- Non-food Packaging

- Corrugated Packaging Market

Corrugated Packaging Market Size, Share, Trends, Growth, and Forecasts for 2025 - 2032

Corrugated Packaging Market by Package Type (Single Wall, Double Wall, Triple Wall, Single Face Boards), by Application (Electronics and Electricals, Food and Beverages), Distribution Channel (Direct, Indirect Sales), and Regional Analysis for 2025 - 2032

Corrugated Packaging Market Size and Trends

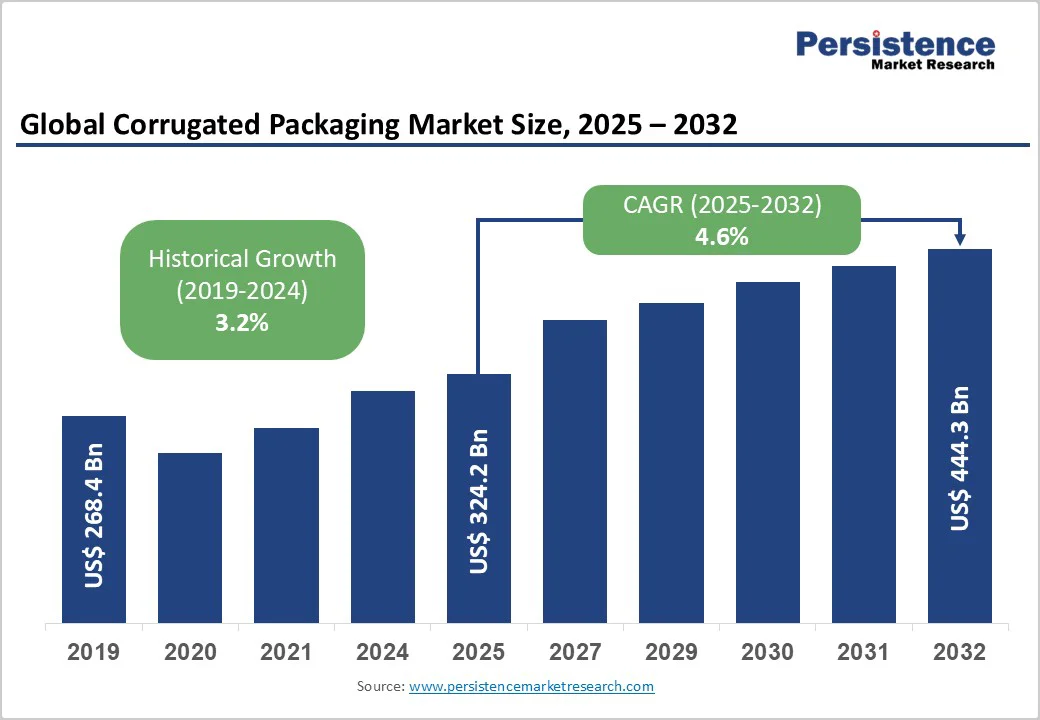

The corrugated packaging market size is likely to be valued at US$ 324.2 Billion in 2025 and is estimated to reach US$ 444.3 Billion in 2032, growing at a CAGR of 4.6% during the forecast period 2025-2032. The corrugated packaging market growth is being fueled by sustainability goals and developments in packaging design. The rapid rise of online retail also continues to boost demand globally.

