- Biotechnology

- Yeast Infection Treatment Market

Yeast Infection Treatment Market Size, Share, and Growth Forecast 2026 - 2033

Yeast Infection Treatment Market by Treatment Type (Polygene, Azoles, Echinocandin, Others), by Indication (Genital Candidiasis, Invasive Candidiasis, Oropharyngeal/Esophageal Candidiasis, Others), by Form, by Route of Administration, by Distribution Channel, by Regional Analysis, 2026 - 2033

Yeast Infection Treatment Market Share and Trends Analysis

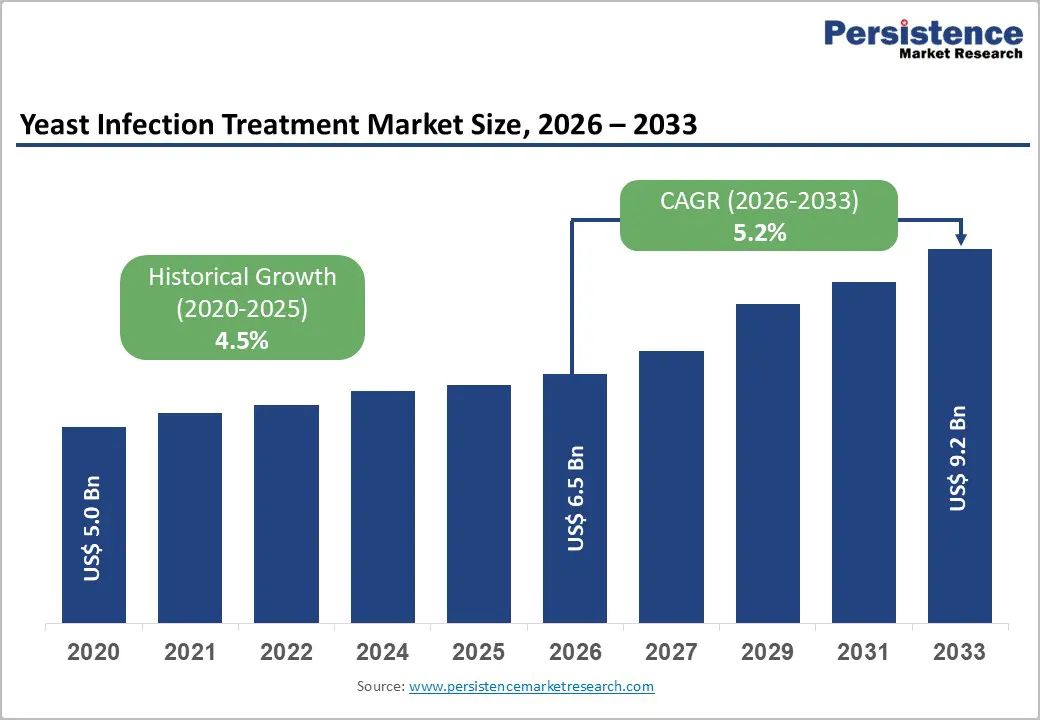

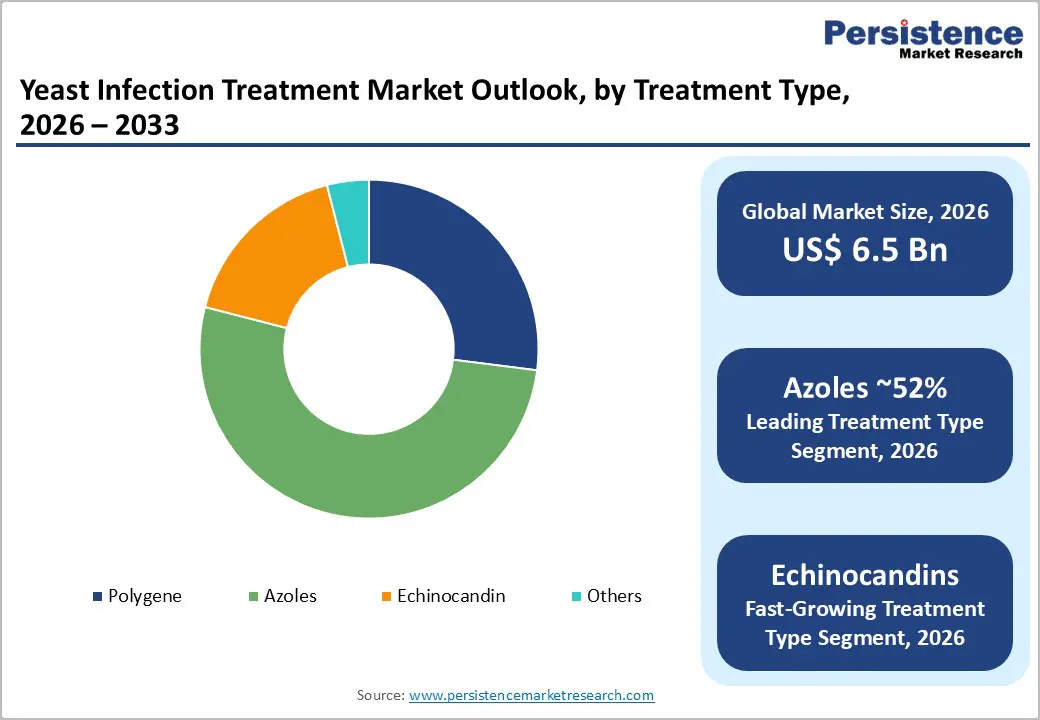

The global yeast infection treatment market size is expected to be valued at US$ 6.5 billion in 2026 and projected to reach US$ 9.2 billion by 2033, growing at a CAGR of 5.2% between 2026 and 2033. The yeast infection treatment market focuses on therapies for fungal infections, primarily caused by Candida species.

These infections commonly affect the vaginal, oral, and skin and range from mild to invasive conditions. Rising diabetes prevalence and a growing immunocompromised population have significantly increased susceptibility to fungal infections