- Plastics, Polymers & Resins

- Thermoplastic Decorative Films Market

Thermoplastic Decorative Films Market Size, Share, and Growth Forecast 2026 - 2033

Thermoplastic Decorative Films Market Function (2D Lamination, 3D Lamination, Self-Adhesive Films), Installation (New, Re-decoration), Material Type (Vinyl and Polyvinyl Chloride, PET, Polypropylene, TPU, TPO, TPE), Application (Furniture, Doors & Windows, Automotive Interior and Exterior), End-user (Residential, Commercial, Transportation, Institutional), and Regional Analysis, 2026 - 2033

Thermoplastic Decorative Films Market Size and Trend Analysis

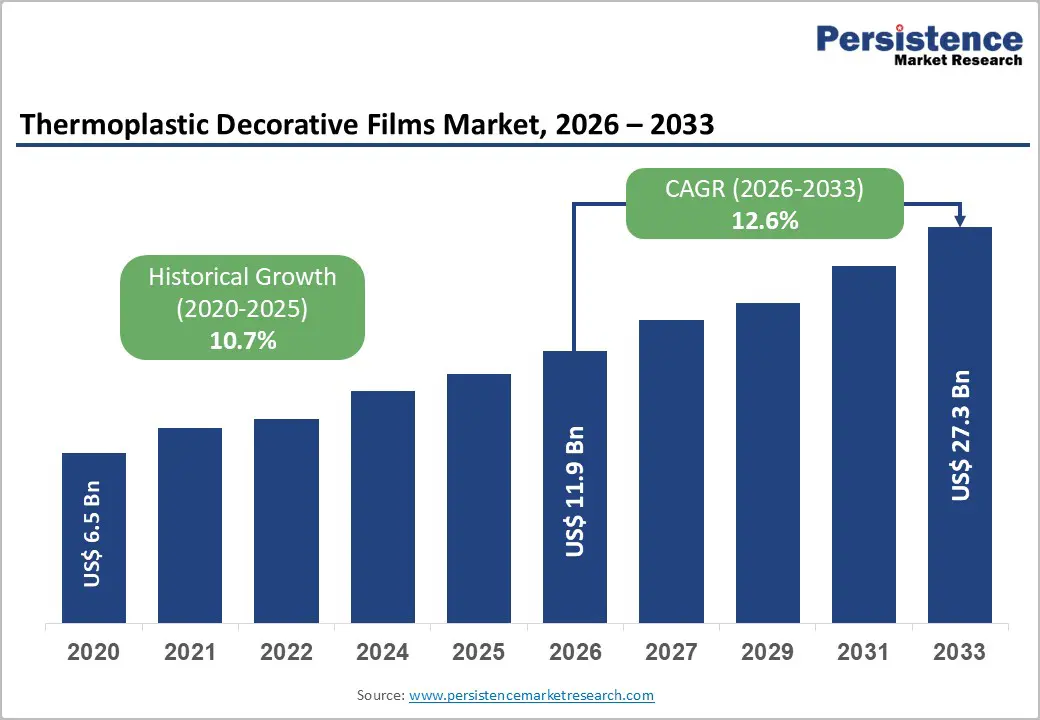

The global thermoplastic decorative films market size is likely to be valued at US$ 11.9 billion in 2026 and is expected to reach US$ 27.3 billion by 2033, growing at a CAGR of 12.6% during the forecast period from 2026 to 2033.

This rapid expansion is driven by rising demand for aesthetic, cost-effective, and sustainable surface-finishing solutions in furniture, doors & windows, and automotive interiors, supported by urbanization, infrastructure development, and design-driven consumer preferences.

