- Testing, Inspection, & Certification

- IT Service Management Tools Market

IT Service Management Tools Market Size, Share, and Growth Forecast 2026 - 2033

IT Service Management Tools Market by Management Type (Configuration Management, Performance Management, Network Management, Database Management), by Deployment (On-Premise, Cloud), by End Use (BFSI, IT and ITES, Media and Entertainment, Retail, Manufacturing, Education, Government, Others), by Regional Analysis, 2026-2033

IT Service Management Tools Market Size and Trend Analysis

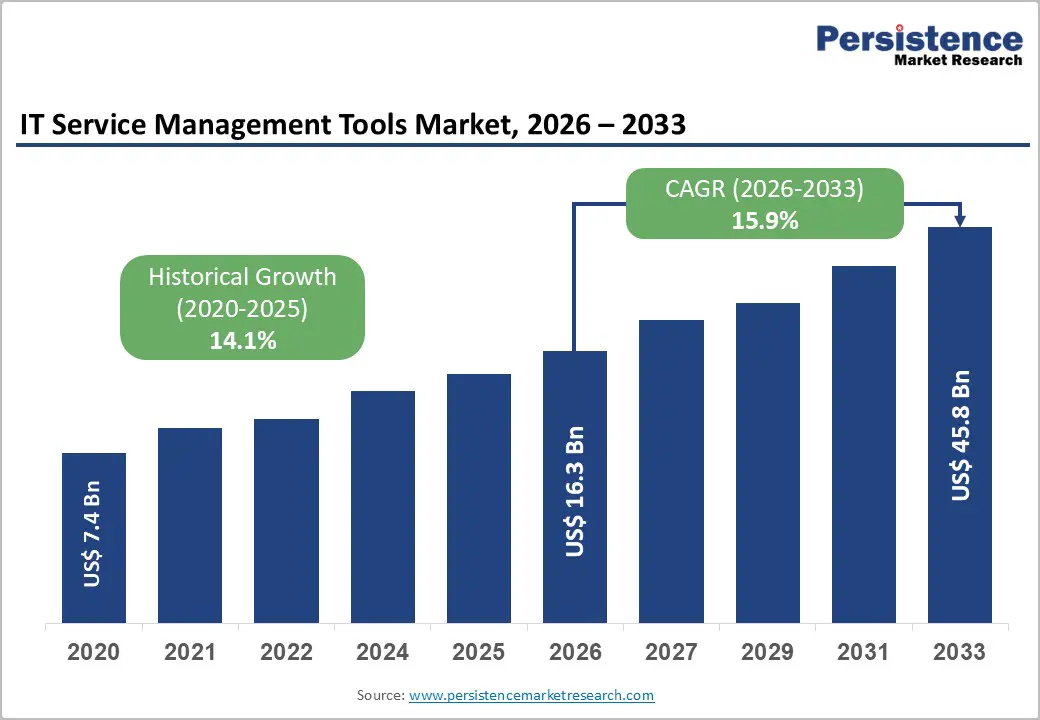

The global IT Service Management Tools market size is likely to be valued at US$ 16.3 Billion in 2026 and is expected to reach US$ 45.8 Billion by 2033, growing at a CAGR of 15.9% during the forecast period from 2026 to 2033. The market growth is driven primarily by accelerating digital transformation initiatives across industries and the critical need for organizations to streamline IT operations in increasingly complex hybrid and multi-cloud environments.

