ID: PMRREP11149| 214 Pages | 27 Nov 2025 | Format: PDF, Excel, PPT* | IT and Telecommunication

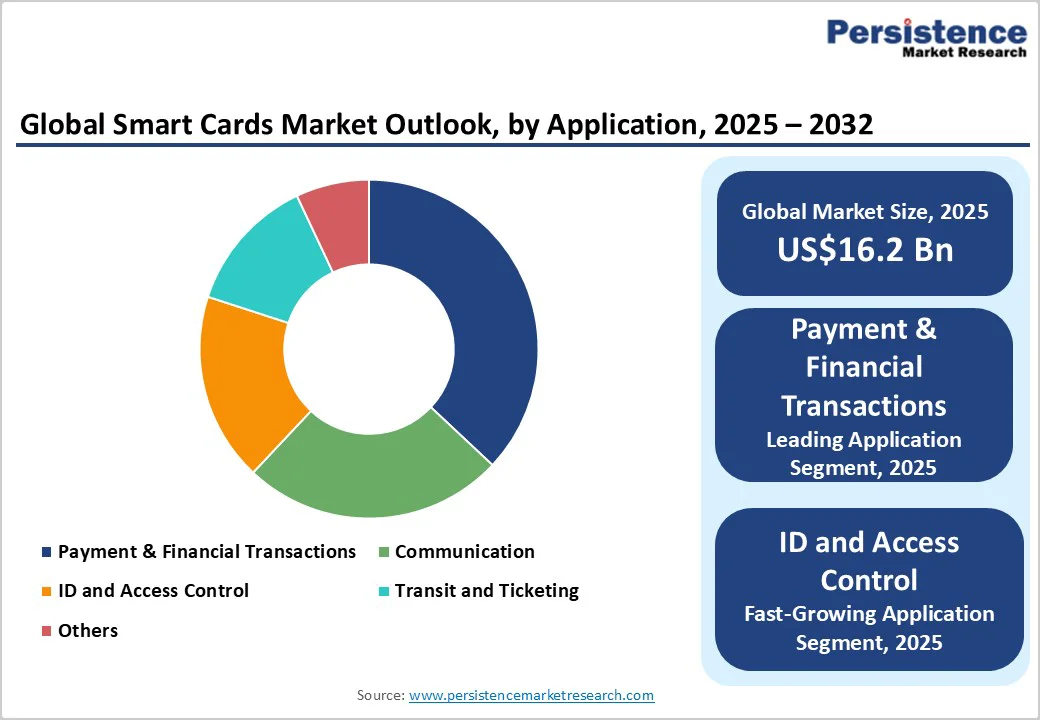

The global smart cards market size is likely to be valued at US$16.2 Billion in 2025 and is expected to reach US$25.4 Billion by 2032, growing at a CAGR of 6.5% during the forecast period from 2025 to 2032, driven by the rising demand for secure user authentication, data encryption, and subscriber identity management in mobile networks.

The rapid adoption of 5G networks, IoT devices, and mobile payment systems is further boosting the demand for smart cards. The ongoing shift toward cashless transactions and digital governance initiatives is fueling market expansion. Advancements in multi-application, biometric, and NFC-enabled smart cards are enhancing functionality and enabling broader deployment across various sectors.

| Key Insights | Details |

|---|---|

|

Smart Cards Market Size (2025E) |

US$16.2 Bn |

|

Market Value Forecast (2032F) |

US$25.4 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

6.5% |

|

Historical Market Growth (CAGR 2019 to 2024) |

4.8% |

The shift toward cashless and contactless payments is driving smart card adoption globally, fueled by hygiene concerns and the demand for frictionless transactions. Financial institutions and retailers are increasingly issuing EMV-compliant and multi-application smart cards to enhance transaction speed, security, and user experience. Government initiatives promoting digital wallets, e-payments, and fintech integration are opening new growth avenues. Contactless usage has surged, with Barclays reporting 94.6% of in-store payment cards contactless in 2024 compared to 53.8% in Europe during 2022, while the U.S. saw 24% of contactless payments via smartphones and wearables according to the 2024 Debit Issuer Study, reflecting enduring post-pandemic consumer preferences.

