- Hardware & Software IT Services

- Smart Door Lock Market

Smart Door Lock Market Size, Share, and Growth Forecast 2026 - 2033

Smart Door Lock Market by Product Type (Deadbolt Locks, Lever Handle Locks, Mortise Locks, Knob Locks, Padlock, Others), by Access Mechanism (Smartphone App, Keypad, Fingerprint, Others), by Technology, by End-user, and Regional Analysis for 2025 - 2032

Market Overview

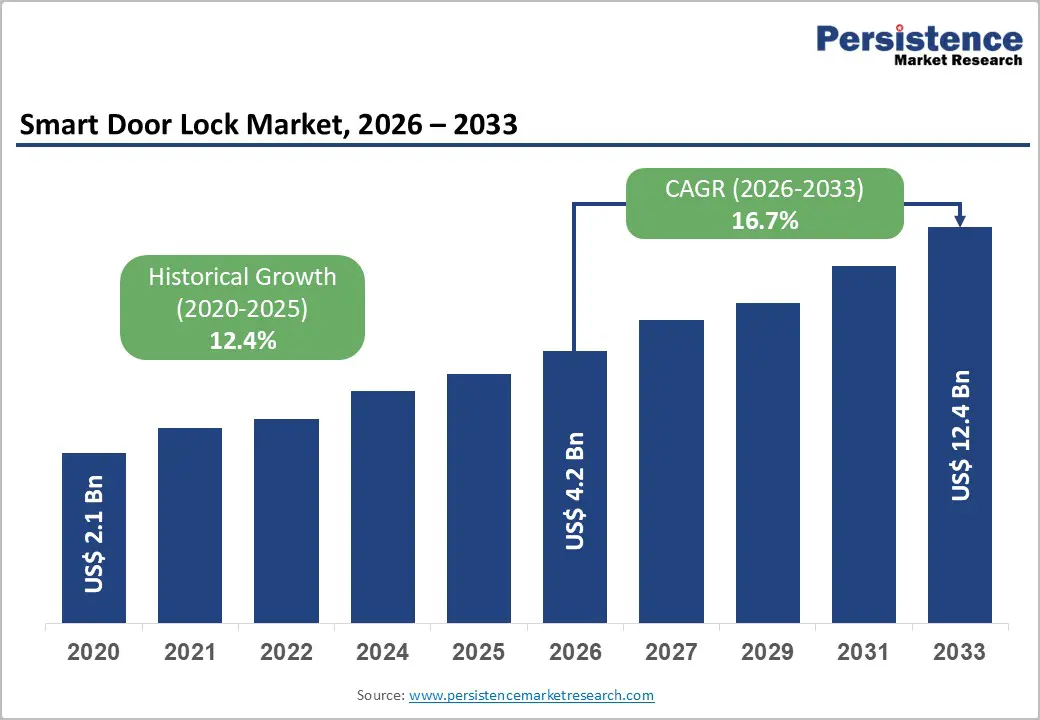

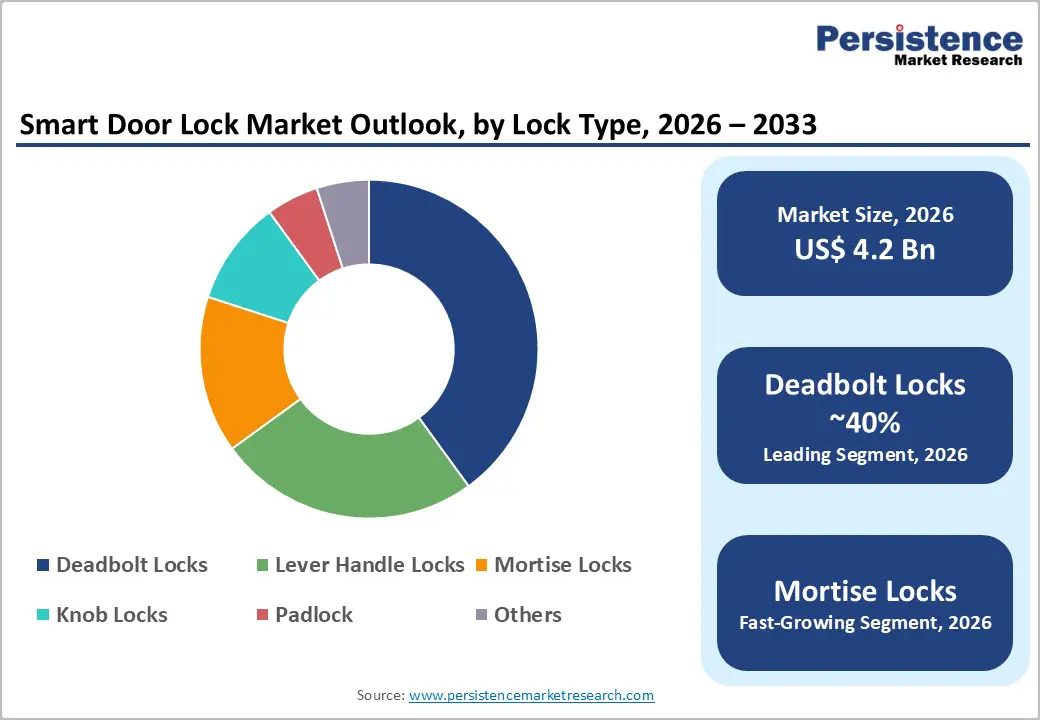

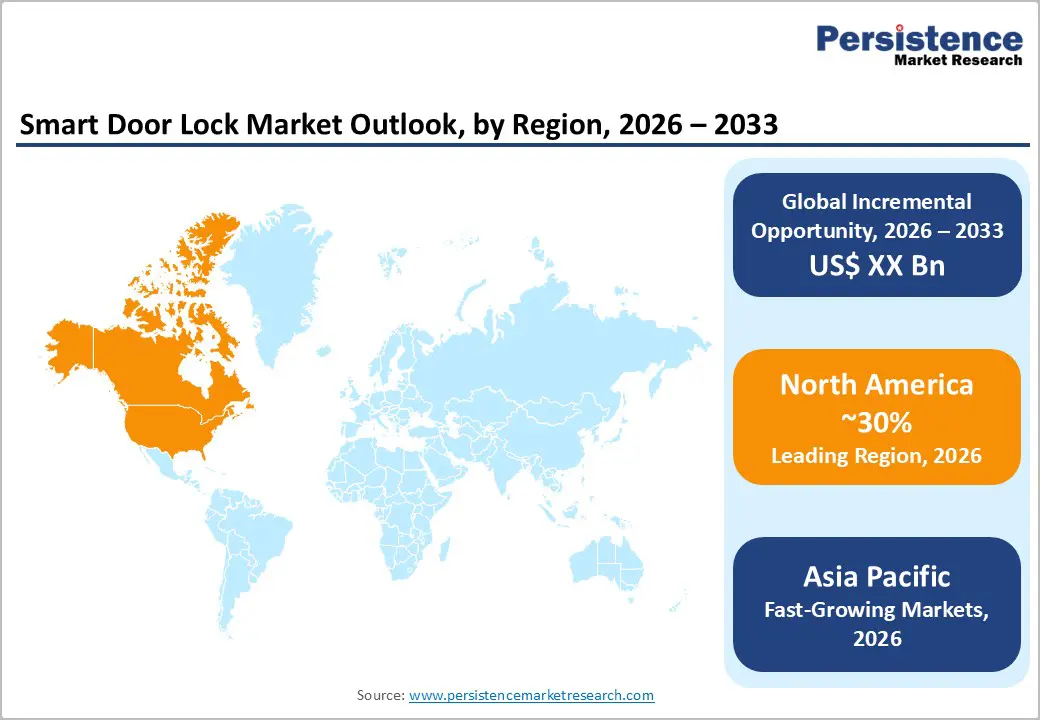

The global Smart Door Lock Market size was valued at US$ 4.2 Bn in 2026 and is projected to reach US$ 12.4 Bn by 2033, growing at a CAGR of 16.7% between 2026 and 2033. Growth is primarily driven by rising smart home penetration, heightened concerns about property crime, and increasing consumer preference for keyless, connected access solutions that integrate with existing security ecosystems. As smart home adoption in North America and Europe is forecast to exceed 170 million households, and smart home safety spending surpasses US$ 40 Bn globally, smart door locks are becoming a core node in broader connected security and automation platforms.

Key Market Highlights

- Leading region: North America leads the Smart Door Lock Market, driven by high smart home penetration, strong presence of security and tech players, and early adoption of Wi Fi and cloud managed locks across residential and commercial properties.

- Fastest growing region: Asia Pacific is the fastest growing region, supported by rapid urbanization, expanding middle class households, aggressive smart city programs, and strong local manufacturing that delivers affordable, feature rich smart locks.