Key Industry Highlights

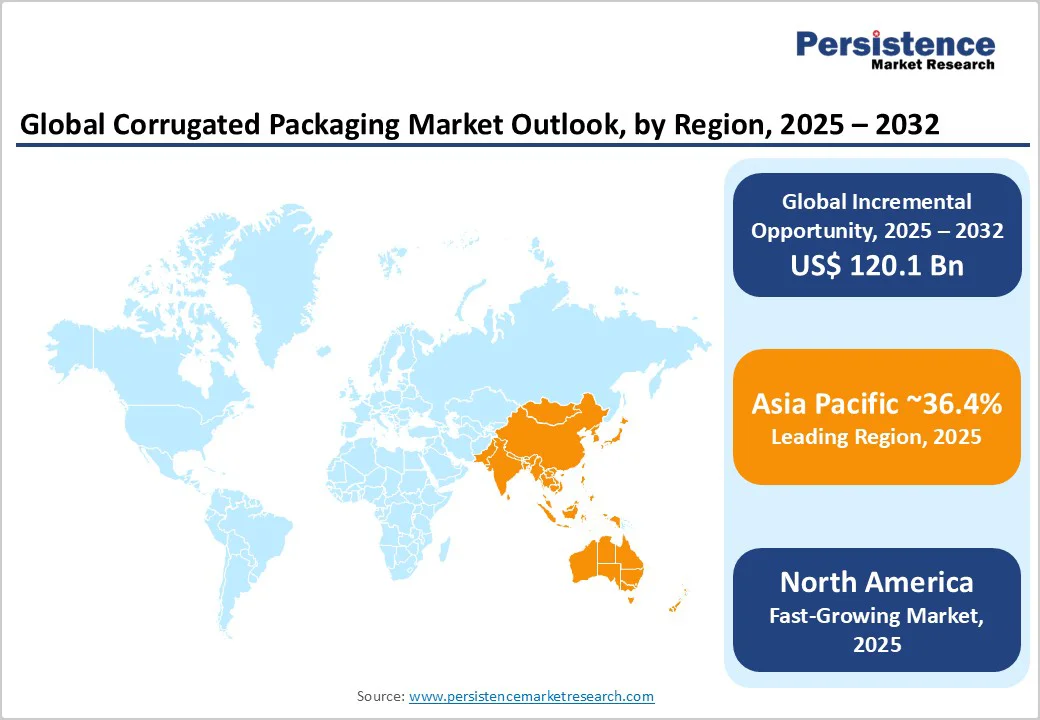

- Leading Region: Asia Pacific with about 36.4% share in 2025, backed by massive manufacturing and export activities across China and India.

- Fastest-growing Region: North America, boosted by rising sustainability commitments by brands replacing plastic with recyclable corrugated boxes.

- New Plant: With an investment of more than US$ 110 million, Saica Group, has begun to build its second Saica Pack plant in the U.S., a new corrugated manufacturing facility in Anderson. The 350,000-square-foot facility will produce more than 1,200,000 MSF of corrugated packaging.

