- Chipsets & Processors

- Massive MIMO Market

Massive MIMO Market Size, Share, and Growth Forecast, 2026 - 2033

Massive MIMO Market by Antenna Array Type (16T16R, 32T32R, 64T64R, 128T128R & Above), Technology (LTE Advanced, LTE Advanced Pro, 5G), Spectrum (TDD [Time Division Duplex], FDD [Frequency Division Duplex]), End-user, and Regional Analysis for 2026 - 2033

Massive MIMO Market Size and Trends Analysis

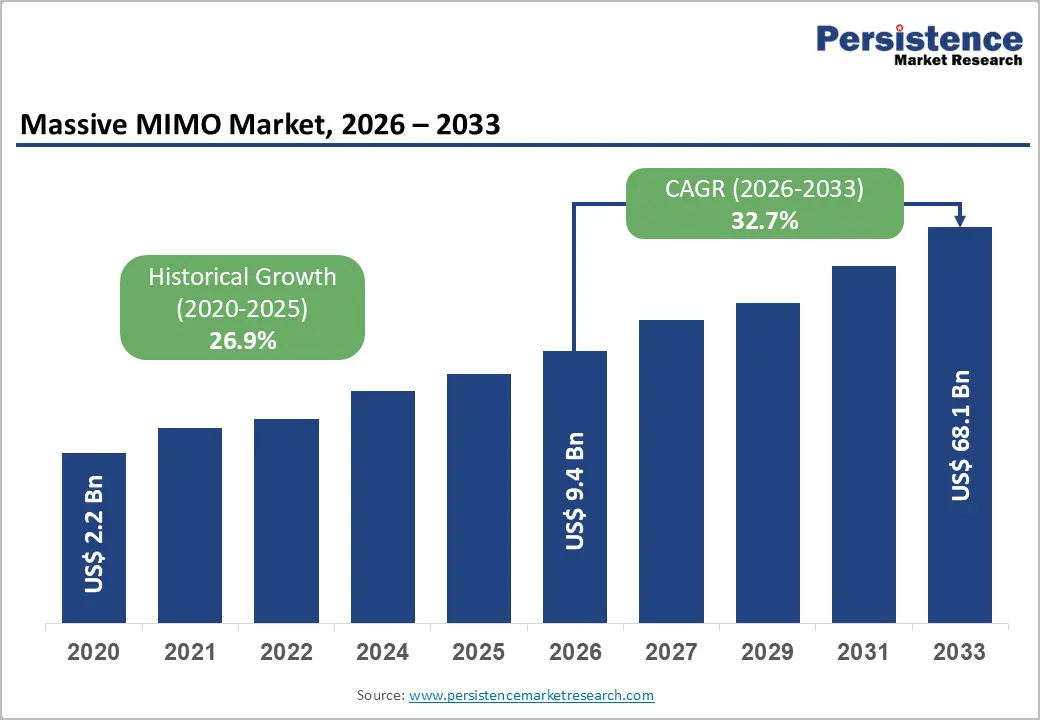

The global massive MIMO market size is projected to rise from US$9.4 billion in 2026 to US$68.1 billion by 2033. It is anticipated that the market will grow at a CAGR of 32.7% from 2026 to 2033, driven by the surge in mobile data traffic, widespread 5G network deployments, and the need for higher spectral efficiency and network capacity.

The increasing adoption of advanced technologies such as AI-driven beamforming, network slicing, and ultra-dense networks further fuels demand. Telecom operators are upgrading legacy infrastructure to meet rising connectivity and low-latency requirements, supporting the market’s expansion.

Key Industry Highlights:

- Leading Antenna Array Type: 64T64R dominates with over 38% market share in 2026, valued above US$ 3.6 Bn, offering an optimal balance of spectral efficiency, coverage, and cost. 128T128R & above is the fastest-growing at 41.6% CAGR, driven by demand for ultra-high capacity, advanced beamforming, and dense urban coverage.

- Leading Technology: LTE-Advanced holds over 36% market share in 2026, valued at over US$ 3.4 Bn, supporting high-speed connectivity with cost-effective upgrades. 5G is the fastest-growing at 42.6% CAGR, as Massive MIMO is critical for achieving low latency, high spectral efficiency, and advanced use cases.

- Leading Spectrum: TDD leads with over 63% market share in 2026, valued at over US$5.9 Bn, enabling dynamic uplink/downlink allocation and efficient beamforming. FDD shows significant growth due to legacy network continuity and new innovations improving FDD Massive MIMO viability.