- Dominant segment: Deadbolt Locks dominate the product mix with around 40% share, reflecting their central role on primary entry doors and compatibility with popular retrofit solutions from brands such as Yale, August, and Master Lock Company LLC.

- Fastest growing segment: Wi Fi and multi protocol smartphone app-based locks are the fastest growing segment, as consumers and enterprises demand always connected, remotely manageable access solutions tightly integrated with wider smart home and security ecosystems.

- Key market opportunity: Cloud managed, subscription based access platforms and integration of smart door locks with smart city, insurance, and property management services offer significant long term revenue growth beyond hardware sales.

|

Global Market Attributes |

Key Insights |

|---|---|

|

Water Heater Market Size (2026E) |

US$ 4.2 Bn |

|

Market Value Forecast (2033F) |

US$ 12.4 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

16.7% |

|

Historical Market Growth (CAGR 2020 to 2024) |

12.4% |

Market Dynamics

Market Growth Drivers

Proliferation of Smart Homes and Mobile First Lifestyles

Rapid expansion of smart homes is the single most important catalyst for the Smart Door Lock Market, with North America alone expected to reach about 78 million smart homes by 2024, representing more than 50% of all households. Similar penetration growth in Europe, projected to surpass 100 million smart homes, is pulling connected security devices including smart locks into the mainstream. Widespread smartphone ownership enables app based remote locking, guest access, and activity logs, while integration with voice assistants from major ecosystem providers such as Amazon, Google, and Apple has normalized voice controlled entry. As consumers increasingly bundle surveillance cameras, smart doorbells, and locks within a unified smart home or Smart Grid Market enabled environment, smart door locks become a critical hardware endpoint for digital access management and intrusion prevention.

Heightened Focus on Security, Access Management, and Convenience

Rising awareness of burglary, package theft, and unauthorized access is encouraging residential and commercial users to upgrade from mechanical locks to smart, auditable access control solutions. Smart door locks provide event logs, real time alerts, and temporary digital keys, enabling property managers, hospitality operators, and homeowners to manage access without distributing physical keys. In residential segments, consumer reports indicate strong interest in features like auto locking, one time access codes, and integration with smart doorbells and alarms, significantly improving perceived safety. Commercial properties especially co working spaces, retail, and hospitality benefit from centralized credential management and fast reprogramming of access rights, aligning with the broader digitalization of building operations and remote facility management.

Market Restraints

Cybersecurity, Privacy, and Reliability Concerns

Cybersecurity remains one of the most significant barriers to wider smart door lock adoption, as internet connected locks create a new attack surface for hackers and raise concerns about remote compromise and data privacy. Research projects in Europe, such as IoTAC, highlight that as smart home systems proliferate, households become increasingly exposed to cyber threats, necessitating robust hardware and software security for connected devices. High profile cases of vulnerabilities in poorly secured IoT products and worries about cloud based data storage can slow adoption among risk averse consumers and institutional buyers, increasing demand for independently certified, encrypted, and security hardened smart locks.

Higher Upfront Costs and Installation Complexity

Compared with conventional mechanical locks, smart door locks typically carry a substantial price premium, often costing several times more when including connectivity modules, bridges, and professional installation. Battery maintenance, compatibility with existing doors, and potential need for hubs or WiFi range extenders add complexity for less tech savvy users, especially in retrofit scenarios. In cost sensitive emerging markets, these factors can delay adoption, as many households and small businesses prioritize budget mechanical solutions over premium connected hardware, even when the long term benefits of smart access control are recognized.

Market Opportunities

Expansion of Cloud Managed Access and “Access as a Service” Models

Cloud managed access control and subscription based “access as a service” platforms offer major growth opportunities for smart door lock vendors targeting multi site commercial, hospitality, and institutional customers. Solutions from providers such as ASSA ABLOY, Salto Systems S.L., and Allegion plc allow facility managers to issue, revoke, and audit digital credentials across hundreds or thousands of doors from centralized dashboards, integrating locks, key cards, and mobile credentials. Growing adoption of hybrid work, short term rentals, and flexible retail formats increases the value of scalable, cloudy access systems that lower the cost and operational friction associated with mechanical rekeying. As Smart Door Lock Market platforms converge with identity and building management systems, recurring revenue from licenses, analytics, and support is expected to outpace pure hardware margins.

