- Nutraceuticals & Functional Foods

- Vitamin C Ingredients Market

Vitamin C Ingredients Market Size, Trends, Share, Growth, and Regional Forecast, 2026 to 2033

Vitamin C Ingredients Market by Product Type (Ascorbic Acid, Sodium Ascorbate, Calcium Ascorbate, Coated Vitamin C, Others), by Source (Natural, Synthetic), by End Use (Pharmaceuticals & Nutraceuticals, Food & Beverages, Cosmetics & Personal Care, Animal Feed & Nutrition, Functional Foods, Others), and by Regional Analysis, 2026 - 2033

Vitamin C Ingredients Market Share and Trends Analysis

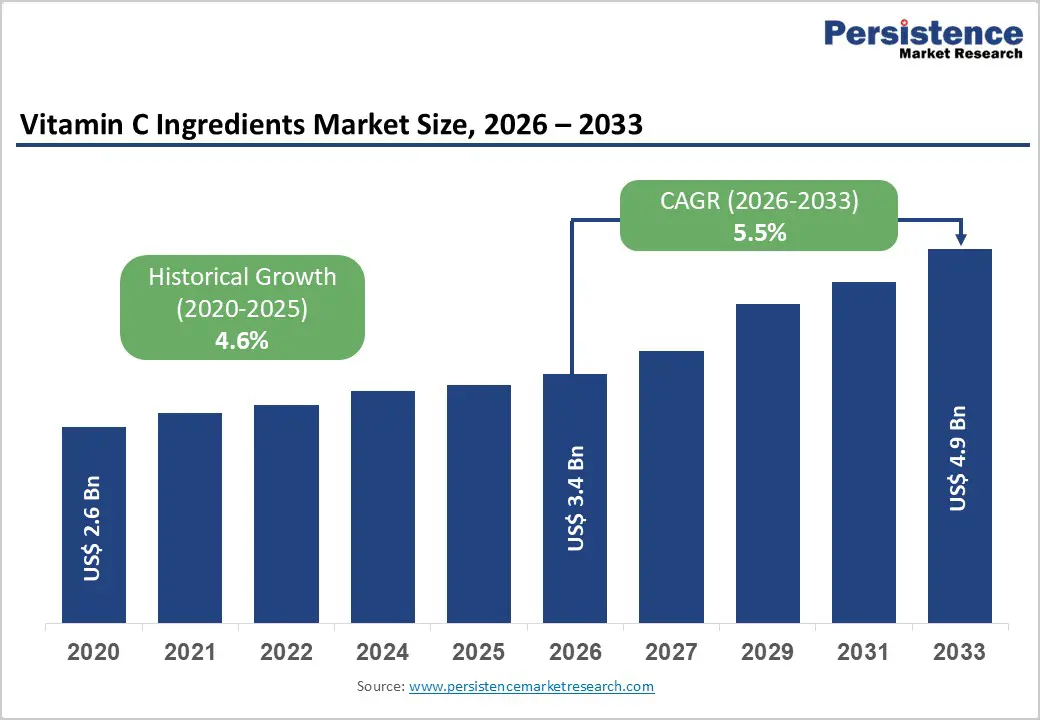

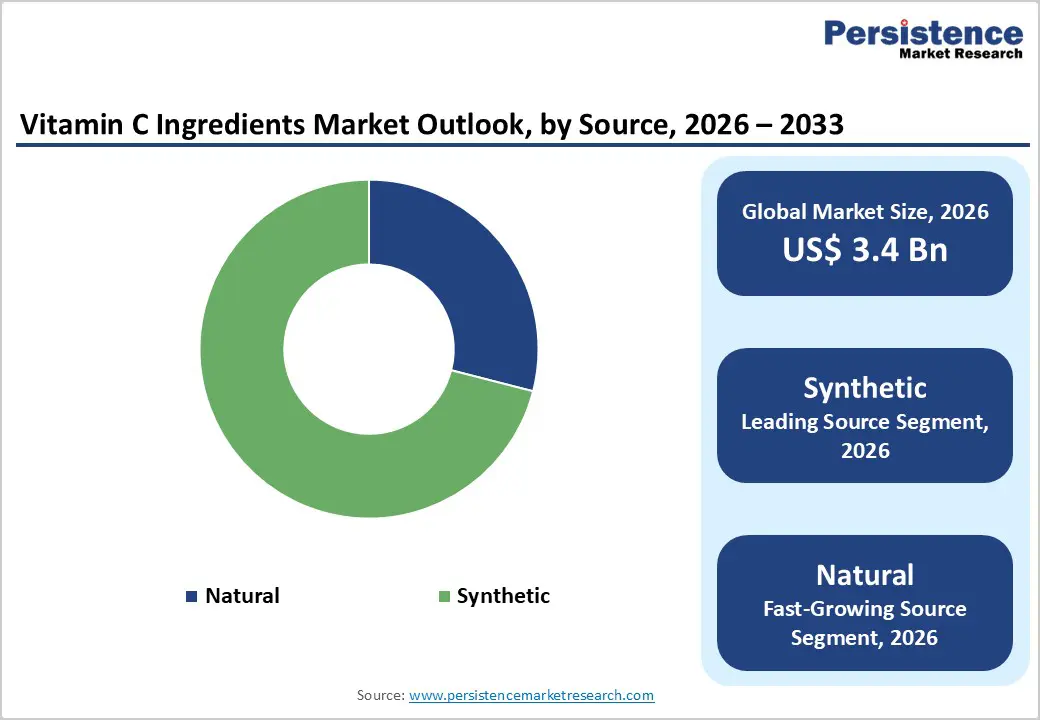

The global vitamin C ingredients market size is expected to be valued at US$ 3.4 billion in 2026 and projected to reach US$ 4.9 billion by 2033, growing at a CAGR of 5.5% between 2026 and 2033.

Vitamin C ingredients are evolving from single-function additives into strategic enablers of immune health, skin health, and performance nutrition. Shifts in daily preventive health behavior, cosmetic science, and functional formulation are redefining how vitamin C is sourced, positioned, and commercialized globally.

