- Beverages

- South Africa UHT Milk Market

South Africa UHT Milk Market Size, Share, and Growth Forecast 2026 - 2033

South Africa UHT milk market by Product Type (Skimmed, Whole, Partly Skimmed, Fat Filled), by Source (Animal-based, Plant-based), by Sales Channel (Hypermarkets/Supermarkets, Specialist Retailers, Convenience Stores, Online Retail Stores, Others), and by Regional Analysis, 2026-2033

South Africa UHT Milk Market Share and Trends Analysis

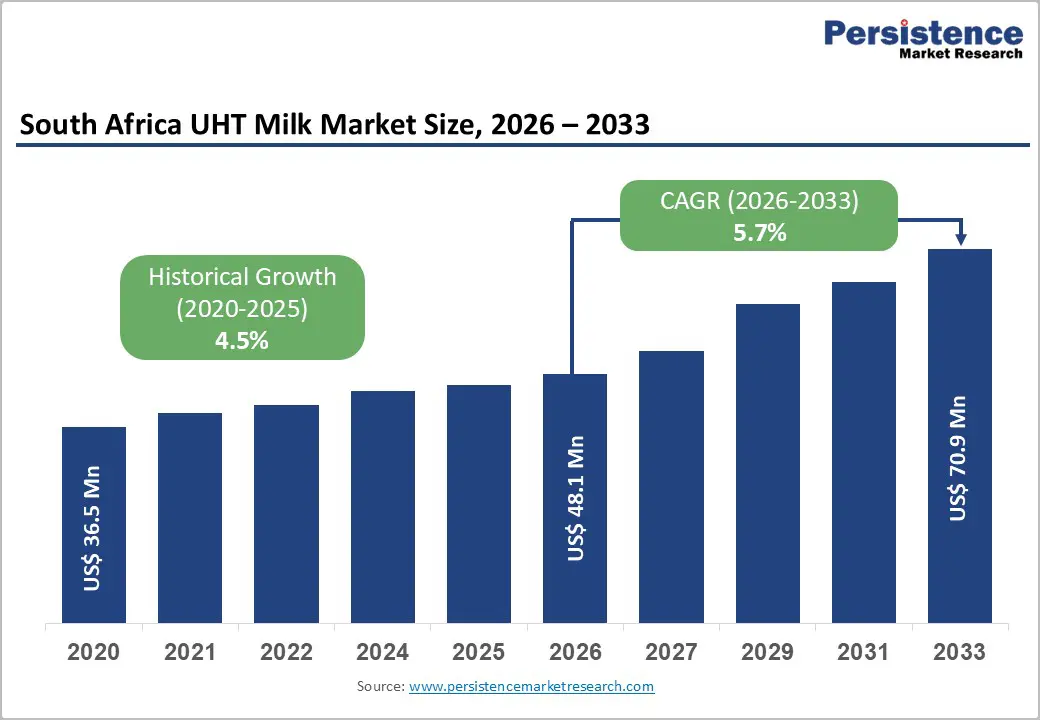

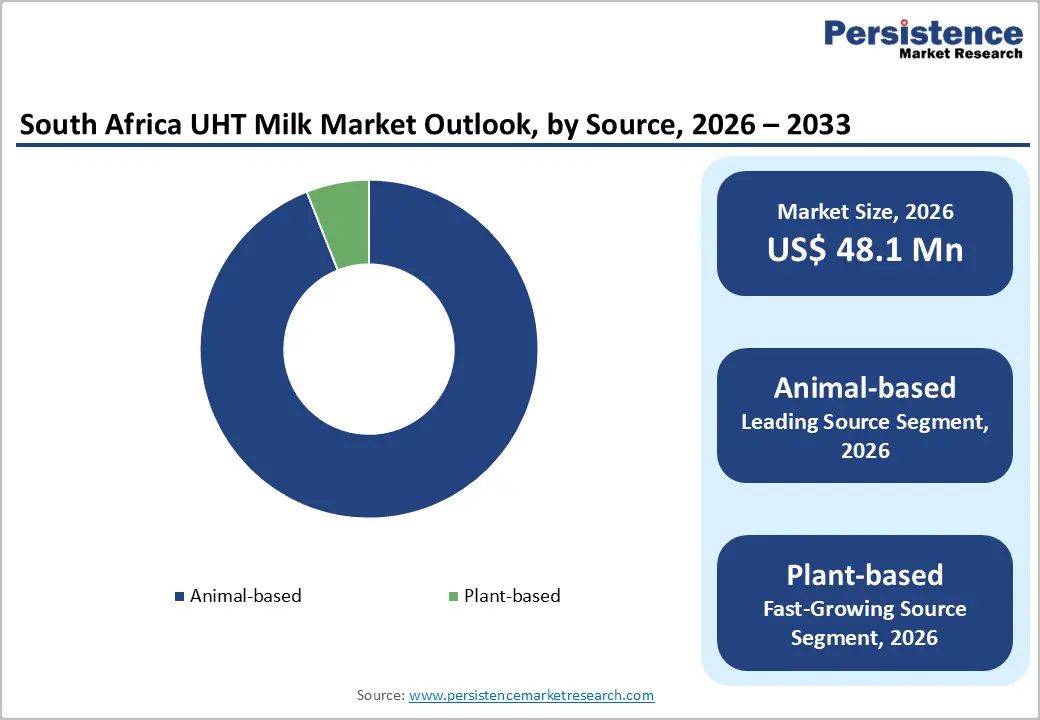

The global South Africa UHT milk market size is expected to be valued at US$ 48.1 million in 2026 and projected to reach US$ 70.9 million by 2033, growing at a CAGR of 5.7% between 2026 and 2033.

Urban lifestyles, evolving household structures, and ambient storage convenience are reshaping how milk is consumed across South Africa. UHT milk has moved from a fallback option to a pantry essential, supported by strong processing infrastructure, nationwide distribution, and growing interest in value-added dairy formats.

Key Industry Highlights

- Leading Product Type Segment: Whole UHT Milk, holding around 53% market share, driven by strong cultural preference for full-cream taste, creamy mouthfeel, and its role in everyday family nutrition and traditional foods.

- Fastest-Growing Product Type Segment: Partly Skimmed UHT Milk, supported by rising urban health awareness, calorie-conscious diets, and increasing concern over lifestyle-related conditions.

- Fastest-Growing Source Segment: Plant-Based UHT Milk, gaining traction among urban youth in Gauteng and Western Cape due to lactose intolerance awareness and sustainability-driven choices.