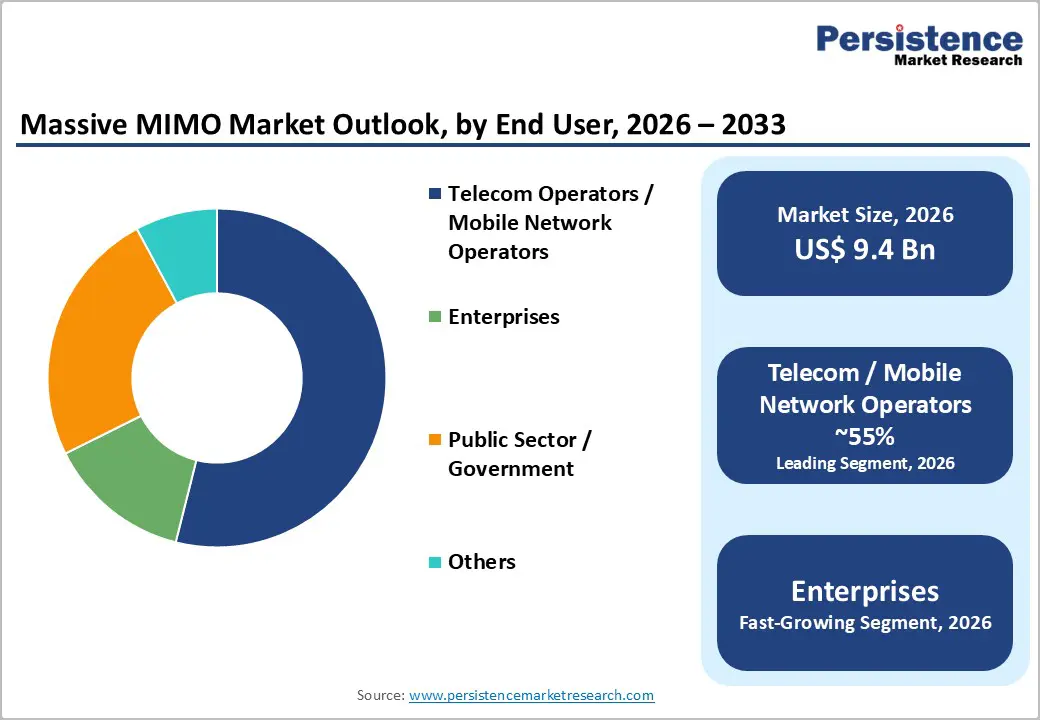

- Leading End-user: Telecom / mobile network operators hold over 55% market share in 2026, valued above US$ 5.2 Bn, driven by the need for high-speed, low-latency 5G services. Enterprises are growing fastest at a 43.1% CAGR, adopting private 5G networks for manufacturing, healthcare, smart campuses, and real-time applications.

