- Medical Devices

- Vitamin D Home Testing Market

Vitamin D Home Testing Market Size, Share, and Growth Forecast 2026 – 2033

Vitamin D Home Testing Market by Product Type (Strips, Cassettes, Digital Kits), Technology (Immunoassay, Chromatography, Other), Distribution Channel (Hospital Pharmacies, Online Pharmacies, Retail Pharmacies) and by Regional Analysis 2026 - 2033

Vitamin D Home Testing Market Size and Share Analysis

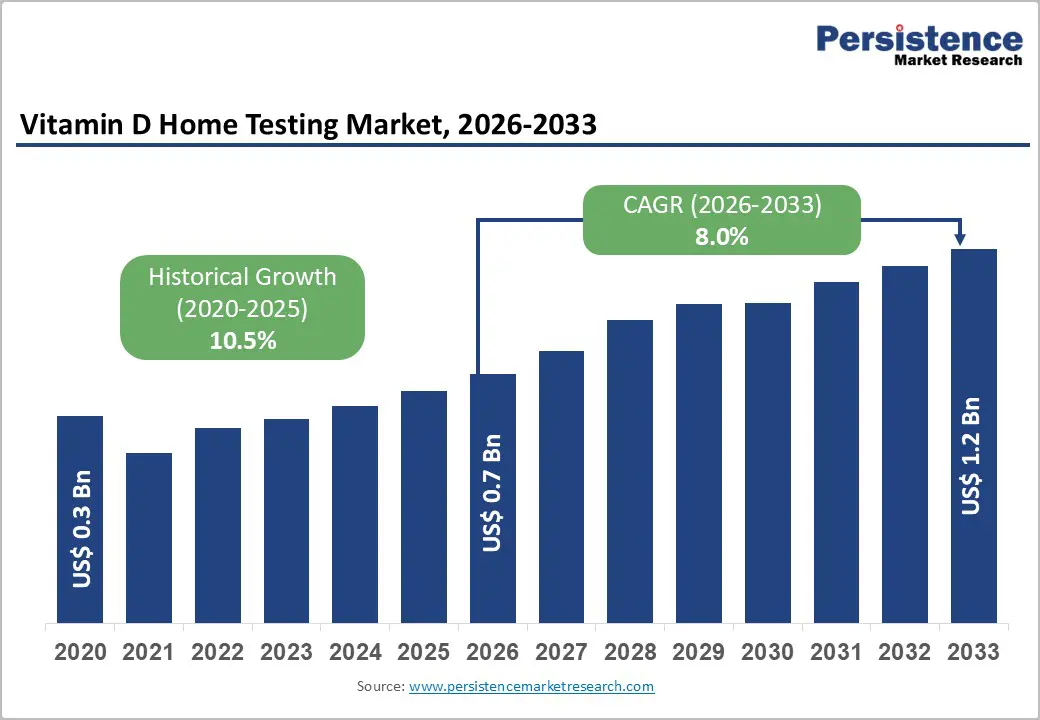

The global vitamin D home testing market size is likely to be valued at US$0.7 billion in 2026 and is projected to reach US$1.2 billion by 2033, registering a CAGR of 8.0% during the forecast period 2026-2033. The global vitamin D home testing market has emerged as an important segment within the global diagnostics industry, fueled by growing awareness of the benefits of maintaining sufficient Vitamin D levels. Timely detection plays a critical role in preventing complications, improving patient outcomes, and, in some cases, enabling curative interventions. The integration of digital health platforms and mobile applications with itamin D home testing services marks a major step forward in personalized healthcare, offering users greater convenience and control. Market prospects remain strong, with steady expansion expected in the coming years. Key drivers include the rising prevalence of vitamin D deficiency worldwide, supportive government initiatives promoting preventive health screenings, and the increasing acceptance of at-home diagnostic solutions. Together, these factors are positioning vitamin D home testing as a rapidly growing area within the broader diagnostics landscape.

