- Metalworking & Fabrication

- Tool Hammer Market

Tool Hammer Market Size, Share, and Growth Forecast, 2026 - 2033

Tool Hammer Market by Product Type (Sledge Hammers, Others), Hammer Material (Brass, Bronze, Steel, Others), Application (Nailing, Chipping & Cutting, Bricks, Others), Distribution Channel (Company Owned Website, Others), and Regional Analysis for 2026 – 2033

Tool Hammer Market Size and Trends Analysis

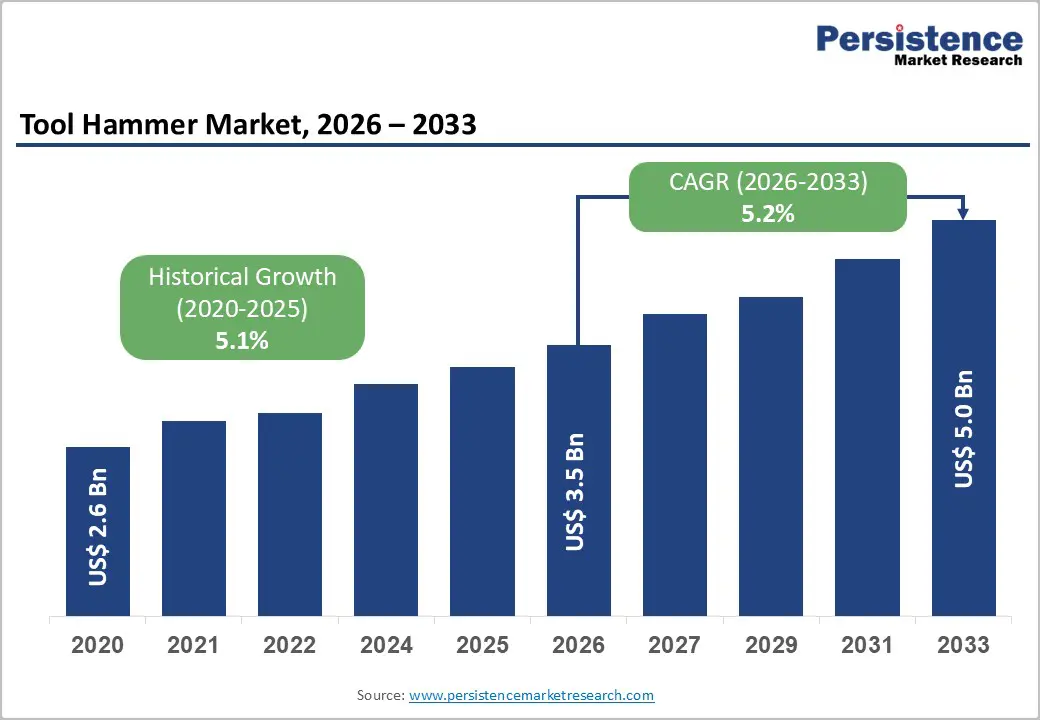

The global tool hammer market size is likely to be valued at US$3.5 billion in 2026, and is expected to reach US$5.0 billion by 2033, growing at a CAGR of 5.2% during the forecast period from 2026 to 2033, driven by the increasing prevalence of construction and renovation activities, rising demand for durable, non-sparking tool hammers in industrial safety applications, and advancements in ergonomic and composite-handled hammer designs.

Growing demand for reliable, high-impact tool hammers, particularly claw hammers and sledge hammers, in residential and commercial projects is accelerating adoption among end users. Advances in non-sparking brass and bronze alloys are further increasing adoption by providing superior safety in hazardous environments. Increasing recognition of the tool hammer as critical for precision nailing and demolition tasks in emerging DIY and infrastructure markets remains a major driver of market growth.