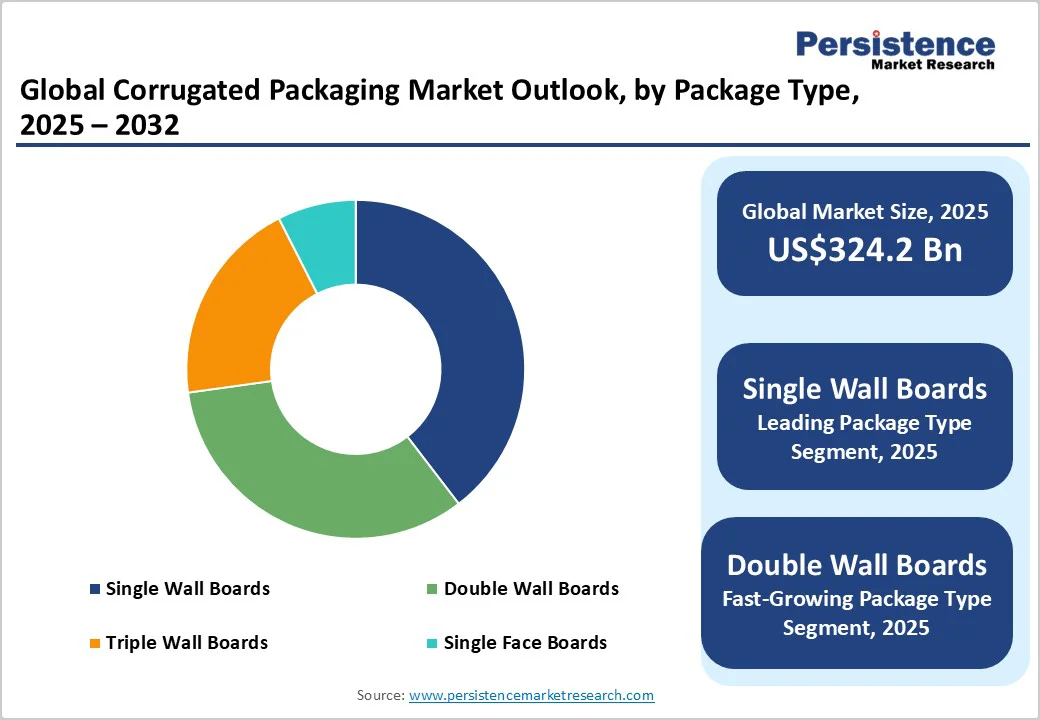

- Leading Package Type: Single wall boards hold nearly 39.6% share in 2025, as they provide optimal strength-to-weight ratio suitable for most consumer and e-commerce packaging.

- Dominant Application: Food and beverages, approximately 33.1% of the corrugated packaging market share in 2025, due to the growth of takeaway and online food delivery services.

- Key Distribution Channel: Direct sales recorded about 67.2% share in 2025, as these enable better pricing, consistent quality control, and long-term supply partnerships.

| Key Insights | Details |

|---|---|

|

Corrugated Packaging Market Size (2025E) |

US$ 324.2 Billion |

|

Market Value Forecast (2032F) |

US$ 444.3 Billion |

|

Projected Growth (CAGR 2025 to 2032) |

4.6% |

|

Historical Market Growth (CAGR 2019 to 2024) |

3.2% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis- Rising Preference for Eco-friendly and Circular Packaging Solutions

The surging emphasis on sustainability is a key growth driver for corrugated packaging. Made primarily from paper-based, renewable fibers, corrugated boxes are biodegradable and easily recyclable, complying with global circular economy goals. Governments across Europe and Asia Pacific are introducing strict regulations on single-use plastics, pushing brands to shift toward paper-based packaging.

IKEA and Nestlé have already phased out plastic secondary packaging in favor of corrugated alternatives. In addition, the ability to use recycled content without compromising strength makes corrugated packaging a preferred choice for businesses seeking low-carbon and eco-certified packaging solutions.

Development of Digital Printing and Customization Technologies

The ongoing expansion of digital printing technologies has significantly improved the value proposition of corrugated packaging. Brands can now personalize boxes with high-quality graphics, localized branding, or promotional designs without the requirement for large-scale print runs. This flexibility reduces setup costs and waste while supporting limited-edition or region-specific campaigns.

For example, Amazon and Coca-Cola use digitally printed corrugated boxes for festive and regional promotions, strengthening customer engagement. As e-commerce and D2C brands increasingly use packaging as a branding tool, digitally printed corrugated boxes are becoming a key growth catalyst for the industry.

Barrier Analysis- Limited Load-bearing Capacity and Structural Weakness in Storage

A key restraint for corrugated packaging is its limited strength when exposed to excessive stacking or uneven weight distribution. Unlike rigid materials such as plastic or wood, corrugated boxes can deform or collapse under heavy loads, especially during bulk transportation or long-term warehouse storage. This weakness often results in product damage and high logistics losses.

Industries dealing with heavy goods, including automotive or machinery, still rely on wooden crates or plastic pallets instead of corrugated boxes for this reason. To address this, companies such as Smurfit Kappa are developing reinforced corrugated designs with honeycomb structures, but widespread adoption remains limited due to high costs.

Sensitivity to Environmental Conditions Affecting Durability

Another key limitation is the susceptibility of corrugated materials to moisture and temperature changes. High humidity or condensation can weaken the paper fibers, causing boxes to lose rigidity or warp, while low humidity can make them brittle and prone to cracking. This poses challenges in cold chain logistics and tropical climates, where maintaining packaging integrity is critical.

For example, food exporters in Southeast Asia often use laminated or wax-coated corrugated boxes to prevent moisture absorption, increasing production costs. Although moisture-resistant coatings are improving, balancing sustainability with weather durability continues to be a key industry challenge.

