- Healthcare Services

- Managed Equipment Service Market

Managed Equipment Service Market Size, Share, Trends, Growth, and Forecasts for 2025 - 2032

Managed Equipment Service Market by Service (Maintenance Services, Operational Services, Support Services, Managed Service Desk), Equipment (Medical Equipment, IT Equipment, Industrial Equipment, Laboratory Equipment), Service Provider Type (Original Equipment Manufacturer (OEM) Providers, Third-Party Providers, Independent Service Organizations (ISOs)), End-use, and Regional Analysis for 2025 - 2032

Managed Equipment Service Market Size and Trends Analysis

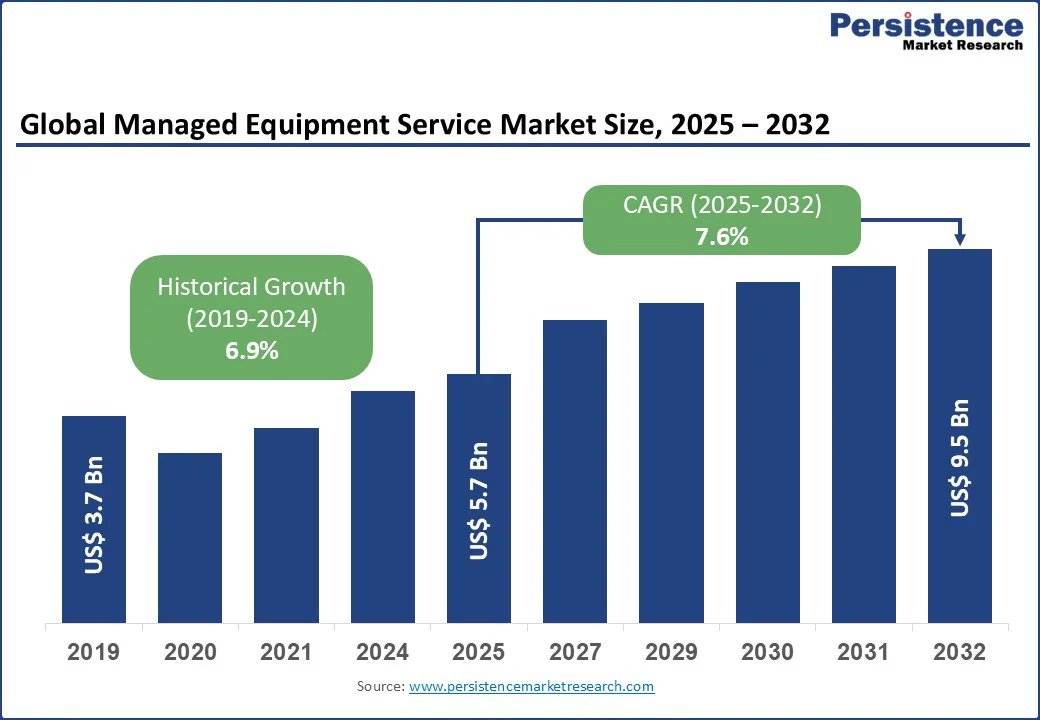

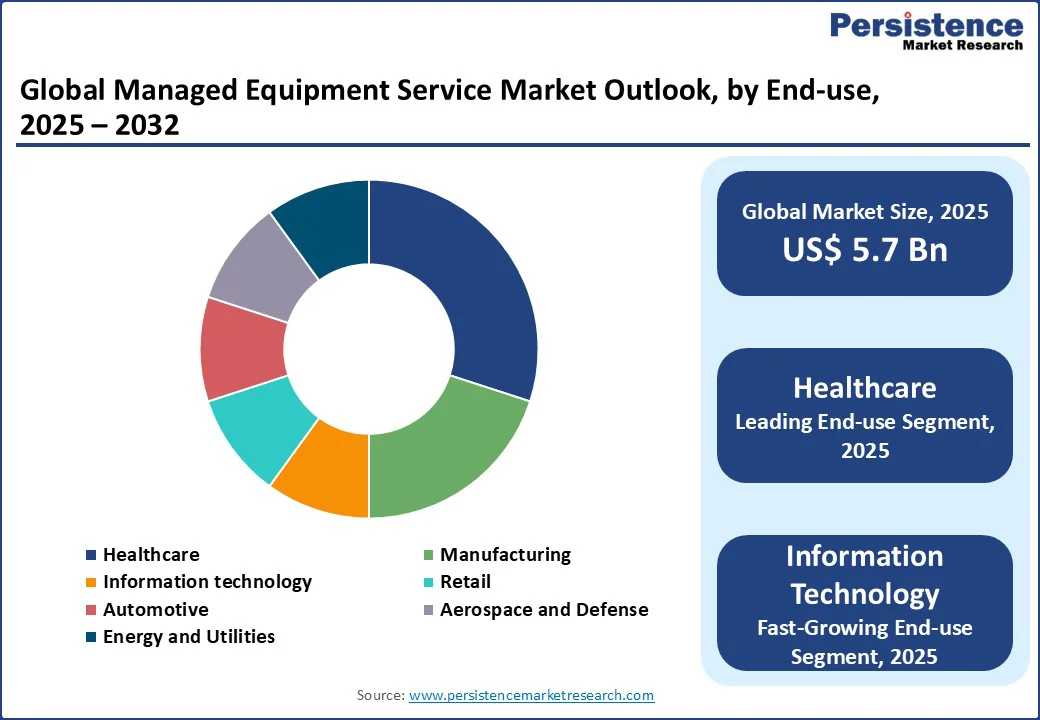

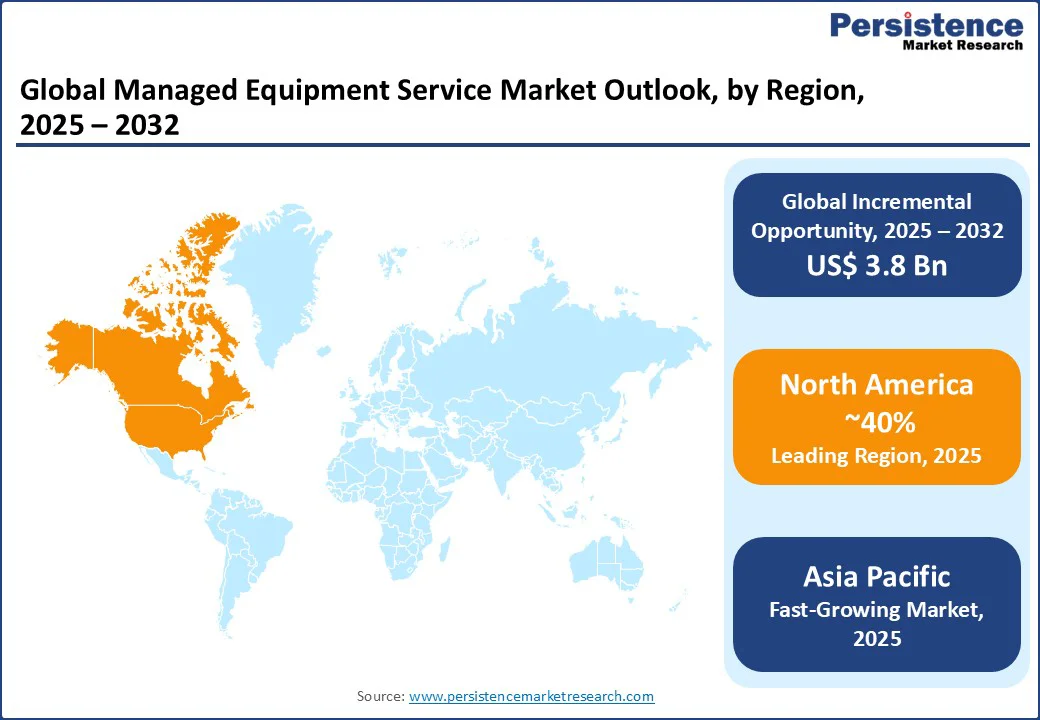

The global managed equipment service (MES) market size is likely to be valued at US$ 5.7 Bn in 2025, expected to grow at US$ 9.5 Bn by 2032, registering a CAGR of 7.6% during 2025-2032.