Key Market Highlights

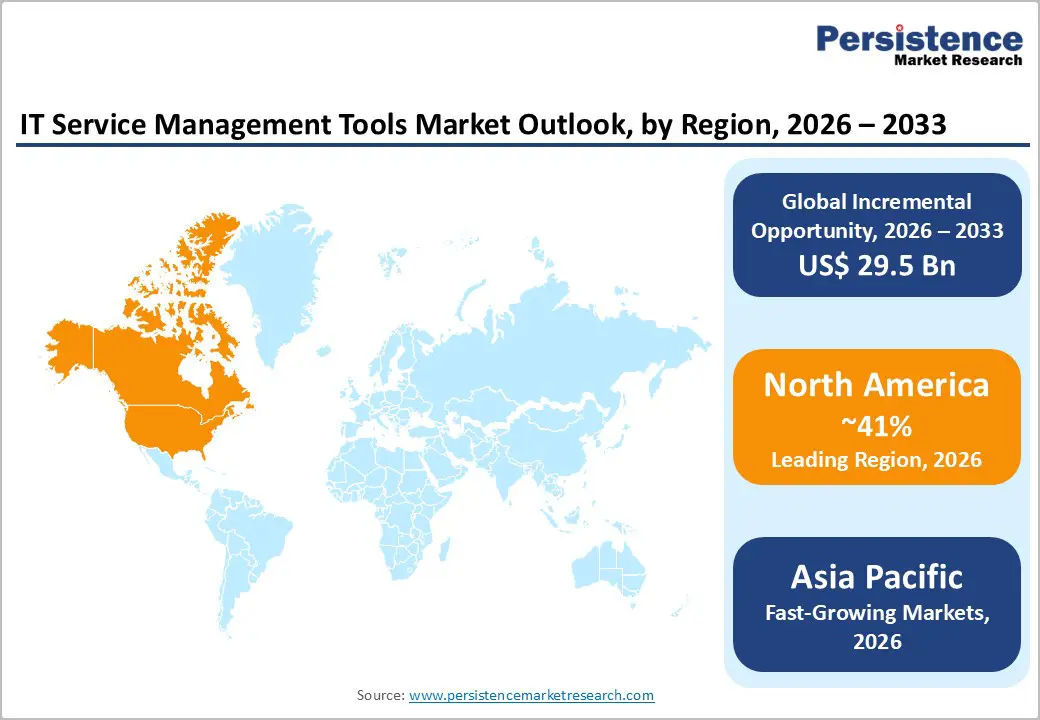

- Leading Region: North America dominates the global ITSM market with 41% market share in 2024, driven by mature IT infrastructure, early cloud adoption, strong presence of major ITSM vendors, and regulatory requirements including HIPAA and PCI DSS that mandate comprehensive IT service management governance and compliance capabilities.

- Fastest Growing Region: Asia Pacific represents the fastest-growing regional market with India expected to achieve 16.9% CAGR, driven by rapid digital transformation, expanding IT services industries, manufacturing modernization through Industry 4.0, and widespread cloud adoption accelerating beyond global average growth rates.

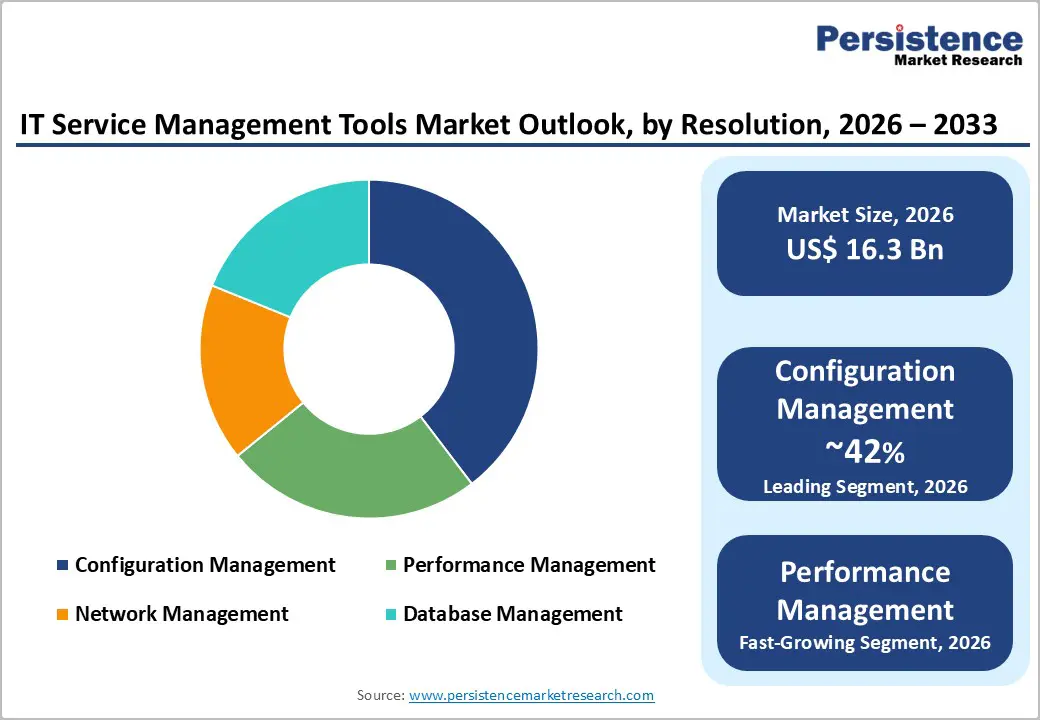

- Dominant Segment: Configuration Management maintains approximately 42% of the ITSM market, as organizations recognize that maintaining accurate asset inventories and tracking configuration changes across hybrid and multi-cloud environments is fundamental to effective IT operations and compliance management.