Key Industry Highlights:

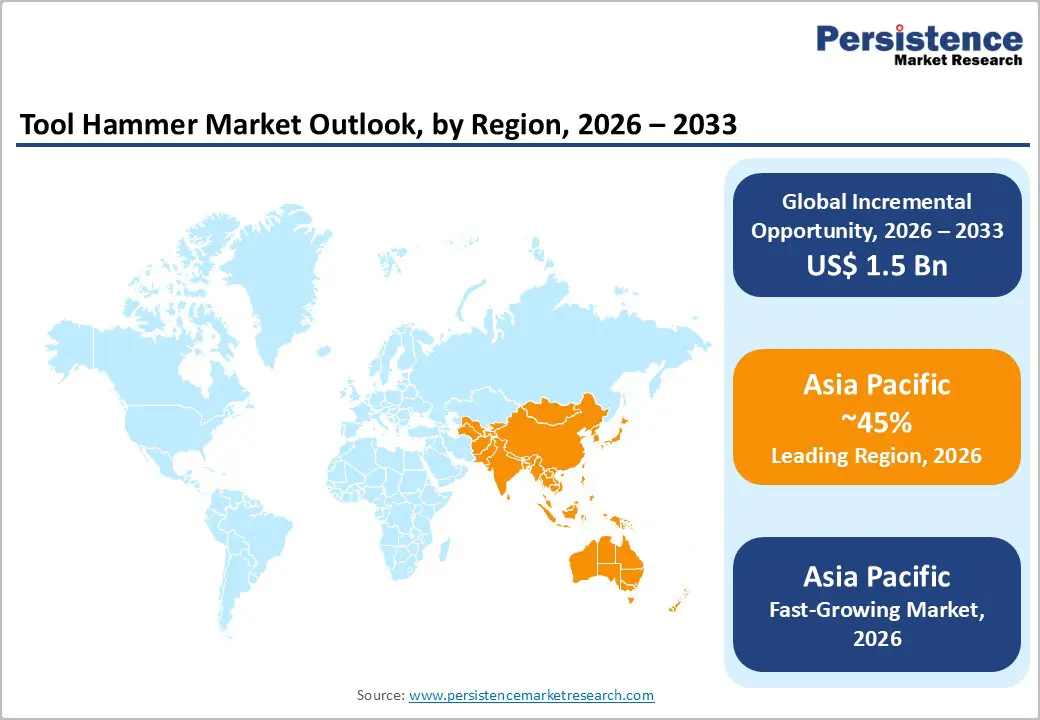

- Leading Region: Asia Pacific to dominate, accounting for a 45% market share in 2026, driven by rapid urbanization, massive infrastructure projects, and high construction volumes in China and India.

- Fastest-growing Region: Asia Pacific, fueled by expanding residential building, rising industrial maintenance, and growing investments in hand tools.

- Dominant Product Type: Claw hammers, to hold approximately 35% of the market share, as they remain the most versatile and widely used hammer type.

- Leading Hammer Material: Steel, to account for over 70% of the market revenue, due to its strength, cost-effectiveness, and widespread availability.

- Leading Application: Nailing, to contribute nearly 40% of the market revenue, due to everyday use in framing and finishing work.

