- Communication Infrastructure & Services

- Managed VPN Market

Managed VPN Market Size, Share, and Growth Forecast 2026 - 2033

Managed VPN Market by VPN Type (Remote Access VPN, Site-to-Site VPN, VPN-as-a-Service, Mobile VPN), by Distribution Channel (Managed Service Providers, Telecom Operators, Cloud Service Providers, Others), End-users (BFSI, Healthcare, IT and ITES, Energy and Power, Media and Entertainment, Transportation and Logistics, Manufacturing, Others), by Regional Analysis, 2026 - 2033

Managed VPN Market Size and Trend Analysis

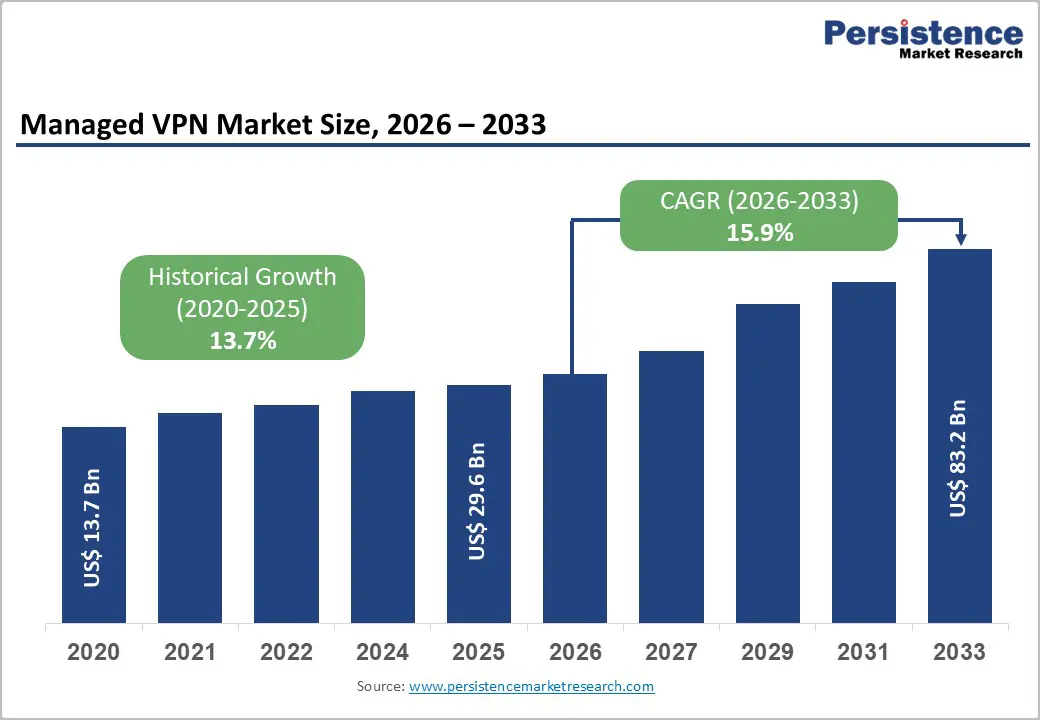

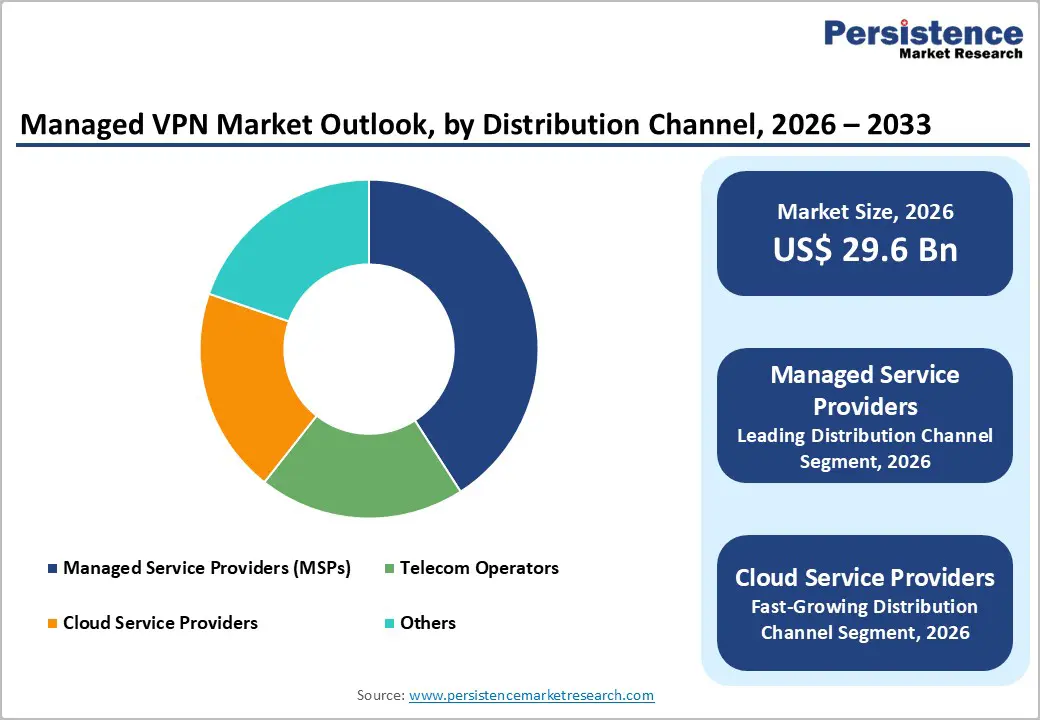

The global managed VPN market size is expected to be valued at US$ 29.6 billion in 2026 and projected to reach US$ 83.2 billion by 2033, growing at a CAGR of 15.9% between 2026 and 2033.

The market growth is driven by the persistent shift toward hybrid and remote work models, which have become a permanent feature in enterprise operations. Organizations are increasingly prioritizing secure network connectivity to protect distributed workforces accessing critical business applications from multiple locations. Additionally, the rising sophistication of cyber threats and stringent regulatory compliance requirements around data protection are compelling enterprises to adopt managed VPN solutions that provide enterprise-grade security without requiring significant capital expenditure.

Key Industry Highlights:

- Leading Region: North America leads the managed VPN market with about 38% share due to strong enterprise cloud adoption, strict compliance requirements, and the presence of major vendors.

- Fastest Growing Region: Asia Pacific is the fastest-growing region with an expected 20% CAGR through 2033, driven by rapid digitalization and the expansion of over 1.6 billion mobile internet users.