Key Industry Highlights:

- Dominant Product Type: Cassettes dominate the product segment with approximately 35% market share, attributed to ease of use, accuracy, and regulatory approvals

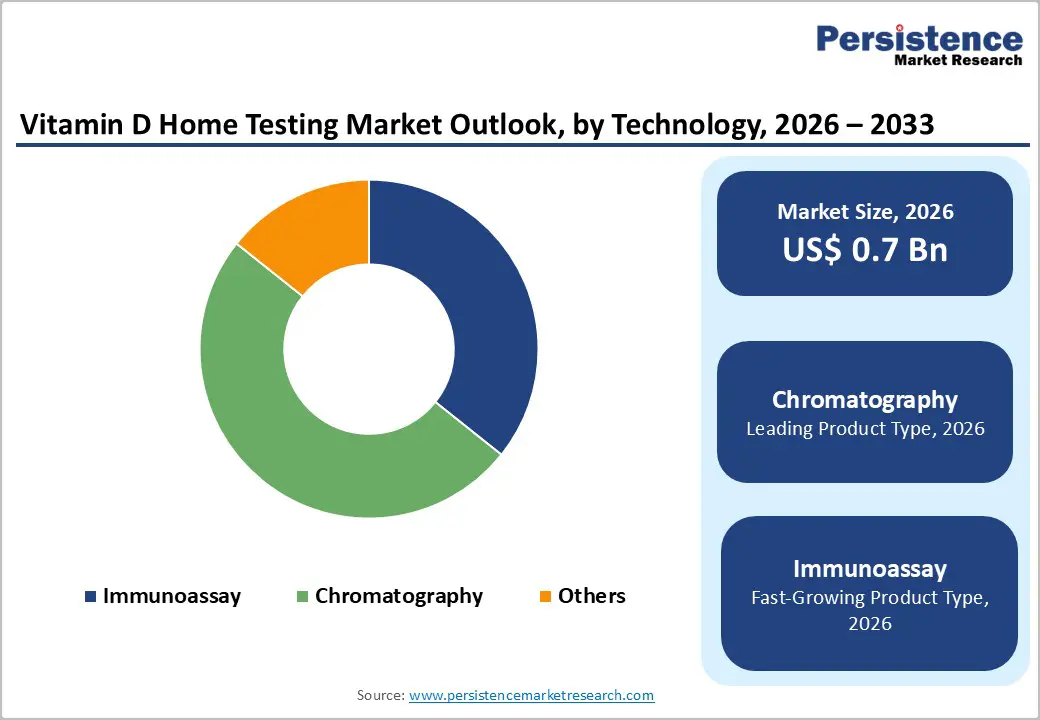

- Fastest Growing Technology: Immunoassay is the fastest growing technology for vitamin D home testing due to convenience, affordability, and rapid results

- Emerging Distribution Channel: E-commerce and online pharmacies are the fastest growing segment. Platforms like Amazon, Alibaba Health, and 1mg are expanding access, offering doorstep delivery and subscription models. This digital shift enhances convenience, affordability, and consumer reach, driving rapid adoption across global preventive healthcare markets

