- Inks, Coatings, Adhesives & Sealants (ICAS)

- Decorative Films and Foils Market

Decorative Films and Foils Market Size, Share, and Growth Forecast, 2025 - 2032

Decorative Films and Foils Market By Material Type (PVC Films, Polyester (BOPET) Films, Others), Product Type (Self-Adhesive Films, Laminates & Over-Laminates, Others), Application, and Regional Analysis for 2025 - 2032

Decorative Films and Foils Market Size and Trends Analysis

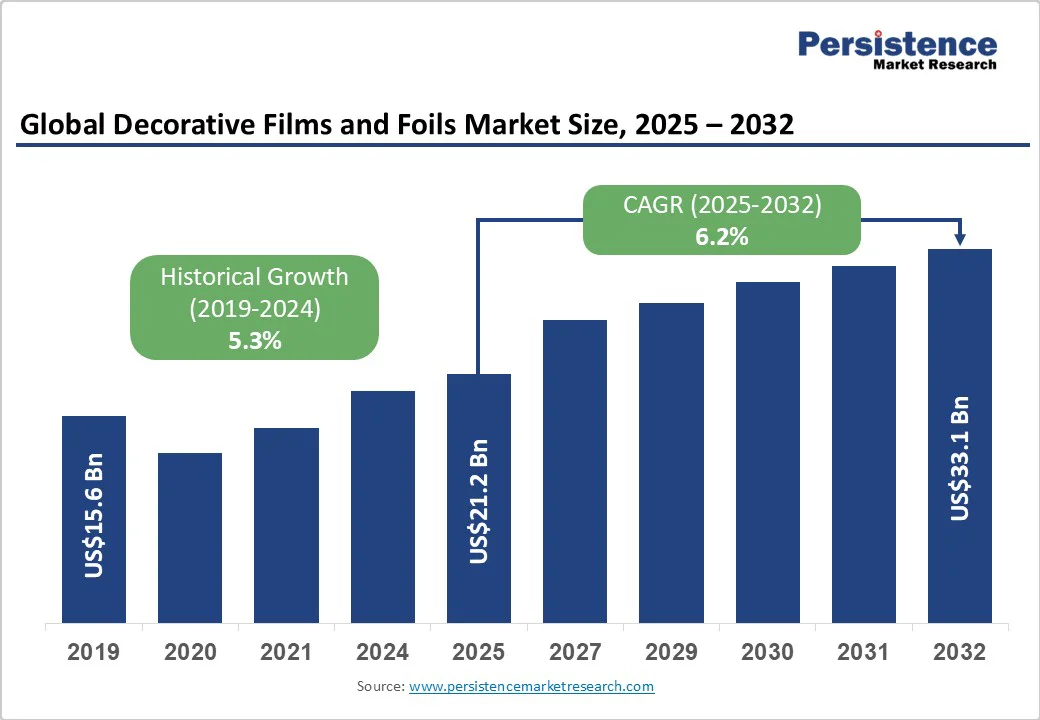

The global decorative films and foils market size was valued at US$21.2 Billion in 2025 and is projected to reach US$33.1 Billion by 2032, growing at a CAGR of 6.2% during the forecast period from 2025 to 2032, driven by the rising demand for cost-efficient aesthetic enhancements in residential and commercial interiors, expansion of automotive and electronics applications, and increasing adoption of digitally printable and recyclable films.

The shift toward energy-efficient, lightweight, and sustainable materials has elevated decorative films as a preferred alternative to laminates and veneers. Regulatory emphasis on eco-design and recyclability, along with expanding manufacturing capacity in Asia Pacific, underpins sustained market expansion.