Opportunity Analysis- Adoption of Recycled Fibers and Emerging Alternatives

The rising focus on sustainability is creating new opportunities for using recycled and alternative fibers in corrugated packaging. Manufacturers are investing in closed-loop recycling systems to recover post-consumer waste and reintroduce it into box production. At the same time, companies are experimenting with fast-growing, renewable materials such as bamboo, bagasse, and wheat straw to reduce dependency on virgin wood pulp.

For instance, Nine Dragons Paper and Huhtamaki have started integrating bamboo fibers into corrugated board manufacturing to improve strength and biodegradability. This shift not only meets eco-conscious consumer preferences but also helps companies comply with evolving regulations on recycled content and deforestation control.

Development in Lightweight and High-strength Paper Grades

Developing unique paper grades that maintain durability with less material usage presents another prominent opportunity for corrugated packaging producers. Lightweight corrugated boards reduce transportation costs, lower emissions, and improve handling efficiency. Companies such as Mondi and DS Smith are introducing next-generation kraft liners and fluting papers that deliver high compression strength with reduced fiber input.

For example, DS Smith’s Next Fiber technology allows up to 15% less material use without compromising box performance. Such developments support both sustainability goals and profitability, as businesses can transport more goods using light, yet equally strong corrugated packaging.

Category-wise Analysis

Package Type Insights

Single wall boards are predicted to account for approximately 39.6% of share in 2025 as they provide the ideal balance between strength, weight, and cost. These boards are suitable for most standard packaging requirements, especially for consumer goods, electronics, and lightweight industrial products. Their easy foldability and printability make them compatible with automated packaging lines and digital printing processes, which is why e-commerce and retail brands favor them for shipping boxes. Also, single wall boards help reduce material usage, complying with global sustainability goals.

Double wall boards are seeing steady demand because they provide improved durability and crush resistance, making them ideal for heavy-duty or long-distance shipments. These boards are commonly used in packaging bulk food products, appliances, and industrial goods that require extra cushioning. The surging use of double wall boards in B2B logistics and cross-border e-commerce is supporting their steady demand. For instance, key exporters in Asia and Europe prefer double wall boards to ensure goods remain intact during container transport, especially for fragile or bulky items.

Application Insights

Food and beverages will likely capture around 33.1% of share in 2025 because the industry demands hygienic, lightweight, and sustainable solutions for transporting and storing products safely. Corrugated boxes deliver excellent protection against contamination and physical damage while being recyclable and cost-effective. The shift toward takeaway and delivery models has boosted their use in food packaging. Coca-Cola and PepsiCo have adopted corrugated secondary packaging with reduced plastic use, while McDonald’s and Domino’s are switching to corrugated solutions for recyclable food transport boxes.

E-commerce is a key application area as every online order requires protective and customizable packaging that can handle complex logistics. Corrugated boxes are preferred for their strength, recyclability, and adaptability to various shapes and weights. Amazon and Flipkart have standardized corrugated boxes with easy-open, returnable, and branding-friendly designs to improve customer experience and reduce waste. The rise of social commerce and direct-to-consumer (D2C) brands has also increased the demand for visually appealing and brand-printed corrugated packaging that doubles as a marketing tool.

Distribution Channel Insights

Direct sales are poised to hold nearly 67.2% of share in 2025 because large companies and industrial users prefer to buy directly from manufacturers for customized solutions and better pricing control. Direct partnerships enable packaging producers to provide personalized board grades, structural design, and supply chain integration. For example, food processors and FMCG giants often enter long-term contracts with corrugated packaging manufacturers to ensure consistent quality and on-time supply.

Indirect sales are gaining impetus as small businesses, online retailers, and regional distributors increasingly buy through third-party suppliers, wholesalers, or e-commerce packaging platforms. This channel provides flexibility for customers who require limited quantities or diverse packaging options without long-term contracts. Online B2B marketplaces such as Packhelp in Europe and Bizongo in India are extending the reach of corrugated packaging suppliers by connecting them directly with small enterprises.

Regional Insights

Asia Pacific Corrugated Packaging Market Trends

In 2025, Asia Pacific is estimated to account for nearly 36.4% of share due to booming e-commerce, industrialization, and manufacturing activities in China, India, Vietnam, and Indonesia. China remains the production hub, with several new corrugation plants being set up to meet domestic and export packaging requirements. Companies such as Nine Dragons Paper and Lee & Man Paper are expanding recycled containerboard production to meet sustainability goals and regional packaging demand.