- Dominant Segment: Site-to-Site VPN is the dominant VPN type with 49% share in 2025 as global enterprises prioritize secure, continuous inter-office connectivity.

- Fastest Growing Segment: Cloud Service Providers form the fastest-growing distribution channel with an estimated 18% CAGR as organizations shift workloads to cloud platforms and require hybrid connectivity.

- Key Market Opportunity: SASE integration and Zero Trust adoption present the biggest opportunity, with 65% of SD-WAN purchases expected to include SASE bundles by 2027.

| Key Insights | Details |

|---|---|

| Managed VPN Market Size (2026E) | US$ 29.6 billion |

| Market Value Forecast (2033F) | US$ 83.2 billion |

| Projected Growth CAGR (2026 - 2033) | 15.9% |

| Historical Market Growth (2020 - 2025) | 13.7% |

Market Dynamics

Drivers - Accelerating Adoption of Remote and Hybrid Work Models

The global workforce has undergone a fundamental transformation, with approximately 72% of organizations planning to make remote or hybrid work permanent for at least a portion of their workforce. This structural shift in work arrangements has created unprecedented demand for managed VPN solutions that enable secure access to corporate resources from distributed locations. According to workplace analytics research, 73% of companies now rely on VPN connections to secure remote access to company applications and tools, making managed VPN services essential infrastructure.

The shift is particularly pronounced in the technology and financial services sectors where highly skilled talent expects flexible work arrangements. Managed VPN service providers are capitalizing on this trend by offering scalable, subscription-based solutions that eliminate the need for enterprises to maintain expensive on-premises VPN infrastructure, thereby reducing the total cost of ownership while ensuring a consistent security posture across the organization.

