- Processed Food

- Vegan Cheese Alternatives Market

Vegan Cheese Alternatives Market Size, Share, and Growth Forecast, 2026 - 2033

Vegan Cheese Alternatives Market by Product Type (Soy Cheese, Almond Cheese, Cashew Cheese, Coconut Cheese, Others), Form (Blocks, Slices, Shreds, Spreads, Others), Source (Plant Milk, Nuts, Soy, Others), End-User (Household, Food Service Industry, Others), and Regional Analysis for 2026 - 2033

Vegan Cheese Alternatives Market Share and Trends Analysis

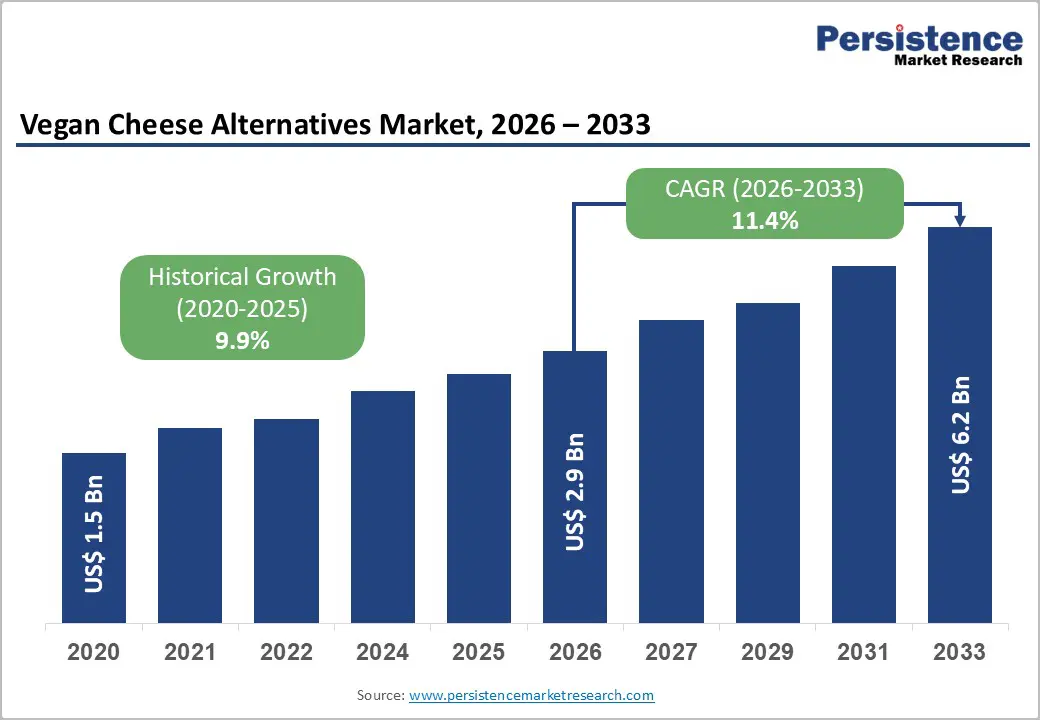

The global vegan cheese alternatives market size is likely to be valued at US$ 2.9 billion in 2026, and is projected to reach US$ 6.2 billion by 2033, growing at a CAGR of 11.4% during the forecast period 2026−2033. Rising consumer awareness of plant-based diets and dietary intolerance drives demand. Shifting demographic preferences toward sustainable nutrition encourages adoption across urban populations. Integration of advanced food-processing technologies enables production of diverse flavors and textures.

Expanding retail and e-commerce penetration facilitates consumer access and scalability. Regulatory support for plant-based labeling enhances trust and compliance. Clinical awareness regarding health benefits of reduced dairy intake reinforces preference for plant-derived alternatives. Technological innovation in formulation and preservation strengthens product shelf life and market reach. Healthcare infrastructure improvements, including hospital and institutional food service adoption, stimulate demand by incorporating plant-based options into standard dietary programs.