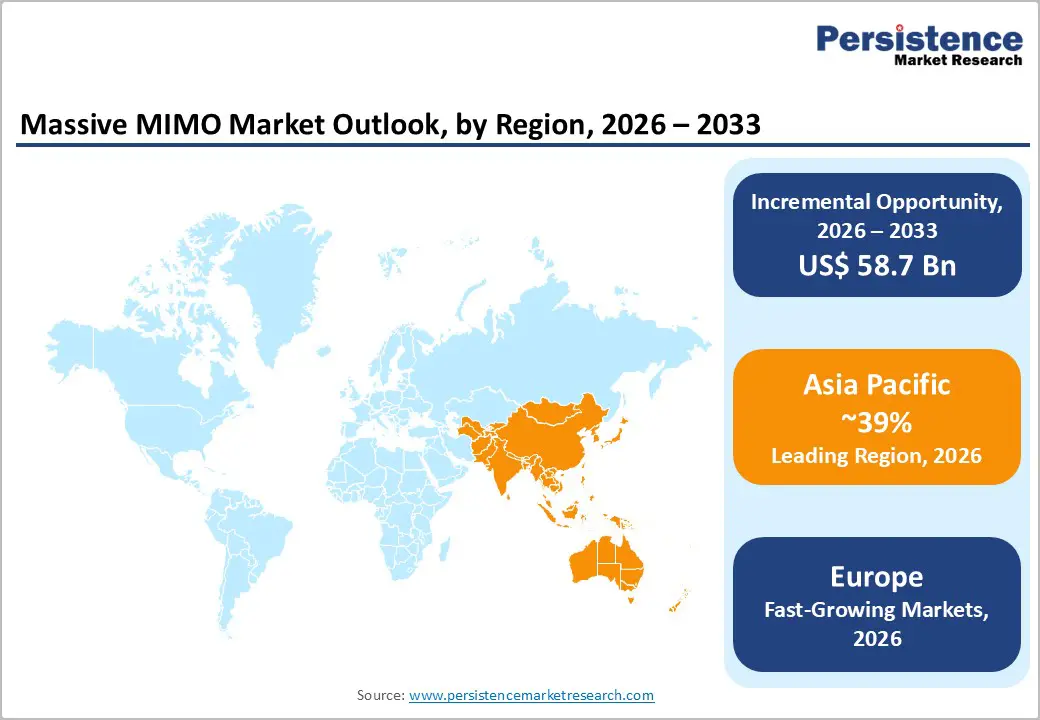

- Leading Region: Asia Pacific leads with over 39% share in 2026, valued above US$ 3.7 Bn, led by China, Japan, and emerging India deployments. North America holds 31% share at US$ 2.9 Bn, driven by C-band and 2.5 GHz expansions. Europe holds over 18% share, led by Germany, UK, France, and Spain, with regulatory support and vendor diversification initiatives.

| Key Insights | Details |

|---|---|

| Massive MIMO Market Size (2026E) | US$9.4 Bn |

| Market Value Forecast (2033F) | US$68.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 32.7% |

| Historical Market Growth (CAGR 2020 to 2025) | 26.9% |

Market Dynamics

Driver - 5G Network Deployment and Infrastructure Modernization

The global rollout of 5G networks and ongoing infrastructure modernization are key catalysts for the massive MIMO market. Telecom operators are upgrading legacy 4G radio access networks with Massive MIMO-enabled base stations to support enhanced mobile broadband, ultra-low latency, and higher network capacity. Technology is critical for efficiently utilizing mid-band and high-band 5G spectrum, where advanced beamforming is required to overcome propagation challenges and improve coverage. Large-scale network densification initiatives, including small cells and heterogeneous networks, further accelerate Massive MIMO adoption. As global 5G population coverage is projected to approach ~60% by the end of 2025, demand for advanced radio technologies that enhance capacity and performance continues to rise.

Rising Mobile Data Traffic and Connected Device Proliferation

Rapid growth in mobile data consumption, driven by video streaming, cloud services, online gaming, and real-time applications, is placing significant strain on existing network capacity. Simultaneously, the proliferation of connected devices, including smartphones, IoT sensors, wearables, and smart infrastructure, is increasing user density and traffic concurrency across networks. Massive MIMO addresses these challenges by enabling simultaneous multi-user transmission, significantly improving spectral efficiency and overall throughput without additional spectrum. This capability allows operators to manage dense usage environments and maintain quality of service. According to Ericsson, global mobile network data traffic reached 188 Exabytes per month in Q3 2025, underscoring the urgency for scalable capacity solutions such as Massive MIMO.

Restraint - Regulatory Spectrum Fragmentation and FDD-TDD Allocation Divergence

Massive MIMO performs optimally in TDD bands due to channel reciprocity, while many regions still rely heavily on fragmented FDD spectrum, reducing achievable gains. Variations in national spectrum policies force equipment vendors to design region-specific hardware, increasing R&D and manufacturing costs. Lack of harmonized mid-band spectrum delays large-scale deployments and cross-border interoperability. Operators face higher integration and optimization complexity when managing mixed FDD-TDD networks. This fragmentation slows network rollouts, reduces economies of scale, and dampens return on investment for telecom operators.

Capital Intensity and Infrastructure Deployment Costs

Massive MIMO deployment requires substantial capital investments in advanced antenna systems, radio access equipment, baseband processing infrastructure, and network integration services. The complexity of antenna array design, coupled with requirements for specialized installation expertise and site preparation, creates significant cost barriers, particularly for emerging market operators with constrained capital budgets. While the technology delivers superior long-term return on investment through enhanced spectral efficiency and reduced operational costs, the upfront capital requirements inhibit adoption among smaller regional operators and rural telecom providers, thereby limiting the total addressable market.

Opportunity - Open RAN Ecosystem Maturation and Multivendor Network Architectures

Standardized O-RAN interfaces enable Massive MIMO radios from different suppliers to interoperate seamlessly, reducing vendor lock-in and broadening operators' procurement choices. This shift expands the addressable market for specialized and regional Massive MIMO vendors previously excluded from integrated RAN deployments. As operators prioritize flexibility, innovation, and supply-chain resilience, Open RAN-based deployments are expected to contribute a significant share of Massive MIMO revenues by 2030, accelerating competitive adoption and market diversification.