Key Industry Highlights:

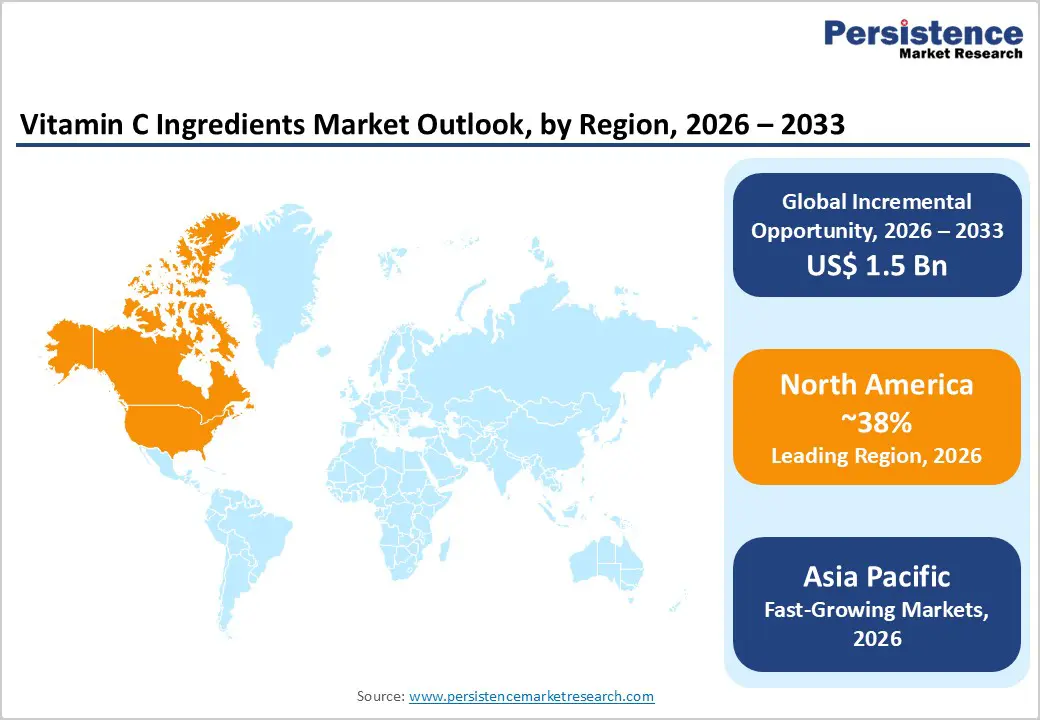

- Leading Region: Asia Pacific, holding approximately 38% market share, supported by large-scale synthetic vitamin C manufacturing in China, expanding nutraceutical consumption in India, and strong cosmetic innovation pipelines in Japan and South Korea.

- Fastest-Growing Region: Latin America, driven by rising demand for fortified beverages, affordable immune-support supplements, and growing use of vitamin C in cosmetic and personal care formulations across Brazil, Mexico, and Argentina.

- Dominant Source Segment: Synthetic Vitamin C Ingredients, accounting for around 71% share in 2025 due to scalable production, consistent purity, regulatory familiarity, and suitability for high-volume food, pharma, and cosmetic applications.

- Fastest-Growing End-Use Segment: Cosmetics & Personal Care, fueled by increased use of stabilized vitamin C derivatives in anti-aging, brightening, and pollution-defense skincare, alongside premium dermocosmetic and male grooming trends.

