- Executive Summary

- Global Methyl Methacrylate Market Snapshot 2024 and 2032

- Market Opportunity Assessment, 2024-2032, US$ Bn

- Key Market Trends

- Industry Developments and Key Market Events

- Demand Side and Supply Side Analysis

- PMR Analysis and Recommendations

- Market Overview

- Market Scope and Definitions

- Value Chain Analysis

- Macro-Economic Factors

- Global GDP Outlook

- Global Automotive Sales by Region

- Global Automotive Sales by Vehicle Type

- Forecast Factors – Relevance and Impact

- COVID-19 Impact Assessment

- PESTLE Analysis

- Porter's Five Forces Analysis

- Geopolitical Tensions: Market Impact

- Regulatory and Technology Landscape

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Trends

- Price Trend Analysis, 2019 – 2032

- Region-wise Price Analysis

- Price by Segments

- Price Impact Factors

- Global Methyl Methacrylate Market Outlook:

- Key Highlights

- Global Methyl Methacrylate Market Outlook: Application

- Introduction/Key Findings

- Historical Market Size (US$ Bn) and Volume (Tons) Analysis by Application, 2019-2023

- Current Market Size (US$ Bn) and Volume (Tons) Analysis and Forecast, by Application, 2024-2032

- Polymethyl Methacrylate (PMMA)

- Surface Coatings

- Emulsion Polymers

- Adhesives and Sealants

- Plastic Additives

- Paints and Inks

- Others

- Market Attractiveness Analysis: Application

- Global Methyl Methacrylate Market Outlook: End-Use Industry

- Introduction/Key Findings

- Historical Market Size (US$ Bn) and Volume (Tons) Analysis by End-Use Industry, 2019-2023

- Current Market Size (US$ Bn) and Volume (Tons) Analysis and Forecast, by End-Use Industry, 2024-2032

- Automotive

- Building & Construction

- Electronics

- Signs & Displays

- Medical

- Paints & Coatings

- Consumer Goods

- Others

- Market Attractiveness Analysis: End-Use Industry

- Global Methyl Methacrylate Market Outlook: Region

- Key Highlights

- Historical Market Size (US$ Bn) and Volume (Tons) Analysis by Region, 2019-2023

- Current Market Size (US$ Bn) and Volume (Tons) Analysis and Forecast, by Region, 2024-2032

- North America

- Europe

- East Asia

- South Asia & Oceania

- Latin America

- Middle East & Africa

- Market Attractiveness Analysis: Region

- North America Methyl Methacrylate Market Outlook:

- Key Highlights

- Pricing Analysis

- North America Market Size (US$ Bn) and Volume (Tons) Analysis and Forecast, by Country, 2024-2032

- U.S.

- Canada

- North America Market Size (US$ Bn) and Volume (Tons) Analysis and Forecast, by Application, 2024-2032

- Polymethyl Methacrylate (PMMA)

- Surface Coatings

- Emulsion Polymers

- Adhesives and Sealants

- Plastic Additives

- Paints and Inks

- Others

- North America Market Size (US$ Bn) and Volume (Tons) Analysis and Forecast, by End-Use Industry, 2024-2032

- Automotive

- Building & Construction

- Electronics

- Signs & Displays

- Medical

- Paints & Coatings

- Consumer Goods

- Others

- Europe Methyl Methacrylate Market Outlook:

- Key Highlights

- Pricing Analysis

- Europe Market Size (US$ Bn) and Volume (Tons) Analysis and Forecast, by Country, 2024-2032

- Germany

- Italy

- France

- U.K.

- Spain

- Russia

- Rest of Europe

- Europe Market Size (US$ Bn) and Volume (Tons) Analysis and Forecast, by Application, 2024-2032

- Polymethyl Methacrylate (PMMA)

- Surface Coatings

- Emulsion Polymers

- Adhesives and Sealants

- Plastic Additives

- Paints and Inks

- Others

- Europe Market Size (US$ Bn) and Volume (Tons) Analysis and Forecast, by End-Use Industry, 2024-2032

- Automotive

- Building & Construction

- Electronics

- Signs & Displays

- Medical

- Paints & Coatings

- Consumer Goods

- Others

- East Asia Methyl Methacrylate Market Outlook:

- Key Highlights

- Pricing Analysis

- East Asia Market Size (US$ Bn) and Volume (Tons) Analysis and Forecast, by Country, 2024-2032