Key Industry Highlights

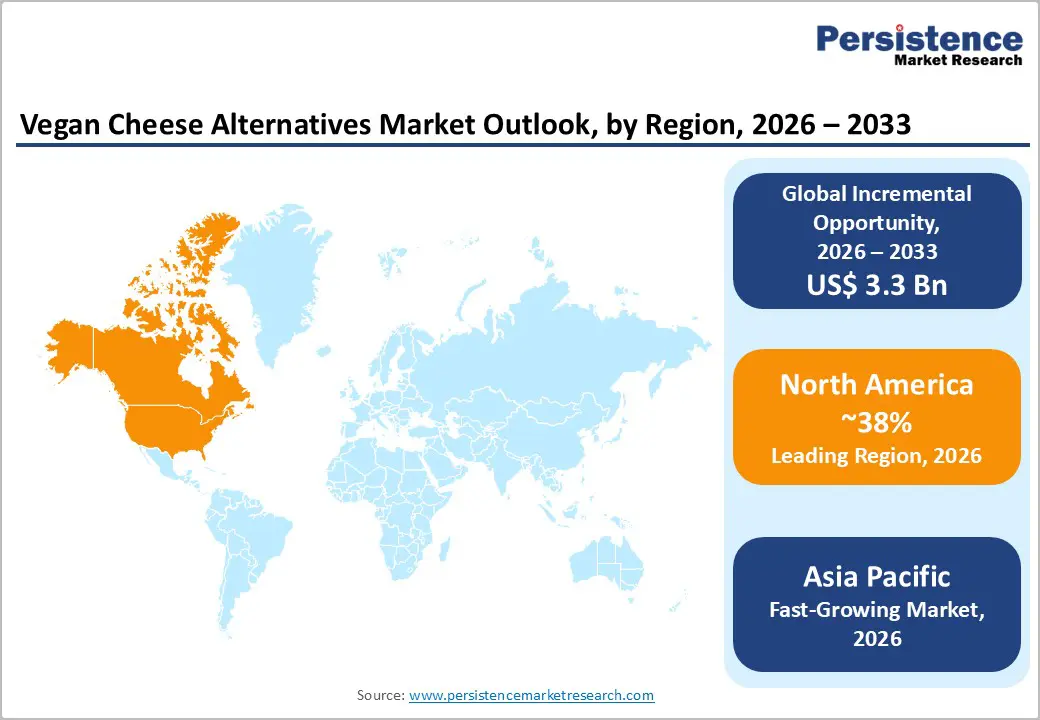

- Dominant Region: North America is poised to lead with an estimated 38% market share in 2026, driven by retail strength and health-focused demand.

- Fastest-growing Regional Market: Asia Pacific is forecasted to be the fastest-growing market between 2026 and 2033, propelled by large-scale urbanization and rising consumer demand.