Millimeter Wave and Higher Frequency Band Expansion

Millimeter wave (mmWave) and higher-frequency bands are increasingly being adopted to unlock the wide bandwidth needed for ultra-high data rates and low-latency 5G services. These bands face challenges such as high path loss, limited coverage, and sensitivity to blockages, making advanced antenna technologies essential. Telecom operators deploying mmWave for urban hotspots, enterprise networks, and fixed wireless access are driving demand for high-capacity Massive MIMO solutions. Spatial multiplexing enables multiple users to be served simultaneously, thereby maximizing spectrum utilization. As networks evolve toward advanced 5G and early 6G use cases, Massive MIMO becomes a foundational technology for successful high-frequency deployments.

Category-wise Analysis

Antenna Array Type Insights

64T64R dominates the global market, capturing more than 38% market share in 2026 with a value exceeding US$ 3.6 Bn as it provides an optimal balance between spectral efficiency, coverage, and cost. It supports high-capacity data transmission, enabling operators to meet the surging demand for 5G services like HD video streaming, cloud applications, and IoT connectivity. Its scalability allows deployment in both urban and suburban areas, ensuring robust network performance without excessive infrastructure investment. They are compatible with most existing base stations, reducing integration complexity and accelerating rollout.

128T128R & above demonstrates the highest growth rate at 41.6% CAGR due to network operators increasingly demanding ultra-high capacity and spectral efficiency to handle surging mobile data traffic. These higher-order arrays support more simultaneous users, advanced beamforming, and better coverage in dense urban areas. They are essential for mid- and high-band 5G deployments, supporting low-latency applications like AR/VR, autonomous vehicles, and industrial IoT. As traffic and service complexity grow, operators are upgrading to 128T128R to future-proof networks.

Technology Insights

LTE advanced holds over 36% market share in 2026 with a value exceeding US$ 3.4 Bn as it continues to serve as the backbone for high-speed mobile connectivity in many regions, supporting growing data traffic and broadband demands. Its widespread deployment enables operators to enhance spectral efficiency and network capacity with massive MIMO without overhauling existing infrastructure. LTE-Advanced’s compatibility enables cost-effective network upgrades while meeting user demand for low-latency, high-speed services.

5G is expected to grow at the highest rate, with a CAGR of 42.6% driven by accelerating operator 5G deployment strategies and increasing end-user device penetration. It benefits from vastly superior spectral efficiency, lower latency characteristics, and enhanced support for advanced use cases, including autonomous vehicles, extended reality applications, and industrial IoT. Massive MIMO adoption in 5G networks is virtually mandatory rather than optional, as 5G performance targets are unattainable without advanced antenna systems.

Spectrum Insights

TDD (Time Division Duplex) commands the largest market share at over 63% in 2026, with a value exceeding US$ 5.9 Bn, due to its ability to dynamically allocate uplink and downlink capacity based on traffic demand and its efficient support for data-intensive applications such as video streaming, cloud services, and IoT. It also reduces spectrum costs by using a single frequency band for both uplink and downlink. TDD enables advanced beamforming and accurate channel state feedback, improving spectral efficiency and overall network performance.

FDD (Frequency Division Duplex) is expected to grow at a significant rate due to its persistent importance in established wide-area coverage networks and legacy system continuity. FDD's fixed uplink and downlink frequency separation creates challenges for advanced beamforming techniques, but Samsung's recent innovations addressing FDD-specific technical constraints have substantially improved FDD Massive MIMO commercial viability. FDD dominance in North American spectrum allocations and European legacy networks ensures continued demand for FDD-capable solutions throughout the forecast period.

End-user Insights

Telecom operators/mobile network operators maintain a dominant market position with over 55% market share in 2026 and a value exceeding US$ 5.2 Bn, as they seek to meet the soaring demand for high-speed, low-latency 5G services. Massive MIMO enables them to increase network capacity, support more simultaneous connections, and improve spectral efficiency, which is critical for urban and high-traffic areas. Operators are also focused on upgrading existing infrastructure to handle exponential mobile data growth.

Enterprise is projected to grow at the highest rate, with a CAGR of 43.1%, driven by increasing demand for private 5G networks across industries such as manufacturing, logistics, healthcare, and smart campuses. Enterprises need ultra-reliable, low-latency connectivity to support AR/VR applications and high-density wireless environments. It enables higher spectral efficiency and network capacity, allowing businesses to handle heavy data traffic and real-time applications. Enterprises are adopting digital transformation initiatives that require robust wireless infrastructure for automation, analytics, and secure communication.