- China

- Japan

- South Korea

- East Asia Market Size (US$ Bn) and Volume (Tons) Analysis and Forecast, by Application, 2024-2032

- Polymethyl Methacrylate (PMMA)

- Surface Coatings

- Emulsion Polymers

- Adhesives and Sealants

- Plastic Additives

- Paints and Inks

- Others

- East Asia Market Size (US$ Bn) and Volume (Tons) Analysis and Forecast, by End-Use Industry, 2024-2032

- Automotive

- Building & Construction

- Electronics

- Signs & Displays

- Medical

- Paints & Coatings

- Consumer Goods

- Others

- East Asia Market Size (US$ Bn) and Volume (Tons) Analysis and Forecast, by , 2024-2032

- South Asia & Oceania Methyl Methacrylate Market Outlook:

- Key Highlights

- Pricing Analysis

- South Asia & Oceania Market Size (US$ Bn) and Volume (Tons) Analysis and Forecast, by Country, 2024-2032

- India

- Southeast Asia

- ANZ

- Rest of SAO

- South Asia & Oceania Market Size (US$ Bn) and Volume (Tons) Analysis and Forecast, by Application, 2024-2032

- Polymethyl Methacrylate (PMMA)

- Surface Coatings

- Emulsion Polymers

- Adhesives and Sealants

- Plastic Additives

- Paints and Inks

- Others

- South Asia & Oceania Market Size (US$ Bn) and Volume (Tons) Analysis and Forecast, by End-Use Industry, 2024-2032

- Automotive

- Building & Construction

- Electronics

- Signs & Displays

- Medical

- Paints & Coatings

- Consumer Goods

- Others

- Latin America Methyl Methacrylate Market Outlook:

- Key Highlights

- Pricing Analysis

- Latin America Market Size (US$ Bn) and Volume (Tons) Analysis and Forecast, by Country, 2024-2032

- Brazil

- Mexico

- Rest of LATAM

- Latin America Market Size (US$ Bn) and Volume (Tons) Analysis and Forecast, by Application, 2024-2032

- Polymethyl Methacrylate (PMMA)

- Surface Coatings

- Emulsion Polymers

- Adhesives and Sealants

- Plastic Additives

- Paints and Inks

- Others

- Latin America Market Size (US$ Bn) and Volume (Tons) Analysis and Forecast, by End-Use Industry, 2024-2032

- Automotive

- Building & Construction

- Electronics

- Signs & Displays

- Medical

- Paints & Coatings

- Consumer Goods

- Others

- Middle East & Africa Methyl Methacrylate Market Outlook:

- Key Highlights

- Pricing Analysis

- Middle East & Africa Market Size (US$ Bn) and Volume (Tons) Analysis and Forecast, by Country, 2024-2032

- GCC Countries

- South Africa

- Northern Africa

- Rest of MEA

- Middle East & Africa Market Size (US$ Bn) and Volume (Tons) Analysis and Forecast, by Application, 2024-2032

- Polymethyl Methacrylate (PMMA)

- Surface Coatings

- Emulsion Polymers

- Adhesives and Sealants

- Plastic Additives

- Paints and Inks

- Others

- Middle East & Africa Market Size (US$ Bn) and Volume (Tons) Analysis and Forecast, by End-Use Industry, 2024-2032

- Automotive

- Building & Construction

- Electronics

- Signs & Displays

- Medical

- Paints & Coatings

- Consumer Goods

- Others

- Competition Landscape

- Market Share Analysis, 2024

- Market Structure

- Competition Intensity Mapping

- Competition Dashboard

- Company Profiles

- DowDuPont Inc.,

- Company Overview

- Product Portfolio/Offerings

- Key Financials

- SWOT Analysis

- Company Strategy and Key Developments

- BASF SE,

- Mitsubishi Chemical Holding Corporation,

- Arkema,

- Evonik industries AG,

- S.K. Panchal and Co.,

- LG Chem,

- Monómeros del Vallés S.L.,

- NIPPON SHOKUBAI CO., LTD.,

- Sumitomo Corporation,

- Shanghai Huayi Group Corp. Ltd.,

- Heilongjiang Zhongmeng Longxin Chemical Co., Ltd.

- Kowa India Pvt. Ltd.