Integration with Zero Trust Network Access and SASE Convergence

The technology landscape is undergoing significant consolidation with Secure Access Service Edge (SASE) platforms increasingly bundling managed VPN capabilities with Zero Trust Network Access (ZTNA) frameworks. Industry analysts project that 65% of SD-WAN purchases between now and 2027 will be bundled with SASE offerings, compared with only 20% in 2024, representing a monumental shift in enterprise security architecture. This convergence is driving managed VPN market growth as organizations recognize that traditional perimeter-based security models are obsolete in cloud-native environments.

Major technology vendors, including Palo Alto Networks and Cisco Systems, have announced advanced SASE platforms that integrate managed VPN connectivity with identity-driven access controls, enabling enterprises to transition from implicit trust models to granular, application-specific access policies. The convergence reduces operational complexity by consolidating multiple security point solutions into unified platforms, which appeals particularly to organizations with limited IT resources.

Restraints

Skill Gaps and Operational Complexity in Deployment

Despite the apparent advantages of managed VPN solutions, enterprises face significant challenges in implementing and managing sophisticated security frameworks. The cybersecurity industry is experiencing critical talent shortages, with numerous organizations reporting difficulty in recruiting and retaining qualified network security professionals. This skills deficit extends beyond traditional VPN management to encompass emerging technologies such as ZTNA and SD-WAN integration, creating bottlenecks in deployment timelines.

Moreover, the transition from legacy VPN architectures to modern managed solutions requires careful planning, testing, and staff training, which many mid-market organizations struggle to execute effectively. Organizations with limited IT teams often postpone migration to managed VPN platforms due to concerns about operational disruption and the perceived complexity of configuration management in hybrid network environments.

Regulatory and Privacy Compliance Constraints

The regulatory landscape surrounding VPN services and data management has become increasingly complex, with governments worldwide implementing stricter data residency and privacy requirements. Notable examples include India’s CERT-In directive from 2022, which mandates that VPN providers store user data for five years, leading major international VPN providers such as ExpressVPN and NordVPN to remove physical servers from the country to maintain privacy commitments. These conflicting mandates between national security authorities and global privacy standards create significant compliance burdens for managed VPN service providers operating internationally.

Additionally, regulations such as GDPR in Europe and industry-specific compliance frameworks in healthcare and finance impose stringent requirements on data handling, encryption protocols, and audit logging, increasing operational costs for managed VPN providers and potentially limiting service availability in certain geographies.

Opportunity - Expansion into Small and Medium-Sized Enterprises with Managed Services

The democratization of enterprise-grade network security has opened substantial opportunities in the SME segment, which historically lacked access to sophisticated VPN infrastructure due to cost and complexity barriers. Research indicates that small and medium-sized enterprises represent the fastest-growing segment within the broader managed network services market, with adoption accelerating at a significantly higher CAGR compared to large enterprises.

Managed VPN service providers are capturing this opportunity through subscription-based pricing models and simplified onboarding processes that eliminate upfront capital expenditure requirements. The shift toward Network-as-a-Service (NaaS) models enables SMEs to access enterprise-grade security controls without maintaining dedicated IT infrastructure, fundamentally altering the competitive dynamics of the market. Industry observations show that over 35% of WAN users are planning to implement VPN solutions in the coming years, indicating substantial runway for market expansion as traditional network architectures transition to managed cloud-native models.

Growth of Artificial Intelligence and Machine Learning in Managed VPN Platforms

The integration of artificial intelligence and machine learning capabilities into managed VPN platforms represents a significant market opportunity as vendors differentiate offerings through advanced threat detection, predictive analytics, and automated remediation. Leading vendors such as Palo Alto Networks have demonstrated the commercial viability of AI-driven security with their Prisma SASE 4.0 platform, which recently achieved 35% year-over-year SASE revenue growth, exceeding overall market growth rates by more than double. These AI-powered platforms enable real-time identification of sophisticated threats that traditional VPN architectures fail to detect, including encrypted malware assembly within browsers and zero-day exploits.