The increasing adoption of hospital equipment outsourcing and clinical asset management to optimize costs and enhance operational efficiency has encouraged the need for managed equipment service in the clinical sector. Governments are promoting PPP models for healthcare infrastructure development, boosting MES adoption in public hospitals.

Key Industry Highlights:

- Leading Service: Maintenance services hold a 40% market share in 2025, driven by medical device maintenance services.

- Fastest Growing Service: Managed Service Desk is fueled by hospital equipment management services.

- Equipment Dominates: Medical Equipment accounts for 45% market share, supported by diagnostic imaging equipment.

- Leading End-user: Healthcare holds a 50% market share, driven by hospital cost optimization strategies.

- Leading Service Provider Type: OEM Providers command a 40% market share, supported by healthcare service providers.

- Leading Region: North America holds a 40% market share, with the U.S. leading in healthcare infrastructure modernization.

|

Global Market Attribute |

Key Insights |

|

Managed Equipment Service Market Size (2025E) |

US$ 5.7 Bn |

|

Market Value Forecast (2032F) |

US$ 9.5 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

7.6% |

|

Historical Market Growth (CAGR 2019 to 2024) |

6.9% |

Market Dynamics

Driver: Rising Healthcare Investments and Technological Advancements

The managed equipment service market is propelled by increasing investments in healthcare infrastructure modernization, advancements in medical device maintenance services, and the growing need for hospital cost optimization strategies.

The global healthcare sector is increasingly focused on upgrading healthcare equipment, particularly diagnostic imaging equipment such as MRI, CT, and X-ray systems, to meet rising patient demands and improve clinical outcomes. This drives demand for hospitaervices that rely on managed medical equipment services to ensure equipment reliability and compliance with safety standards.

Technological advancements, including the integration of AI and IoT in clinical asset management, enable predictl sive maintenance, reducing equipment downtime and enhancing operational efficiency for hospital equipment management services. The shift toward equipment-as-a-service (EaaS) for hospitals allows healthcare facilities to outsource hospital equipment outsourcing, providing access to cutting-edge healthcare equipment without significant capital investments.

Restraint: High Service Costs and Skill Shortage

The Managed Equipment Service Market faces significant challenges due to the high costs of medical device maintenance services, a shortage of skilled professionals, and complex regulatory requirements. Maintaining sophisticated healthcare equipment, such as diagnostic imaging equipment, requires specialized expertise and advanced tools, leading to elevated service costs that can strain budgets, particularly for smaller healthcare facilities. This impacts the adoption of cost-saving with MES solutions, as some organizations struggle to justify the expense of hospital equipment outsourcing.

The shortage of trained biomedical engineers and technicians creates bottlenecks in delivering effective clinical asset management, particularly for complex systems such as MRI, CT, X-ray maintenance, limiting the scalability of managed medical equipment services. Regulatory frameworks, varying across regions, impose strict compliance standards for healthcare service providers, increasing operational complexity and costs for hospital equipment management services.

Opportunity: Growth in Predictive Maintenance and EaaS Models

The expansion of predictive maintenance technologies, growing healthcare infrastructure in emerging markets, and the rise of equipment-as-a-service (EaaS) for hospitals present significant opportunities for the Managed Equipment Service Market.

Predictive maintenance, powered by AI and IoT, enhances medical device maintenance services by anticipating equipment failures and optimizing maintenance schedules, improving efficiency for MES for diagnostic imaging equipment.

Emerging markets, particularly in the Asia Pacific and Latin America, are investing heavily in healthcare infrastructure modernization, creating opportunities for hospital services to adopt managed medical equipment services. These regions are expanding healthcare access, driving demand for hospital equipment outsourcing to support growing patient volumes.

The EaaS model offers flexible, subscription-based access to healthcare equipment, appealing to healthcare facilities seeking hospital cost optimization strategies without large upfront investments. These trends create opportunities for healthcare service providers to expand the MES market growth trends in healthcare infrastructure services and diagnostic imaging equipment maintenance.