India’s growth is led by e-commerce giants, including Flipkart and Amazon, who are partnering with local converters to adopt lightweight and recyclable corrugated boxes. However, Asia Pacific still faces challenges in recycling infrastructure and raw material cost volatility. Governments across the region are enforcing new Extended Producer Responsibility (EPR) rules to encourage the use of eco-friendly and recyclable corrugated materials.

North America Corrugated Packaging Market Trends

North America’s market is mature but evolving through development and digitalization. The U.S. dominates regional production, with companies such as WestRock, International Paper, and Packaging Corporation of America focusing on automation and smart manufacturing to offset labor shortages. Digital printing on corrugated packaging has gained traction among retail and e-commerce players, including Walmart and Amazon, who demand customized branding and fast turnaround.

Despite steady demand, North America saw a dip in box shipments in early 2025 due to relatively slow retail and manufacturing activity. However, the rise of reusable and returnable corrugated boxes is creating new opportunities as companies aim to reduce single-use packaging waste and comply with upcoming sustainability mandates.

Europe Corrugated Packaging Market Trends

In Europe, the market is characterized by strict sustainability regulations and high recycling rates, often exceeding 90%. Domestic players such as Smurfit Kappa, Mondi, and DS Smith are at the forefront of circular packaging innovation. For instance, DS Smith’s Circular Design Metrics tool helps brands design fully recyclable packaging with minimal carbon footprint.

Europe is also witnessing consolidation, with Mondi recently acquiring Schumacher Packaging’s Western European assets to strengthen its position in premium corrugated solutions. Demand is strong in sectors such as food, beverages, and consumer goods, where shelf-ready and lightweight packaging are prioritized. However, energy costs and tightening EU packaging waste regulations continue to challenge profitability, pushing companies to innovate further in material efficiency and sustainable design.

Competitive Landscape

The corrugated packaging market is highly consolidated, with a few global giants such as Smurfit Kappa, WestRock, International Paper, and DS Smith controlling a large share of the market. These companies have vertically integrated operations, owning both paper mills and converting facilities, which helps them manage costs and secure raw material supply. The recent merger between Smurfit Kappa and WestRock has created one of the largest paper-based packaging firms globally, signaling how consolidation is influencing the competitive landscape.

Business Strategies

Sustainability is a key competitive differentiator in the corrugated packaging market. Most leading companies are focusing on circular packaging solutions, lightweight corrugated boards, and increased recycled content. Smurfit Kappa, for instance, invested in eco-design labs across Europe to help brands reduce carbon emissions through better packaging design. DS Smith has also pledged that all its packaging will be 100% recyclable or reusable by 2030.

Key Industry Developments

- In March 2025, Oji India Packaging Pvt Ltd inaugurated its fifth manufacturing facility in India at Sri City, Andhra Pradesh. This new 43,000-square-metre facility will specialize in corrugated boxes and packaging accessories.

- In February 2025, DS Smith launched a folding box made of lightweight small-flute corrugated cardboard. It is an alternative to rigid assembled boxes made from grayboard.

Companies Covered in Corrugated Packaging Market

- Mondi Group

- WestRock Company

- International Paper Company

- DS Smith PLC

- Smurfit Kappa Group

- Nine Dragons Paper (Holdings) Limited

- Georgia-Pacific Equity Holdings LLC.

- Oji Holdings Corporation

- Lee & Man Paper Manufacturing Ltd.

- Packaging Corporation of America

- Others

Frequently Asked Questions

The corrugated packaging market is projected to reach US$ 324.2 Billion in 2025.

Rising preference for recyclable packaging materials and increasing focus on lightweight designs are the key market drivers.

The corrugated packaging market is poised to witness a CAGR of 4.6% from 2025 to 2032.

Expansion in circular economy initiatives and rising adoption of smart packaging are the key market opportunities.

Mondi Group, WestRock Company, and International Paper Company are a few key market players.