Regional Insights

North America Massive MIMO Market Trends

North America maintains market leadership with over 31% share in 2026, reaching US$ 2.9 Bn value driven by substantial investments from major North American operators in 5G network modernization and expansion of mid-band spectrum, particularly C-band and 2.5 GHz frequencies. A supportive regulatory environment led by the FCC, through structured spectrum auctions and clear licensing frameworks, has accelerated 5G infrastructure deployment and vendor competition. Leading operators are investing heavily to enhance network capacity and spectral efficiency. Verizon has conducted large-scale virtualized 5G RAN trials with Samsung, while T-Mobile has signed multi-year, multi-billion-dollar 5G equipment agreements with Nokia and Ericsson.

Asia Pacific Massive MIMO Market Trends

Asia-Pacific is expected to hold over 39% market share in 2026, reaching US$ 3.7 Bn in value. China leads Asia Pacific massive MIMO deployments, driven by strong state-backed 5G investment and large-scale rollouts by China Mobile, China Unicom, and China Telecom, making it the world’s largest 5G and Massive MIMO market. China began early FDD and TDD Massive MIMO field trials around 2016-2017, accelerating domestic vendor capabilities and commercial adoption. Japan has expanded Massive MIMO within its 5G networks, with NTT DOCOMO deploying advanced 4.5 GHz Massive MIMO radios in partnership with vendors such as Ericsson. India is an emerging market, supported by rapid 5G expansion, rising data consumption, and large-scale Massive MIMO deployments by leading operators.

Europe Massive MIMO Market Trends

Europe is expected to hold more than 18% share by 2026, with concentrated deployments in Germany, the United Kingdom, France, and Spain, reflecting regional regulatory harmonization and vendor diversification priorities. European regulatory authorities have mandated vendor diversification across operator procurement, specifically to limit dependence on single infrastructure suppliers and support open-architecture implementations. Germany, as the region’s largest economy and industrial hub, has prioritized Massive MIMO deployment to support manufacturing competitiveness and smart factory initiatives. United Kingdom operators have pursued independent 5G strategies following regulatory separation from EU frameworks, while maintaining a commitment to advanced antenna systems and potentially diverging on specific technical standards.

Competitive Landscape

The massive MIMO market is consolidated but rapidly evolving, with few established infrastructure vendors commanding over 60% of total market revenue while facing rising competition from specialized Open RAN vendors, emerging technology providers, and regional integrators. Manufacturers maintain market leadership through comprehensive vertical integration, global scale, and continuous innovation in antenna and AI-driven technologies. Others focus on lightweight, energy-efficient designs, Open RAN compatibility, and modular or virtualized architectures to enable deployment flexibility and cloud-native networks.

Key Industry Developments:

- In December 2025, Ericsson’s AIR 3255 Massive MIMO radios are now live on NTT DOCOMO’s 5G network, covering the 4.5?GHz band to handle high traffic demand. The 13?kg, energy-efficient units reduce power use by 25% and CO? footprint by 20%, while supporting multi-user MIMO for improved network performance, flexibility, and customer experience.

- In October 2025, Tejas Networks launched its next generation 64T64R Massive MIMO radio, Ojas64, at IMC 2025 in New Delhi, offering up to 320W output, multi-gigabit speeds, and significant spectral efficiency gains with a reduced carbon footprint.

Companies Covered in Massive MIMO Market

- Huawei Technologies Co., Ltd.

- Ericsson AB

- Nokia Corporation

- Samsung Electronics Co., Ltd.

- ZTE Corporation

- NEC Corporation

- Fujitsu Limited

- CommScope Inc.

- Airspan Networks Inc.

- Mavenir Systems, Inc.

- Others

Frequently Asked Questions

The global market is projected to be valued at US$9.4 Bn in 2026.

The need for higher network capacity, faster data speeds, and ultra-reliable connectivity to support growing data traffic, IoT devices, and high-density urban deployments is a key driver of the market.

The Massive MIMO market is expected to witness a CAGR of 32.7% from 2026 to 2033.

Rural and urban network densification, and integration with advanced technologies like AI-driven beamforming and network slicing, is creating strong growth opportunities.

Huawei Technologies Co., Ltd., Ericsson AB, Nokia Corporation, Samsung Electronics Co., Ltd., and ZTE Corporation are among the leading key players.