and inconsistent pre-purchase inspection standards. Nevertheless, the significant price advantage of used vehicles ensures sustained demand, particularly among price-sensitive consumers and in rural and semi-urban geographies where purchasing power remains constrained.

In contrast, new passenger cars represent the fastest-growing segment, expanding at an estimated CAGR of 19.8%. Growth is being fueled by improving access to consumer financing, wider availability of competitively priced models, and supportive government policies aimed at strengthening local assembly and manufacturing. The implementation of the African Continental Free Trade Area (AfCFTA) has further reduced new-vehicle import costs by approximately 8-12%, narrowing the price gap with used imports. Additionally, rising procurement from ride-hailing operators, corporate fleet expansion, and increasing consumer preference for warranty coverage and advanced safety features are accelerating new-vehicle adoption across key urban markets.

Country-wise Insights and Trends

Morocco dominates Africa’s passenger car market through leadership and exports

Morocco has emerged as Africa’s undisputed passenger car market leader and manufacturing hub, commanding over 60% of continental passenger car revenue and anchoring the region’s automotive value chain. According to OICA, new passenger car sales in Morocco reached 471,950 units in 2023 and increased to 524,467 units in 2024, underlining the country’s strong demand momentum. The domestic passenger car market is valued at approximately US$ 4.5 billion, supported by sustained double-digit growth and rising export-oriented production. Morocco is Africa’s largest automotive exporter, shipping US$ 15.8 billion in automotive products in 2024, accounting for nearly 33% of national exports and exceeding South Africa’s automotive export volumes by an estimated 40-50%. This leadership is reinforced by large-scale manufacturing operations of Renault-Dacia and Stellantis, with combined production capacity exceeding 500,000 units annually and total output forecast at 614,000 units in 2024. Proactive industrial policies, tax incentives, and renewable energy integration have attracted US$ 3.2 billion in automotive investments through 2026, increasingly focused on electric vehicles, batteries, and software-defined technologies. Preferential trade access to the EU and regional agreements further strengthen Morocco’s position as the primary bridge between African automotive demand and European supply chains.

South Africa leads Africa’s automotive market amid pressures and transformation

South Africa remains Africa’s most industrially mature automotive market, contributing 38.29% of continental automotive volume in 2024, despite rising competitive pressure from Morocco’s expanding manufacturing base. According to OICA, new passenger car sales increased from 336,012 units in 2023 to 350,384 units in 2024, while total domestic new-vehicle sales reached 515,850 units in 2024 and are projected to exceed 536,612 units by end-2025, surpassing pre-pandemic levels for the first time in five years. However, production declined by 5% in 2024, falling from 599,755 units to 559,645 units, reflecting capacity constraints and market saturation.

The automotive sector generates US$ 45-50 billion annually, supports over 100,000 direct jobs, and contributes roughly 5% of national GDP. South Africa hosts assembly operations for Toyota, Volkswagen, Mercedes-Benz, Ford, and BMW, supported by a deeply integrated supplier ecosystem. Toyota leads new passenger car sales with 25-26% market share, followed by Volkswagen Group (12.9%), Suzuki (11.7%), Hyundai (6.1%), and Ford (5.9%). Consumer demand is dominated by compact SUVs and crossovers (37.7% of sales) and hatchbacks (36.2%), while grey-market used imports account for 45-50% of registrations. Since 2022, Chinese brands such as GWM, Chery, and Geely have captured 5-8% market share, intensifying price competition. Although the government targets 20-25% EV production by 2030, EV adoption remains limited (1-2% of sales) due to infrastructure gaps, grid instability, and cost barriers, delaying large-scale transition until post-2027.

Competitive Landscape

Africa's passenger-car market exhibits a consolidated competitive structure with the top 5 manufacturers commanding 60-65% of new-vehicle sales volume. Toyota dominates with 25-26% market share across South Africa and Kenya, leveraging locally-manufactured models and established dealer networks. Volkswagen Group (VW, Audi, Skoda) maintains 12-13% share through multi-brand portfolio strategies and price-segment diversification. Suzuki (11-12%), Hyundai (6-7%), and Ford (5-6%) maintain entrenched secondary positions. Chinese manufacturers, including GWM, Chery, BYD, and Geely have collectively captured 8-10% market share since 2022, establishing competitive intensity and driving price compression particularly in economy and mid-range segments. Market concentration reflects capital-intensity barriers and established distribution-network advantages, which constrain greenfield entrant prospects. However, electric-vehicle segments exhibit substantially lower concentration with BYD, Tesla, Citroën, and emerging startups challenging incumbents through technology differentiation and pricing innovation.

Key Industry Developments:

- In 2024, Renault strengthened its manufacturing presence in Morocco through expanded Tangier facility capacity, investing US$ 480 million to support production of next-generation Renault 5 compact EV models and Dacia platforms

- In 2024, BYD launched local assembly operations in South Africa, introducing three EV model lines into the domestic market at price points 25-30% below incumbent EV offerings. The company committed US$ 800 million in phased investment to establish battery-assembly capacity and vehicle-manufacturing facilities targeting 50,000-unit annual production by 2027.

- In 2024, Stellantis committed US$ 1.2 billion to accelerate EV platform manufacturing in Morocco through dedicated production lines for Peugeot, Citroën, and Opel brands. Production targets include 35,000 EV units annually by 2026, with explicit emphasis on affordability-focused models (US$ 12,000-20,000 price range).

Companies Covered in Africa Passenger Car Market

- Toyota Motor Corporation

- Volkswagen AG

- Suzuki Motor Corporation

- Hyundai Motor Company

- Ford Motor Company

- BYD Co., Ltd.

- Great Wall Motors (GWM)

- Renault Group

- Stellantis

- Mercedes-Benz AG

- BMW Group

- Chery Automobile Co.

- Mahindra & Mahindra

- Kia Motors

- General Motors (Isuzu, Chevrolet)

- Other Market Players

Frequently Asked Questions

The Passenger Car market is estimated to be valued at US$ 116.6 Bn in 2026.

The primary demand driver for the Africa passenger car market is the structural reliance on affordable personal mobility solutions, driven by rapid urbanization, limited public transportation infrastructure, and rising population growth across the continent.

In 2026, Morocco dominated the market with an exceeding 60% revenue share in the African passenger Car market.

Among the categories of vehicles, the Sedan passenger car has the highest preference, capturing beyond 40% of the market revenue share in 2026, surpassing other category of vehicles.

Toyota Motor Corporation, Volkswagen AG, Suzuki Motor Corporation, Hyundai Motor Company, Ford Motor Company, BYD Co., Ltd., Great Wall Motors (GWM), and Renault Group.