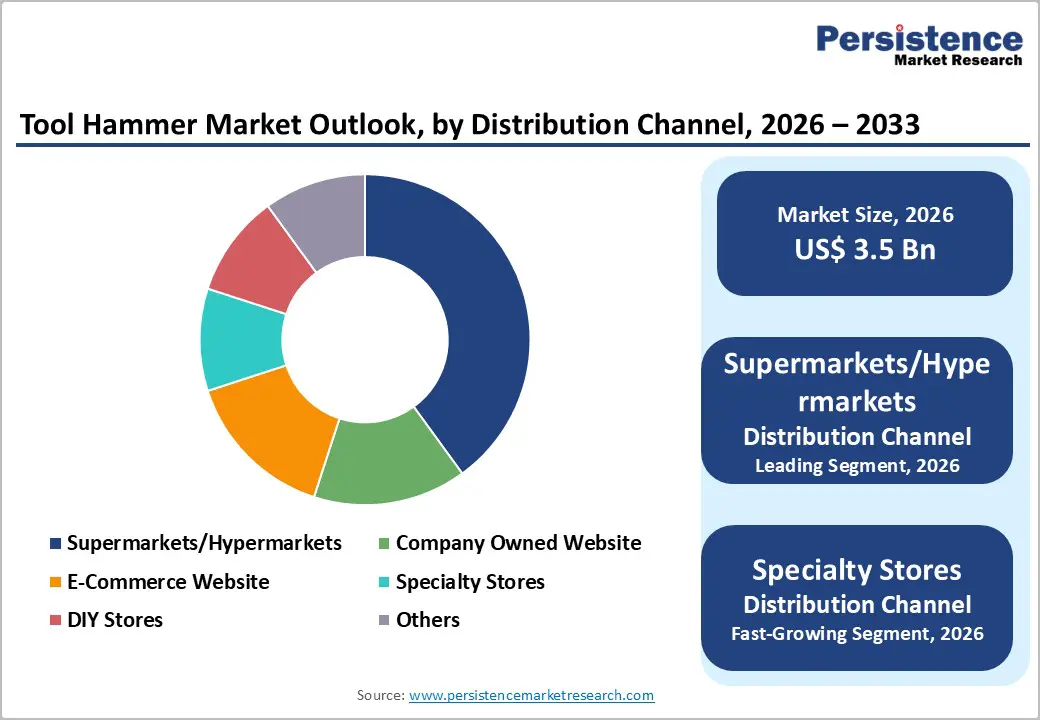

- Leading Distribution Channel: Supermarkets/Hypermarkets, to contribute nearly 30% of the market revenue, due to impulse purchases and broad accessibility.

| Key Insights | Details |

|---|---|

| Tool Hammer Market Size (2026E) | US$3.5 Bn |

| Market Value Forecast (2033F) | US$5.0 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.2% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.1% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Rising Demand for Construction and Renovation Activities and Demand for Durable Tool Hammers

The rising demand for construction and renovation activities is a key driver accelerating the adoption of durable tool hammers across residential, commercial, and industrial sectors. Rapid urbanization, infrastructure development, and housing expansion are increasing the volume of building projects worldwide, creating a strong need for reliable hand tools that can withstand intensive daily use. Renovation and remodeling projects, especially in mature markets, are also expanding as aging buildings require upgrades, repairs, and structural reinforcement. In such environments, hammers are among the most frequently used tools for framing, roofing, demolition, and finishing work, making durability a critical consideration in purchasing.

Contractors and professional tradespeople increasingly prefer hammers made from forged steel, fiberglass, and advanced composite materials because they offer higher strength, impact resistance, and longer service life. Durable hammers reduce tool replacement frequency, lower downtime, and improve job-site productivity, which directly supports project efficiency and cost control. Safety regulations and workplace standards are prompting builders to adopt tools that provide better grip, shock absorption, and ergonomic performance, thereby increasing demand for premium, long-lasting hammer designs.

High Development and Raw Material Volatility Costs

High development and raw material volatility costs present a significant barrier for companies advancing next-generation tool hammers and novel designs. Developing innovative grades such as fiberglass-handled sledgehammers, non-sparking bronze clawhammers, or ergonomic scutchhammers requires extensive research, specialized forging, and advanced handle-molding technologies that are far more expensive than standard steel hammers. Volatility is an even greater challenge: steel and alloy prices fluctuate with global supply chains, affecting costs for many refined variants, drop-forged lots, and safety-enhanced products that are sensitive to material price swings, necessitating rigorous cost optimization to ensure they remain competitive throughout production. Achieving long-term performance often requires costly drop tests, sophisticated hardness testing, and premium alloys, which significantly increase R&D expenditures.

Meeting stringent regulatory expectations for non-sparking certification (ATEX/IECEx), ergonomic standards, and batch consistency requires multiple validation studies under various conditions and across several use cases. This adds both time and financial burden to development timelines. Scaling up manufacturing requires controlled forging facilities, specialized heat-treatment lines, and quality-assurance systems, thereby increasing overall costs. For smaller manufacturers, these challenges can limit material diversification or delay commercialization.