Category-wise Analysis

Service Insights

Maintenance Services hold a 40% market share in 2025, driven by medical device maintenance services. They ensure optimal performance of diagnostic imaging equipment. Healthcare facilities rely heavily on advanced diagnostic imaging equipment such as MRI machines, CT scanners, and X-ray systems for accurate diagnosis and treatment planning.

Ensuring the optimal performance of these devices is critical for patient safety and operational efficiency. Maintenance services under MES contracts provide preventive and corrective maintenance, calibration, and compliance checks, minimizing downtime and extending equipment lifespan.

Managed Service Desk is fueled by hospital equipment management services. It supports real-time issue resolution. It enables quick troubleshooting, ticket management, and coordination with on-site technicians, ensuring minimal disruption to clinical workflows. This service improves response times, enhances user experience, and provides data insights for predictive maintenance.

Equipment Insights

Medical Equipment commands a 45% market share in 2025, driven by diagnostic imaging equipment. It supports hospital services, growing demand for diagnostic imaging equipment such as MRI machines, CT scanners, and X-ray systems.

These advanced devices are essential for accurate disease diagnosis and treatment planning, making them a critical component of hospital services. the high cost of acquisition and maintenance often creates financial challenges for healthcare providers.

IT Equipment is fueled by healthcare infrastructure modernization. It supports digital health systems. As hospitals transition toward smart healthcare ecosystems, IT equipment such as servers, networking devices, and digital platforms plays a pivotal role in supporting connected care. These systems enable seamless integration of electronic health records (EHR), telemedicine, and remote monitoring solutions, enhancing both clinical efficiency and patient engagement.

Service Provider Type Insights

OEM Providers hold a 40% market share in 2025, driven by healthcare service providers. They offer specialized medical device maintenance services. Their expertise guarantees compliance with regulatory standards and optimal performance of critical medical equipment such as MRI machines, CT scanners, and surgical instruments. OEMs often provide technology upgrades and training programs, giving healthcare providers confidence in quality and reliability.

Third-Party Providers are fueled by cost-saving with MES solutions. They offer flexibility. Their ability to service devices from different brands makes them attractive for hospitals looking to optimize budgets without compromising functionality. Furthermore, third-party MES providers often incorporate innovative technologies such as remote monitoring and predictive maintenance at competitive prices.

End-use Insights

Healthcare holds a 50% market share in 2025, driven by hospital cost optimization strategies. It relies on managed medical equipment services. These services enable hospitals to outsource the procurement, maintenance, and replacement of medical equipment, ensuring access to the latest technology without heavy upfront investments. MES enhances operational efficiency by minimizing equipment downtime and streamlining maintenance schedules.

Information Technology is fueled by healthcare infrastructure modernization. As hospitals undergo digital transformation, IT plays a vital role in integrating medical equipment with advanced healthcare systems, such as electronic health records (EHR) and hospital information systems (HIS). Managed IT services complement MES by enabling remote monitoring, predictive maintenance, and data-driven decision-making.

Regional Insights

North America Managed Equipment Service Market Trends

North America holds a 40% global market share in 2025, with the U.S. leading due to advanced healthcare infrastructure services and high demand for hospital equipment outsourcing. The U.S. market thrives on healthcare infrastructure modernization, with hospitals and clinics prioritizing hospital services to maintain diagnostic imaging equipment such as MRI, CT, and X-ray systems. The focus on improving patient outcomes and operational efficiency drives demand for managed medical equipment services, as healthcare facilities seek reliable medical device maintenance services to ensure equipment uptime.

The rise of chronic diseases and an aging population increases the need for clinical asset management, with MES for diagnostic imaging equipment playing a critical role in supporting diagnostic accuracy. Healthcare service providers such as GE Healthcare and Siemens Healthineers leverage equipment-as-a-service (EaaS) for hospitals to offer flexible solutions, aligning with hospital cost optimization strategies.