National governments are increasingly deploying smart cards as core infrastructure for digital governance, national security, and financial inclusion. Large-scale programs, such as India’s Aadhaar system with over 1.38 billion IDs issued by mid-2024, are driving demand across ID verification, banking, access control, and welfare delivery. Regulatory frameworks such as the EU’s eIDAS 2.0 and GCC-wide e-ID rollouts further expand smart card adoption in citizen identification, border control, healthcare, and social security systems. These initiatives extend the market beyond payment cards, creating multi-decade revenue opportunities, with 72% of digital ID adoption in Asia Pacific and 15% in Europe, according to Thales Group.

Smart card adoption is hindered by high infrastructure investment and integration complexity. Merchants and transport authorities must spend heavily on upgrading POS terminals, card readers, and backend systems to support contactless payments and advanced authentication. Small and medium enterprises, especially in emerging markets, often face capital constraints that delay deployment. The need to maintain compatibility with legacy magnetic stripe and contact-based cards adds further complexity. Uneven infrastructure readiness results in slower adoption in secondary cities and rural areas compared to developed economies and major metropolitan regions.

The rapid expansion of mobile payment applications, digital wallets, and cloud-based credential systems is limiting demand for traditional smart cards. With global smartphone penetration exceeding 86% of adults and 68% owning smartphones, according to the World Bank 2025 Global Findex report, NFC-enabled devices now support contactless transactions without physical cards. Leading platforms such as Apple Pay, Google Pay, and Samsung Pay have built extensive merchant networks and large consumer bases, offering seamless device integration and biometric authentication. These solutions reduce the need for card manufacturing, distribution, and replacement, challenging conventional smart card adoption.

Next-generation smart card technologies such as biometric authentication, blockchain integration, AI-powered fraud detection, and SoC designs are driving premium adoption in banking, government ID programs, and fintech. Biometric payment cards, including fingerprint and facial recognition, are gaining traction, exemplified by China’s Construction Bank launching fingerprint-enabled “hard wallet” cards for digital yuan transactions. Expansion of smart city infrastructure across Asia Pacific, the Middle East, and Latin America for transport, utilities, and citizen services is creating distributed demand. With over 80% of countries adopting National Urban Policies and 93% prioritizing urban development according to UN-Habitat’s World Smart Cities Outlook 2024, government-backed smart city initiatives present significant opportunities for integrated smart card solutions.

The growing shift toward contactless fare collection in urban mobility presents a significant opportunity. By enabling seamless travel across buses, metros, trains, and ferries, smart cards improve operational efficiency, reduce cash handling, minimize fare evasion, and accelerate boarding times. Transit authorities are increasingly leveraging usage data to optimize routes, schedules, and capacity planning, while multi-modal integration with parking and bike-sharing enhances card utility. Governments and private operators are investing in interoperable, high-security infrastructure, particularly in rapidly urbanizing regions. The automated fare collection market is projected to grow exponentially by 2032.

MPU microprocessors are expected to account for more than 58% of the market share in 2025, due to their high processing capabilities, which meet the growing demands for secure transactions, complex applications, and multi-functionality. Microprocessor cards contain complete computing architectures, including arithmetic logic units, control units, and memory hierarchies, enabling sophisticated cryptographic operations, dynamic transaction processing, and multifunctional application support. Their flexibility and security make them the preferred choice for modern smart card applications.

Memory is projected to grow at a significant rate due to the rising need for storing larger volumes of user data, authentication credentials, and transaction records in applications such as banking, telecom, and government IDs. Increasing adoption of multi-application smart cards such as those combining payment, identification, and access control requires higher storage capacity. The expansion of IoT, e-Governance, and digital identity programs also fuels demand for high-memory chips. Memory cards offer simplified architectures with reduced manufacturing complexity and lower unit costs compared to microprocessor alternatives, enabling deployment in price-sensitive applications.

Contactless interfaces are expected to cross more than 46% share with value, due to the growing need for faster, secure, and hygienic transactions across sectors such as banking, transportation, and retail. The rise of digital payments, tap-and-go transit systems, and access control in smart cities has accelerated adoption. Consumers increasingly prefer contactless solutions for convenience and reduced physical contact, especially post-pandemic. Advancements in NFC and RFID technologies have made contactless cards more reliable and widely accepted globally.