- Market Drivers: Rapid urbanization, busy work lifestyles, bulk shopping behavior, and the convenience of ambient storage without refrigeration.

- Market Opportunities: Expansion of fortified UHT milk variants and premium plant-based alternatives targeting wellness, immunity, and bone health.

| Key Insights | Details |

|---|---|

| South Africa UHT Milk Market Size (2026E) | US$ 48.1 Mn |

| Market Value Forecast (2033F) | US$ 70.9 Mn |

| Projected Growth (CAGR 2026 to 2033) | 5.7% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.5% |

Market Dynamics

Driver – Urbanization and Evolving Consumer Convenience Trends

The rapid pace of urbanization in provinces like Gauteng, Western Cape, and KwaZulu-Natal is a major catalyst for the market. As more South Africans migrate to metropolitan areas, there is a marked shift in dietary habits and shopping behaviors. Busy working professionals and "nuclear" families increasingly prefer bulk-buying groceries once a month rather than making frequent trips for fresh produce. The convenience of aseptic packaging, which allows UHT milk to be stacked in pantries without occupying precious refrigerator space, aligns perfectly with modern urban living. Data from Statistics South Africa (Stats SA) suggests that the urban population has surpassed 68% of the total population, directly expanding the primary consumer base for long-life products. Additionally, the increasing participation of women in the workforce has spurred the demand for convenient milk options for infant and child nutrition.

