- Home Care & Utilities

- Washing and Cleaning Products Market

Washing and Cleaning Products Market Size, Share, and Growth Forecast, 2026-2033

Washing and Cleaning Products Market by Product Family (Laundry & Fabric Care, Dishwashing Care, Surface Cleaning Products, Floor & Hard Surface Cleaners, Toilet & Bathroom Cleaners, Disinfectants & Hygiene Enhancers, Specialized Cleaning Products), Product Format (Liquids, Powders, Gels, Pods, Sprays, Wipes, Aerosols), End-Use (Residential, Commercial, Industrial), and Regional Forecast for 2026-2033

Washing and Cleaning Products Market Share and Trends Analysis

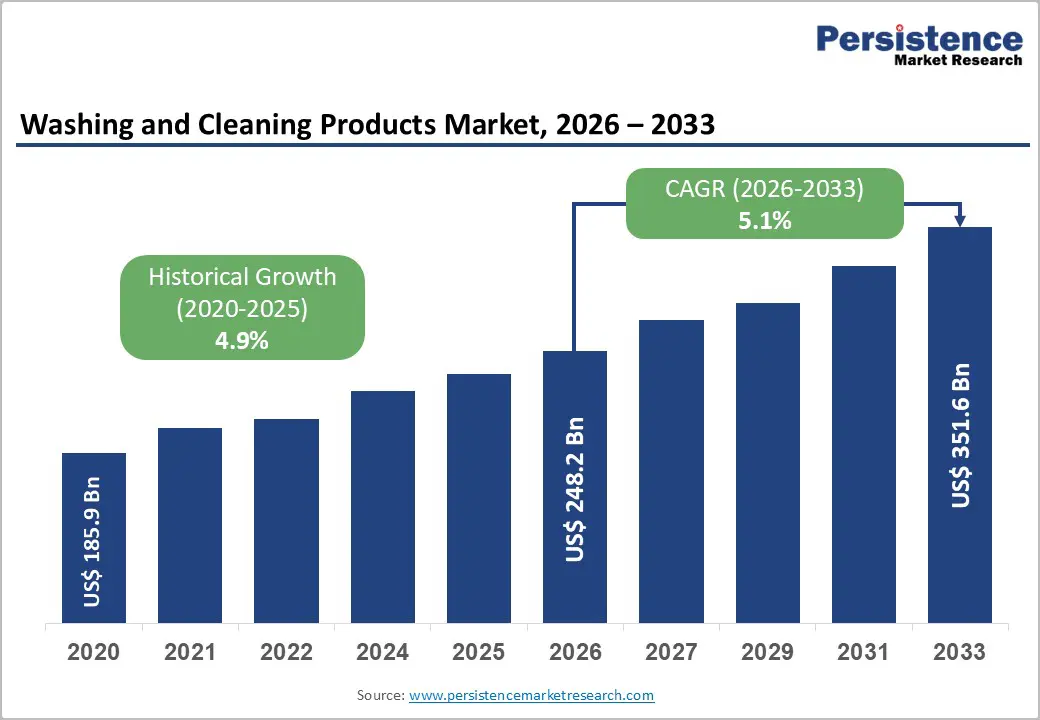

The global washing and cleaning products market is expected to grow from US$ 248.2 billion in 2026 to US$ 351.6 billion by 2033, at a CAGR of 5.1%. Growth is driven by rising hygiene awareness, urbanization, and increasing demand in both households and commercial settings. Governments are enforcing stricter sanitation standards, boosting institutional demand. Manufacturers are innovating with concentrated formulas, eco-friendly ingredients, and convenient formats like pods and wipes. Emphasis on performance, safety, and sustainability is shaping competitive strategies and premium pricing opportunities.

Key Industry Highlights

- Product Leadership: Laundry & fabric care is estimated to account for about 38% share in 2026, owing to high-frequency household and commercial usage, while disinfectants & hygiene enhancers are expected to grow the fastest through 2033, driven by institutional hygiene mandates.