- Market Driver: Rising integration of vitamin C into everyday immune-support foods, beverages, and supplements, shifting demand from episodic supplementation toward routine, lifestyle-based consumption.

- Opportunities: Custom-designed vitamin C blends for functional beverages and sports nutrition, leveraging encapsulation, pH stability, and clean-label formulations to deliver targeted performance and recovery benefits.

- Key Developments: In November 2025, SEIWA launched iVC 3GA-green, a plant-derived sustainable anti-ageing vitamin C ingredient. In January 2025, OnScent introduced Acerola Cherry Ferment with vitamin C, while Alpha-H enhanced Liquid Gold with added vitamin C to advance its skincare positioning.

| Key Insights | Details |

|---|---|

| Vitamin C Ingredients Market Size (2026E) | US$ 3.4 Bn |

| Market Value Forecast (2033F) | US$ 4.9 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.6% |

Market Dynamics

Driver - Rising use of vitamin C in immune-support formulations across foods, beverages, and supplements

Immune resilience has moved from seasonal concern to everyday priority, reshaping demand for vitamin C ingredients across foods, beverages, and supplements. Consumers increasingly associate vitamin C with daily defense rather than short-term illness management, encouraging regular intake through fortified juices, gummies, powders, and ready-to-drink shots.

Food and beverage manufacturers are incorporating vitamin C into breakfast staples, hydration products, and immunity-focused snacks, responding to demand for proactive wellness solutions that align with routine consumption patterns. This shift has expanded the use of vitamin C beyond tablets to mass-market consumables.

Supplement brands are reinforcing this momentum by positioning vitamin C as a foundational immune nutrient combined with zinc, probiotics, and botanical extracts. Advances in stabilization technologies have improved shelf life and taste masking, enabling higher inclusion rates without sensory trade-offs. As immune health becomes integrated into lifestyle nutrition, vitamin C ingredients are transitioning into high-volume, multi-category inputs across global consumer health ecosystems.

Restraints - Regulatory variation across food, pharma, and cosmetic uses

Fragmented regulatory frameworks across food, pharmaceutical, and cosmetic applications present a structural challenge for vitamin C ingredient suppliers. Each end-use category imposes distinct purity standards, labeling requirements, and permissible dosage limits, thereby complicating cross-sector product development.

A formulation approved for dietary supplements may encounter reformulation barriers in skincare or functional beverages, thereby increasing compliance costs and delaying commercialization timelines for manufacturers operating across multiple industries.

These regulatory inconsistencies are exacerbated in cross-border trade, where approval pathways vary widely across regions. Ingredient producers must maintain parallel documentation, certifications, and testing protocols to meet jurisdiction-specific requirements.

Smaller companies often struggle with the financial and technical burden of multi-market compliance, limiting innovation and scalability. This regulatory complexity discourages rapid portfolio diversification and can delay market entry for novel vitamin C formats, particularly in high-growth cosmetic and nutraceutical applications.

Opportunity - Customizing vitamin C blends for functional beverages and sports nutrition

Personalized performance nutrition is opening new avenues for customized vitamin C ingredient blends tailored to functional beverages and sports nutrition products.

Athletes and active consumers increasingly seek formulations aligned with endurance, recovery, hydration, or stress management goals. Vitamin C is being engineered into synergistic blends with electrolytes, amino acids, and plant extracts to enhance management of oxidative stress during physical exertion.

Startups and ingredient innovators are leveraging encapsulation, pH-stable forms, and fast-dissolving systems to optimize bioavailability in liquid formats. These technical improvements enable precise dosing without compromising taste or clarity, which is critical for sports drinks and pre-workout beverages.

Customization also supports clean-label positioning by reducing dependence on additives. As brands compete through functionality rather than volume alone, tailored vitamin C solutions offer strong differentiation potential for emerging players and established manufacturers targeting premium performance nutrition segments.

Category-wise Analysis

By Source Insights

Synthetic Vitamin C ingredients held 71% share as of 2025, reflecting strong manufacturing scalability and consistent quality advantages. Synthetic production delivers high-purity ascorbic acid with predictable potency, enabling reliable performance across food, pharmaceutical, and cosmetic formulations. Large-scale production efficiencies support stable pricing, making synthetic vitamin C the preferred choice for mass-market applications requiring uniformity and long shelf life.

Formulation flexibility further reinforces dominance, as synthetic variants integrate easily into powders, liquids, tablets, and topical products without variability risks associated with natural extraction. Supply reliability remains a decisive factor for multinational brands operating high-volume production lines. While consumer interest in natural sourcing continues to rise, synthetic vitamin C retains leadership due to its regulatory familiarity, technical stability, and ability to meet global demand without agricultural supply constraints.