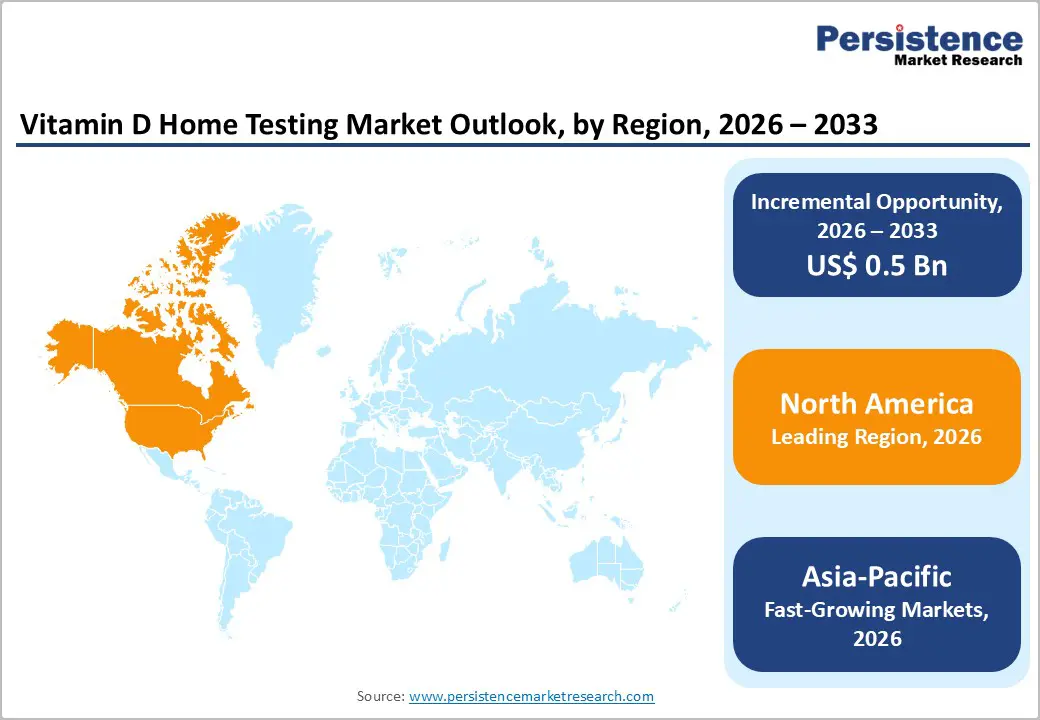

- Leading Region: North America dominates the global vitamin D home testing market with more than 30% of total market share, due to high prevalence of vitamin D deficiency, advanced healthcare infrastructure and affirmative reimbursement policies

- Key Opportunity: Supportive government initiatives, preventive healthcare adoption, and demand for rapid, convenient diagnostics create strong growth potential, positioning home kits as a vital segment of personalized healthcare.

| Key Insights | Details |

|---|---|

| Global Vitamin D Home Testing Market Size(2026E) | US$0.7 Bn |

| Market Value Forecast (2033F) | US$1.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 8.0% |

| Historical Market Growth (CAGR 2020 to 2025) | 10.5% |

Market Dynamics

Drivers – Increased demand for convenient diagnostics

The rising demand for convenient diagnostics is a major force propelling the at-home vitamin D testing market. Consumers today are increasingly focused on preventive healthcare and proactive monitoring of their nutritional status. Vitamin D deficiency, which is linked to weakened immunity, bone disorders, and chronic illnesses, has become a global concern. Traditionally, testing required visits to clinics or laboratories, which could be time-consuming and costly. Home testing kits now offer a simple alternative, allowing individuals to collect samples through finger-prick methods and either obtain rapid results instantly or send them to labs for analysis.

This convenience empowers people to monitor their health regularly without disrupting daily routines. The integration of digital health platforms and mobile apps further enhances accessibility, enabling users to track results, receive personalized recommendations, and share data with healthcare providers. E-commerce platforms and online pharmacies have also expanded availability, making these kits easy to purchase and use. Governments and health organizations are encouraging early detection and preventive screenings, which adds momentum to adoption. As awareness grows, the preference for quick, reliable, and user friendly diagnostics continues to drive the expansion of the Vitamin D home testing market, positioning it as a vital segment of modern healthcare.

Technological advances and integration with digital health apps are boosting the adoption

Advnacements in rapid finger prick Vitamin D kits have transformed the way individuals monitor their health, making testing more accessible and user-friendly. Finger-prick kits allow users to collect a small blood sample at home with minimal discomfort. Rapid immunoassay technology enables results within minutes, eliminating the need for clinical visits. For example, companies like LetsGetChecked and Everlywell provide home kits where users prick their finger, place drops of blood on a test card, and either receive instant results or mail the sample for lab analysis.

Integration with digital health apps has further enhanced usability. Many kits now sync with mobile platforms, allowing users to track Vitamin D levels over time, receive personalized recommendations, and share data with healthcare providers. Apps such as Thriva in the UK and myLAB Box in the US provide dashboards that interpret results and suggest lifestyle or dietary changes. This digital connectivity empowers individuals to take proactive steps in managing deficiency. Combined, these innovations have democratized Vitamin D testing, making it faster, more convenient, and aligned with the growing trend of personalized, preventive healthcare.

Restraints – Accuracy concerns and regulatory barriers to slow down the usage

Rapid finger prick Vitamin D kits are often met with skepticism due to concerns about precision, as their results can differ from laboratory assays. Research indicates that 20–25% of home test outcomes deviate notably from standardized lab values, creating uncertainty among healthcare providers. Market growth is further slowed by regulatory hurdles, with approvals from bodies like the FDA in the U.S. or CE in Europe typically requiring 12–24 months. In emerging regions, inconsistent regulatory standards add complexity to product entry. Moreover, differences in kit quality across manufacturers weaken consumer trust, posing another challenge to widespread adoption.