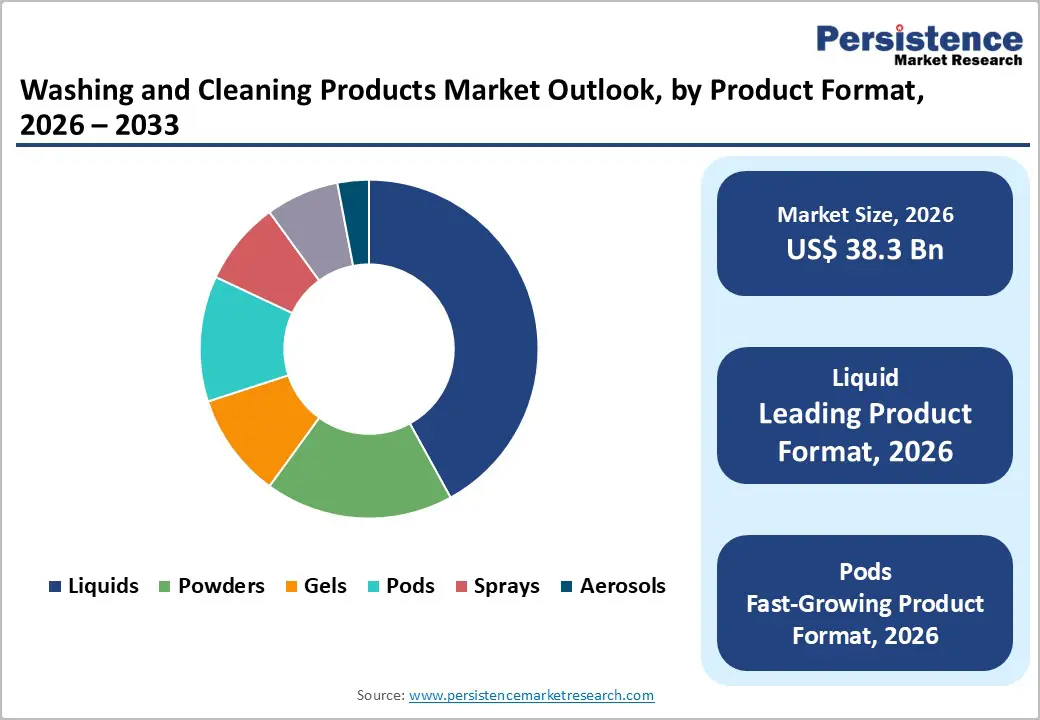

- Format Dynamics: Liquid formats are projected to dominate with around 42% share in 2026 due to versatility across applications, while pods are anticipated to expand the fastest at nearly 8% CAGR, aided by the extensive demand for convenience and reduced packaging waste.

- End-Use Split: Residential applications are likely to represent roughly 60% of demand in 2026, fueled by routine daily cleaning needs, while industrial and institutional segments are forecast to grow fastest at 6.4% CAGR, supported by healthcare and commercial hygiene compliance.