- Fastest Growing Segment: Artificial Intelligence-driven incident management and automation capabilities represent the fastest-growing functional segment, with market participants investing heavily in predictive analytics, automated ticket resolution, and intelligent routing that reduce manual effort and accelerate service delivery significantly.

- Key Market Opportunity: SME adoption of cloud-based ITSM solutions presents substantial growth opportunity, as subscription-based SaaS models with low-code configuration reduce implementation barriers, enabling organizations with limited IT resources to deploy enterprise-grade ITSM capabilities and achieve 20% operating cost reductions.

| Key Insights | Details |

|---|---|

|

IT Service Management Tools Market Size (2026E) |

US$ 16.3 Billion |

|

Market Value Forecast (2033F) |

US$ 45.8 Billion |

|

Projected Growth CAGR(2026-2033) |

15.9% |

|

Historical Market Growth (2020-2025) |

14.1% |

Market Dynamics

Market Growth Drivers

Increasing IT Infrastructure Complexity and Digital Transformation Initiatives

Organizations across all sectors are undergoing rapid digital transformation, which has significantly increased the complexity of IT environments. The shift toward hybrid and multi-cloud infrastructure, combined with the proliferation of Software as a Service (SaaS) applications and microservices architectures, requires sophisticated management tools to maintain visibility and control. According to industry data, North American organizations spent over US$ 11 Billion on ITSM solutions in recent years as they invested heavily in modernizing their IT operations.

The need for real-time monitoring, automated incident response, and comprehensive asset tracking across distributed infrastructure is compelling organizations to adopt comprehensive ITSM platforms. Cloud-native architectures and containerized workloads have further amplified the demand for intelligent ITSM tools that can handle ephemeral resources and dynamic environments, making automation and AI-driven capabilities essential features rather than optional add-ons.

Expansion of Remote and Hybrid Work Models Requiring Seamless Service Delivery

The permanent shift toward hybrid and remote work arrangements has fundamentally transformed how IT services must be delivered. Distributed teams spanning multiple time zones and locations require IT support that operates continuously without geographic constraints. Cloud-based ITSM platforms have become indispensable for enabling IT teams to manage service requests, incidents, and changes from anywhere while maintaining consistent quality. Research indicates that 95% of Indian IT companies are planning to shift to cloud-based ITSM infrastructure by 2028, reflecting the global trend toward cloud adoption.

Self-service portals and AI-powered virtual agents embedded within ITSM platforms have become critical in reducing the burden on helpdesks while improving end-user satisfaction. The ability to access IT services remotely, combined with mobile-first design approaches, ensures that employees can resolve issues independently or receive prompt support regardless of their location, directly supporting business continuity and employee productivity in distributed work environments.

Market Restraints

High Implementation Complexity and Integration Challenges with Legacy Systems

Despite the clear benefits of modern ITSM solutions, organizations face substantial challenges in implementing and integrating these platforms with existing legacy IT infrastructure. The complexity of deploying ITSM solutions across heterogeneous environments increases both project timelines and costs, particularly when organizations must maintain operations during migration phases. Legacy systems often lack standardized APIs and modern data exchange protocols, requiring custom development and manual workarounds that increase implementation expenses and extend time-to-value.

Organizations frequently struggle with Configuration Management Database (CMDB) accuracy and maintenance, as discovering and mapping all IT assets and their interdependencies across legacy and modern systems requires significant effort and specialized expertise. The reluctance to disrupt existing systems that are performing critical business functions, combined with the need for extensive change management and staff retraining, creates organizational resistance that slows adoption and increases implementation costs. These implementation challenges result in longer sales cycles and higher total cost of ownership for enterprises, particularly smaller organizations with limited IT resources.

Data Security, Privacy Compliance, and Regulatory Concerns Deterring Cloud Migration

Security and compliance concerns remain significant obstacles preventing some organizations from adopting cloud-based ITSM solutions. Regulations such as GDPR (General Data Protection Regulation) in Europe and HIPAA (Health Insurance Portability and Accountability Act) in the United States impose strict requirements on how sensitive data must be handled, stored, and protected. Many organizations, particularly in highly regulated industries such as financial services and healthcare, maintain concerns about data sovereignty and control when moving ITSM workloads to cloud platforms.