Development of Ergonomic and Specialized Hammers

The development of ergonomic and specialized hammers has emerged as a significant opportunity in the tool hammer market, driven by the growing focus on user safety, comfort, and efficiency. Traditional hammers, while effective, often contribute to repetitive strain injuries, hand fatigue, and reduced productivity during prolonged use. To address these challenges, manufacturers are designing hammers with ergonomically shaped handles, vibration-dampening materials, and optimized weight distribution, thereby reducing physical stress on users’ hands, wrists, and arms. These innovations not only enhance comfort but also improve accuracy and control, particularly in tasks requiring precision, such as carpentry, finishing, or framing.

Specialized hammers, including framing hammers, sledgehammers, and claw hammers with tailored head designs and materials, are being developed to meet the specific requirements of professional trades and industrial applications. For instance, fiberglass or composite handles provide both strength and shock absorption, while magnetic nail holders or multi-functional hammer heads allow users to perform complex tasks more efficiently. The growing adoption of ergonomic and specialized hammers is further fueled by workplace safety regulations, which encourage companies to provide tools that minimize the risk of injury.

Category-wise Analysis

Product Type Insights

Claw hammers are expected to dominate the market, capturing around 35% of the market share by 2026. Their popularity is driven by their dual functionality, offering both nail-driving and nail-removal capabilities in one tool. This makes them indispensable for construction, carpentry, and DIY projects. With a well-balanced design, ergonomic handles, and durable steel heads, claw hammers deliver reliable performance across various tasks. Their ease of use, affordability, and availability in different sizes and materials further contribute to their widespread appeal. The Stanley 51-152 Claw Hammer, for example, is a popular choice in construction, woodworking, and DIY work, thanks to its combination of nail-driving and nail-removal features. Its forged steel head ensures long-lasting durability, while the fiberglass handle with an ergonomic grip helps reduce user fatigue, making it ideal for both professional and home use.

Sledgehammers are likely to be the fastest-growing segment due to their essential role in heavy-duty construction, demolition, and industrial applications. Their ability to deliver high-impact force makes them ideal for breaking concrete, masonry, and other tough materials, which are increasingly used in urban infrastructure and large-scale projects. Rising construction and renovation activities, along with the growing demand in the mining and manufacturing sectors, have boosted adoption. Groz Indestructible Handle Sledgehammer 34512 and similar heavy-duty sledgehammers from established tool manufacturers are increasingly adopted in construction, demolition, and industrial applications for their ability to deliver high impact force for breaking concrete and driving stakes.

Hammer Material Insights

Steel is expected to lead the market, holding approximately 70% of the share in 2026, driven by unmatched strength, cost-effectiveness, and widespread availability for general-purpose hammers. Their dominance continues as contractors prioritize durability. Rising adoption of brass non-sparking and expanded bronze safety campaigns highlights the growing focus on hazardous-zone alternatives. Stanley Black & Decker’s steel hammer range, including Stanley FatMax® steel hammers, remains a top choice among professionals and contractors as forged steel heads deliver unmatched durability, impact strength, and long term reliability for general-purpose construction and renovation tasks.

Brass is expected to be the fastest-growing segment, driven by strong demand for non-sparking safety tools and increasing adoption in the oil and gas and mining industries. The growing shift toward hazardous-zone platforms, along with improved compliance, is accelerating adoption. Advancements in alloy hardness and the continued progress of drop-forged entering production trials drive market growth. The Abc Hammers 6 lb Brass Hammer and the C&T 16 oz Solid Brass Non Sparking Hammer illustrate professional-grade brass hammers used in industrial safety applications. These tools are designed to deliver reliable performance without creating sparks, making them suitable for maintenance, assembly, and heavy work in oil & gas refineries, chemical plants, and mining sites.