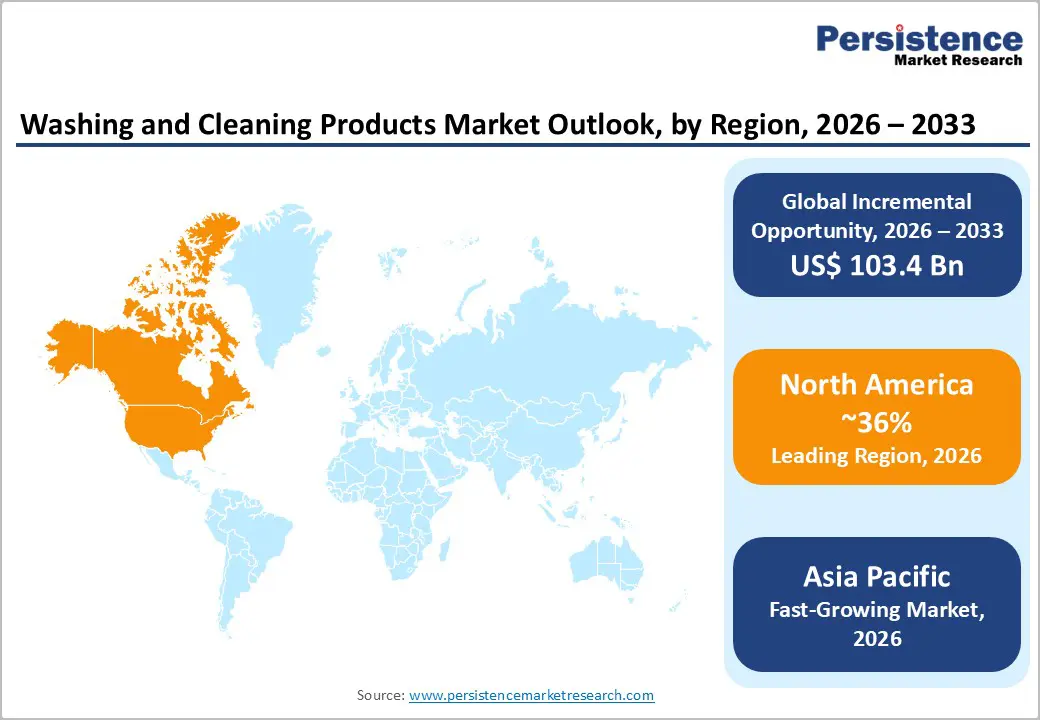

- Regional Performance: North America is expected to lead with an estimated36% share in 2026, backed by high per-capita consumption, whereas Asia Pacific is projected to be the fastest-growing market at 6.8% CAGR, driven by large-scale urbanization and sanitation initiatives.

- Competitive Focus: Competitive strategies are increasingly oriented toward sustainability-led innovation and expansion of professional and institutional cleaning portfolios, as companies seek to align with regulatory requirements and long-term demand visibility.

| Key Insights | Details |

|---|---|

|

Washing and Cleaning Products Market Size (2026E) |

US$ 248.2 Bn |

|

Market Value Forecast (2033F) |

US$ 351.6 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

5.1% |

|

Historical Market Growth (CAGR 2020 to 2025) |

4.9% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Hygiene Awareness and Smart Cleaning Technologies Drive Market Demand

Hygiene awareness has structurally increased following sustained public health campaigns led by organizations such as the World Health Organization (WHO), Centers for Disease Control and Prevention (CDC), and national sanitation programs. Government-backed initiatives promoting hand hygiene, surface sanitation, and safe food handling have translated into higher per-capita consumption of cleaning and disinfectant products. Effective household and institutional cleaning is recognized as a cornerstone of infection prevention strategies, reinforcing long-term demand across residential, healthcare, and public environments. This trend has sustained growth in disinfectants, surface cleaners, and hygiene enhancers, while creating stable demand even beyond temporary pandemic-driven spikes.

Rapid urbanization has reshaped household cleaning behavior and product preferences, with over 56% of the population currently residing in urban areas, a proportion projected to rise steadily through 2035. Urban households increasingly favor convenience-oriented products such as liquid detergents, pods, wipes, and sprays, driven by lifestyle constraints and efficiency needs. Technology innovations are reinforcing this trend. For example Samsung’s Bespoke AI Smart Laundry appliances optimize detergent dosing through fabric sensing and SmartThings integration, while DTGen’s AI-based dishware recognition demonstrates potential for automated, soil-level-adjusted detergent dispensing. These intelligent systems enhance cleaning performance, reduce waste, and elevate user convenience, boosting demand for premium laundry & fabric care products and ready-to-use surface cleaners.

Formulation & Regulatory Complexity Coupled with Supply Chain Constraints

The washing and cleaning products market is facing heightened formulation complexity and compliance pressures as regulators expand chemical safety and environmental standards. In 2025, the European Chemicals Agency (ECHA) updated proposals to restrict per- and polyfluoroalkyl substances (PFAS) across multiple sectors, potentially affecting surfactants and solvents used in cleaning formulations, with evaluations expected to conclude in 2026, increasing compliance planning costs for manufacturers. Similarly, expanded candidate lists for substances of very high concern under REACH require firms to manage additional hazards and disclosures, elevating operational burden and extending development timelines.

These regulatory pressures are compounded by supply chain constraints arising from the chemical industry slowdown. Weak demand in key end markets, overcapacity in basic chemicals, high energy costs, geopolitical tensions, and pricing volatility for critical raw materials such as surfactants, solvents, and specialty resins have reduced supply reliability and increased production costs. These factors make securing consistent, high-quality inputs more challenging, particularly for industrial and institutional cleaning products, and heighten margin pressures across the value chain, reinforcing this restraint as a significant structural market challenge.