- DowDuPont Inc.,

- Appendix

- Research Methodology

- Research Assumptions

- Acronyms and Abbreviations

- Specialty & Fine Chemicals

- Methyl Methacrylate Market

Methyl Methacrylate Market Size, Share, Growth, and Regional Forecast for 2025 - 2032

Methyl Methacrylate Market By Application (Polymethyl Methacrylate (PMMA), Surface Coatings, Emulsion Polymers, Adhesives and Sealants, Plastic Additives, Paints and Inks, Others), By End-Use Industry, and Regional Analysis for 2025 - 2032

Methyl Methacrylate Market Share and Trends Analysis

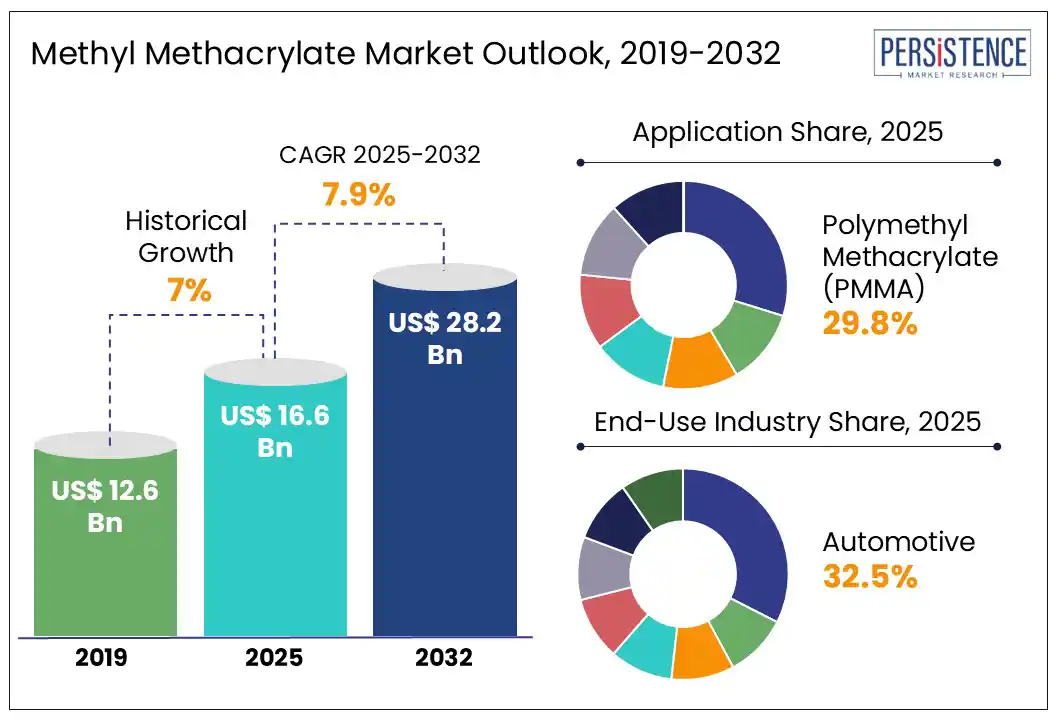

The global methyl methacrylate market size is likely to be value at US$ 16.6 billion in 2025 and is expected to reach US$ 28.2 billion by 2032, representing a CAGR of 7.9% during the forecast period from 2025 to 2032.

The methyl methacrylate (MMA) market growth is propelled by its wide-ranging applications across multiple industries such as automotive, construction, electronics, and medical devices. MMA is highly valued for its exceptional clarity, durability, and lightweight characteristics, which make it an essential raw material in the production of polymethyl methacrylate (PMMA) and other related polymers. Furthermore, accelerating industrialization and the growing emphasis on sustainable and eco-friendly materials are key factors shaping the market’s growth and dynamics on a global scale.