Key Industry Highlights:

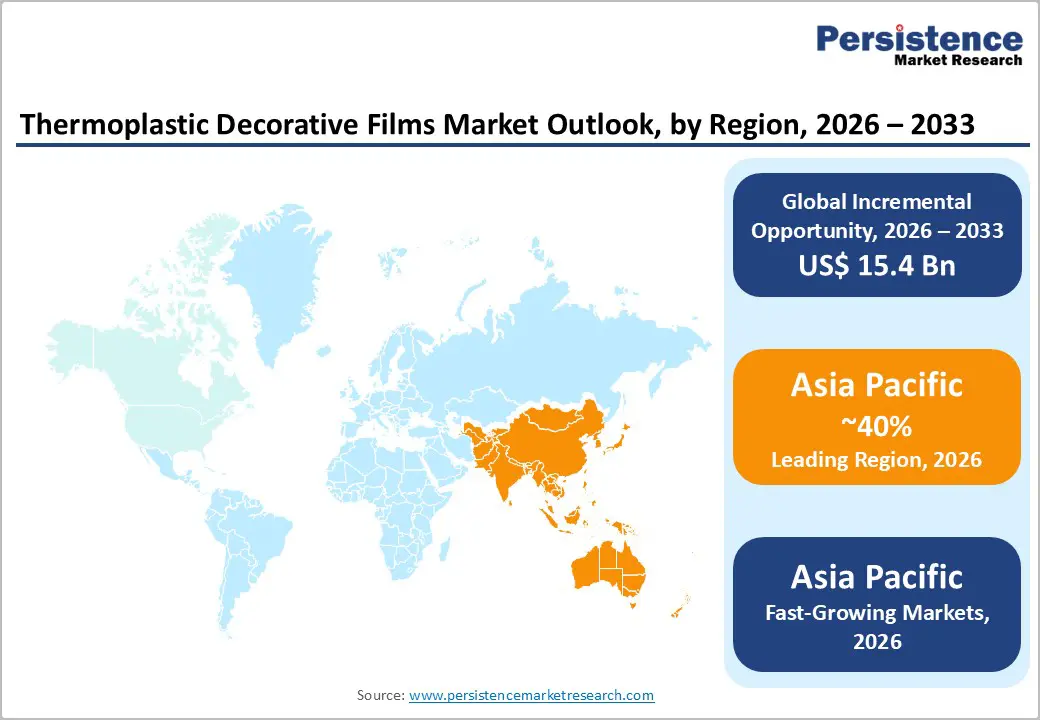

- Leading Region: Asia Pacific holds the largest market share with 40% share, driven by rapid urbanization, expanding furniture/construction sectors, EV production growth, and policy-led infrastructure spending in China, India, Japan, and ASEAN countries.

- Fastest-Growing Region: Asia Pacific is the fastest-growing region with rising CAGR of 8.9%, due to booming residential construction, industrialization, low-cost manufacturing bases, rising disposable incomes, and strong demand for modern interior finishes across commercial and residential segments.

- Leading Segment: The furniture application segment holds 30% share, and leads demand as decorative films are extensively used to provide premium finishes on wardrobes, kitchen units, tables, and cabinets at lower cost than solid wood or laminates.

- Fastest-Growing Segment: The residential segment is growing fastest as home renovation, DIY décor, and self-adhesive film adoption surge, supported by higher home-improvement spending and modular interior trends globally.

- Key Market Opportunity: Demand for PVC-free, low VOC, and recyclable decorative films presents a strong growth opportunity as sustainability goals, green-building standards, and ESG commitments drive preference for eco-friendly surface materials.