Sustainable and Innovative Growth Opportunities in Emerging and Developed Markets

The washing and cleaning products market growth is increasingly shaped by the shift toward sustainable and bio-based products, driven by rising environmental awareness and evolving regulatory expectations. Consumers are gravitating toward plant-based surfactants, biodegradable formulas, and recyclable or refillable packaging formats that reduce environmental impact. For example, bio-enzyme detergents, concentrate refill pouches, and plastic-neutral packaging are gaining traction as eco-preferred alternatives in mature markets. This shift presents value-creation potential in premium laundry detergents, surface cleaners, and disinfectants, where environmentally conscious consumers demonstrate willingness to pay a price premium, encouraging manufacturers to enhance sustainability credentials across product portfolios.

Changing consumer dynamics in emerging markets and rural penetration offer substantial volume growth opportunities, fueled by rising disposable incomes, expanding retail distribution, and government-led sanitation initiatives that increase the adoption of branded cleaning products beyond urban centers. Technological innovation in product formats, such as water-soluble pods, compact concentrated liquids, smart dosing systems, and refill stations, further enhances convenience, dosing accuracy, and cost efficiency. These format advancements support margin expansion, strengthen brand loyalty, and enable manufacturers to serve both value-oriented and premium segments, creating long-term growth prospects across diverse consumer groups and geographic markets.

Category-wise Analysis

Product Family Insights

Laundry & fabric care is estimated to lead with approximately 38% of the washing and cleaning products market revenue share in 2026, reflecting its broad applicability and frequent use across households and commercial laundries. Hindustan Unilever, for instance, introduced a premium liquid detergent variant designed for shorter washes and convenience, capturing consumer attention in both urban and semi-urban markets. Henkel expanded its Persil portfolio in North America with liquid and pod innovations emphasizing sustainability through reduced water usage and recycled packaging. The combination of convenience, efficiency, and eco-friendly attributes reinforces consistent demand. Recurring consumption patterns and brand loyalty further secure stable revenue streams, while innovations in concentrated formulas and refillable packaging enhance profit margins and market resilience.

Disinfectants & Hygiene Enhancers are projected to be the fastest-growing product family with an estimated CAGR of 7.2% through 2033, supported by rising hygiene awareness and institutional sanitation mandates. Unilever’s Cif Infinite Clean introduced probiotic surface cleaners to the market, providing lasting germ control for residential consumers. Reckitt Benckiser strengthened Dettol and Lysol portfolios with disinfectants demonstrating improved antimicrobial efficacy, particularly in healthcare and public infrastructure settings. Household and institutional uptake of disinfectant solutions remains strong due to heightened sanitation awareness. Expansion into premium and specialized formulas supports growth in both developed and emerging markets. Manufacturers are leveraging innovation to meet evolving consumer expectations and regulatory compliance, securing long-term category expansion.

Product Format Insights

Liquid formats are estimated to dominate with roughly 42% revenue share in 2026, driven by versatility across laundry, dishwashing, and surface cleaning applications. Church & Dwight Co. expanded its sustainability initiatives by enhancing liquid laundry detergents and optimizing packaging to lower plastic use and emissions, reflecting innovation within the liquid segment. These liquid formats support flexible formulations across household and institutional cleaning needs and enable concentrated varieties that improve performance while reducing water and packaging waste. Liquid formats continue to benefit from broad consumer familiarity and ease of use, reinforcing strong repeat purchase behavior. Additionally, liquid products accommodate a wide range of performance and eco friendly claims that appeal to both value oriented and premium buyers. The versatility and adaptability of liquid formats sustain their leadership amidst diverse product portfolios.

Pods are expected to grow fastest at an approximate 2026-2033 CAGR of 8%, driven by convenience, precise dosing, and sustainability advantages. Church & Dwight’s ARM & HAMMER Power Sheets laundry detergent expanded into the retail market, representing a move toward dry, convenient, and lower waste formats that reduce traditional liquid packaging. This aligns with broader industry efforts to innovate formats that are easy to store, ship, and use, meeting rising consumer demand for convenience and sustainability. Tablets, pods, and sheets also minimize dosing errors and significantly reduce packaging volume, which appeals to both environmentally conscious consumers and institutional buyers focused on operational efficiency. Adoption is growing in developed markets and expanding to urban centers in emerging regions, reinforcing both premiumization and environmental positioning.

