- Technology

- Enterprise Social Networks and Online Communities Market

Enterprise Social Networks and Online Communities Market Size, Share, and Growth Forecast 2026 - 2033

Enterprise Social Networks and Online Communities Market by Deployment Model (Cloud-based, On-premise, Hybrid), Organization Size (Large enterprises, Small & Medium Enterprises), Industry Type (Healthcare, BFSI, IT & Telecom, Government, Retail & Consumer Goods, Others), and Regional Analysis, 2026 - 2033

Enterprise Social Networks and Online Communities Market Size and Trend Analysis

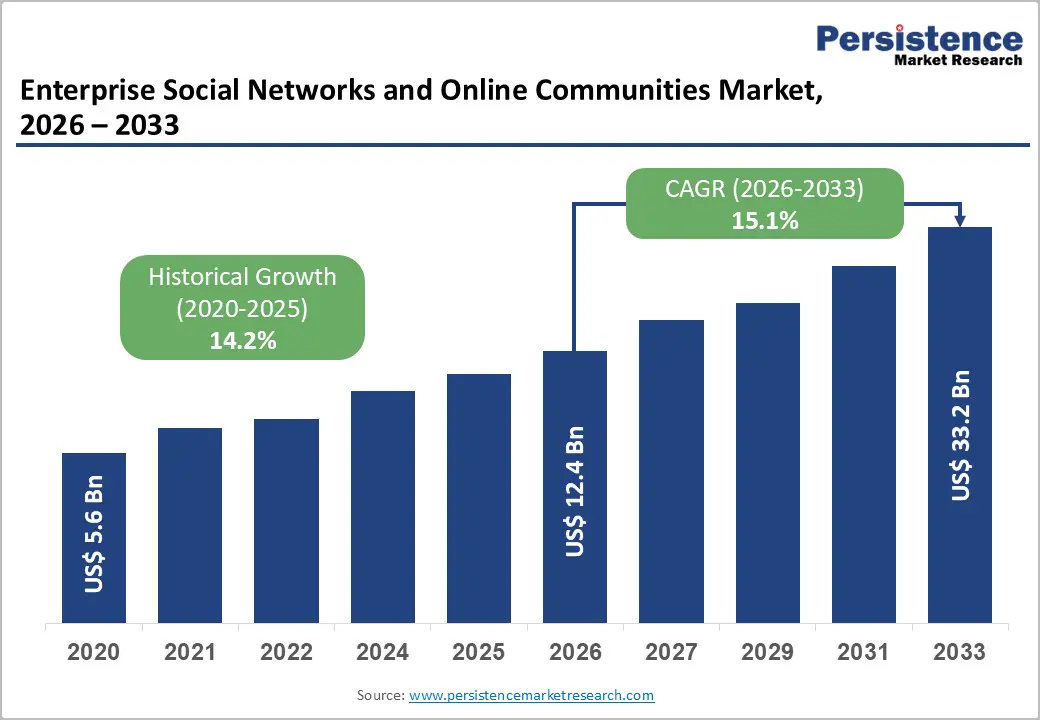

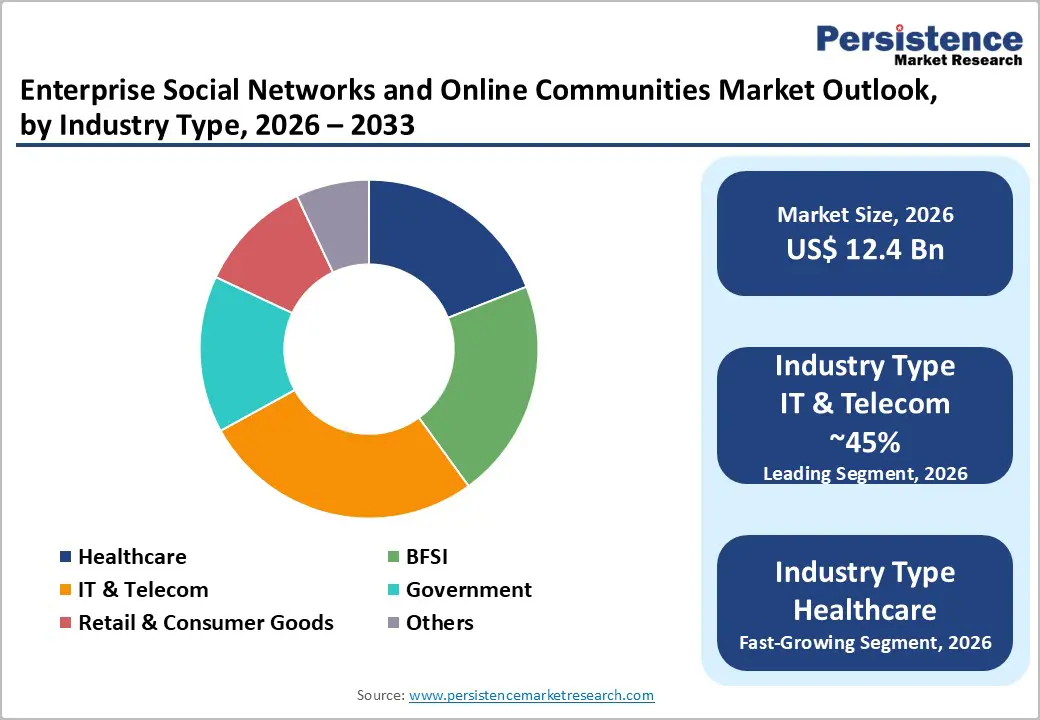

The global enterprise social networks and online communities market is projected to be valued at US$ 12.4 billion in 2026 and is expected to reach US$ 33.2 billion by 2033, expanding at a CAGR of 15.1% from 2026 to 2033.