Europe Managed Equipment Service Market Trends

Europe accounts for a 30% global share, led by Germany, the UK, and France, driven by regulatory compliance and advanced healthcare equipment. Germany’s market benefits from a strong emphasis on compliance and quality in hospital services, with MES for diagnostic imaging equipment ensuring the reliability of healthcare equipment such as MRI and CT scanners. The country’s advanced healthcare system supports hospital equipment outsourcing, as facilities adopt managed medical equipment services to streamline operations.

The UK market is driven by the need for hospital cost optimization strategies, with clinical asset management gaining traction in public and private hospitals to maintain diagnostic imaging equipment. France’s market thrives on technological advancements in medical device maintenance services, with healthcare service providers adopting equipment-as-a-service (EaaS) for hospitals to enhance efficiency.

Asia Pacific Managed Equipment Service Market Trends

Asia Pacific is the fastest-growing region, with a CAGR of 8.5%, led by China, Japan, and India, driven by rapid healthcare infrastructure services. China’s market is fueled by government-led initiatives to modernize hospital services, with managed medical equipment services supporting the maintenance of diagnostic imaging equipment to meet growing patient demand.

The country’s healthcare reforms emphasize hospital equipment outsourcing, driving clinical asset management adoption. India’s market grows due to increasing access to healthcare and a focus on hospital cost optimization strategies, with MES for diagnostic imaging equipment gaining traction in urban hospitals. Japan’s market benefits from advanced healthcare infrastructure modernization, with medical device maintenance services ensuring the reliability of MRI, CT, and X-ray maintenance in high-tech medical facilities.

Competitive Landscape

The global managed equipment service market is highly competitive, with Siemens Healthineers, GE Healthcare, Philips Healthcare, Medipass Healthcare, Althea Group, Canon Medical, Healthcare Technologies International (HTI), Medecon Healthcare, BCAS Biomed, MES Group, iDAE (Beijing) MedTech, and NATEX Measurement Solutions focusing on healthcare equipment, hospital services, and medical device maintenance services.

Companies leverage hospital cost optimization strategies and equipment-as-a-service (EaaS) for hospitals to gain market share. Strategic partnerships and R&D investments in healthcare infrastructure services drive managed equipment service market growth trends, addressing clinical asset management needs.

Key Developments

- In 2025, Sutter Health and GE HealthCare announced a seven-year, approximately $1 billion strategic partnership in January 2025, called the Care Alliance, focused on enhancing diagnostic imaging services across Sutter Health's facilities in California. This collaboration involves providing GE HealthCare's AI-powered imaging technologies and software upgrades to improve patient care, streamline diagnostic processes, and expand access to advanced imaging for the 3.5 million patients Sutter Health serves.

- In 2023, Philips Healthcare significantly expanded its Equipment-as-a-Service (EaaS) offerings, including the Enterprise Monitoring as a Service (EMaaS) and other technology asset management solutions, to provide hospitals with subscription-based access to equipment and services. This expansion helps hospitals avoid large upfront capital costs, gain predictable operating expenses, and ensure their equipment remains up-to-date with the latest software and hardware, ultimately improving patient care and operational efficiency.

Companies Covered in Managed Equipment Service Market

- Siemens Healthineers

- GE Healthcare

- Philips Healthcare

- Medipass Healthcare

- Althea Group

- Canon Medical

- HTI

- Medecon Healthcare

- BCAS Biomed

- MES Group

- iDAE (Beijing) MedTech

- NATEX Measurement Solutions

- Others

Frequently Asked Questions

The managed equipment service market is projected to reach US$ 5.7 Bn in 2025, driven by healthcare equipment and hospital services.

Rising healthcare infrastructure modernization and cost-saving with managed equipment service solutions fuel hospital equipment outsourcing.

The managed equipment service market is likely to grow at a CAGR of 7.6% from 2025 to 2032, and reaching US$ 9.5 Bn.

Predictive maintenance and equipment-as-a-service (EaaS) for hospitals, with 20% growth in emerging markets, drive clinical asset management.

Key players include Siemens Healthineers, GE Healthcare, Philips Healthcare, Canon Medical, and Althea Group.