Application Insights

Nailing is set to dominate the market, accounting for nearly 40% of revenue by 2026, as it remains the primary application for framing, large-scale carpentry projects, and the construction of diverse structures that require precise nail driving. The strong integration of trained carpenters, along with the need to handle high-volume and finishing tasks, drives increased consumption. The nailing sector is also leading the adoption of claw hammers and exploring the use of ball peen hammers. The Stanley Black & Decker nailing hammer, for instance, features anti-vibration technology and an ergonomic design, enhancing comfort during frequent nail driving. Its widespread popularity in both professional and DIY markets underscores how nailing applications continue to drive tool usage across a wide range of construction activities.

Demolition is expected to be the fastest-growing segment, driven by its growing role in renovation and concrete work. Demolition tools provide a powerful, efficient, and accessible force, making them ideal for workers in heavy-duty, low-fatigue environments. The growth of urban renewal projects, expanded outreach initiatives, and the broader availability of both routine and premium hammers are further driving adoption, particularly in urban and semi-urban areas. Makita's demolition hammers are known for their high impact force, durability, and manageable weight, enabling workers to complete renovation and demolition tasks faster and with less fatigue. Makita is globally recognized for its professional-grade demolition tools that strike a balance between power and ergonomics, contributing to the segment's rapid expansion.

Distribution Channel Insights

Supermarkets/Hypermarkets are expected to dominate the market, accounting for nearly 30% of revenue in 2026, as they remain the primary hubs for impulse purchases, large retail programs, and the management of diverse hammer types requiring easy access. Their strong reach, trained staff, and ability to handle high-volume or promotional blends drive higher consumption. Supermarkets are leading steel rollouts as well as administering emerging brass trials. DMart and Smart Bazar carry widely accessible steel and basic tool hammers from brands such as Stanley Black & Decker and Lifelong. These retail formats benefit from large footfall and impulse buying behavior, encouraging customers to pick up everyday tools during routine shopping.

Specialty stores are estimated to be the fastest-growing segment, driven by their strong digital presence and expanding role in comparison shopping. They offer a convenient, quick, and accessible selection, attracting buyers who prefer detailed reviews and home delivery services. Increased outreach programs, e-commerce focus, and wider availability of routine and premium hammers further accelerate uptake, boosting rapid adoption across both urban and semi-urban areas. CPO Commerce, a dedicated online tool retailer, has grown rapidly by offering a broad selection of hand tools, including hammers, directly to consumers and professionals through its platforms, including CPOOutlets.com and CPODeWALT.com. The company focuses on tools and accessories, allowing customers to easily compare products, read reviews, and make purchases with home delivery a key advantage over traditional channels.

Regional Insights

North America Tool Hammer Market Trends

Market growth in North America is driven by the region's advanced construction practices, a strong DIY culture, and heightened awareness of the benefits of ergonomic tools. The distribution networks in the U.S. and Canada provide extensive support for hand-tool programs, ensuring that hammers are widely accessible to those involved in nailing, demolition, and renovation. The rising demand for fiberglass-handled hammers that are easy to grip and provide greater comfort is further accelerating adoption, as these features help reduce fatigue.

Ongoing innovation in hammer technology, such as non-sparking materials, enhanced ergonomics, and improved safety features, is attracting substantial investment from both public and private sectors. Government initiatives and OSHA campaigns continue to promote safety measures that reduce injury risks, prevent productivity losses, and address emerging safety concerns, ensuring sustained demand in the market. The growing emphasis on brass grades and specialized uses, particularly in industrial applications, is expanding the range of potential uses for tool hammers.

Europe Tool Hammer Market Trends

Europe is propelled by increasing awareness of ergonomic benefits, strong construction systems, and government-led safety programs. Countries such as Germany, France, and the U.K. have well-established building frameworks that support routine hammer use and encourage the adoption of innovative tool delivery methods, including tool hammers. These durable formulations are particularly appealing for nailing populations, regulation-conscious operators, and renovation users, improving productivity and coverage rates.