Key Industry Highlights

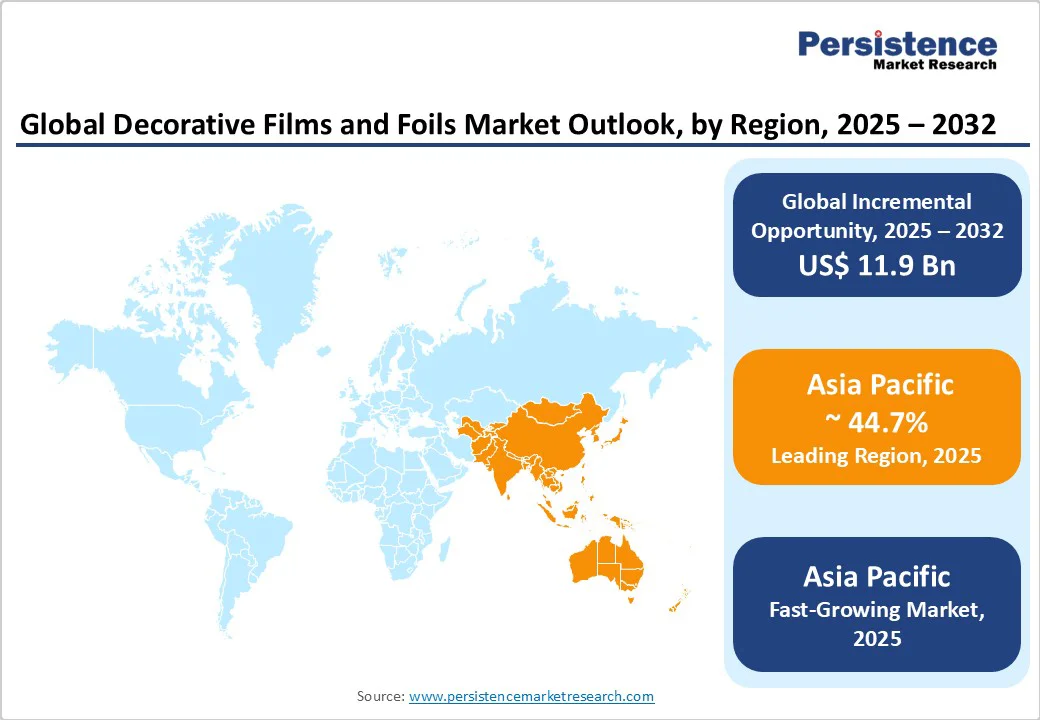

- Leading Region: Asia Pacific dominates the global market, accounting for approximately 44.7% of total market consumption in 2025, driven by large manufacturing bases, urbanization, and growing construction and furniture industries.

- Fastest-Growing Region: Asia Pacific is also the fastest-growing region, fueled by export opportunities, low-cost production, and high adoption of innovative and sustainable film solutions.

- Investment Plans: Major investment activity focuses on capacity expansion, digital printing integration, and sustainable product lines. Examples include LG Hausys’ expansion of its Deco Foil Division in 2024 and Cosmo Films’ PVC-free product launch in 2024, supporting high-demand residential, commercial, and automotive applications.

- Dominant Material Type: PVC and Polyester (BOPET) remain the leading material segment, representing 62% of market revenue in 2025, preferred for wall panels, furniture laminates, and cabinetry overlays due to versatility, durability, and cost-effectiveness.

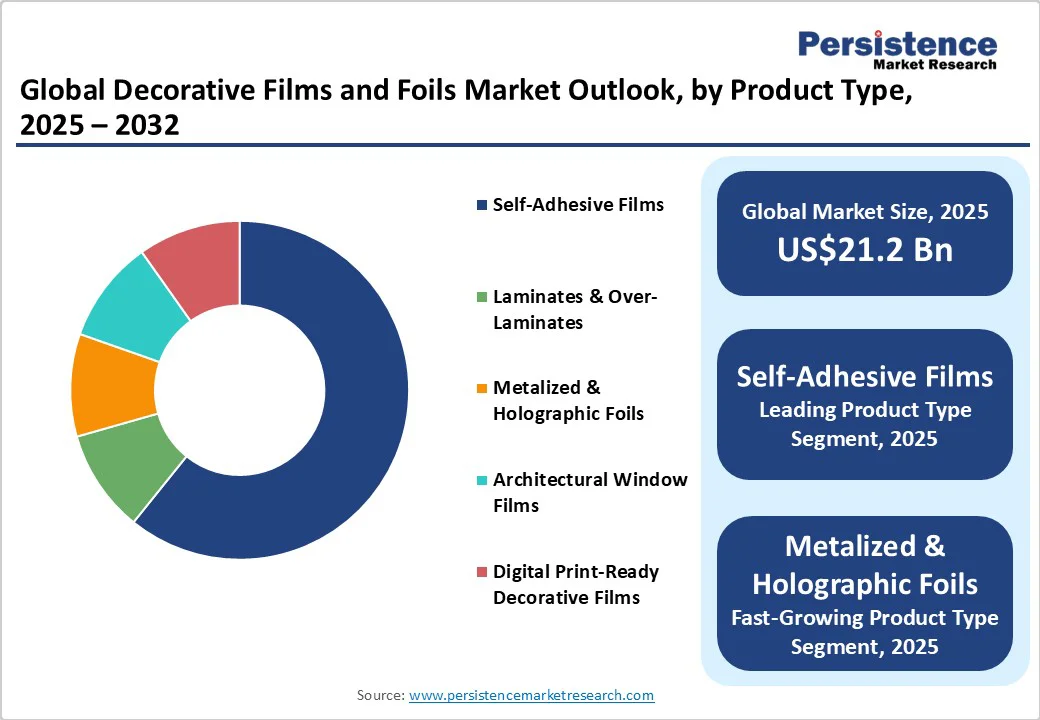

- Leading Product Type: Self-Adhesive Decorative Films hold the largest share at approximately 47% of global sales, driven by convenience, rapid installation, and popularity in both residential DIY and commercial refurbishment projects.