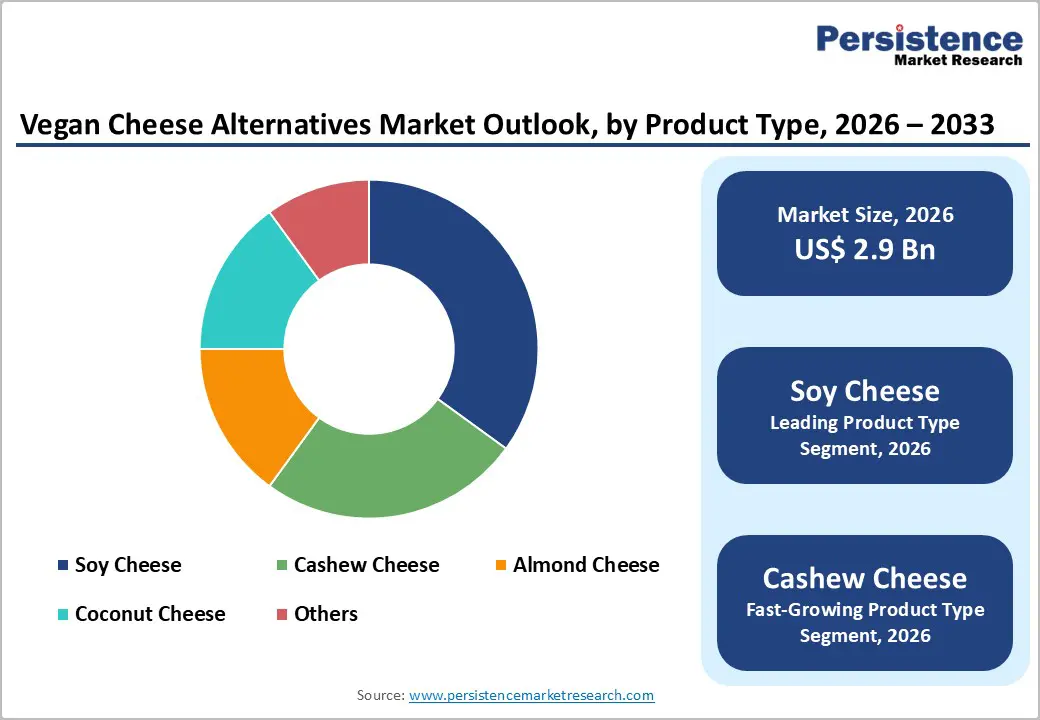

- Leading Product Type: Soy cheese is expected to hold 35% market share in 2026, supported by familiarity, affordability, and broad distribution.

- Fastest-growing Product Type: Cashew cheese is expected to be the fastest-growing segment from 2026 to 2033, driven by taste and premium appeal.

| Key Insights | Details |

|---|---|

|

Vegan Cheese Alternatives Market Size (2026E) |

US$ 2.9 Bn |

|

Market Value Forecast (2033F) |

US$ 6.2 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

11.4% |

|

Historical Market Growth (CAGR 2020 to 2025) |

9.9% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Demographic Shifts and Evolving Consumer Preferences

Younger age cohorts and evolving lifestyle patterns are reshaping dietary choices, influencing food procurement strategies across consumer segments. Evidence from a nationally representative survey indicates that around 10% of the population in Great Britain reported reducing or eliminating animal products from their diets in some capacity in 2025, reflecting a meaningful shift toward plant-rich eating habits among broad demographic groups. This trend shows that increasing numbers of consumers prioritize nutrient-dense, plant-derived options to align with dietary goals related to health maintenance and wellbeing. Younger generations, urban populations, and individuals with higher educational attainment demonstrate greater openness to plant-based diets, leading to changes in grocery basket compositions and dining preferences.

National dietary frameworks in developed economies reinforce this movement by highlighting plant-forward eating patterns as aligned with public health objectives. Guidance from federal agencies emphasizes consumption of fruits, vegetables, legumes, and other plant-sourced foods as components of nutrient-rich dietary patterns that support reduction of chronic illness risk and enhanced wellbeing across life stages. These official recommendations influence institutional meal planning, educational initiatives, and public sector procurement specifications, prompting foodservice providers and retailers to adjust portfolios accordingly. Shifts in dietary norms, driven by demographic and preference patterns, thus create a sustained need for alternative offerings that meet emerging nutritional expectations and evolving consumer priorities.

Technological Advancements and Product Innovation

Advances in production methods and ingredient science enhance formulation capabilities through innovative techniques that improve sensory attributes and functionality. Precision fermentation, enzyme-assisted processing, and advanced microbiology have been applied to generate components that better replicate traditional cheese texture and taste, supporting broader culinary applications. These technologies enable manufacturers to reduce reliance on artificial additives while enhancing nutritional stability and shelf performance, strengthening product portfolios and supply consistency. Improved ingredient performance lowers operational inefficiencies in processing and broadens appeal across multiple culinary formats, prompting investment in scalable industrial solutions and supporting portfolio diversification.

Guidance issued by the U.S. Food and Drug Administration (FDA) on labeling of plant-based alternatives to animal-derived foods in 2025 reflects regulatory engagement with product differentiation and consumer information, encouraging producers to adopt clear naming and labeling practices that identify plant sources. This regulatory activity signals official recognition of diverse formulations and supports industry investment in formulation science and quality assurance protocols. Public sector emphasis on transparency in naming and labeling can reduce consumer informational barriers and raise confidence, prompting companies to integrate advanced production technologies to align with regulatory expectations and evolving consumer preferences.

High Production Costs and Supply Chain Complexity

Production expense structures in food processing create cost pressures that influence pricing and accessibility across product lines. Specialized ingredients required for alternative formulations often undergo extensive processing, blending, and packaging, all of which demand capital investment in equipment and skilled labor that smaller producers struggle to amortize. Volatile input costs for plant proteins further complicate procurement planning and cost forecasting, increasing exposure to commodity price swings. Sourcing from geographically dispersed suppliers adds transportation and storage costs, while limited bargaining power relative to established food sectors raises unit expenses. These factors compress margins and require higher retail prices that can slow adoption in price-sensitive segments.