| Key Insights | Details |

|---|---|

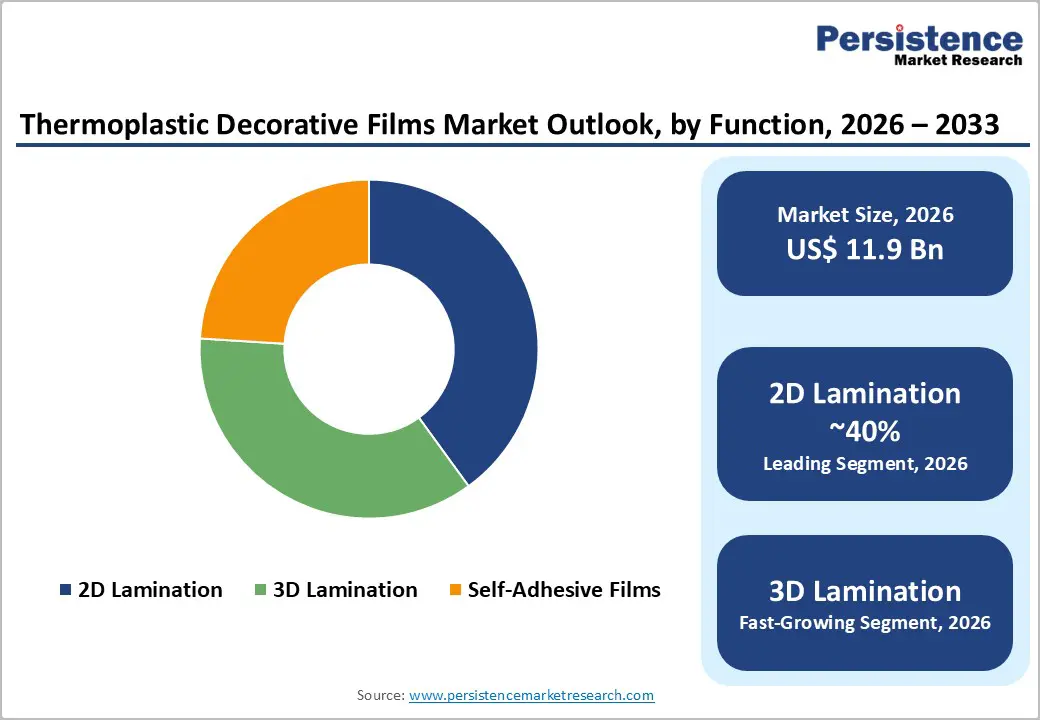

| Thermoplastic Decorative Films Market Size (2026E) | US$ 11.9 Billion |

| Market Value Forecast (2033F) | US$ 27.3 Billion |

| Projected Growth CAGR (2026 - 2033) | 12.6% |

| Historical Market Growth (2020 - 2025) | 10.7% |

Market Dynamics

Drivers - Growing Preference for Stylish, Affordable, and Durable Surface Finishes Driving Decorative Film Adoption across Industries

A key growth driver for the Thermoplastic Decorative Films Market is the rising preference for visually appealing, high-quality, and affordable surface finishes across furniture, doors & windows, and automotive interiors. Consumers and developers increasingly choose wood-grain, marble, metallic, and high-gloss textures that replicate premium materials at significantly lower costs.

Compared with solid wood, laminates, and paint, decorative films offer strong consistency in color, texture, and surface durability while reducing overall material and labor expenses by nearly 30%. These benefits make them especially attractive for large-scale residential and commercial projects. Rapid urbanization and rising home-improvement spending in Asia Pacific and Latin America are further accelerating adoption. As buyers seek modern design without premium pricing, thermoplastic decorative films are becoming a preferred solution for both new construction and renovation projects.

Rapid Expansion of Furniture, Construction, and Automotive Sectors Creating Strong and Consistent Demand for Decorative Films

The expanding furniture, construction, and automotive industries are major contributors to rising demand for thermoplastic decorative films. The global furniture sector continues to grow steadily due to urban living, higher disposable incomes, and the increasing popularity of online retail platforms. At the same time, residential and commercial construction is rising as governments invest in infrastructure, housing programs, and smart-city developments.

In the automotive industry, manufacturers are placing greater focus on interior design, premium finishes, and brand differentiation, which has increased demand for decorative surface solutions. Thermoplastic films are widely used in dashboards, door panels, cabinets, and molded furniture components due to their durability and design flexibility. Together, these fast-growing sectors are creating sustained and diversified demand across residential, commercial, and transportation applications worldwide.