End Use Insights

Residential and household applications are projected to hold an estimated 60% revenue share in 2026, propelled by consistent usage across kitchens, bathrooms, and laundry rooms. Clorox Professional announced a supply agreement with Vizient to provide a range of cleaning and disinfecting products to healthcare and commercial facilities, highlighting how residential style consumer brands are also extending into professional hygiene channels and raising overall category visibility. Meanwhile, consumer cleaning habits continue to favor branded, multi purpose formats that combine surface, laundry, and disinfectant functions, enhancing convenience for households. Recurring usage and rising expectations for convenience and sustainability support ongoing residential demand. Product innovations that emphasize eco friendly ingredients and concentrated formulations further align with evolving consumer preferences, solidifying this segment’s dominant position.

Industrial and institutional applications are expected to grow at about 6.4% CAGR between 2026 and 2033, driven by hygiene compliance requirements and bulk procurement in sectors such as healthcare, hospitality, and manufacturing. Ecolab launched its ReadyDose™ tablet based cleaning program designed to simplify and standardize institutional cleaning routines, reducing storage space and chemical waste through compact tablet delivery systems. These professional grade solutions enhance dosing accuracy and operational efficiency for facility managers. Demand for targeted, high performance formulations that deliver consistent cleaning outcomes and support hygiene protocols continues to rise. Long term contracts with facility networks and digital integration of dosing systems strengthen supplier positioning. Investments in institutional focused innovations reflect deeper market penetration and sustained growth in this application segment.

Regional Insights

North America Washing and Cleaning Products Market Trends

North America is expected to be the leading regional market for washing and cleaning products, estimated to hold 34% of the global market share in 2026, owing to strong per capita consumption, mature retail channels, and high adoption of premium and sustainable cleaning products. Clorox announced its planned acquisition of GOJO Industries, the maker of Purell hand sanitizer, a strategic move that underscores continued investment in hygiene oriented cleaning solutions within the region. This development reflects how companies are consolidating hygiene and cleaning portfolios to meet elevated sanitation expectations across households and institutions.

Regulatory enforcement by the U.S. Environmental Protection Agency (EPA) and the Food and Drug Administration (FDA) continues to shape product innovation, encouraging safety compliant and eco friendly formulations. Institutional demand remains robust, especially within healthcare, hospitality, and commercial cleaning sectors that require high efficacy disinfectants and specialized sanitizing systems. Brand loyalty and frequent product upgrades through concentrated liquids, multifunctional sprays, and smart dispensing solutions sustain recurring demand. Investments in digital engagement, omnichannel distribution, and differentiated product lines strengthen long term growth prospects. Strategic partnerships, acquisitions, and portfolio expansions further solidify North America’s leadership position.

Europe Washing and Cleaning Products Market Trends

Europe represents a mature and innovation-focused market for washing and cleaning products, with Germany, the U.K., France, and Spain leading regional demand. Sustainability and regulatory alignment are key competitive drivers, underpinned by harmonized European Union (EU) standards around chemical safety and biodegradability. Manufacturers are actively reformulating products to meet evolving requirements and consumer preferences for high-performance, environmentally responsible cleaners that minimize harsh chemicals and reduce waste. Product innovation emphasizes multifunctional and concentrated formats that enhance convenience and efficiency for residential and institutional users alike.

The China Clean Expo in Shanghai attracted a growing contingent of European cleaning brands and equipment providers, such as Nilfisk and Comet, which showcased advanced cleaning technologies and sustainable solutions before expanding distribution back into their home markets. This reflects increasing cross-regional engagement and adoption of innovation trends that influence European product offerings. As Southern and Eastern European economies experience rising urbanization and disposable incomes, demand for branded cleaning products continues to grow steadily. Combined with strong retail presence and enhanced e-commerce access, Europe balances mature consumption with targeted growth opportunities in premium and eco-configured product segments.