Opportunities

Expansion of E-commerce and Online Pharmacies

Digital connectivity and online distribution are transforming the Vitamin D home testing market by making diagnostics more convenient, personalized, and widely accessible. The integration of mobile apps and digital health platforms allows users to track their Vitamin D levels over time, receive tailored recommendations, and share results directly with healthcare providers. This connectivity empowers individuals to take proactive steps in managing deficiencies and supports the broader shift toward preventive healthcare. At the same time, the rise of e-commerce and online pharmacies has lowered barriers to access, enabling consumers to purchase test kits easily from platforms like Amazon, 1mg, or company websites. Subscription models and doorstep delivery further enhance convenience, particularly for tech savvy and health-conscious populations. Together, these trends are reshaping consumer expectations, positioning Vitamin D home testing as a vital tool in modern healthcare by combining digital innovation with broad distribution networks to drive adoption and growth.

Category-wise Analysis

Product Type Insights

Cassette Segment to Account for the Most Significant Share

Cassette based kits are dominating over strip formats due to their ease of use, accuracy, and wider regulatory acceptance. Strips, while cost-effective, often require more careful handling and interpretation, which can lead to user errors. Cassettes, on the other hand, are designed with clear sample wells and result windows, making them more user friendly for consumers who may not have medical training. This design reduces contamination risks and enhances reliability, which is crucial for building trust in home diagnostics. Regulatory approvals also favor cassette formats, as many CE marked and FDA-cleared Vitamin D kits are cassette-based. This has boosted adoption in regions like North America and Europe, where compliance and safety standards are strict. Companies such as Everlywell (U.S.), Thriva (U.K.), and Cerascreen (Germany) primarily distribute cassette-style kits, reinforcing their market dominance.

Cassette style kits, particularly those utilizing blood spot sampling or rapid immunoassay methods, represent the fastest expanding segment of the market. In contrast, strip formats are still largely confined to laboratory and research applications, with limited uptake among everyday consumers. The widespread dominance of cassettes stems from their blend of user-friendly design, reliable accuracy, and strong regulatory approval, making them the preferred option for at-home Vitamin D testing across global markets.

Technology Insights

Immunoassay Technology is enabling faster and user-friendly diagnostics

Recent advances in lateral flow immunoassay (LFIA) technology have made finger prick Vitamin D kits more reliable, delivering results within minutes compared to traditional lab assays that take days. These kits use microfluidic channels and improved antibody sensitivity to detect 25-hydroxy Vitamin D levels with greater precision. For example, companies like Accurex Biomedical in India and Boditech Med in South Korea have introduced rapid chromatographic kits that provide near instant readings at home. These innovations allow results to be generated within minutes, offering convenience and accessibility for users at home. Enhanced accuracy and simplified sample collection have boosted consumer confidence, while integration with digital health apps enables tracking and personalized recommendations. Advancements in LFIA technology are thus anticipated to transform vitamin D home testing, making it quicker, more reliable, and easier for users.

Regional Insights

North America Vitamin D Home Testing Market Trends

North America is expected to account for a significant share of the vitamin D Home Testing market due to a combination of demographic, healthcare, and socioeconomic factors. The region has a. In the U.S. and Canada, several factors are driving the growth of the vitamin D home testing market, reflecting broader trends in preventive healthcare and consumer convenience. One of the strongest drivers is the high prevalence of vitamin D deficiency. Studies indicate that nearly 35% of adults in the U.S. and 30% in Canada have insufficient vitamin D levels, often linked to limited sun exposure, dietary gaps, and lifestyle changes. This has created strong demand for accessible testing solutions.

Rapid testing for vitamin D deficiency in North America is driven by high prevalence rates, with studies showing 30–35% of adults have insufficient levels. Rising awareness of vitamin D’s role in immunity, bone health, and chronic disease prevention fuels demand for convenient diagnostics. Preventive healthcare trends encourage individuals to monitor nutrient status proactively, while technological advances in finger prick kits and digital health integration make testing faster and user-friendly. Expanding e-commerce and online pharmacy channels further improve accessibility. Together, these factors position rapid vitamin D testing as a key tool in personalized and preventive healthcare across the region.

Europe Vitamin D Home Testing Market Trends

In the U.K., Germany, France, and other European countries, vitamin D deficiency is widespread due to limited sunlight exposure, especially during long winters. Studies suggest that 40–60% of adults across Europe have insufficient vitamin D levels, creating strong demand for convenient diagnostics. Preventive healthcare trends are accelerating adoption, as individuals increasingly monitor nutrient levels to reduce risks of osteoporosis, immune disorders, and chronic diseases. Rapid finger prick kits and home testing solutions align with this shift, offering quick results without the need for clinical visits. Companies such as Thriva (U.K.) and Cerascreen (Germany) provide kits integrated with digital health platforms, enabling users to track results, receive personalized recommendations, and share data with healthcare providers.