The rapid adoption of hybrid work environments and organization-wide digital transformation initiatives largely drives market growth. Enterprises increasingly rely on social collaboration platforms to enhance internal communication, streamline knowledge sharing, and improve employee engagement. In parallel, the growing preference for cloud-based solutions, due to their scalability, cost efficiency, and ease of deployment, is accelerating adoption, particularly among small and medium-sized enterprises operating in digitally evolving markets.

Key Industry Highlights:

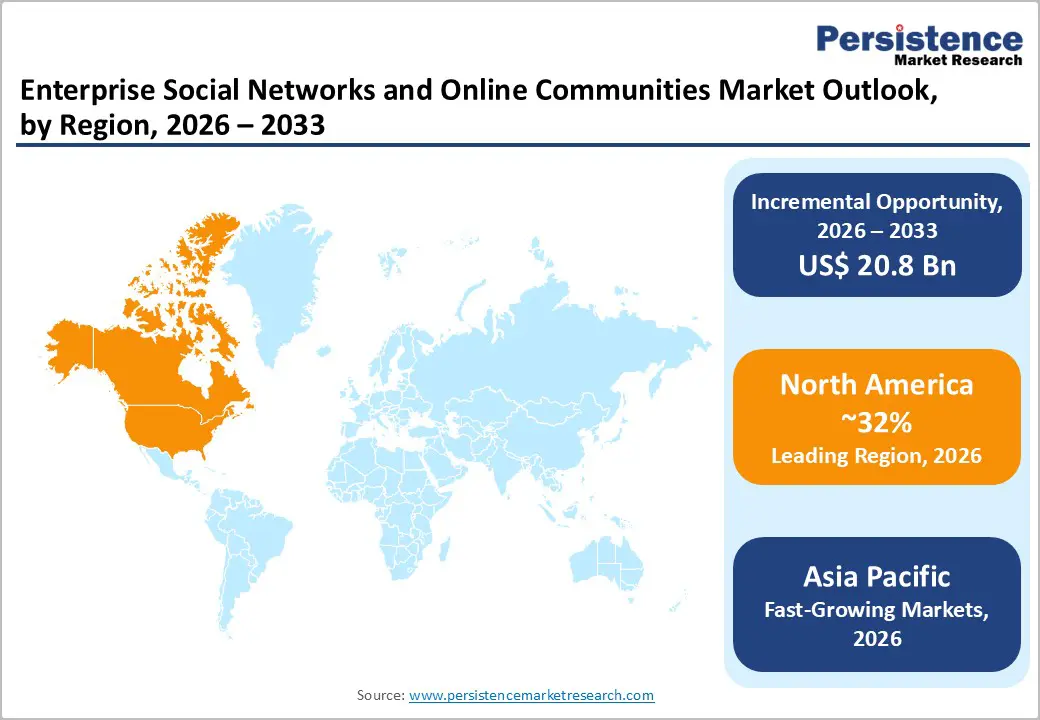

- Leading Region: North America leads with 32% market share, 91 of Fortune 100 companies using Teams, and ~6.7 million websites using Google Workspace.

- Fastest-Growing Region: Asia Pacific holds a 28% share, fueled by digital initiatives in China, India, and Japan and is projected to reach $21.4 Bn in AI investment by 2024.