Asia Pacific Washing and Cleaning Products Market Trends

Asia Pacific is poised to be the fastest-growing regional market, projected to expand at approximately 6.8% CAGR through 2033, supported by rapid urbanization, rising incomes, and expanding consumption in China, India, Japan, and ASEAN markets. Demand is strong across both household and institutional cleaning products, driven by increasing hygiene awareness and the adoption of branded, high-performance solutions. Multi-sector growth is evident in China’s professional cleaning ecosystem, where the China Clean Expo 2026 is set to gather nearly 500 exhibitors showcasing the latest cleaning technologies and sustainable solutions, reflecting robust industry momentum and innovation adoption.

Local manufacturers are advancing product development and supply chain capabilities to meet growing demand. For example, Shanghai Easylife International Group showcased a new range of eco-friendly wipes at the 2025 East China Fair, featuring biodegradable materials and antibacterial formulations tailored to sustainability-conscious consumers and export markets. Government sanitation campaigns, expanding rural retail access, and formulations adapted to local usage conditions further support market growth. Investments in digital retail platforms, distribution infrastructure, and cross-border trade participation accelerate adoption and reinforce Asia Pacific’s position as the fastest-developing regional market.

Competitive Landscape

The global washing and cleaning products market structure is moderately consolidated, with Procter & Gamble, Unilever, Henkel, Clorox, and Ecolab at the forefront on account of their strong brand names and reach, extensive distribution networks, and deep consumer insights. These players invest in R&D, sustainable formulations, smart dispensing, and multifunctional products to meet household and institutional needs. Their innovation and scale provide a competitive edge across premium and mass-market segments. Continuous product launches and portfolio expansions help maintain loyalty and revenue growth.

Regional and niche players, such as Church & Dwight, Reckitt, and Shanghai Easylife International Group, focus on eco-friendly, tablet/pod, and professional cleaning solutions to strengthen local and specialized market presence. Barriers such as chemical regulations, compliance costs, and complex supply chains limit new entrants. Digitalization and e-commerce enable smaller companies to compete, while strategic acquisitions and partnerships drive gradual market consolidation. Niche players often lead in specialized products, driving differentiation and adoption.

Key Industry Developments

- In January 2026, Clorox announced a definitive agreement to acquire GOJO Industries, maker of Purell, in a US$ 2.25 billion all-cash deal, expected to close by the end of fiscal 2026. The acquisition strengthens Clorox’s Health & Wellness segment, particularly in the professional B2B channel, which accounts for over 80% of GOJO’s US$ 800 million annual sales.

- In December 2025, Reckitt Benckiser finalized the sale of its Essential Home portfolio, including Air Wick, Cillit Bang, Calgon, and Woolite, to Advent International for up to US$ 4.8 billion. The deal consolidates key household cleaning brands under a private equity-owned structure while also allowing Reckitt to streamline operations and allocate resources toward high-growth hygiene and wellness segments.

- In July 2025, Hindustan Unilever expanded its laundry portfolio with the launch of Surf Excel liquid detergent targeting the premium segment, aiming to capture evolving consumer preferences for superior cleaning performance. The move reflects HUL’s strategic focus on product premiumization and category growth in India’s fast-growing laundry care market.

Companies Covered in Washing and Cleaning Products Market

- Procter & Gamble Co.

- Unilever plc

- Reckitt

- Henkel AG & Co. KGaA

- Colgate-Palmolive Company

- SC Johnson

- Church & Dwight Co., Inc.

- Kao Corporation

- Clorox Company

- LG Household & Health Care

- Godrej Consumer Products

- Seventh Generation

- BlueWonder

Frequently Asked Questions

The global washing and cleaning products market is projected to reach US$ 248.2 billion in 2026.

Rising hygiene awareness, urbanization, growth in dual-income households, and increasing institutional and commercial cleaning demand are primary market drivers.

The market is poised to witness a CAGR of 5.1% from 2026 to 2033.

Opportunities include the shift toward sustainable and bio-based products, expansion in emerging markets, innovative product formats (pods, tablets, smart dispensers), and institutional procurement.

Procter & Gamble, Unilever, Henkel, Clorox, Ecolab, Church & Dwight, Reckitt, and Shanghai Easylife International Group are some of the leading companies in the market.