| Key Insights | Details |

|---|---|

| Decorative Films and Foils Market Size (2025E) | US$21.2 Bn |

| Market Value Forecast (2032F) | US$33.1 Bn |

| Projected Growth (CAGR 2025 to 2032) | 6.2% |

| Historical Market Growth (CAGR 2019 to 2024) | 5.3% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Growing Renovation and Retrofit Activities

The rise in residential and commercial renovations is driving decorative film demand, offering affordable, low-disruption surface upgrades. Popular in the U.S. and Western Europe, these films replace traditional panels with quick installation and diverse designs, supporting recurring purchases and expanding opportunities for manufacturers and installers in the retrofit market.

Expansion in Automotive and Consumer Electronics Interiors

Automotive and electronics industries are adopting decorative films for lightweight, cost-effective interior finishes that mimic premium materials. As demand grows for customizable, textured surfaces, high-gloss and soft-touch films gain popularity. Used in vehicles, appliances, and devices, these films enhance aesthetics, reduce environmental impact, and expand revenue beyond traditional construction sectors.

Sustainability and Material Innovation

Sustainability has become a defining industry priority. Producers are transitioning toward mono-polymer, PVC-free, and solvent-free structures to comply with stringent global regulations and corporate environmental goals. The introduction of the recyclable BOPP, CPP, and polyester substrates is helping manufacturers achieve lower emissions and higher material recovery rates.

Advancements in coatings and adhesives have also improved UV resistance and durability, increasing the lifespan of decorative films. This evolution toward greener, high-performance solutions enhances long-term adoption across architecture, automotive, and consumer goods sectors.

Barrier Analysis - Raw Material Price Volatility

The market remains exposed to price fluctuations in key feedstocks such as PVC, polypropylene, and polyester resins. Sudden changes in crude oil prices or supply chain disruptions can elevate production costs and compress margins for converters and distributors. Decorative film producers must navigate these fluctuations through strategic sourcing, supplier diversification, and operational efficiency. For small and mid-sized players, input volatility can delay production schedules and affect competitiveness.

Competitive Pressure from Alternative Finishes

Decorative films face competition from premium materials, such as real wood veneer, powder-coated metal, and high-end laminates. Some consumer segments still associate films with shorter lifespans or lower prestige, particularly in luxury markets.

Poor-quality installations can reinforce these perceptions when films peel or discolor under environmental stress. Overcoming these challenges requires manufacturers to invest in quality assurance, certifications, and brand positioning to ensure trust and repeat business in premium segments.

Opportunity Analysis - Functional and Smart Decorative Films

Emerging film technologies that integrate embedded lighting, sensors, or printed electronics present new value creation opportunities. These functional decorative foils combine aesthetic appeal with smart capabilities, finding use in automotive ambient lighting, interactive retail displays, and next-generation home interiors.

If functional films capture even a small fraction of total decorative film demand, they could generate incremental revenues surpassing several hundred million dollars by 2030. Early adoption by OEMs positions suppliers at the forefront of premium product innovation.

Rapid Expansion in Asia Pacific

Asia Pacific is projected to record the fastest growth during 2025 - 2032, supported by large-scale construction activity, rising disposable incomes, and expanding furniture manufacturing bases in China, India, and ASEAN countries. The region’s cost-efficient production ecosystem, availability of raw materials, and infrastructure investment programs encourage capacity expansions and joint ventures. Regional producers can capitalize on export opportunities while meeting domestic urbanization-driven demand.

Category-wise Analysis

Material Type Insights

PVC and polyester (BOPET) together account for approximately 62% of the market revenue in 2025, driven by their cost-effectiveness, durability, and design versatility. PVC films are widely used in wall coverings, furniture laminates, and cabinetry overlays due to their strong adhesion and smooth finish.

BOPET films excel in high-end applications requiring dimensional stability, scratch resistance, and gloss retention. Both materials offer excellent printability and surface adaptability, enabling textures, including woodgrain, marble, metallic, and matte. Leading brands such as LG Hausys, Renolit, and Avery Dennison extensively use PVC-based films across residential and commercial interior design projects.