Restraints - Rising Environmental Regulations on PVC Materials Encouraging Shift Toward Safer and More Sustainable Decorative Film Alternatives

Environmental concerns surrounding polyvinyl chloride and vinyl-based decorative films represent a significant market restraint. Regulatory authorities such as European Chemicals Agency and U.S. Environmental Protection Agency are tightening controls on plasticizers, phthalates, and chemical additives used in PVC production. These measures aim to reduce health risks, improve recyclability, and lower environmental impact.

As a result, architects, furniture manufacturers, and developers are increasingly shifting toward alternative materials such as PET, polypropylene, and TPU films. Green building certifications are also promoting low-emission and recyclable materials in commercial projects. While PVC films remain cost-effective and durable, rising regulatory pressure and sustainability awareness may gradually slow growth in vinyl-dominated segments across Europe and North America.

High Price Sensitivity and Low-Cost Substitutes Limiting Decorative Film Penetration in Budget-Focused Market Segments

Another major limitation in the Thermoplastic Decorative Films Market is high price sensitivity, particularly in emerging economies. Although decorative films provide superior durability, moisture resistance, and design versatility, their initial cost remains higher than traditional finishes such as paint, laminates, and basic wood veneers. In low-income housing projects and budget furniture segments, cost remains the primary purchase factor, limiting widespread adoption of premium decorative films.

Additionally, local manufacturers often produce low-quality imitation films at significantly reduced prices, creating intense price competition. These alternatives can reduce demand for branded and high-performance films while compressing profit margins for established companies. As a result, market growth in price-conscious regions remains slower despite strong long-term performance advantages offered by thermoplastic decorative film solutions.

Opportunity - Strong Market Potential Emerging from Growing Demand for Recyclable, Low-VOC, and Eco-Friendly Decorative Film Materials

The growing focus on sustainability presents a strong opportunity for the Thermoplastic Decorative Films Market. Manufacturers are increasingly developing PVC-free, recyclable, and low-VOC film solutions using PET, polypropylene, TPU, and TPO materials. These alternatives support circular-economy goals while meeting stricter environmental regulations. Industry sustainability programs and green-building frameworks promoted by organizations such as the U.S. Green Building Council are encouraging wider adoption of eco-friendly surface materials across residential and commercial projects.

Consumers and corporate buyers are also prioritizing environmentally responsible products as part of their ESG commitments. As sustainability becomes a purchasing requirement rather than a preference, demand for premium recyclable decorative films is expected to rise, creating higher-margin growth opportunities for innovative manufacturers.

Increasing use of Advanced 3D Lamination and Self-Adhesive Films Supporting Customization and Faster Installation Trends

The rapid adoption of 3D lamination and self-adhesive decorative films is creating high-value growth opportunities across automotive interiors and furniture applications. These films allow seamless coverage of curved surfaces, complex designs, and molded components while reducing material waste and installation time.

In automotive manufacturing, they are widely used for dashboards, door trims, center consoles, and steering-wheel overlays to achieve premium finishes and enhanced durability. In furniture and interior décor, self-adhesive films support quick renovations and DIY projects, making them popular for retrofitting cabinets and panels. As design complexity, customization demand, and fast installation become industry priorities, these advanced film formats are expected to become the fastest-growing product segments within the Thermoplastic Decorative Films Market.

Category-wise Analysis

Function Insights

2D lamination remains the leading functional segment in the Thermoplastic Decorative Films Market, accounting for approximately 40% of total market value. Its dominance is driven by extensive use in flat furniture surfaces, wall panels, doors, and cabinetry where cost-effective finishing is required.

These films are commonly applied to MDF, plywood, and particleboard using hot or cold pressing techniques, delivering consistent color, surface texture, and long-term durability. Major manufacturers such as LG Hausys, Renolit, and Hanwha L&C have introduced high-resolution wood-grain and modern color finishes tailored for furniture markets. Their continuous innovation keeps 2D lamination as the backbone of volume demand across residential and commercial sectors.