The responsibility of cloud providers to maintain robust security controls, ensure data residency compliance, and provide detailed audit trails creates apprehension among risk-conscious enterprises. Additionally, organizations must ensure that ITSM platforms maintain compliance with evolving regulatory frameworks across multiple jurisdictions, creating complex compliance management requirements that some legacy on-premises solutions can address more easily. The potential costs of non-compliance, which can reach millions of dollars in fines, make organizations cautious about cloud migration despite the operational advantages such solutions offer.

Market Opportunities

AI and Machine Learning Integration for Predictive Analytics and Automated Service Resolution

The integration of artificial intelligence and machine learning into ITSM platforms represents one of the most significant growth opportunities in the market. AI-driven capabilities enable predictive incident detection, allowing IT teams to identify and resolve potential issues before they impact end-users, significantly reducing mean time to resolution (MTTR) and improving service quality. Research findings indicate that 86% of IT professionals believe AI-powered technology is essential for making IT organizations more efficient, and 65% predict that AI and automation will improve overall IT service quality.

Vendors such as ServiceNow have launched AI-powered solutions like virtual agents that can automatically categorize incidents with 99% accuracy and intelligently route tickets to appropriate teams, reducing manual intervention. ManageEngine has demonstrated that deploying AI-driven platforms can improve query resolution rates from 75% to 98.8%, while IBM and BMC Software continue investing heavily in AI capabilities for predictive service management. The growing adoption of Large Language Models (LLMs) and generative AI technologies is creating opportunities for vendors to embed conversational AI agents within ITSM platforms, enabling natural-language ticket creation and knowledge base searches that dramatically enhance user experience and operational efficiency.

Rapid Adoption Among Small and Medium-Sized Enterprises (SMEs) Driving Subscription-Based Growth

SMEs represent a rapidly expanding market segment for cloud-based ITSM solutions, as these organizations increasingly recognize the necessity of professional IT service management despite limited IT resources and budgets. The shift toward subscription-based Software as a Service (SaaS) pricing models has fundamentally democratized access to enterprise-grade ITSM capabilities, enabling SMEs to deploy sophisticated tools without massive upfront capital investments. Research data shows that SMEs can reduce operating costs by 20% and increase customer satisfaction by 15% after deploying cloud-based ITSM solutions with automation capabilities.

The proliferation of low-code and no-code configuration options enables SMEs to customize solutions without extensive professional services engagements, reducing implementation timelines and costs. Vendors are recognizing this opportunity and developing streamlined offerings specifically targeting SMEs, with simplified user interfaces, predefined best-practice workflows, and bundled services that lower barriers to entry. As SMEs increasingly adopt cloud-first strategies and remote work models become standardized across organizational sizes, the demand for affordable, scalable, easy-to-deploy ITSM solutions continues to accelerate, creating substantial revenue opportunities for vendors offering SME-focused offerings.

Category-wise Insights

Configuration Management Analysis

Configuration Management represents the foundational capability within ITSM platforms, responsible for maintaining accurate inventories of all IT assets and their interdependencies within the Configuration Management Database (CMDB). This segment holds approximately 42% of the ITSM market, as organizations recognize that maintaining a single source of truth for all IT assets is critical for effective incident management, change control, and service continuity. The importance of Configuration Management has increased substantially as organizations manage hybrid and multi-cloud infrastructure, where automatic discovery of configuration items (CIs) across diverse cloud providers, virtualized environments, and on-premises systems is essential.

Modern ITSM platforms employ advanced discovery engines and continuous monitoring capabilities to automatically detect configuration changes, flag policy drift, and maintain real-time CMDB accuracy without manual intervention. The segment is being driven by increased regulatory compliance requirements that mandate detailed audit trails of all configuration changes, making automated configuration management essential for organizations subject to HIPAA, PCI DSS, and SOX compliance obligations.

Performance Management Analysis

Performance Management capabilities within ITSM platforms enable organizations to monitor, analyze, and optimize the performance of IT services and underlying infrastructure components. This segment captures approximately 28% of the overall ITSM market, as organizations recognize that proactive performance monitoring directly impacts user experience and business outcomes. Performance Management modules provide real-time visibility into system performance metrics, service availability, and capacity utilization across hybrid infrastructure environments. The segment is growing rapidly as organizations adopt more sophisticated monitoring approaches to manage the performance implications of containerized workloads, serverless architectures, and distributed microservices.