Technological advancements in tool hammer development, such as enhanced handle damping, application-targeted delivery, and improved non-sparking grades, are further boosting market potential. European authorities are increasingly supporting research and trials for hammers against both routine and specialized needs, strengthening market confidence. The growing emphasis on convenient, low-fatigue options is aligned with the region’s focus on preventive worker health and reducing injuries. Public awareness campaigns and promotion drives are expanding reach in both urban and rural areas, while suppliers are investing in forging and novel variants to increase efficacy.

Asia Pacific Tool Hammer Market Trends

Asia Pacific is expected to be both the dominant and fastest-growing market, accounting for 45% of revenue by 2026. This growth is fueled by increased awareness of construction needs, expanding government initiatives, and the widespread adoption of application programs across the region. Countries such as India, China, Japan, and various Southeast Asian nations are actively promoting hammer campaigns to meet the growing demand for new construction and renovation projects. Tool hammers are especially popular in these regions for their affordability, ease of use, and suitability for large-scale construction in both urban and rural areas.

Technological advancements are driving the development of stable, efficient, and easy-to-swing hammers that can endure tough job-site conditions while minimizing fatigue. These innovations are key to reaching remote locations and enhancing overall productivity. The rising demand for nailing, demolition, and chipping applications is further fueling market expansion. Public-private partnerships, increased investments in construction, and growing research and manufacturing capacity in hand tools are all contributing to this growth. The combination of ease of use, better balance, and reduced risk of strain makes tool hammers the preferred choice for many.

Competitive Landscape

The global tool hammer market features competition between established hand-tool leaders and emerging safety-focused suppliers. In North America and Europe, Estwing Manufacturing Company and Stanley Black & Decker lead through strong R&D, distribution networks, and contractor ties, bolstered by innovative one-piece steel and fiberglass programs. In Asia Pacific, Graz Engineering Tools advances with cost-competitive solutions, enhancing accessibility. Non-sparking delivery boosts safety, cuts spark risks, and enables mass integrations across hazardous regions. Strategic partnerships, collaborations, and acquisitions merge expertise, expand portfolios, and speed commercialization. Ergonomic formulations solve fatigue issues, aiding penetration in labor-intensive areas.

Key Industry Developments

- In October 2025, IQIP introduced the Hydrohammer® IQ8, setting a new benchmark in hydraulic impact hammer technology. The IQ8 was engineered to drive the foundations of offshore wind projects, and it was built to handle the largest monopiles, the most challenging soils, and the boldest ambitions, the kind that were pursued by offshore wind developers, contractors, and IQIP alike.

- In July 2025, Mincon Group plc announced the launch of the MP75-MC, the second new addition to its next-generation MP-series range of DTH hammers for 2025. The MP75-MC was designed around Mincon’s high-performance MP-series internal architecture and paired with the proven MC shank to deliver a best-in-class combination of penetration speed, durability, and efficiency. This 7-inch-class DTH hammer was engineered to deliver performance for drilling hole diameters typically reserved for 8” hammers, while being operated using the 6” hammer air packages fitted to modern mobile drill rigs, making it ideal for sites where air availability or rig configuration restricted the use of larger tooling.

Companies Covered in Tool Hammer Market

- Ampco Safety Tools

- Douglas Tool

- Estwing Manufacturing Company

- Faithfull Tools

- Graz Engineering Tools (P) Ltd.

- Hardcore Hammers

- Ken-Tool

- Klein Tools, Inc.

- NC Black Co., LLC.

- Stanley Black & Decker

- Vaughan Manufacturing

Frequently Asked Questions

The global tool hammer market is projected to reach US$3.5 billion in 2026.

The rising prevalence of construction and renovation activities and demand for durable tool hammers are key drivers.

The tool hammer market is poised to witness a CAGR of 5.2% from 2026 to 2033.

Advancements in non-sparking and ergonomic delivery platforms are key opportunities.

Estwing Manufacturing Company, Stanley Black & Decker, Vaughan Manufacturing, Klein Tools, Inc., and Ampco Safety Tools are the key players.