Supply chain complexity combines ingredient sourcing variability with distribution challenges that affect operational efficiency and margin maintenance. Agricultural commodity pricing influenced by weather, trade dynamics, and input costs leads to fluctuating upstream expenses. Processing needs for specialty plant components often require coordination across multiple suppliers and logistics partners, increasing inventory risks and coordination costs. Emerging supply networks may lack robust cold-chain infrastructure or long-term contracts that larger sectors maintain, resulting in inconsistent quality and higher intermediate costs. Structural challenges in sourcing, handling, and logistics constrain price competitiveness and slow penetration in diverse markets.

Consumer Acceptance Barriers

Perceptions of taste, texture, and versatility strongly influence adoption of plant-based alternatives. Consumers accustomed to traditional dairy flavors often perceive plant-based options as less desirable, limiting repeat purchase and trial. Awareness of nutritional equivalence and functional performance remains uneven across households and foodservice operators. Packaging, labeling, and branding that do not clearly convey taste, usage, or quality benefits can reduce consumer confidence. Retail availability is inconsistent, particularly in regions with limited modern trade or specialty stores. Early experiences shape long-term behavior, making sensory consistency and familiar characteristics essential for trust, repeat purchase, and gradual expansion across consumer segments.

Cultural habits and entrenched dietary practices constrain trial and integration across diverse markets. Populations with strong dairy consumption traditions show resistance to substitution in cooking and daily meal routines. Culinary professionals may limit usage in recipes when texture, meltability, or flavor intensity differs from expectations, affecting adoption in foodservice channels. Marketing and education emphasizing ethical, environmental, and health advantages support awareness and trial. Limited knowledge of ingredient quality, allergen management, and processing methods reinforces hesitancy, requiring strategic messaging and product consistency to improve acceptance and enable wider market penetration.

Integration with Functional and Fortified Foods

Federal nutrition guidance emphasizes nutrient-dense eating patterns that include a variety of high-quality protein foods, extending to legumes, nuts, seeds, and soy as recognized plant sources, aligning product positioning with broader dietary priorities in public health strategy. The 2025–2030 Dietary Guidelines for Americans encourage consumption of nutrient-rich foods that support chronic disease prevention and overall wellbeing, signaling that fortified and functional attributes can be strategically integrated to meet official recommendations. Plant-sourced protein and nutrient diversity are presented as compatible with health objectives set by U.S. Departments of Agriculture (USDA) and Health and Human Services (HHS), supporting formulation strategies that address both taste and micronutrient content.

Consumer interest in foods offering benefits beyond basic nutrition continues to expand, with trends reflecting demand for options that support digestive health, immune function, and overall vitality through enriched nutritional profiles. Fortification with vitamins, minerals, and probiotics aligns with public expectations for nutrient-enhanced foods that support wellbeing across life stages. Formulations that clearly communicate functional value through labeling and transparent nutrient information can differentiate offerings in crowded retail environments. Alignment of product innovation with evolving nutrition priorities enables brands to appeal to health-oriented segments seeking practical solutions that contribute to balanced dietary patterns and long-term wellness goals.

Technological Convergence and Product Diversification

Interdisciplinary innovation in food science and production technology expands formulation and processing capabilities by integrating biological systems, engineering, and digital tools. Federal investments from agencies such as the National Institute of Food and Agriculture (NIFA) directed toward novel foods and advanced manufacturing illustrate public support for enhancing quality, safety, and nutritional optimization in emerging food categories. Precision fermentation, automated processing, and digital design platforms enable diversification of texture, flavor, and nutrient profiles beyond basic plant sources, unlocking new formulation categories. These tools improve operational efficiency, accelerate development cycles, and support products that align with evolving consumer expectations for sensory performance and nutrition value across applications.

U.S. nutrition policy shifts emphasize a broader role for diverse plant-sourced proteins in daily dietary patterns, reflecting official guidance to include legumes, nuts, seeds, and soy in recommended eating frameworks. Federal recommendations highlight increased consumption of plant-based protein to support overall nutrient adequacy and chronic disease prevention, creating a favorable environment for innovation in product formulation. Regulatory recognition of plant sources alongside mainstream food categories encourages companies to pursue diversified product portfolios that resonate with evolving dietary preferences.