Advanced analytics capabilities within Performance Management enable IT teams to identify performance trends, predict capacity constraints, and implement optimization measures before service degradation occurs. Integration of Performance Management with incident management workflows enables organizations to automatically trigger incident tickets when performance thresholds are breached, creating closed-loop automation that accelerates problem resolution. The increasing adoption of AI-driven analytics within Performance Management modules enables automatic baselining of normal performance patterns and detection of anomalies that may indicate emerging issues.

Network Management Analysis

Network Management represents approximately 18% of the ITSM market and focuses on managing the configuration, performance monitoring, and troubleshooting of network infrastructure components including routers, switches, firewalls, and network services. As organizations deploy increasingly complex network topologies spanning multiple cloud providers, on-premises data centers, and edge computing sites, comprehensive Network Management capabilities have become essential. The segment is experiencing significant growth driven by the expansion of 5G infrastructure deployments, which require sophisticated management tools to monitor performance across broader geographic areas with lower latency requirements.

Network Management capabilities integrated with ITSM platforms enable IT teams to correlate network incidents with service impact, accelerating root cause analysis and enabling faster resolution. The growth of Software-Defined Networking (SDN) and Network Function Virtualization (NFV) technologies has increased the complexity of network management, as traditional network configuration and monitoring approaches are insufficient for dynamic, software-controlled network environments. Vendors are enhancing Network Management capabilities with advanced visualization tools, automated configuration management, and AI-driven anomaly detection to provide comprehensive visibility and control over increasingly complex network infrastructures.

Database Management Analysis

Database Management within ITSM platforms addresses the unique requirements of managing database infrastructure, performance optimization, and ensuring data availability and compliance. This segment accounts for approximately 12% of the ITSM market and is experiencing strong growth driven by the critical importance of databases to modern applications and the increasing complexity of multi-database environments. Organizations often maintain diverse database platforms including SQL Server, Oracle, PostgreSQL, MongoDB, and NoSQL databases deployed across cloud and on-premises environments, requiring integrated management capabilities. Database Management modules provide monitoring of database performance, capacity planning, automated backup and recovery management, and security compliance tracking essential for protecting sensitive organizational data.

The segment is growing as organizations adopt more sophisticated database technologies, implement real-time analytics requirements, and maintain compliance with stringent data protection regulations. Automation of routine database management tasks such as patching, backup verification, and performance optimization is becoming essential as databases grow larger and more complex, making specialized Database Management capabilities within ITSM platforms increasingly valuable.

Regional Insights

North America IT Service Management Tools Market Trends

North America maintains the largest market share in the global ITSM market, commanding approximately 41% of worldwide revenue in 2024 and representing the most mature and developed market for IT service management solutions. The region's dominance is supported by the strong presence of leading software vendors such as ServiceNow, IBM, Atlassian, BMC Software, and CA Technologies, all of which maintain significant operations and customer bases in North America.

The U.S. government has implemented multiple cybersecurity initiatives including the National Strategy for Trusted Identities in Cyberspace and the NIST Cybersecurity Framework, which have encouraged organizations across both private and public sectors to invest substantially in improving their IT operations and security posture. Organizations in North America are placing greater emphasis on improving both internal and external customer experiences, driving adoption of ITSM platforms that offer self-service portals, AI-powered chatbots, and automation tools that resolve issues rapidly.

Europe IT Service Management Tools Market Trends

Europe represents the second-largest market for ITSM solutions globally, with strong adoption driven by the implementation of the General Data Protection Regulation (GDPR), which has fundamentally changed how organizations manage and protect data. The region's emphasis on data privacy and regulatory compliance has made comprehensive ITSM solutions essential for demonstrating adherence to stringent requirements around data handling, access controls, and audit documentation.

Germany, United Kingdom, France, Spain, and other major European economies are experiencing strong ITSM market growth as organizations recognize that robust IT service management is critical for maintaining compliance with GDPR and ensuring business continuity across the increasingly complex regulatory environment. European enterprises have demonstrated particular interest in ITSM solutions that provide comprehensive audit trails, detailed access logging, and automated compliance reporting capabilities that facilitate regulatory inspections and demonstrate due diligence in data protection.