The competitive advantage associated with AI-enhanced managed VPN solutions is attracting substantial investment and customer adoption, particularly among enterprises handling sensitive financial data or confidential intellectual property. As vendors develop increasingly sophisticated AI capabilities for managed VPN platforms, enterprises are expected to accelerate spending on advanced solutions, driving premium pricing power and margin expansion across the market.

Category-wise Analysis

VPN Type Insights

Site-to-Site VPN remains the backbone of enterprise connectivity, holding around 49% of the managed VPN market in 2025. Its dominance reflects the need for secure, always-on, encrypted tunnels between headquarters, data centers, branch offices, and international sites. Since these VPNs provide deterministic connectivity at the network layer without requiring authentication for each device, they reduce administrative overhead and support consistent access to shared corporate resources. This makes Site-to-Site VPNs essential for organizations with complex network topologies and centralized workloads, and the segment is expected to retain nearly half of the overall market over the next several years.

Distribution Channel Insights

Managed Service Providers lead the distribution of managed VPN services with roughly 38% market share in 2025, reflecting their importance in delivering end-to-end connectivity and security solutions for enterprises that lack in-house networking expertise. MSPs provide bundled services that include VPN management, monitoring, incident response, compliance reporting, and ongoing maintenance, which simplifies vendor coordination and reduces operational burden. Their long-term customer relationships, service-level agreements, and 24/7 support capabilities make them the preferred channel for global enterprises and mid-market organizations seeking reliable managed VPN operations without internal IT overhead.

End-user Insights

The IT and ITES sector accounts for approximately 28% of managed VPN adoption in 2025, making it the largest end-user category. Companies in this sector typically operate globally distributed development teams, remote support centers, and offshore delivery hubs that require secure, high-bandwidth access to internal systems and client platforms. Managed VPNs help maintain data confidentiality, support remote collaboration, and enforce consistent access control across multiple geographies. As digital service delivery and outsourcing models expand further, IT and ITES organizations will continue to drive a significant share of demand in the managed VPN market.

Regional Insights

North America Managed VPN Market Trends and Insights

North America maintains the dominant regional position within the global managed VPN market, accounting for approximately 38% of global market share in 2025. The region’s leadership is driven by the United States’ position as the technological innovation hub, with enterprises investing heavily in advanced security infrastructure to protect valuable intellectual property and customer data. North American enterprises demonstrate the highest willingness to adopt managed VPN solutions as part of comprehensive security modernization programs, supported by mature IT spending budgets and established vendor relationships with leading providers such as Cisco Systems, AT&T Inc., and Verizon Communications.

The regulatory environment in North America, including requirements under HIPAA for healthcare organizations and PCI-DSS for financial institutions, establishes baseline security standards that drive managed VPN adoption across regulated industries. Additionally, approximately 42% of North American internet users actively employ VPN services, indicating a culture of network security consciousness that extends from consumers to enterprise decision-makers. The region’s managed VPN market benefits from sophisticated IT procurement processes, established managed service provider ecosystems, and significant cloud infrastructure deployment, driving demand for seamless hybrid connectivity solutions.

Europe Managed VPN Market Trends and Insights

Europe represents the second-largest regional market, demonstrating sustained growth driven by stringent data protection regulations and advanced technology adoption. The General Data Protection Regulation (GDPR) has fundamentally reshaped enterprise security priorities across European Union member states, requiring organizations to implement advanced encryption, access controls, and audit logging capabilities that managed VPN solutions provide natively. Major European technology hubs, including Germany, the United Kingdom, and France, are experiencing accelerated managed VPN adoption as enterprises prioritize data sovereignty and localized infrastructure.

Germany is expected to experience significant growth at an estimated 23% CAGR through 2033, driven by corporate compliance demands and widespread adoption of decentralized access policies across large industrial organizations. European enterprises demonstrate heightened concern regarding data residency requirements and encryption standards, driving preference for managed VPN providers offering European data center infrastructure and compliance certifications. The region benefits from established managed service provider networks and strong vendor presence from both North American and European technology companies, creating competitive market dynamics that drive innovation and service quality improvements.