Key Industry Highlights:

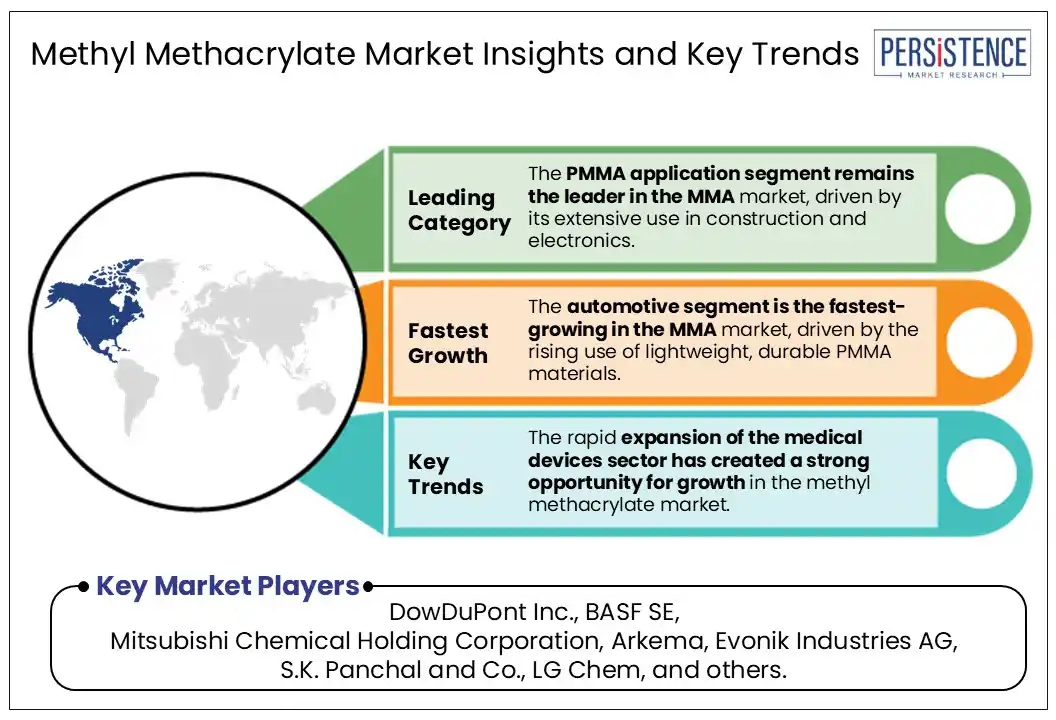

- Polymethyl Methacrylate is the leading application segment, primarily due to its widespread use in the construction and electronics industries.

- The automotive sector is the fastest-growing end-use market, fueled by the use of methyl methacrylate in lightweight exterior panels and lighting components.

- Rapid infrastructure development and electronics manufacturing in the Asia Pacific region are driving an increase in the consumption.

- Innovations in adhesives and sealants that utilize MMA are enhancing performance across various industries.

- The advanced manufacturing of medical devices is creating new applications for MMA-based polymers.

- Increasing regulations on volatile organic compound (VOC) emissions are prompting the development of environmentally friendly MMA formulations.

- The expansion of electronics and display technologies is further fueling the demand for high-quality MMA derivatives.

|

Global Market Attribute |

Key Insights |

|

Methyl methacrylate Market Size (2025E) |

US$ 16.6 Bn |

|

Market Value Forecast (2032F) |

US$ 28.2 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

7.9% |

|

Historical Market Growth (CAGR 2019 to 2024) |

7.0% |

Market Dynamics

Driver - Rising Demand for PMMA-Based Lightweight Automotive Components is Significantly Fueling Global MMA Consumption

Global demand for methyl methacrylate is being strongly driven by the growing use of PMMA-based lightweight components in the automotive industry. As stricter emission regulations and fuel efficiency standards take hold, manufacturers are increasingly turning to PMMA as a lighter, high-performance alternative to traditional glass and metal. Its impact resistance, clarity, and reduced weight make it ideal for applications such as light covers, exterior panels, and interior trims. This shift is not only about performance but reflects evolving design trends and sustainability goals.

In 2023, the collaboration between Mitsubishi Chemical Group and Honda Motor Co., Ltd. resulted in the creation of a new PMMA material specifically designed for automotive body parts. The innovative resin, enhanced with rubber particles, eliminates the need for painting by using colorants for a glossy finish, thereby reducing CO? emissions and supporting recyclability, offering a clear step toward more sustainable vehicle manufacturing.

Restraints - Stringent environmental regulations surrounding MMA emissions restrainproduction expansion globally

The adoption of methyl methacrylate as a sustainable material has been significantly limited by the complexities associated with its disposal and recycling. As MMA-based products, particularly polymethyl methacrylate, are widely used in applications requiring durability and transparency, their end-of-life management has posed substantial environmental challenges. PMMA waste is often not accepted in standard municipal recycling streams, and specialized depolymerization techniques must be employed to recover monomers, which require high energy input and controlled conditions.