Dual interfaces are expected to grow at the highest CAGR, as they combine the convenience of contactless transactions with the security of contact-based systems, addressing the rising need for flexible and secure payment and identification solutions. Governments and enterprises are also embracing dual-interface ID and access cards to enhance interoperability and user convenience. These hybrid architectures allow organizations to retain existing contact-based infrastructure while smoothly transitioning to contactless systems without disrupting operations.

Payment & financial transactions are expected to account for more than 37% share in 2025, driven by the growing need for secure and contactless payment methods. The shift toward cashless economies, propelled by e-commerce expansion, digital banking, and mobile wallet adoption, has accelerated smart card usage. Rising concerns over data theft and fraud have led banks and consumers to prefer EMV and NFC-enabled smart cards for enhanced security. The integration of biometric authentication further meets user demand for faster and safer transactions, while EMV chip standards ensure continued replacement demand throughout card lifecycles.

ID and access control are expected to grow at the highest CAGR, driven by the increasing need for secure identity verification and restricted area access across various sectors. Rising threats of data breaches and identity theft are accelerating the adoption of advanced contactless and biometric smart cards. These solutions enable efficient monitoring, attendance tracking, and access authorization while seamlessly integrating with digital databases. The growing demand for interoperability, automation, and real-time authentication across both public and private infrastructures is fueling this segment’s rapid expansion.

IT & Telecom is expected to account for more than 41% share by 2025, due to the growing need for secure user authentication, subscriber identity management (SIM cards), and data encryption in mobile and digital communication networks. The rapid expansion of 5G networks, IoT devices, and mobile payment systems further drives smart card adoption for secure connectivity. Telecom operators rely on embedded SIMs (eSIMs) and multi-application smart cards to streamline customer access, enhance service personalization, and reduce fraud in digital ecosystems.

The government and public sector are driving rapid growth with a high CAGR, due to increasing demand for secure citizen identification, efficient welfare distribution, and streamlined public services. The rising focus on digital governance, e-passports, national ID programs, and social security schemes is boosting the need for tamper-proof and contactless smart cards. The requirement for secure, verifiable, and easily manageable identification solutions is driving large-scale deployments, significantly contributing to market expansion.

North America is driven by regulatory compliance, advanced technology adoption, and rising demand for secure identity solutions. Stringent standards such as PCI DSS, EMV chip mandates, NIST guidelines, and the REAL ID Act (effective May 2025) are accelerating adoption across payment, government, and border control sectors, with over 93% of travelers already using compliant IDs, noted by the Transportation Security Administration. Healthcare digitization and enterprise security needs are fueling demand for patient identification, secure access, and single sign-on solutions.

Large organizations, campuses, and government agencies increasingly deploy contactless or dual-interface smart cards to prevent fraud and strengthen authentication, expanding use beyond banking and consumer ID.