Restraints – Perception of Nutritional Inferiority and Taste Preferences

A lingering restraint in the South African market is the consumer perception that UHT milk is "less natural" than fresh pasteurized milk. The high-heat treatment process (typically 135°C to 150°C for a few seconds) can slightly alter the taste profile, occasionally resulting in a "cooked" or caramelized flavor that some traditionalists find unappealing. Consumer surveys conducted by various industry bodies indicate that approximately 35% of high-income households still prefer the sensory attributes of fresh milk for direct consumption. Additionally, health-conscious segments often incorrectly assume that the lack of refrigeration and the long shelf life are achieved through preservatives, although the shelf stability is purely a result of aseptic processing and packaging. Overcoming these misconceptions requires significant marketing investment from leading players like Clover and Lactalis.

Opportunity – Expansion of Plant-Based and Functional UHT Alternatives

The "health and wellness" trend is carving out a high-growth niche for plant-based and functional UHT milk in South Africa. Increasing awareness of lactose intolerance and the rise of veganism among urban youth are driving a surge in demand for UHT almond, oat, and soy milks. Unlike their fresh counterparts, UHT plant-based milks are easier for retailers to stock in large quantities. Furthermore, there is a massive opportunity for "fortified" animal-based UHT milk, targeting specific health needs such as bone density (calcium-enriched) or immune support (vitamin-D and zinc enriched). The Milk Producers' Organisation (MPO) has noted that the value-added dairy segment is growing at a faster rate than standard milk, as consumers seek "more than just basic nutrition" from their daily dairy intake. This allows manufacturers to command premium prices and improve profit margins.

Category-wise Analysis

Product Type Analysis

The Whole milk segment is the leading segment in the South Africa UHT Milk Market, capturing a dominant 53% market share in 2025. This dominance is rooted in the traditional South African palate, which favors the creamy texture and rich flavor of full-cream milk. Full-cream UHT milk is also viewed as a complete nutritional source for children, making it a non-negotiable item for many households. Justification for its leadership is further found in its widespread use in traditional South African beverages and porridges.

However, the Partly Skimmed (low-fat) segment is identified as the fastest-growing segment between 2025 and 2032. This shift is driven by a growing health-consciousness among urban middle-class consumers who are monitoring their fat and calorie intake to combat lifestyle diseases like obesity and diabetes, which have seen a rising prevalence in the country.

Source Analysis

Animal-based UHT milk remains the overwhelming leader in the market, holding approximately 94% of the share in 2025. The livestock sector is a cornerstone of South African agriculture, and cow's milk is deeply integrated into the national food security framework. The high protein and calcium content of bovine milk make it the "gold standard" for nutrition. Nevertheless, the Plant-based segment is the fastest-growing source, albeit from a smaller base. Driven by brands like Alpro and local innovators, plant-based UHT options are gaining traction in premium retailers like Woolworths and Checkers.

The growth of the plant-based segment is specifically concentrated in the Western Cape and Gauteng, where the "green-living" movement is most influential among Gen-Z and Millennial demographics.

Market Competitive Landscape

The South Africa UHT Milk Market is characterized by a high degree of consolidation, with a few dominant players controlling the majority of the processing capacity and distribution networks. CLOVER S.A. (PTY) LTD, Lactalis South Africa, and Woodlands Dairy are the "Big Three" that define the market's competitive rhythm. These companies employ aggressive strategies for expansion, often acquiring smaller regional dairies to increase their "milk pool" and logistical reach. Research and development trends are currently focused on sustainable packaging—reducing plastic usage and increasing the use of plant-based caps—and the development of "Native" proteins in dairy. Key differentiators include "Milk Sourcing" transparency and the efficiency of the "Ambient Supply Chain." Emerging business model trends show a move toward vertically integrated systems where processors work closely with a select group of large-scale commercial farmers to ensure a consistent supply of high-quality raw milk.

Companies Covered in South Africa UHT Milk Market

- Lactalis

- CLOVER S.A. (PTY) LTD

- Woodlands Dairy

- Dairy Group

- Farmgate Dairy

- Brookside Dairy Limited

- Others