By End-user Insights

The cosmetics and personal care market is projected to grow at a 8.9% CAGR over the forecast period, driven by rising demand for science-backed skin health solutions. Vitamin C has become a cornerstone ingredient in brightening, anti-aging, and environmental defense formulations due to its role in collagen synthesis and in reducing oxidative stress. Skincare consumers increasingly favor products positioned as preventive rather than corrective, supporting frequent usage.

Brands are investing in stabilized vitamin C derivatives that reduce irritation while maintaining efficacy, enabling broader adoption across sensitive skin categories. Growth is further supported by rising demand for male grooming and by premium dermocosmetic lines targeting urban pollution exposure. As regulatory scrutiny strengthens ingredient transparency, vitamin C’s established safety profile enhances its attractiveness. This momentum positions cosmetics and personal care as one of the most dynamic end-use segments for vitamin C ingredients globally.

Regional Insights

Asia Pacific Vitamin C Ingredients Market Trends

Asia Pacific holds approximately. 38% share in 2026, anchored by large-scale manufacturing and expanding consumer health awareness. China remains a major production hub, benefiting from integrated chemical supply chains and export-oriented capacity. Domestic demand continues to rise as functional foods and immune-support beverages gain traction among urban populations.

India is experiencing robust growth in nutraceutical applications, driven by the adoption of preventive healthcare and pharmacy-led penetration of supplements.

Japan emphasizes high-purity vitamin C for pharmaceutical-grade formulations and premium skincare, while South Korea focuses on cosmetic innovation using stabilized derivatives. Regional growth is reinforced by e-commerce distribution, private-label expansion, and government support for nutrition and wellness industries. Together, these dynamics position the Asia Pacific as both a production powerhouse and a rapidly evolving consumption market.

Middle East & Africa Vitamin C Ingredients Market Trends

The Latin American vitamin C ingredients market is expected to grow at a CAGR of 9.1%, driven by rising health awareness and increasing adoption of functional foods. Brazil leads regional demand, where fortified beverages and immune-support supplements are gaining mainstream acceptance. Local manufacturers are increasingly incorporating vitamin C into powdered drinks aligned with tropical consumption habits.

Mexico is experiencing growth in fortified packaged foods and OTC supplements distributed through pharmacy chains. Argentina shows rising demand among cosmetic and personal care producers for antioxidant-rich formulations. Regional growth benefits from improving regulatory clarity and increasing investment in local processing capabilities. As affordability-driven innovation accelerates, vitamin C ingredients are being positioned as accessible wellness enhancers rather than premium-only inputs, supporting broad-based market expansion across Latin America.

Competitive Landscape

The global Vitamin C ingredients market exhibits a moderately consolidated structure, with established chemical producers and specialized ingredient suppliers holding significant influence. Leading companies prioritize scale efficiency, consistent purity, and long-term supply contracts with food, pharma, and cosmetic brands. Investment in clean-label compatible processing and traceability systems is becoming a competitive necessity.

Sustainability initiatives focus on energy-efficient synthesis, waste reduction, and compliance with environmental regulations. Certifications in quality management, pharmaceutical standards, and cosmetic safety are widely used to enhance buyer confidence.

Product innovation centers on stabilized derivatives, encapsulated formats, and application-specific grades. Regulatory alignment across regions is shaping portfolio strategies, encouraging manufacturers to develop versatile ingredients that meet multi-sector compliance without extensive reformulation.

Key Developments:

- In November 2025, SEIWA launched iVC 3GA-green, a 100% plant-derived, sustainable anti-ageing vitamin, designed to deliver high bioavailability while meeting clean-label and environmentally responsible formulation standards for modern cosmetic and nutraceutical applications.

- In January 2025, OnScent introduced an Acerola Cherry Ferment enriched with vitamin C to support skin elasticity, while Alpha-H upgraded its iconic Liquid Gold formulation by incorporating vitamin C, strengthening its positioning in brightening and age-support skincare solutions.

Companies Covered in Vitamin C Ingredients Market

- DSM-Firmenich N.V.

- BASF SE

- CSPC Pharmaceutical Group Ltd

- Northeast Pharmaceutical Group Co., Ltd

- Zhejiang NHU Co., Ltd

- Lonza Group Ltd

- ADM

- DuPont

- Glanbia plc

- Evonik Industries AG

- Rochem International Inc

- Others

Frequently Asked Questions

The global Vitamin C Ingredients market is projected to be valued at US$ 3.4 Bn in 2026.

Rising use of vitamin C in immune-support formulations across foods, beverages, and supplements is a key driver for the global Vitamin C Ingredients market.

The global Vitamin C Ingredients market is poised to witness a CAGR of 5.5% between 2026 and 2033.

Customizing vitamin C blends for functional beverages and sports nutrition is a key opportunity.

Major players in the global Vitamin C Ingredients market include DSM-Firmenich N.V., BASF SE, Lonza Group Ltd, ADM, DuPont, Glanbia plc, Evonik Industries AG, and others.