worldwide. As a result, demand for effective topical, oral, and intravenous antifungal treatments continues to rise across hospitals, clinics, and retail pharmacies. Market trends indicate steady growth supported by advancements in antifungal drug development and improved diagnostic capabilities. Public health awareness campaigns and better patient education have encouraged early treatment-seeking behavior. Additionally, expanded availability of over-the-counter antifungal products has improved accessibility and convenience, strengthening global market expansion.

Key Industry Highlights:

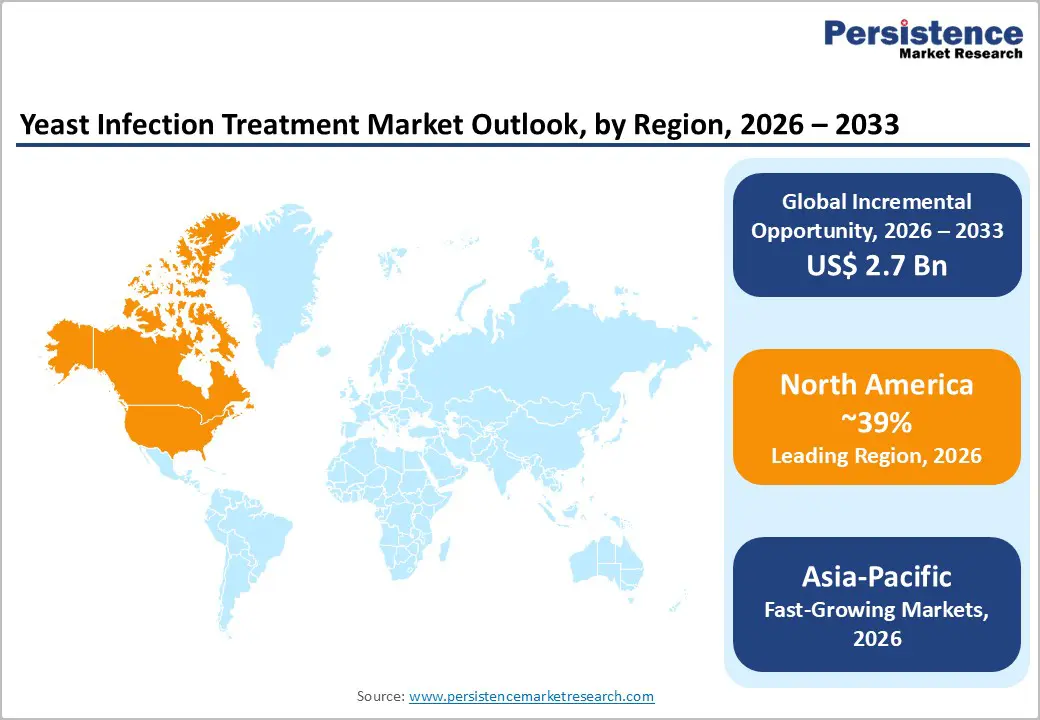

- Leading Region: North America leads the global yeast infection treatment market, supported by high diagnosis rates, strong healthcare infrastructure, widespread availability of OTC antifungals, and continuous regulatory approvals of advanced therapies.

- Fastest Growing Region: Asia Pacific is the fastest-growing region, driven by rising diabetes prevalence, improving healthcare access, expanding pharmaceutical distribution networks, and increasing awareness of women’s health and hygiene.