- Dominant Deployment Segment: Cloud-based platforms command 54.3% share in 2025, with seamless scalability and integration driving adoption.

- Fastest Growing Enterprise Segment: SMEs contribute 51.7% of revenue, growing at 14.9% CAGR through 2035 due to SaaS subscription models.

- Key Market Opportunity: AI and autonomous agents adoption, with 60% of Teams users leveraging AI tools by 2024, enabling real-time insights and workflow automation.

| Key Insights | Details |

|---|---|

|

Enterprise Social Networks and Online Communities Market Size (2026E) |

US$ 12.4 Billion |

|

Market Value Forecast (2033F) |

US$ 33.2 Billion |

|

Projected Growth CAGR (2026-2033) |

15.1% |

|

Historical Market Growth (2020-2025) |

14.2% |

Market Dynamics

Drivers - Accelerating Shift Toward Hybrid and Remote Workforces Reshaping Enterprise Collaboration Needs

The global transition toward hybrid and remote work has fundamentally altered enterprise communication structures, driving sustained demand for enterprise social networks and online communities. Research indicates that nearly six in ten employees with remote-capable roles prefer hybrid work models, while around one-third favor fully remote arrangements. In the U.S., hybrid job postings increased from 15% in Q2 2023 to 24% in Q2 2025, underscoring the permanence of flexible work strategies.

As geographically dispersed teams become the norm, organizations require centralized digital platforms that support real-time collaboration, knowledge sharing, and asynchronous communication across time zones. Enterprise social networks enable workforce alignment, reduce information silos, and preserve organizational culture in decentralized environments, making them a critical foundation for productivity, engagement, and operational continuity in hybrid work ecosystems.

Rise in Digital Transformation Investments and Regulatory Compliance Pressures Strengthening Platform Adoption

Organizations across industries are accelerating digital transformation initiatives to modernize legacy systems and enhance operational efficiency in competitive, digitally driven markets. Regulatory frameworks such as the European Union’s GDPR, which imposes penalties of up to €20 million or 4% of global annual revenue, have significantly heightened enterprise focus on secure and compliant communication environments. Following GDPR enforcement, approximately 73% of European organizations strengthened customer data management practices, while 62% increased cybersecurity investments.

Enterprise social networks and online community platforms offering robust security controls, compliance certifications, and data governance capabilities are increasingly viewed as mission-critical infrastructure. As enterprises operate across multiple jurisdictions and stakeholder trust becomes a strategic priority, these platforms are evolving beyond collaboration tools into secure digital environments that support compliant communication, risk mitigation, and long-term enterprise resilience.

Restraints - Persistent Digital Infrastructure Gaps and Limited Technology Readiness Across Emerging Economies

Despite accelerating global adoption, uneven digital infrastructure development continues to restrain market growth, particularly across emerging economies in Africa, South Asia, and parts of Latin America. Many organizations in these regions face unreliable broadband connectivity, constrained IT budgets, and limited access to skilled technical resources. Studies on SME digitalization consistently identify a lack of financing and insufficient digital literacy as primary barriers to adopting advanced enterprise collaboration platforms.

These infrastructure and capability constraints restrict organizations to lower levels of digital maturity, reducing their ability to deploy comprehensive enterprise social networks and online community solutions. As a result, market penetration remains uneven across regions, with adoption concentrated in digitally mature economies, while growth in lower-income markets is slowed by structural limitations in connectivity, capital investment capacity, and technical preparedness.

Data Privacy Risks, Regulatory Complexity, and Vendor Lock-in Concerns Limiting Cloud Adoption

Enterprises continue to express caution over consolidating sensitive internal communications and employee data within third-party cloud platforms, particularly amid rising cybersecurity incidents and evolving global data protection regulations. Managing compliance across multiple jurisdictions, combined with concerns around data sovereignty, auditability, and long-term control over enterprise data, creates hesitation toward rapid platform migration.

These concerns are especially pronounced in regulated industries such as healthcare and BFSI, where data protection obligations are stringent, and risk tolerance is low. As a result, many organizations favor on-premise or hybrid deployment models despite higher costs and reduced scalability, slowing the adoption of fully cloud-based enterprise social networking solutions in high-value, compliance-sensitive enterprise segments.

Opportunity - Rapid Expansion of Small and Medium Enterprises Driving Enterprise Collaboration Adoption

Small and Medium Enterprises (SMEs) are emerging as the fastest-growing segment for enterprise social networks and online communities, fueled by reduced software costs through subscription-based SaaS models. In 2025, SMEs accounted for 51.7% of market revenue, highlighting their dominant presence. Affordable, cloud-based platforms with intuitive interfaces have democratized access to advanced collaboration tools that were previously limited to large enterprises.