The rise of BOPP and CPP-based recyclable decorative films is reshaping the market amid growing sustainability mandates and ESG-driven goals. Free from PVC, halogens, and heavy metals, these mono-polymer films simplify recycling compared to multilayer alternatives. Industry leaders such as Cosmo Films Ltd., Treofan Group, and Toray Industries are spearheading innovation in recyclable substrates and solvent-free adhesives.

These films offer high optical clarity, strong print adhesion, and lightweight efficiency, making them ideal for eco-conscious manufacturers. Products such as Cosmo’s EcoLustre and Toray’s Lumirror Eco are gaining momentum, especially as regulations such as the EU Circular Economy Action Plan drive demand for sustainable decorative solutions.

Product Type Insights

Self-adhesive decorative films dominate the market with around 47% of total sales in 2025, driven by surging demand for DIY-friendly and affordable renovation solutions. These films feature peel-and-stick backings, enabling easy application on furniture, walls, glass, and appliances without tools or downtime, for retail, office, and rental upgrades.

Leading players such as 3M, Avery Dennison, and LG Hausys offer advanced self-adhesive films with UV resistance, antimicrobial coatings, and air-release technology for smooth installation. Versatile in finish and opacity, they serve diverse uses from privacy glass to faux wood cabinetry. Avery Dennison’s Architectural Finishes Collection alone includes over 900 design options.

Metalized and holographic foils are emerging as the fastest-growing product segment. These foils deliver luxury-grade surface finishes with reflective, embossed, or holographic effects that are highly valued in automotive interiors, consumer electronics, and premium packaging. Brands in the luxury segment, such as BMW, Samsung, and L’Oréal, increasingly use metalized foils to enhance visual appeal and brand differentiation.

Manufacturers such as Leonhard KURZ, Covestro, and Coates Group are pioneering advanced hot stamping and cold transfer foils that combine decorative brilliance with functional benefits such as scratch resistance, fingerprint protection, and chemical durability. Specialty foils are also being engineered to provide functional integration, including light diffusion, conductivity, or heat resistance, expanding their application scope beyond aesthetics.

Regional Insights

Asia Pacific Decorative Films and Foils Market Trends - Manufacturing Powerhouse & Eco-Friendly Innovation

Asia Pacific is the fastest-growing and most industrially diversified region, projected to account for over 44.7% of global market share. The region benefits from large-scale manufacturing ecosystems, low production costs, and sustained infrastructure expansion.

China and India remain key consumption centers, together representing nearly 60% of regional demand in 2025, while Japan, South Korea, and Taiwan dominate high-end film innovations and specialty coating technologies.

The construction boom, particularly in urban housing, hospitality, and commercial real estate, continues to fuel demand for decorative surface laminates and vinyl wraps. The region's automotive and electronics sectors increasingly use functional and aesthetic films for lightweighting and design flexibility.

In July 2024, LG Hausys (Korea) announced the expansion of its Deco Foil Division in Changwon, introducing eco-friendly product lines for interior and automotive use. Similarly, Cosmo Films Ltd. (India) launched a PVC-free decorative film portfolio in September 2024, specifically targeting furniture and interior design markets in Southeast Asia.

China continues to lead global production capacity with a dense network of coating and lamination facilities in provinces such as Guangdong and Zhejiang. Japanese manufacturers such as Toray Industries and Mitsubishi Chemical Films emphasize precision coating, scratch resistance, and thermal durability, catering to electronics and EV interior components.

The region’s strategic advantage lies in its ability to balance cost-efficient production with increasing technological sophistication, making it the primary growth engine for the global decorative films and foils industry.

North America Decorative Films and Foils Market Trends - Retrofit Demand & Sustainable Material Transition

North America remains a high-value, design-driven market for decorative films and foils. The region’s growth is primarily sustained by renovation and retrofitting cycles in residential and commercial construction, combined with a robust automotive manufacturing base. Demand for self-adhesive and surface protection films continues to increase, especially in architectural interiors, glass partitions, and vehicle wraps.

The regulatory framework strongly supports low-VOC, REACH-aligned, and eco-certified decorative materials, prompting a gradual transition away from solvent-based formulations. For example, the U.S. Green Building Council’s LEED guidelines and California Air Resources Board (CARB) standards have accelerated the adoption of environmentally safe PVC alternatives and recyclable substrates.