The presence of additives, dyes, and other polymers in finished products complicates the purity and yield of recycled MMA. These technical constraints have resulted in limited infrastructure investment for its recycling. As a result, the material’s circularity is reduced, and its broader sustainability appeal has been adversely affected across industries prioritizing green alternatives.

Opportunity - Growing focus on Recycling and Reclaiming MMA Creates Sustainability-Driven Growth Opportunities for Market Players

In 2025, the rapid expansion of the medical devices sector has created a strong opportunity for methyl methacrylate market growth. MMA-based polymers, especially polymethyl methacrylate are increasingly used in medical applications due to their optical clarity, biocompatibility, and ease of sterilization. These materials are commonly found in intraocular lenses, bone cement, dentures, and diagnostic devices, meeting the growing demand for lightweight, durable, and transparent solutions in healthcare.

Arkema’s introduction of its Advanced Bio-Circular (ABC) polyamide 11 medical polymer. Designed to replace metals and conventional plastics in high-performance medical uses, it offers excellent biocompatibility, chemical resistance, and sterilization durability. Made from renewable castor oil and containing over 98% bio-based carbon, this recyclable polymer supports both performance and sustainability, reducing climate impact by up to 50% compared to fossil-based options and promoting circularity in healthcare.

Category Wise Insights

Application Insights

In 2025, the polymethyl methacrylate application segment is leading driven by its widespread use across industries such as construction and electronics. Valued for its strength, UV resistance, and aesthetic flexibility, PMMA has been widely adopted in building components like windows, skylights, and signage. In electronics, its optical clarity and insulating properties have supported its use in display screens, light guides, and protective casings. The material's ease of molding, coloring, and fabrication has further encouraged its preference over traditional alternatives.

Evonik Industries has significantly contributed to the growth of this segment through targeted innovations. Their new multi-layer coextrusion plant in Weiterstadt, Germany, has begun producing the world’s widest PMMA flat sheets, designed specifically for architectural and industrial applications. Meanwhile, the Shanghai MATCH facility continues to supply PLEXIGLAS® molding compounds for LED screens, reinforcing PMMA’s value in electronics. These developments reflect the segment’s durability and expanding industrial relevance.

End-Use Industry Insights

In 2025, the automotive segment is a fast-growing sector, owing to the increased adoption of MMA-based lightweight and durable materials, including polymethyl methacrylate. It is extensively used in headlamp lenses, taillights, and exterior automobile panels due to its optical PMMA's clarity, impact strength, and weather resistance. As fuel efficiency and vehicle weight become critical, automakers tend to shift towards using MMA-based materials, that amplifies the demand based on these factors. The growth is aided by stricter regulations to control emissions and improve vehicle performance.

Evonik Industries have invested in the PMMA production, launching a cutting-edge multi-layer coextrusion plant in Weiterstadt, Germany, in 2025. The facility produces high-performance PMMA flat films. These steps further address the growing demand for materials based on MMA in the automotive industry and other sectors.

Regional Insights and Trends

North America Methyl Methacrylate Market Trends

In North America, rising demand for low-VOC industrial coatings has played a pivotal role in driving the consumption of methyl methacrylate, particularly due to increasing environmental regulations fare focused on improving air quality and reducing emissions. MMA-based resins have been widely adopted in coating formulations for automotive, construction, and machinery manufacturing sectors, thanks to their fast-drying nature, chemical resistance, and superior durability. This growing preference reflects a broader shift toward sustainable manufacturing practices and regulatory compliance.

In 2025, BASF Coatings expanded its biomass-balanced product line into North America, introducing about 250 eco-friendly products, including automotive OEM and refinish coatings, under the brands ReSource, Glasurit Eco Balance, and R-M eSense. These formulations contributed to a reduction of nearly 8 million kilograms (17.6 million pounds) of CO? emissions in 2024 alone. This initiative underscores BASF’s commitment to supporting the circular economy and meeting the region's increasing demand for environmentally responsible coatings.

Europe Methyl Methacrylate Market Trends

In Europe, a strong shift toward sustainable materials fuels growing interest in bio-based and recycled sources of methyl methacrylate. This movement has been largely driven by strict environmental regulations and rising consumer awareness surrounding carbon footprints. In response, industries such as automotive, construction, and packaging have accelerated their adoption of environmentally friendly materials to align with circular economy goals. The reliance on fossil fuels is being steadily reduced through innovations in bio-derived MMA and advanced recycling technologies.