E-commerce and online pharmacies are playing a pivotal role in expanding access to vitamin D home testing kits across Europe. Platforms such as Amazon EU and DoctiPharma in France make these kits widely available, reducing barriers for consumers and encouraging adoption. At the same time, regulatory support for preventive diagnostics across the EU strengthens trust in home testing solutions, ensuring quality and safety standards. Growing investment in personalized healthcare, coupled with rising consumer awareness of vitamin D deficiency, further accelerates demand. Together, these factors are driving steady market growth, with innovation and digital connectivity reshaping preventive healthcare across Europe.

Asia Pacific Vitamin D Home Testing Market Trends

In Asian countries, multiple factors are fuelling the rise of rapid and vitamin D home testing. Deficiency rates remain alarmingly high, with research indicating that 70–90% of people in South Asia and 40–60% in East Asia lack adequate vitamin D due to limited sunlight, urban living, and dietary insufficiencies. Growing awareness of vitamin D’s importance for immunity, bone strength, and chronic disease prevention has boosted demand for easy-to-use diagnostics. Preventive healthcare practices, especially in India, China, and Southeast Asia, are encouraging individuals to monitor their nutrient levels regularly. Advances in finger-prick testing technology and integration with mobile health apps have enhanced accessibility and convenience. Meanwhile, e-commerce platforms such as Alibaba Health in China and 1mg in India are expanding distribution channels, while government programs promoting early detection further support adoption. Collectively, these drivers are positioning rapid and vitamin D home testing as a key component of personalized healthcare across Asia.

Competitive Landscape

The rapid home vitamin D testing kit market is becoming increasingly competitive as demand for accessible, preventive healthcare grows. Global diagnostic leaders, regional biotech firms, and emerging startups are all striving to capture market share. Established companies rely on strong research capabilities and regulatory approvals to guarantee accuracy, while newer entrants emphasize affordability and speed to appeal to cost-conscious consumers. The focus is on developing kits that provide quick, reliable results through simple finger-prick samples. The key challenge remains balancing convenience with precision, as consumer confidence hinges on accuracy. Overall, the market is highly fragmented, with innovation, pricing strategies, and accessibility shaping competitive dynamics.

Key Market Developments:

- In March 2025, Polaris DX, the smart-tech diagnostics company, is launching Igloo Pro, a smart low-cost universal analysis platform, which can measure the level of markers such as vitamin D, Ferritin (iron deficiency) and CRP (inflammation), for dentists and other healthcare professionals, ushering in a new era for rapid point-of-care testing (POCT).

- In April 2022, Boditech Med obtained the regulatory nod for ichorma Vitamin D Neo, a diagnostic device that can detect vitamin D deficiency in blood in 12 minutes.

- In 2022, The Quiq kit manufactured by Santa Clara Wellness Pvt. Ltd. was first rolled out in Indian market on digital health platforms like 1mg and Amazon India, targeting consumers who wanted affordable, rapid, and home-based vitamin D Home Testing without visiting diagnostic labs.

Companies Covered in Vitamin D Home Testing Market

- Everlywell

- myLAB Box

- Getein Biotech, Inc.

- Hysen Biotech Inc

- Spark Diagnostics

- Accurex

- Vitrosens Biotechnology

- Autobio Diagnostics

- PRIMA Lab SA

- BTNX, Inc.

- Xiamen Wiz Biotech Co., Ltd

- BIOHIT HealthCare Ltd

- Other

Frequently Asked Questions

The global vitamin D home testing market is projected to reach US$1.2 Bn by 2033, growing at a CAGR of 8.0% from 2026 to 2033.

The primary factors driving demand for vitamin D home testing include high vitamin D deficiency prevalence, and strong consumer awareness for preventive healthcare.

Home-based vitamin D tests are emerging as a fast-growing segment because they combine convenience, affordability, and preventive health awareness, shifting the market toward self-testing kits.

North America leads the global vitamin D home testing market, holding the largest share, approximately 70% of the regional market value, due to advanced healthcare infrastructure, and widespread e‑commerce distribution channels.

An emerging opportunity in at‑home vitamin D testing lies in digital integration and subscription models.

Some of the key players operating in the market are Everlywell, myLAB Box, Thriva, Accurex Biomedical, and Boditech Med.