Material Type Insights

Vinyl and PVC-based decorative films continue to dominate the material segment, accounting for nearly 50% of the Thermoplastic Decorative Films Market. Their popularity stems from excellent flexibility, moisture resistance, scratch durability, and ease of printing complex patterns. PVC films support high-definition wood-grain, marble, metallic, and gloss textures that closely replicate natural materials at lower cost. These properties make them the preferred choice for furniture, cabinetry, doors, and automotive interiors. However, increasing environmental scrutiny is encouraging manufacturers to gradually reduce reliance on conventional PVC by introducing recyclable alternatives. While vinyl will remain dominant in the near term due to affordability and performance, its market share may slowly decline as sustainable materials gain acceptance.

Application Insights

Furniture remains the largest application segment, contributing nearly 30% of total market demand. Decorative films are extensively used in wardrobes, kitchen cabinets, tables, shelving, and modular furniture to provide attractive finishes with improved durability. By replacing solid wood and laminates, films significantly lower production costs while maintaining premium visual appeal.

Rising urban populations, smaller living spaces, and demand for modular furniture are driving higher usage of surface-finished panels. Growth in home renovation and interior décor spending further supports this trend, especially across Asia Pacific and Latin America. As manufacturers continue offering diverse textures and easy-maintenance surfaces, furniture applications are expected to remain the primary revenue driver of the thermoplastic decorative films market.

End-user Insights

The residential sector is emerging as one of the fastest-growing end-use segments, currently holding around 25% of total market demand. Growth is supported by increasing home renovation projects, modular kitchens, bathroom remodeling, and DIY décor activities. Homeowners favor decorative films for their affordability, easy installation, moisture resistance, and modern appearance.

Self-adhesive films are particularly popular for quick upgrades and rental property refurbishments. Expanding residential construction driven by urban migration and rising income levels further strengthens demand. Online platforms offering customized film designs are also accelerating consumer adoption. As lifestyle upgrades and personalized interiors become mainstream, the residential segment is expected to grow faster than the overall market average.

Regional Insights

North America Thermoplastic Decorative Films Market Trends

North America represents a mature and design-focused market, led primarily by the United States. Strong emphasis on interior aesthetics, sustainability, and premium automotive design continues to drive demand. Regulatory frameworks promoting low-VOC materials are encouraging adoption of environmentally friendly decorative films in residential and commercial projects. Automotive manufacturers are increasingly integrating decorative films into electric vehicle interiors for lightweight and modern finishes.

The region also benefits from advanced manufacturing technologies and product innovation, with companies such as Avery Dennison, Klockner Pentaplast, and Omnova Solutions developing high-performance and recyclable film solutions. These factors position North America as a high-value, innovation-driven market with steady long-term growth.

Europe Thermoplastic Decorative Films Market Trends

Europe is a sustainability-driven and regulation-focused market for thermoplastic decorative films. Countries such as Germany, the United Kingdom, France, Spain, and Italy lead demand across furniture, automotive, and construction sectors. Strict environmental standards require low-emission and recyclable surface materials, encouraging widespread adoption of PVC-free decorative films.

Green-building certifications and circular-economy policies further accelerate this shift. Automotive manufacturers in Germany and furniture producers across Western Europe rely heavily on both 2D and 3D lamination technologies for premium finishes. Strong ESG commitments from corporations combined with regulatory consistency across the region continue to create stable growth opportunities, particularly for eco-friendly and high-performance decorative film products.

Asia Pacific Thermoplastic Decorative Films Market Trends

Asia Pacific is the fastest-growing and largest regional market, driven by rapid urbanization, expanding manufacturing bases, and rising consumer spending. China, India, Japan, and ASEAN countries dominate demand across furniture, construction, and automotive applications. Government-led housing programs, smart-city initiatives, and infrastructure investments are boosting residential and commercial construction.