Convergence with Smart Cities, Smart Grid, and Insurance Linked Services

Smart door locks are poised to benefit from broader smart city and Smart Grid Market initiatives that promote secure, data rich, and energy efficient buildings. Integration of smart locks with municipal safe city platforms, neighborhood watch networks and verified delivery ecosystems can enable features such as secure in home parcel delivery and time bound access for public services. Insurers are also exploring partnerships were verified installation of certified smart security devices, including door locks, could reduce premiums due to lower theft risk. Over the long term, combining smart locks with occupancy data, energy management, and emergency response systems creates opportunities for differentiated offerings in high rise residential, mixed use developments, government facilities, and critical infrastructure.

Category wise Insights

Product Type Analysis

Deadbolt Locks represent the leading product type in the Smart Door Lock Market, accounting for an estimated 40% of global revenue, driven by their central role in primary entry doors and compatibility with retrofit friendly smart mechanisms. Studies on smart locks indicate that the deadbolt segment captured more than 42% share in recent years, as retrofit products like the August Wi Fi Smart Lock and Yale Assure series are specifically designed to augment existing deadbolts rather than replace entire locking systems. Consumers in North America and Europe often prefer deadbolt based solutions because they align with local door hardware standards and offer strong physical security. Lever handle, mortise, and knob smart locks are gaining traction in multifamily, hospitality, and European markets, but deadbolts remain the anchor segment for single family homes and many small businesses.

End user Analysis

The Residential segment is the dominant end user category, representing around 50% of global smart lock demand as homeowners increasingly adopt connected security devices. Residential users value keyless entry, integration with smart speakers, and the ability to monitor door status remotely, features highlighted in consumer testing and product reviews for brands such as Yale, August, Samsung Electronics Co., Ltd., and ADT smart home systems. Commercial applications including hospitality, healthcare, retail, and corporate offices collectively account for roughly 30% of demand, leveraging smart locks for multi user credential management, staff access scheduling, and audit trails. Government and institutional customers, together with industrial facilities, form a smaller but strategically important segment requiring high assurance, certified solutions integrated with wider physical security and identity management infrastructures.

Technology Analysis

Wi Fi enabled smart locks hold the largest share among communication technologies, estimated at around 45% of deployments, due to their ability to provide direct cloud connectivity and full remote control without additional hubs. Products such as the August Wi Fi Smart Lock emphasize built in Wi Fi, allowing users to lock, unlock, and monitor activity from anywhere, as well as integrate with voice assistants and third party smart home platforms. Bluetooth solutions remain popular for cost effective, proximity based access, particularly in entry level residential devices and some commercial settings, while Zigbee & Z Wave technologies are widely used in professionally installed smart home ecosystems where low power mesh networking across multiple devices is required. As Matter and next generation IoT standards roll out, multi protocol support and secure over the air updates are expected to become key differentiators across technology segments.

Access Mechanism Analysis

Smartphone App based access is emerging as the leading access mechanism, accounting for an estimated 40% of interactions across modern smart door lock deployments, reflecting near universal smartphone penetration and consumer comfort with app centric control. Vendors highlight remote operation, digital key sharing, and granular control over user permissions as primary benefits of app based access, which is now standard across most portfolios from ASSA ABLOY, Honeywell International Inc., dormakaba Group, and others. Keypad and Fingerprint access remain important, especially for multi user or high traffic environments where not all users can or will rely on smartphones, with biometric locks gaining rapid adoption in Asia due to familiarity with fingerprint authentication on mobile devices. Key fob and key card solutions are widely used in hospitality and corporate environments, while multi factor combinations (e.g., app + PIN + biometric) are increasingly deployed in higher security applications.

Regional Insights

North America Smart Door Lock Market Trends

In North America, the United States leads adoption of smart door locks, underpinned by high smart home penetration and a strong ecosystem of security and technology companies. By 2024, North America is expected to host about 78 million smart homes, equal to roughly 53% of all households, making it the most mature smart home market globally. This environment strongly supports uptake of connected locks integrated with smart doorbells, cameras, and alarm systems provided by vendors such as ADT, Amazon, Google Nest, and major residential security providers.

Regulatory frameworks around data privacy and cybersecurity, including state level laws and voluntary IoT security guidelines, are pushing manufacturers to adopt stronger encryption, secure boot, and regular firmware updates for smart locks and other connected devices. The innovation ecosystem features established access control players like ASSA ABLOY, Allegion plc, and dormakaba Group alongside consumer tech oriented brands and start ups.