As SMEs increasingly compete for skilled talent and pursue operational efficiency, seamless communication and knowledge management platforms have become strategic imperatives. Supported by government initiatives in Asia Pacific, Latin America, and the Middle East & Africa, including subsidies, training programs, and infrastructure development, the SME segment is expected to grow at a CAGR of 14.9% through 2033, representing substantial market expansion opportunities.

Adoption of Advanced Artificial Intelligence and Autonomous Agents Creating Differentiation Opportunities

The integration of generative AI and autonomous agent technologies is transforming enterprise collaboration platforms, offering significant opportunities for innovation and competitive differentiation. Leading providers, such as Salesforce, have integrated Slack with CRM and analytics tools, enabling unified workspaces where human employees and AI agents collaborate seamlessly. By 2024, approximately 60% of Microsoft Teams users leverage AI-powered tools, reflecting strong organizational demand for intelligent assistance.

This convergence of AI, analytics, and enterprise social networks enables platforms to provide real-time recommendations, automate routine communications, and enhance data-driven decision-making. Vendors that successfully deliver these intelligent capabilities can position themselves as providers of comprehensive digital workplace ecosystems, capturing higher market share, premium valuations, and long-term strategic relevance in evolving enterprise environments.

Category-wise Analysis

Deployment Model Insights

Cloud-based platforms dominate the enterprise social networks and online communities market, holding approximately 54.3% of market share in 2025. Their leadership is driven by scalability, accessibility, and the elimination of significant capital expenditure associated with on-premise deployments. Cloud solutions allow rapid updates, seamless integration with business applications, and robust security maintenance, making them the preferred deployment model globally.

While cloud leads, hybrid platforms are the fastest-growing category. Organizations adopt hybrid models to balance flexibility, security, and compliance requirements. These platforms support distributed teams, gradual cloud migration, and advanced features such as AI analytics and integrated communication tools, enabling businesses to scale efficiently while maintaining operational control in regulated or sensitive environments.

Organization Size Insights

Small and Medium Enterprises (SMEs) accounted for approximately 51.7% of the enterprise social networks market revenue in 2025, establishing them as the largest enterprise-size category. SMEs benefit from SaaS subscription models that remove historical cost barriers, allowing affordable access to sophisticated enterprise collaboration tools, improving productivity, and supporting internal knowledge sharing across geographically dispersed teams.

SMEs also represent the fastest-growing segment. They are adopting enterprise social networks to enhance communication, streamline employee engagement, and gain competitive advantages without heavy IT investments. The accessibility, affordability, and user-friendly nature of these platforms position SMEs as key drivers of market expansion in the coming years.

Industry Insights

The IT & Telecom sector leads adoption, holding approximately 45% market share across industry verticals. Technology-driven and geographically distributed organizations leverage cloud-based collaboration platforms to improve cross-functional communication, project coordination, and operational efficiency. High digital literacy and reliance on integrated digital workplace solutions reinforce IT & Telecom as the market’s adoption leader.

The healthcare and BFSI sectors are the fastest-growing categories. Adoption is driven by regulatory compliance, patient safety imperatives, and operational complexity. Enterprise social networks facilitate rapid information exchange, coordination across distributed teams, and audit trail maintenance, enabling these knowledge-intensive industries to meet compliance standards, optimize decision-making, and enhance collaborative efficiency in highly regulated environments.

Regional Insights

North America Enterprise Social Networks and Online Communities Market Trends

North America leads the global market, accounting for approximately 32% of the total market share in 2025. Adoption is strongest in the United States, where nearly 6.7 million websites utilize Google Workspace, reflecting broad organizational digital transformation. Microsoft Teams has become a standard in large enterprises, with 91 of the Fortune 100 companies implementing the platform for internal collaboration. Mature IT infrastructure, strong cybersecurity frameworks, and substantial enterprise IT budgets support rapid deployment of advanced collaboration tools.

Cloud-based platforms remain the backbone of adoption, enabling real-time communication, seamless Microsoft 365 integration, and robust security. Enterprises increasingly demand AI-powered features, compliance certifications, and end-to-end security, creating premium segments. These requirements allow vendors to offer comprehensive, high-value collaboration solutions while consolidating multiple communication and workflow tools across organizations.