Furniture manufacturing hubs in Vietnam, Thailand, and Indonesia are increasing usage of decorative films for export-oriented production. Meanwhile, growth in electric vehicle manufacturing across China and India is fueling demand for premium interior surface solutions. Cost-effective labor, rising middle-class populations, and strong industrial expansion position Asia Pacific as the key growth engine of the global thermoplastic decorative films market.

Competitive Landscape

The global thermoplastic decorative films market shows moderate consolidation, with a group of global manufacturers controlling significant production capacity alongside numerous regional converters and printers. Leading players focus on proprietary extrusion technologies, surface coatings, and high-definition printing to enhance product performance and design realism. Companies are increasingly offering integrated solutions that combine films with adhesives, primers, and customized textures to improve installation efficiency.

Sustainability has become a core competitive differentiator, with strong investment in recyclable materials and low-VOC formulations. Digital printing, rapid prototyping, and on-demand customization are also reshaping business models. Overall, competitive advantage is shifting toward companies with strong R&D capabilities, regulatory expertise, scalable manufacturing, and eco-friendly innovation strategies.

Key Developments:

- In May 2025: LG Hausys introduced a new PVC-free thermoplastic decorative film designed for furniture and doors & windows applications, offering low VOC emissions and enhanced scratch resistance to appeal to green-building projects and eco-conscious residential buyers, reinforcing its market leadership.

- In October 2024: Renolit announced a €40 million investment to expand decorative film production capacity at its European facility, adding new extrusion lines and digital printing systems to meet rising demand from furniture, construction, and automotive customers and improve product flexibility.

- In February 2023: Avery Dennison introduced an advanced self-adhesive thermoplastic decorative film tailored for automotive interiors, providing high formability, scratch resistance, and easy installation to support electric-vehicle manufacturers seeking premium, durable interior trim solutions.

Companies Covered in Thermoplastic Decorative Films Market

- LG Hausys, Ltd.

- Renolit

- Hanwha L&C

- Klockner Pentaplast Group

- Omnova Solutions

- Avery Dennison

- Peiyu Plastic Corporation

- Mondoplastico S.p.A.

- AVI Global Plast Pvt. Ltd.

- Ergis Group

- Macro Plastic Sdn. Bhd.

- Jindal Group

- Konrad Hornschuch AG

- Fine Decor GmbH

- Alfatherm s.p.a.

- Covestro AG

- SABIC

- Eastman Chemical Company

- Toray Industries, Inc.

- Mitsubishi Chemical Group Corporation

Frequently Asked Questions

The global Thermoplastic Decorative Films Market is valued at US$ 11.9 Billion in 2026 and is projected to reach US$ 27.3 Billion by 2033, growing at a CAGR of 12.6% from 2026 to 2033, with a historical CAGR of 10.7% between 2020 and 2025.

Key demand drivers include rising demand for aesthetic and cost-effective surface finishes, growth of furniture, construction, and automotive sectors, and urbanization, which drive adoption of thermoplastic decorative films in furniture, doors & windows, and automotive interiors.

The 2D lamination segment is the leading function category, capturing 40% of demand due to its widespread use in flat-panel furniture, doors & windows, and wall panels.

Asia Pacific is the largest regional market for thermoplastic decorative films, accounting for roughly 40% of global value, driven by urbanization, furniture, construction, and automotive expansion in China, Japan, India, and ASEAN countries.

A key opportunity lies in the shift toward sustainable, recyclable, and PVC-free thermoplastic decorative films aligned with green-building certifications and circular-economy principles, particularly in Europe and North America.

Leading players include LG Hausys, Ltd., Renolit, Hanwha L&C, Klockner Pentaplast Group, Omnova Solutions, Avery Dennison, Peiyu Plastic Corporation, Mondoplastico S.p.A., AVI Global Plast Pvt. Ltd., Ergis Group, Macro Plastic Sdn. Bhd., Jindal Group, Konrad Hornschuch AG, Fine Decor GmbH, and Alfatherm s.p.a., among others.