Asia Pacific IT Service Management Tools Market Trends

Asia Pacific represents the fastest-growing regional market for ITSM solutions, with anticipated growth significantly exceeding rates in mature markets as digital transformation initiatives accelerate across the region. India, China, Japan, and ASEAN countries are experiencing particularly strong growth driven by expanding IT industries, increasing cloud adoption, and digital transformation initiatives across manufacturing, financial services, and public sector organizations.

India's digital economy is growing at an exceptional pace, with research indicating that India's ITSM market is expected to grow at a CAGR of 16.9%, significantly exceeding the global average, as organizations increasingly automate IT processes to improve service efficiency and customer satisfaction. The region is characterized by significant manufacturing sector presence, and adoption of Industry 4.0 principles is driving demand for sophisticated ITSM capabilities that manage the IT infrastructure supporting modern production environments.

Competitive Landscape

Market Structure Analysis

The global ITSM market demonstrates moderate concentration with dominant tier-one vendors capturing significant market share while numerous smaller players serve niche segments and specific customer requirements. Tier-one vendors including ServiceNow, IBM, BMC Software, and Atlassian maintain approximately 40-45% of the global market share, supported by their comprehensive solution portfolios, established customer relationships, and continuous innovation in AI and automation capabilities. ServiceNow has established clear market leadership with 44.4% market share among the top 10 ITSM vendors and is aggressively expanding its AI capabilities, recently expanding its partnership with Google Cloud to integrate generative AI across enterprise technology stacks and create AI-enhanced experiences for millions of users.

Key Market Developments

- January 2025: ServiceNow and Google Cloud announced a comprehensive expansion of their partnership, integrating generative AI across enterprise technology stacks. ServiceNow Now Platform, ITSM, CRM, and SIR solutions are now available on Google Cloud Marketplace, enabling AI-enhanced user experiences through BigQuery enterprise data insights and Google Workspace integration.

- November 2024: Atlassian introduced new functionalities in Jira Service Management focused on automating alert and issue remediation flows, significantly enhancing operational efficiency for organizations managing complex IT environments and enabling faster resolution of infrastructure incidents.

- March 2025: ManageEngine's ServiceDesk Plus platform achieved significant LLM deployment, processing 315 million tokens and executing 140,000+ AI actions, demonstrating the vendor's commitment to embedded AI capabilities without reliance on third-party APIs.

Companies Covered in IT Service Management Tools Market

- ServiceNow, Inc.

- Atlassian Corporation

- IBM Corporation

- CA Technologies

- BMC Software, Inc.

- Ivanti Software

- ASG Software Solutions

- Axios Systems

- SAP SE

- Cherwell Software

- Broadcom Inc.

- Zendesk, Inc.

- SolarWinds Corporation

- GoTo

- ManageEngine

Frequently Asked Questions

The global IT Service Management Tools market is expected to reach US$ 45.8 Billion by 2033, growing from US$ 16.3 Billion in 2026 at a CAGR of 15.9%, driven by increasing digital transformation initiatives, cloud adoption acceleration, and integration of artificial intelligence capabilities across enterprise IT operations.

Key demand drivers include the exponential increase in IT infrastructure complexity as organizations adopt hybrid and multi-cloud architectures, the permanent shift toward remote and hybrid work models requiring seamless distributed service delivery, the critical need for regulatory compliance with GDPR and HIPAA frameworks, and the integration of AI and machine learning technologies enabling predictive analytics and automated service resolution.

Configuration Management holds the largest market share at approximately 42%, as organizations recognize that maintaining accurate Configuration Management Databases (CMDBs) tracking all IT assets and their interdependencies is essential for effective incident resolution, change management, and demonstrating compliance with regulatory requirements.

North America dominates with 41% of the global market share, supported by the presence of major ITSM vendors, strong investment in digital transformation, mature IT infrastructure, and stringent regulatory requirements that necessitate comprehensive IT service management governance and compliance capabilities.

Key opportunities include the rapid adoption of AI and machine learning technologies for predictive incident management and automated service resolution reducing mean time to resolution by 40-60%, and the expansion of cloud-based ITSM adoption among small and medium-sized enterprises that can reduce operating costs by 20% through subscription-based SaaS models.

Market leaders include ServiceNow with 44.4% share among top 10 vendors, Atlassian, BMC Software, Ivanti Software, ManageEngine, Zendesk, IBM Corporation, CA Technologies, SolarWinds, and GoTo,