Europe Enterprise Social Networks and Online Communities Market Trends

Europe is the second-largest regional market, influenced by GDPR and strong adoption in Germany, the UK, and France. Germany leads with approximately 0.8 million websites using Google Workspace, while France and the UK have around 0.6 million each. Regulatory requirements drive platform adoption, as organizations focus on data sovereignty, privacy compliance, and transparent processing practices. GDPR enforcement, with cumulative fines exceeding €2.8 billion, has made compliance a core requirement for enterprise social networking solutions.

The region is projected to grow at a CAGR of 12.4% through 2033, driven by initiatives such as Germany’s Industry 4.0 and France’s SME digital transformation programs. Manufacturing, creative, and design sectors show strong adoption momentum, using enterprise social networks to enhance knowledge sharing, collaboration, and innovation across distributed teams.

Asia Pacific Enterprise Social Networks and Online Communities Market Trends

Asia Pacific is the fastest-growing regional market, accounting for approximately 28% of the global market share in 2025. Government-led digital initiatives, such as China’s digital economy programs, India’s Digital India, and Japan’s Society 5.0, are driving adoption, particularly among SMEs seeking cost-effective cloud solutions. China and India’s growing SME populations and manufacturing prominence create strong demand for scalable collaboration platforms that support distributed operations and supply chains.

The region’s rapid digital transformation, coupled with large populations and increasing AI adoption, positions the Asia-Pacific to surpass North America and Europe by 2033. Enterprise social networks facilitate efficient knowledge sharing, workforce productivity, and operational continuity across geographically dispersed teams, making these platforms essential for regional competitiveness and organizational growth.

Competitive Landscape

The global enterprise social networks and online communities market exhibits a moderately consolidated structure, with global leaders coexisting alongside specialized regional and vertical-focused solutions. Market dominance is largely driven by deep integration with existing enterprise software ecosystems, extensive vendor investment in artificial intelligence, and the ability to leverage installed user bases for seamless workflow integration and unified platform management.

Competition increasingly revolves around platform extensibility, support for third-party developer ecosystems, and integration of multiple collaboration functions within a single environment. Emerging differentiation strategies focus on AI-powered analytics, autonomous agent capabilities, advanced security frameworks, and compliance across jurisdictions, while smaller specialized vendors maintain relevance through niche focus and tailored pricing models.

Key Developments:

- In June 2025, Salesforce completed seamless integration of the Slack communication platform directly into its CRM system, positioning Slack as the core operating system for enterprise work within Salesforce environments. The integration enables bi-directional data flow between Slack conversations and Salesforce records, with Tableau Next analytics now directly accessible within Slack, creating unified workspaces where humans and AI agents collaborate on customer outcomes and business processes.

- In August 2024, Microsoft announced that Teams achieved 320 million monthly active users globally with 200 million daily active users, coupled with 93% adoption among Fortune 100 companies and 95% among Fortune 500 organizations. The platform's integration with Microsoft 365 applications and AI-powered Copilot features continues driving sustained adoption across enterprise segments and geographic regions.

- In April 2024, the ILO, DICT, and Japanese government jointly inaugurated a Digital Transformation Center in the Pampanga region specifically designed to provide MSMEs and regional stakeholders with comprehensive training, technology resources, and strategic guidance for digital adoption, targeting enhanced digitalization accessibility and competency development across the emerging market SME population.

Companies Covered in Enterprise Social Networks and Online Communities Market

- Google Inc.

- Lithium Technologies Inc.

- TIBCO Software Inc.

- SAP SE

- Salesforce

- VMware

- Cisco Systems

- IBM Corporation

- Vanilla Forums

- Zimbra

- Axero Solutions

- Igloo Software

- Zoho Corporation

- Aurea Software Inc.

- Microsoft Corporation

Frequently Asked Questions

Enterprise social networks and online communities market is poised to reach US$ 33.2B by 2033 from US$ 12.4B in 2026, driven by hybrid work, digital transformation, and advanced collaboration.

Growth fueled by 60% hybrid work preference, 73% EU firms enhancing data management post-GDPR, and SaaS democratization for SMEs.

SMEs fastest-growing segment with 51.7% revenue share in 2025 and 14.9% CAGR through 2035, supported by SaaS and government programs.

North America dominates with 32% market share, 91 of Fortune 100 companies using Teams, 320 million Teams MAUs, and ~6.7 million websites using Google Workspace, supported by mature IT infrastructure and budgets.

AI-powered autonomous agents represent the top opportunity, with 60% of Teams users adopting AI tools by 2024, enabling real-time recommendations, workflow automation, and data-driven decision-making.