Category-wise Analysis

Product Type Insights

Soy cheese is anticipated to secure around 35% of the vegan cheese alternatives market revenue share in 2026, reflecting established consumer familiarity, affordability, and broad distribution across retail and food service channels. Clinical acceptance and research on soy-based protein benefits support adoption among health-conscious consumers. Production processes are optimized for consistency and shelf life, enabling large-scale manufacturing. Accessibility in urban and semi-urban markets ensures steady demand from households and institutional buyers. Innovation in flavor profiles and packaging enhances consumer adherence and brand preference.

Cashew cheese is expected to be the fastest-growing segment during the 2026-2033 forecast period, propelled by sensory appeal, premium positioning, and rising preference for nut-based products. Consumer perception of higher nutritional value and favorable taste drives adoption among affluent and urban populations. Expansion of e-commerce platforms and niche retail outlets improves accessibility. Innovation in fermentation and flavoring technologies enhances product quality and shelf life. Integration with plant-based culinary trends, including gourmet and artisanal offerings, supports incremental market capture.

End-User Insights

Household consumers are likely to be the leading segment with a projected 55% market share in 2026 due to home consumption trends, diet-conscious purchasing, and retail accessibility. Shoppers increasingly prioritize plant-based options that align with personal health goals, ethical considerations, and environmental awareness. Digital platforms enable easy access to a wide range of products, facilitating repeat purchases and fostering brand loyalty through subscription services and targeted promotions. Cost efficiency compared with dining out encourages regular consumption. Packaging innovations that enhance portion control, resealability, and shelf-life improve convenience and reduce waste, reinforcing consistent use and sustained engagement with plant-based offerings across households.

Food service industry is anticipated to be the fastest-growing segment from 2026 to 2033, fueled by plant-based menu adoption in restaurants, cafes, and institutional catering. Culinary professionals value consistency in texture, flavor, and meltability for reliable recipe integration. Regulatory endorsement supports safe and standardized incorporation of plant-based alternatives in commercial kitchens. Technology-enabled procurement systems streamline sourcing and inventory management, ensuring product availability. Rising consumer demand for ethical, sustainable, and plant-based dining experiences drives menu diversification. Partnerships between suppliers and foodservice operators enhance access to innovative formulations, expanding adoption and revenue growth within the sector.

Regional Insights

North America Vegan Cheese Alternatives Market Trends

North America is expected to lead with an estimated 38% of the vegan cheese alternatives market share in 2026, supported by mature retail infrastructure, high purchasing power, and established health-focused behaviors in the United States and Canada. Supermarkets, specialty stores, and e-commerce platforms provide widespread product availability, enabling consistent household adoption. Regulatory frameworks on labeling, nutritional transparency, and food safety reinforce consumer confidence. Urban populations prioritize dietary quality and sustainability, influencing repeat purchases. Investment in advanced processing technologies and cold-chain logistics ensures consistent product quality. Collaboration between manufacturers and retailers enables rapid product rollout, responding to evolving taste preferences and expanding portfolio offerings across both countries.

Culinary sector integration in the United States and Canada, with restaurants, cafes, and institutional catering incorporating plant-based alternatives, strengthens leadership. Professional kitchens value texture, meltability, and flavor consistency, driving adoption in commercial channels. Marketing emphasizing health benefits, environmental impact, and ethical sourcing resonates with informed consumers, supporting willingness to pay. Research institutions contribute to innovation in fortified and nutrient-enhanced formulations. Cross-industry partnerships, including supply chain optimization and ingredient sourcing, improve operational efficiency. Digital platforms and educational campaigns enhance product discovery and reinforce brand loyalty.

Europe Vegan Cheese Alternatives Market Trends

Europe shows steady adoption, supported by cultural acceptance and regulatory encouragement. Established retail networks, including supermarkets, specialty stores, and online platforms, provide wide accessibility for households seeking convenient and nutritious options. Urban populations demonstrate growing preference for nutrient-rich and sustainable food products, influencing purchasing patterns and encouraging repeat consumption. Regulatory frameworks emphasize labeling transparency, food safety, and ingredient standards, reinforcing consumer confidence and retailer participation. Investment in production technology, cold-chain logistics, and quality control ensures consistent product performance. These factors enable companies to maintain brand credibility and meet evolving demand across diverse urban centers.