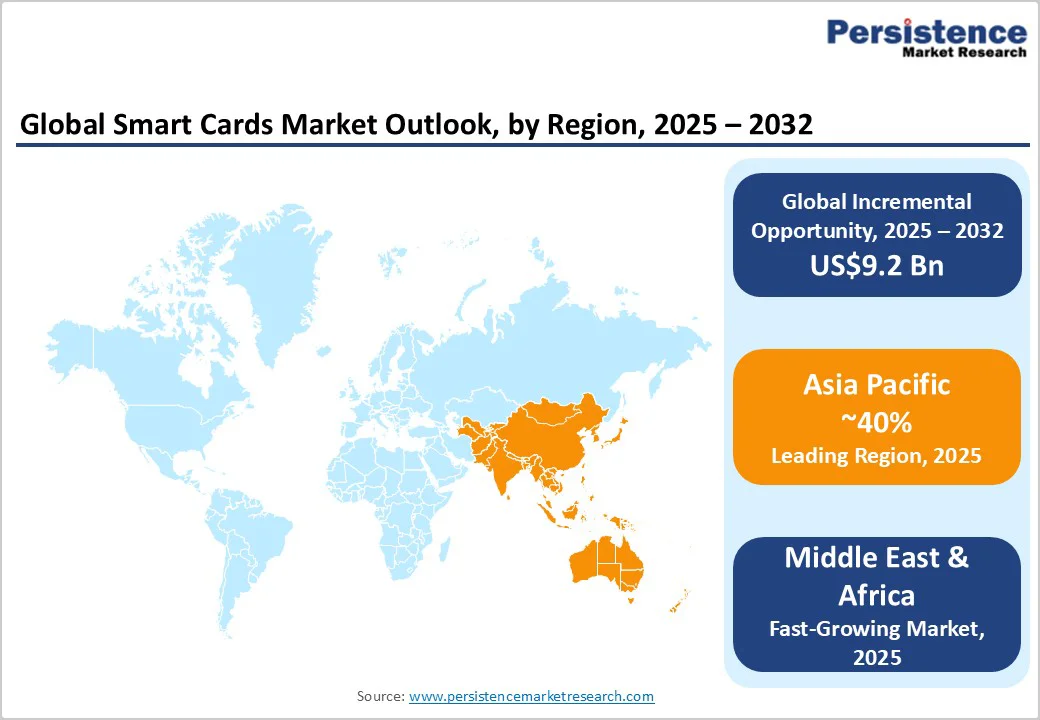

Asia Pacific is projected to account for over 40% of the smart cards market by 2025, driven by large-scale government initiatives such as India’s Aadhaar program and Japan’s healthcare smart card adoption. Regional manufacturing advantages in China and Taiwan support cost leadership, while multi-application cards enhance citizen service efficiency, e.g., China’s Digital Social Security Card has reached ~1.38 billion people and enabled over 50 billion digital service interactions. Growing urbanization, smart-city projects, and transit integration further boost demand, complemented by expanding financial inclusion and digital payments, such as India’s UPI, achieving 83.7% of digital transaction volume in FY2024-25.

The Middle East & Africa smart cards market is projected to grow at a high CAGR, driven by government-led initiatives in secure identity and e-ID programs. In South Africa, the Department of Home Affairs issued 2.82 million Smart IDs in FY 2023/24, up 7% from the previous year, with applications now open for naturalized citizens and permanent residents, while phasing out older ID formats.

GCC nations are rolling out national e-ID and e-passport programs, supporting large-scale government procurement cycles. Modernization efforts, including system-on-chip and microcontroller cards, are fueling demand for smart card issuance infrastructure, readers, and lifecycle services. The UAE’s national identity smart card ecosystem processed over 34 million smart transactions in 2024, reflecting a 59% growth from 2023, according to the Ministry of Human Resources & Emiratisation.

The global smart cards market is moderately consolidated, led by major players such as Thales, IDEMIA, and Giesecke+Devrient, alongside agile regional competitors. These manufacturers leverage vertically integrated operations, from chip design to personalization, ensuring high security and innovative solutions. They maintain a competitive edge through continuous R&D, strategic partnerships, and mergers & acquisitions, expanding both technological capabilities and global market presence. This dynamic approach drives innovation and strengthens their position in the industry.

The smart cards market is projected to be valued at US$16.2 Billion in 2025.

Rising digitalization, cybercrime, and regulatory compliance are the key drivers of the smart cards market.

The smart cards market is poised to witness a CAGR of 6.5% from 2025 to 2032.

E-governance initiatives, contactless transactions, and the expansion of IoT and 5G networks are creating strong growth opportunities.

Thales Group, IDEMIA, Giesecke + Devrient, and HID Global Corporation are among the leading key players.

| Report Attribute | Details |

|---|---|

|

Historical Data/Actuals |

2019 - 2024 |

|

Forecast Period |

2025 - 2032 |

|

Market Analysis |

Value: US$ Bn |

|

Geographical Coverage |

|

|

Segmental Coverage |

|

|

Competitive Analysis |

|

|

Report Highlights |

|

By Chip

By Interface

By Application

By End-user

By Region

Delivery Timelines

For more information on this report and its delivery timelines please get in touch with our sales team.

About Author