Europe Smart Door Lock Market Trends

Europe is experiencing robust growth in smart door lock adoption, albeit from a lower penetration base than North America, as smart homes in the region are forecast to exceed 100 million by 2024 with penetration of more than 40% of households. Countries such as Germany, the U.K., France, and Spain are at the forefront of this expansion, driven by rising demand for integrated smart home solutions and the modernization of multi family housing and hospitality infrastructure. European consumers show strong interest in privacy preserving and security certified solutions, driving demand for products that meet stringent regional cyber security and data protection requirements.

The region benefits from homegrown leaders such as ASSA ABLOY (with brands like Yale and August), dormakaba Group, and Salto Systems S.L., which provide advanced electronic access control solutions spanning residential, commercial, and institutional applications. Ongoing regulatory harmonization around IoT security labeling and building standards is expected to further professionalize the market, favoring vendors that can demonstrate secure design, long term support, and interoperability across different smart home and building automation standards.

Asia Pacific Smart Door Lock Market Trends

Asia Pacific is the fastest growing regional market for smart door locks, supported by rapid urbanization, expanding middle classes, and dynamic smart city initiatives in China, Japan, South Korea, India, and ASEAN economies. The smart lock market in Asia Pacific is projected to grow at a CAGR above 24%, driven by high technology adoption rates, strong local manufacturing bases, and falling device prices. China accounts for the largest share in the region, benefiting from aggressive smart home marketing, extensive e commerce distribution, and strong domestic brands offering feature rich biometric and app controlled locks at competitive prices.

In Japan and South Korea, dense urban housing and tech savvy populations support early adoption of advanced features such as facial recognition, integrated video doorbells, and multi protocol connectivity. India and emerging ASEAN markets are witnessing rising adoption in mid to premium residential projects, gated communities, and commercial real estate, with brands like Samsung Electronics Co., Ltd., Lumi United Technology Co., Ltd., and local OEMs playing prominent roles.

Competitive Landscape

Market Structure Analysis

The Smart Door Lock Market is moderately consolidated, with global access control leaders such as ASSA ABLOY, Allegion plc, and dormakaba Group competing alongside diversified technology companies like Honeywell International Inc., Samsung Electronics Co., Ltd., and network specialists such as TP Link Systems Inc. Market leaders differentiate through broad portfolios covering deadbolt, mortise, and cylindrical formats; multi technology connectivity (Wi Fi, Bluetooth, Zigbee, Z Wave); and deep integration with smart home and professional security ecosystems.

Emerging trends include subscription based cloud access platforms, white label solutions for telecom and utility partners, and vertically targeted offerings for hospitality, co living, and enterprise access control. Continuous R&D investment focuses on enhanced cyber security, battery life optimization, and seamless user experiences across mobile and web interfaces.

Key Market Developments

- In June 2025, Eaton and Siemens Energy launched a strategic initiative to deliver modular, grid-independent power systems for data centers in North America. The joint solution integrates on-site generation and smart infrastructure to improve grid resilience and accelerate renewable integration.

- In June 2025, Minda collaborated with Toyodenso to produce advanced automotive switches for the Indian market. This partnership aims to deliver comprehensive solutions for two-wheelers and passenger vehicles, including design and manufacturing.

Companies Covered in Smart Door Lock Market

- ASSA ABLOY

- Honeywell International Inc.

- Allegion plc

- dormakaba Group

- Salto Systems, S.L.

- Hampton Products International Corp.

- TP-Link Systems Inc.

- Samsung Electronics Co., Ltd.

- Master Lock Company LLC

- Yale

- ADT

- Others Key Players

Frequently Asked Questions

The global Smart Door Lock Market is projected to reach approximately US$ 12.4 billion by 2033, increasing from about US$ 4.2 billion in 2026, at a forecast CAGR of 16.7% between 2026 and 2033.

Key demand drivers include rapid smart‑home proliferation, increasing concerns about property crime, widespread smartphone adoption, and growing preference for keyless, remotely manageable access integrated with connected security ecosystems and digital property‑management platforms.

Deadbolt Locks currently lead the market by product type, with about 4042% share, while Wi‑Fienabled and smartphone appcontrolled locks dominate on the technology and access side due to their remote connectivity and integration capabilities.

North America holds the largest regional share, supported by high smart‑home penetration, strong consumer purchasing power, and presence of major security and access‑control companies offering integrated smart lock solutions for residential and commercial customers.

Major players include ASSA ABLOY, Honeywell International Inc., Allegion plc, dormakaba Group, Salto Systems, S.L., TP‑Link Systems Inc., and Lumi United Technology Co., Ltd., complemented by regional and specialist brands.