- Dominant Segment: Azoles dominate the market due to broad-spectrum efficacy, affordability, extensive clinical usage, and availability in both prescription and over-the-counter formulations.

- Fastest Growing Segment: Echinocandins are the fastest-growing segment, fueled by rising antifungal resistance, increasing cases of invasive candidiasis, and growing adoption in hospital and critical care settings.

| Key Insights | Details |

|---|---|

| Yeast Infection Treatment Market Size (2026E) | US$ 6.5 billion |

| Market Value Forecast (2033F) | US$ 9.2 billion |

| Projected Growth CAGR (2026 - 2033) | 5.2% |

| Historical Market Growth (2020 - 2025) | 4.5% |

Market Dynamics

Driver - Rising Prevalence of Fungal Infections & Advancements in Antifungal Therapies

The increasing prevalence of fungal infections, particularly candidiasis, is a major factor driving the yeast infection treatment market. According to the Centers for Disease Control and Prevention (CDC), nearly 75% of women experience at least one vaginal yeast infection in their lifetime, with recurrent cases affecting approximately 5-9%, necessitating effective and sustained therapies. The growing burden of chronic conditions such as diabetes further elevates susceptibility to Candida infections. The World Health Organization reports that global diabetes prevalence stands at 10.5%, and elevated blood glucose levels create favorable conditions for Candida growth. Additionally, aging populations and rising use of broad-spectrum antibiotics contribute to higher infection rates. As awareness improves and diagnosis becomes more accessible, demand for effective topical and systemic antifungal therapies continues to expand across both developed and developing healthcare systems.

Therapeutic advancements are further strengthening market growth. The development of improved azoles and echinocandins has enhanced treatment success, particularly in resistant and invasive infections. Newer formulations offer broader antifungal coverage, fewer side effects, and improved dosing convenience. Combination therapies and extended-spectrum agents have demonstrated high clinical success rates, increasing physician confidence in prescribing advanced options. Continuous research and regulatory approvals are expanding available treatment choices, supporting long-term market expansion.

Restraints - Antifungal Resistance & High Treatment Costs

The rise in antifungal resistance poses a significant challenge to market growth. Increasing resistance to commonly prescribed azole therapies complicates the management of recurrent and severe infections. Resistant Candida strains often require alternative or combination treatments, which may not be readily available in all regions. Prolonged treatment durations and therapeutic failures can reduce patient confidence and increase healthcare burdens. In hospital settings, resistant infections may result in longer stays and higher complication risks, further straining healthcare resources. This growing resistance trend necessitates ongoing research but also limits the effectiveness of standard therapies.

High treatment costs represent another important barrier. Advanced antifungal agents, particularly echinocandins used for invasive infections, are considerably more expensive than traditional oral or topical options. In low- and middle-income countries, limited insurance coverage and out-of-pocket expenses restrict patient access to specialized therapies. Price sensitivity in emerging markets can slow adoption despite rising infection rates, ultimately constraining overall revenue growth.

Opportunity - Echinocandin Development & Expansion Through Online Channels

The development of echinocandins for drug-resistant infections presents a strong growth opportunity. These agents are increasingly recommended for severe and invasive candidiasis due to their targeted mechanism of action and favorable safety profiles. Growing resistance to first-line treatments is encouraging healthcare providers to adopt echinocandins more widely in hospital settings. Continued investment in research pipelines and expanded clinical indications can unlock premium pricing potential, particularly in tertiary care centers. As stewardship programs promote appropriate antifungal use, demand for advanced therapies is expected to rise steadily.

Expansion through online pharmacy platforms also offers meaningful growth potential. Digital health adoption is increasing rapidly, enabling patients to access prescription and over-the-counter antifungals discreetly and conveniently. E-pharmacies improve availability in underserved regions and reduce stigma associated with genital infections. Partnerships with digital healthcare providers and telemedicine platforms can broaden market reach, particularly in high-growth Asia-Pacific markets, supporting sustained long-term expansion.

Category-wise Analysis

By Treatment Type Insights

The yeast infection treatment market is segmented into polyenes. azoles, echinocandins, and other antifungal therapies. Azoles represent the most prescribed class due to their broad-spectrum activity, affordability, and availability in both topical and oral formulations. They are widely used for uncomplicated vaginal, oral, and skin infections, making them the first-line option in most outpatient settings. Polyenes, including amphotericin B, are typically reserved for more severe or systemic fungal infections because of their potent fungicidal properties. However, their use may be limited by potential toxicity and the need for monitored administration in clinical environments.

Echinocandins such as caspofungin and micafungin are increasingly utilized for invasive candidiasis and infections caused by resistant yeast strains. These agents are particularly important in immunocompromised patients and critical care settings. The “others” segment includes combination therapies and newly developed antifungal agents aimed at addressing emerging drug resistance. Continuous research and development in this segment are expanding therapeutic options and improving clinical outcomes.