Asia Pacific Managed VPN Market Trends and Insights

Asia Pacific emerges as the fastest-growing regional market, expected to expand at an estimated 20% CAGR through 2035, representing the most significant growth opportunity within the global managed VPN landscape. The region encompasses rapidly expanding digital economies in China, India, Japan, and Southeast Asian nations, where enterprises are accelerating cloud migration, remote work adoption, and digital transformation initiatives at unprecedented rates. India specifically is forecast to rise at a 25% CAGR through 2035, driven by massive demand for secured digital connectivity across rapidly growing small business and educational technology sectors.

The Asia Pacific region is experiencing extraordinary mobile internet proliferation, with over 1.6 billion unique mobile internet users, approximately half the global total, creating unprecedented demand for mobile VPN and cloud-based connectivity solutions. Leading Indian technology companies and Tata Communications Ltd. are substantially expanding managed VPN service offerings to capture growing demand from multinational enterprises establishing regional operations and domestic organizations undergoing digital transformation. The region benefits from cost-competitive service delivery models, substantial government investments in 5G infrastructure, and increasing regulatory focus on cybersecurity standards that drive managed VPN adoption across enterprise and government sectors.

Competitive Landscape

Market Structure Analysis

The global managed VPN market reflects a moderately concentrated structure shaped by strong competition between long-established network service providers and newer cloud-focused security platform vendors. The market is shifting from conventional managed connectivity toward integrated architectures that combine VPN, SD-WAN, SASE and advanced security functions. Major participants rely on extensive service delivery capabilities, long-term enterprise relationships and investment in automation and AI-based security enhancements to strengthen their position as the market becomes increasingly service driven. Competitive strategies emphasize platform unification, simplified management, and enterprise-wide security integration to address rising demand for consolidated networking and cybersecurity solutions.

The landscape continues to evolve through active consolidation as vendors seek broader portfolios and recurring revenue from fully managed security stacks. Cloud-native providers and zero-trust specialists are introducing service models that challenge traditional telecom-centric offerings. Market differentiation now centers on integrated platforms, proactive threat intelligence, automated policy control and high-quality managed service execution rather than basic encrypted connectivity.

Key Market Developments

- September 2025: Palo Alto Networks Launches Prisma SASE 4.0 with Integrated Prisma Browser - Palo Alto Networks introduced Prisma SASE 4.0 featuring AI-driven in-browser protection, supported by its SASE ARR reaching US$1.3 billion with 35% YoY growth.

- August 2023: Verizon and HCLTech announced a global collaboration for Managed Network Services supporting 5G, SD-WAN, and SASE deployments for enterprise customers, expanding Verizon’s next-generation networking capabilities.

- June 2025: Cisco and Palo Alto Networks Accelerate Single-Vendor SASE Adoption - Dell’Oro Group reported SASE revenue reaching US$2.6 billion in Q1 2025, up 17% YoY, driven largely by strong single-vendor platform growth.

Companies Covered in Managed VPN Market

- AT&T Inc.

- Cisco Systems, Inc.

- BT Group PLC

- CenturyLink, Inc.

- Vodafone Group Plc

- Verizon Communications Inc.

- Orange Business Services SAS

- Tata Communications Ltd.

- NTT Corporation

- Telefónica, S.A.

- Palo Alto Networks Inc.

- Microsoft Corporation (Azure)

- IBM Corporation

- Fortinet Inc.

- Juniper Networks Inc.

Frequently Asked Questions

The Managed VPN market is expected to reach around US$ 29.6 billion by 2026.

Key drivers include growing remote/hybrid work adoption, rising cyber threats, and increasing integration of VPN with SASE and Zero Trust architectures.

North America leads the market, holding about 38-40% share due to strong enterprise IT spending and regulatory compliance needs.

The largest opportunity lies in SASE platforms integrating managed VPN with Zero Trust Network Access.

Major players include AT&T, Verizon, Orange Business Services, Tata Communications, Cisco, Palo Alto Networks, and Fortinet.