Culinary and foodservice sectors contribute to market growth, with restaurants, cafes, and institutional catering integrating plant-based alternatives into menus. Professional kitchens prioritize consistent texture, flavor, and meltability to maintain quality across diverse applications. Marketing campaigns emphasizing environmental benefits, ethical sourcing, and health outcomes resonate with informed consumers and support willingness to pay. Local manufacturers innovate formulations, incorporating fortified ingredients and adapting flavor profiles to meet regional taste preferences. Strategic partnerships across supply chains improve operational efficiency and ensure reliable product availability. Digital platforms support product discovery, repeat purchase, and brand loyalty across retail and commercial channels.

Asia Pacific Vegan Cheese Alternatives Market Trends

Asia Pacific is forecasted to be the fastest-growing market for vegan cheese alternatives between 2026 and 2033, stimulated by rapid urbanization, rising disposable income, and exposure to global dietary trends. Expanding modern retail formats, including supermarkets, hypermarkets, and e-commerce platforms, improve accessibility for consumers seeking plant-based options. Younger, health-conscious populations demonstrate higher adoption of nutrient-rich and sustainable foods, influencing household and institutional procurement patterns. Investment in cold-chain infrastructure, logistics, and supply networks ensures consistent product quality and availability across metropolitan and emerging cities. These developments support steady demand growth and create an environment favorable for new product introductions.

Urban foodservice channels, including restaurants, cafes, and institutional catering, accelerate adoption across the region. Culinary professionals prioritize texture, meltability, and flavor versatility to maintain consistency in menu offerings. Marketing initiatives emphasizing environmental impact, ethical sourcing, and health benefits resonate with informed consumers and influence purchasing behavior. Local manufacturers innovate formulations to align with regional taste preferences, supporting diversified offerings. Expansion of digital platforms enables product discovery, repeat purchase, and brand loyalty. Strategic partnerships between suppliers and foodservice operators improve procurement efficiency and ensure broader distribution.

Competitive Landscape

The global vegan cheese alternatives market is moderately competitive, with key players including Miyoko's Creamery, Violife, Oatly, Daiya Foods, Treeline Cheese, and Kite Hill. Competition focuses on product quality, flavor authenticity, texture, nutritional content, and brand positioning rather than major differences in core offerings. Companies invest in plant-based formulations, fortified ingredients, and sustainable sourcing. Retail presence, e-commerce platforms, and foodservice partnerships further influence competitive positioning and market share.

Market dynamics are shaped by rising consumer demand for plant-based and ethical diets, driving continuous product innovation and portfolio expansion. Packaging improvements, portion control, and extended shelf-life support household adoption, while professional kitchens prioritize consistency and versatility. Key players focus on life-cycle management, recipe optimization, and geographic expansion. Marketing emphasizing nutrition, sustainability, and ethical sourcing strengthens brand loyalty, ensuring differentiation and growth within a moderately competitive environment.

Key Industry Developments

- In February 2026, RIND expanded its portfolio with the launch of Brie Crème, a spreadable plant-based take on traditional brie made from cultured cashews and tofu designed for charcuterie boards, bread spreads, and pairing with fruit.

- In December 2025, Belgian food tech startup Those Vegan Cowboys secured €6.25 million in funding to scale its precision-fermented animal-free casein ahead of a planned 2026 US launch, advancing development of next-generation cheese alternatives.

- In October 2025, Italian startup Dreamfarm expanded into France through a retail partnership with Monoprix, launching its plant-based cheeses across around 70 supermarkets in Paris. The rollout of products such as mozzarella and ricotta alternatives reflects rising European demand for clean-label dairy substitutes and accelerating growth in the vegan cheese segment.

Companies Covered in Vegan Cheese Alternatives Market

- Miyoko's Creamery

- Violife

- Oatly

- Daiya Foods

- Treeline Cheese

- Kite Hill

- GreenVie

- Alpro

- Nature & Moi

- The Vegan Cheese Company

- Good Planet Foods

- Sunnyside Farms

Frequently Asked Questions

The global vegan cheese alternatives market is projected to reach US$ 2.9 billion in 2026.

Rising health consciousness, ethical and sustainable eating trends, and innovation in plant-based formulations are driving the market.

The market is poised to witness a CAGR of 11.4% from 2026 to 2033.

Integration with functional and fortified foods and expansion of product diversification present key market opportunities.

Some of the key market players include Miyoko's Creamery, Violife, Oatly, Daiya Foods, Treeline Cheese, and Kite Hill.