In 2025, BASF is transitioning its entire Ethyl Acrylate portfolio to bio-based sources, using European grain-derived bioethanol that does not compete with food production. This new EA offers a 30% lower product carbon footprint compared to fossil-based alternatives and is offered as a drop-in solution for coatings and adhesives. Additionally, BASF introduced an ISCC PLUS-certified biomass-balanced version, demonstrating its commitment to sustainable production and supporting Europe’s drive toward greener manufacturing.

Asia Pacific Methyl Methacrylate Market Trends

In the Asia Pacific region, rapid infrastructure growth and the expansion of electronics manufacturing have been recognized as key drivers of increased methyl methacrylate consumption. Urbanization and large-scale construction projects have elevated the demand for durable, lightweight materials such as polymethyl methacrylate, a major MMA derivative. Simultaneously, the electronics sector has increasingly relied on MMA-based components for their clarity and resilience in applications like displays, lenses, and protective coatings. These trends have been further supported by government-led initiatives aimed at modernization and technological advancement across leading regional economies.

In 2025, LG Chem played a pivotal role in reinforcing this momentum by partnering with HL Mando, a prominent Korean automotive parts manufacturer, to co-develop adhesives tailored for electronic components in vehicles. These innovations, designed to improve the safety and performance of advanced driver assistance systems, include thermal gap fillers and insulating adhesives advancements expected to expand MMA usage in automotive electronics across the region.

Competitive Landscape

The global methyl methacrylate market is characterized by intense competition among key industry players who focus on innovation, capacity expansion, and sustainability initiatives to strengthen their market positions. Leading manufacturers invest heavily in research and development to produce high-performance MMA and PMMA products tailored for diverse applications like automotive, construction, and electronics. Strategic collaborations and partnerships are common, enabling companies to enhance product portfolios and enter new geographic markets.

Several players prioritize sustainability by developing bio-based MMA and adopting environmentally friendly manufacturing processes, responding to growing regulatory pressures and consumer demand for green products. Capacity expansions, particularly in Asia Pacific, are pursued to meet rising regional demand driven by rapid industrialization. Smaller regional players compete on cost-effectiveness and niche applications, adding further dynamism to the competitive landscape.

Key Industry Developments

- In August 2024, BASF will transition its entire Ethyl Acrylate portfolio to bio-based sources starting in Q4 2024. This change, part of its sustainability commitment, will reduce the Product Carbon Footprint by 30% compared to fossil-based EA. The bio-based EA will be made from bioethanol sourced from European grains and residues, ensuring it does not compete with food production. This initiative meets the increasing demand for sustainable materials in coatings and adhesives.

- In December 2024, LG Chem has built a pyrolysis oil plant in Dangjin, South Korea, with a capacity of 20,000 tons per year. The facility processes waste plastics, including marine waste and vinyl, to create pyrolysis oil for recycled plastic materials. This initiative underscores LG Chem's commitment to sustainability and the circular economy, aiming to reduce carbon emissions and promote resource circulation.

Companies Covered in Methyl Methacrylate Market

- DowDuPont Inc.,

- BASF SE,

- Mitsubishi Chemical Holding Corporation,

- Arkema,

- Evonik industries AG,

- S.K. Panchal and Co.,

- LG Chem,

- Monómeros del Vallés S.L.,

- NIPPON SHOKUBAI CO., LTD.,

- Sumitomo Corporation,

- Shanghai Huayi Group Corp. Ltd.,

- Heilongjiang Zhongmeng Longxin Chemical Co., Ltd.

- Kowa India Pvt. Ltd.

Frequently Asked Questions

The global Methyl methacrylate market is projected to be valued at 16.6 Bn in 2025.

The Methyl methacrylate market is driven by rising demand for PMMA-based lightweight automotive components is significantly fueling global MMA consumption.

The Methyl methacrylate market is poised to witness a CAGR of 7.9% from 2025 to 2032.

Growing focus on recycling and reclaiming MMA creates sustainability-driven growth opportunities for market players is the key market opportunity.

Major players in the Methyl methacrylate market include DowDuPont Inc., BASF SE, Mitsubishi Chemical Holding Corporation, Arkema, LG Chem, and others.