Leading manufacturers such as 3M Company, Avery Dennison, and Omnova Solutions (acquired by Synthomer) have launched product lines that align with energy efficiency and sustainability goals. In March 2024, 3M Architectural Finishes Division unveiled its DI-NOC Carbon Neutral Series, which utilizes 30% post-consumer recycled content and targets LEED-compliant building projects.

Avery Dennison also announced in June 2024 an expansion of its smart-label and decorative film facility in Ohio to strengthen its architectural portfolio. Investment activity in the region is directed toward digital printing integration, UV-curable coatings, and localized supply chains to minimize import dependency.

Europe Decorative Films and Foils Market Trends -Design Leadership & Circular Material Compliance

Europe upholds its position as a center of innovation and premium decorative design. The region’s leadership stems from its emphasis on aesthetic precision, recyclability, and regulatory compliance. Germany serves as the hub for automotive interior and specialty foil applications, while the U.K., France, and Spain exhibit strong demand in commercial renovation and retail décor projects.

The European Green Deal and Circular Economy Action Plan (CEAP) are shaping material innovation by restricting non-recyclable PVCs and incentivizing mono-material, PVC-free decorative foils. This regulatory landscape has propelled leading European producers such as Leonhard KURZ Stiftung & Co., Covestro AG, and Renolit SE to invest in bio-based polymers and solvent-free coatings.

Recent developments illustrate this shift: in February 2025, Leonhard KURZ inaugurated its Sustainability Innovation Hub in Fürth, Germany, aimed at scaling recyclable transfer foils for the automotive and electronics sectors. Similarly, Covestro introduced a new UV-stable polycarbonate film series in April 2024 for high-end appliance and lighting applications.

European producers are also integrating digital surface simulation tools for rapid prototyping, aligning with Industry 4.0 design workflows. Strategic investments are heavily directed toward waste reduction, energy-efficient coating systems, and high-gloss metallic effects tailored to luxury segments.

Competitive Landscape

The global decorative films and foils market is moderately fragmented, combining global conglomerates with specialized regional converters. Leading multinationals, including Avery Dennison, 3M, Leonhard KURZ, Cosmo Films, DuPont Teijin Films, and Sekisui Chemical, collectively hold a significant portion of global revenue.

Numerous local players cater to regional design preferences and price segments. Market consolidation is ongoing, with top players leveraging brand equity, technology leadership, and distribution networks to maintain competitive positioning.

Dominant strategies include innovation in sustainable and functional products, regional capacity expansion, and strategic collaborations with OEMs and designers. Market leaders prioritize high-performance coatings, recyclable structures, and digital print compatibility to meet evolving customer and regulatory expectations.

Key Industry Developments

- In March 2025, 3M Company launched its DI-NOC Carbon Neutral Series of architectural films, incorporating 30% post-consumer recycled content, aimed at supporting LEED-compliant building projects and expanding its sustainable product offerings in North America.

- In June 2024, Avery Dennison expanded its smart-label and decorative film facility in Ohio, USA, increasing production capacity for architectural and automotive applications, while enhancing digital printing capabilities for customized surface designs.

- In February 2025, Leonhard KURZ inaugurated its Sustainability Innovation Hub in Fürth, Germany, focused on developing recyclable transfer foils for automotive interiors and consumer electronics, aligning with European circular economy initiatives.

Companies Covered in Decorative Films and Foils Market

- 3M Company

- Avery Dennison Corporation

- LG Hausys

- Leonhard KURZ

- Covestro AG

- Cosmo Films Ltd.

- Renolit SE

- Omnova Solutions

- Toray Industries

- Mitsubishi Chemical Corporation

- Coates Group

- Avery Weigh-Tronix

- Uflex Limited

- Huhtamaki PPL Ltd.

- CCL Industries Inc.

- Eastman Chemical Company

- Polyplex Corporation

- Jindal Films

- SKC Inc.

- Flexcon Company Inc.

Frequently Asked Questions

The decorative films and foils market size was valued at US$21.2 Bn in 2025.

The market is projected to reach US$33.1 Bn by 2032.

Key trends include increasing adoption of self-adhesive decorative films for residential and commercial renovation and growing demand for recyclable polypropylene and mono-polymer films driven by sustainability mandates.

By material type, PVC and Polyester (BOPET) dominate with 62% market share. By product type, self-adhesive decorative films hold the largest share at 47%.

The global market is expected to grow at a CAGR of 6.2% from 2025 to 2032.

Some of the major players in the decorative films and foils market include 3M Company, Avery Dennison Corporation, LG Hausys, Leonhard KURZ, and Covestro AG.