By Distribution Channel Insights

The market is distributed across retail pharmacies, hospital pharmacies, specialty stores, online platforms, and other outlets. Retail pharmacies remain the primary channel for over-the-counter antifungal medications, particularly for mild to moderate infections. Their accessibility and pharmacist guidance make them a preferred choice for consumers seeking immediate treatment. Hospital pharmacies play a crucial role in dispensing prescription-based antifungal therapies for severe or invasive infections, ensuring appropriate dosing and monitoring within inpatient settings.

Specialty stores focusing on personal care and dermatological products may offer preventive and supportive solutions for yeast infections. Online sales channels are expanding rapidly due to increasing digital healthcare adoption and consumer preference for discreet purchasing. E-commerce platforms provide convenience, competitive pricing, and home delivery services. Other channels, including hypermarkets and general stores, also contribute by offering widely recognized OTC antifungal brands to the broader population.

Regional Insights

North America Yeast Infection Treatment Market Trends

North America represents a well-established market for yeast infection treatments, supported by advanced healthcare systems and strong disease awareness. High diagnosis rates and routine gynecological check-ups contribute to consistent demand for antifungal therapies. The region also reports a significant burden of diabetes and other chronic conditions that increase susceptibility to fungal infections. According to the Centers for Disease Control and Prevention, vaginal yeast infections remain highly common among women, reinforcing the need for accessible treatment options. Availability of both prescription and over-the-counter antifungal products strengthens patient access across urban and rural settings.

Innovation and regulatory oversight further shape the regional landscape. Approvals and monitoring by the U.S. Food and Drug Administration ensure safety and efficacy standards for new antifungal agents. Growing attention to antifungal resistance has encouraged adoption of advanced therapies in hospital environments. Additionally, expanding e-pharmacy services and telehealth consultations are improving discreet access to treatment, supporting steady market growth across the region.

Asia Pacific Yeast Infection Treatment Market Trends

Asia Pacific is witnessing steady expansion in the yeast infection treatment market due to rising healthcare awareness and improving medical infrastructure. Rapid urbanization and changing lifestyles have contributed to higher incidence of diabetes and weakened immunity in several countries. The World Health Organization highlights the growing burden of non-communicable diseases in the region, indirectly increasing fungal infection risks. Improved access to primary healthcare services and expanding pharmaceutical distribution networks are strengthening treatment availability.

Governments across countries such as India, China, and Southeast Asian nations are investing in public health programs and affordable medicine initiatives. Increasing acceptance of over-the-counter antifungal products has enhanced early intervention rates. Online pharmacy platforms are also expanding, allowing patients to purchase medications discreetly. Rising awareness campaigns related to women’s health and hygiene further contribute to demand, positioning Asia Pacific as a high-potential growth region for yeast infection therapies.

Market Competitive Landscape

The yeast infection treatment market is moderately competitive, with key pharmaceutical companies and generic drug manufacturers vying on product efficacy, safety, and accessibility. Leading players focus on expanding antifungal portfolios including azoles, echinocandins, and newer agents through clinical research and strategic launches. Over-the-counter brands compete on convenience and consumer awareness, while hospital-focused therapies emphasize advanced treatment for resistant and invasive infections. Growth strategies include geographic expansion, partnerships with healthcare providers, and broader digital distribution via e-pharmacies. Ongoing innovation to address resistance and improved patient compliance further shapes competitive dynamics across global markets.

Key Industry Developments:

- In February 2025, international medical societies released revised guidelines for the diagnosis and management of Candida infections.

- In March 2023, the U.S. Food and Drug Administration approved rezafungin (brand name Rezzayo), a new echinocandin antifungal, for treating invasive candidiasis and candidemia.

Companies Covered in Yeast Infection Treatment Market

- Abbott Laboratories

- Astellas Pharma Inc.

- Astra Zeneca

- Allergan

- Brundavan Laboratories Private Limited

- Bayer

- Corden Pharma

- Merck & Co., Inc.

- Novartis

- Pfizer Inc.

- Synmedic Laboratories

- Sanofi

- Others

Frequently Asked Questions

The yeast infection treatment market is estimated to be valued at US$ 6.5 Bn in 2026.

Rising fungal infection prevalence, increasing diabetes cases, antifungal resistance, improved diagnostics, and expanding over-the-counter treatment accessibility drive market growth.

The global market is expected to witness a CAGR of 5.2% between 2026 and 2033.

A few of the prominent players operating in the market are Abbott Laboratories, Astellas Pharma Inc., Astra Zeneca, Allergan, and Brundavan Laboratories Private Limited.

North America is the leading region in the global yeast infection treatment market.