- Plastics, Polymers & Resins

- Long Fiber Thermoplastics Market

Long Fiber Thermoplastics Market Size, Share, and Growth Forecast, 2026 – 2033

Long Fiber Thermoplastics Market by Resin Type (Polypropylene, Polyamide, Thermoplastic Polyurethane, Polybutylene, Others), Application (Automotive, Aerospace, Electrical & Electronics, Others), and Regional Analysis for 2026 – 2033

Long Fiber Thermoplastics Market Size and Trends Analysis

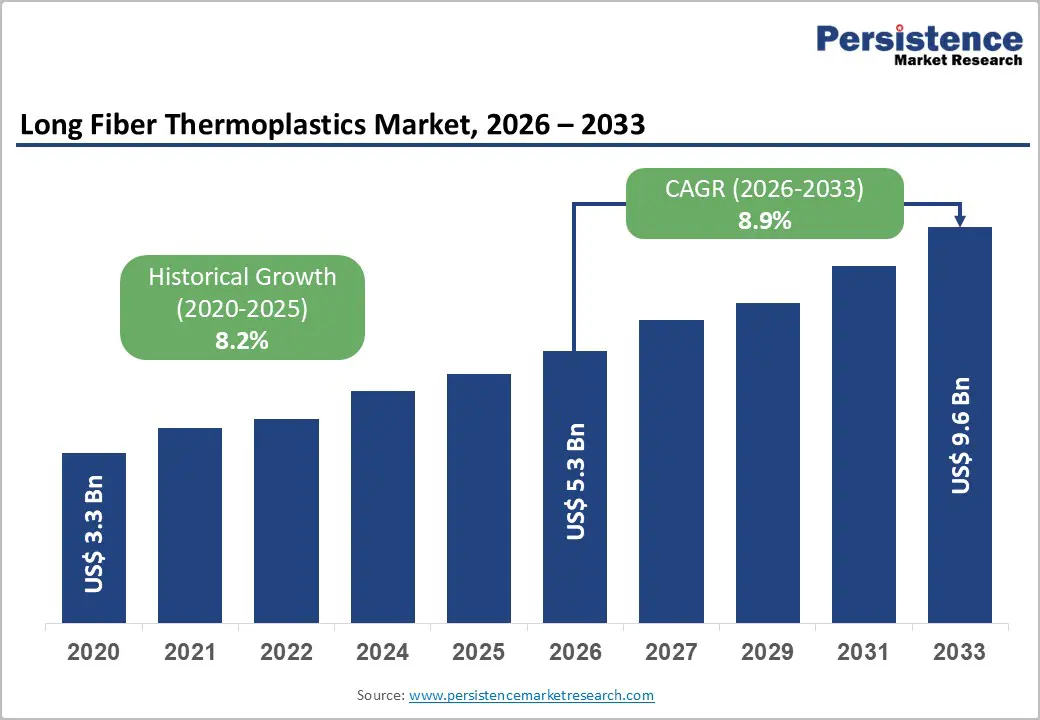

The global long fiber thermoplastics market size is likely to be valued at US$5.3 billion in 2026 and is expected to reach US$9.6 billion by 2033, growing at a CAGR of 8.9% during the forecast period from 2026 to 2033, driven by the increasing demand for lightweight, high-strength materials across industries, with automotive lightweighting leading adoption due to stringent fuel efficiency and emission regulations. Expanding applications in aerospace, electrical & electronics, and industrial sectors, where LFTs offer superior strength-to-weight ratios, impact resistance, and recyclability compared to traditional metals and short-fiber composites.

Key factors sustaining market expansion include advancements in manufacturing processes such as direct LFT and enhanced injection molding, the rising trend of sustainable and recyclable composites, and ongoing technological innovations in resin formulations, which continue to drive growth through new product development and regional expansion.

Key Industry Highlights:

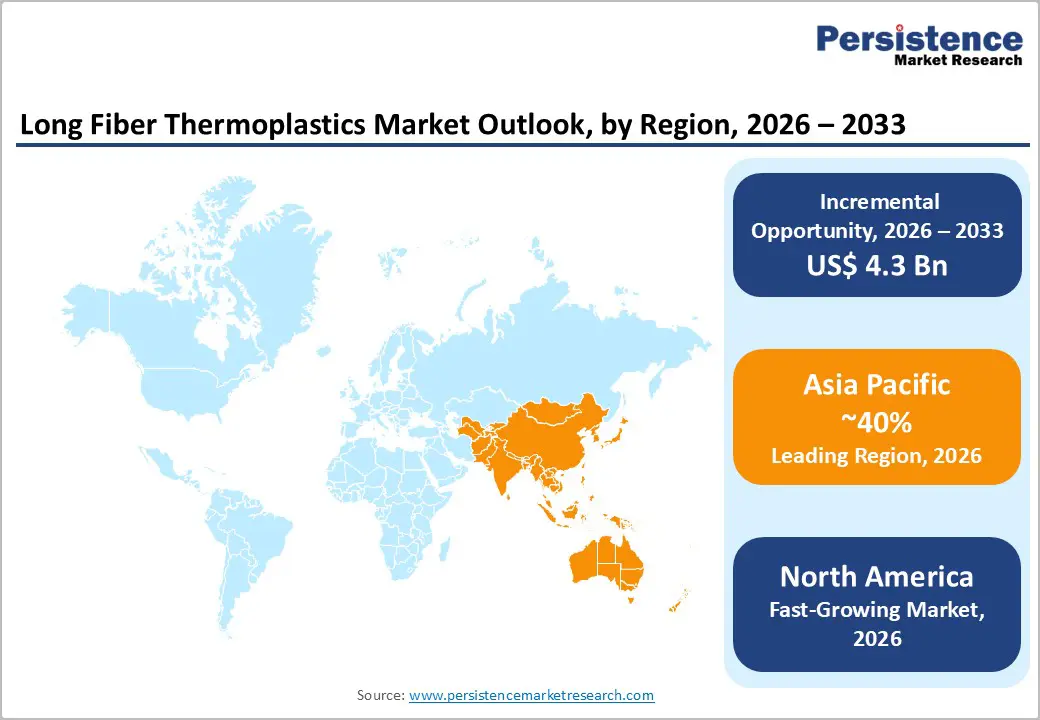

- Leading Region: Asia Pacific is anticipated to be the leading region, accounting for a market share of 40% in 2026, driven by its manufacturing advantages and rapid expansion in automotive and electronics production.

- Fastest-growing Region: North America is likely to be the fastest-growing region in long fiber thermoplastics in 2026, supported by automotive innovation, aerospace demand, and advanced R&D capabilities.

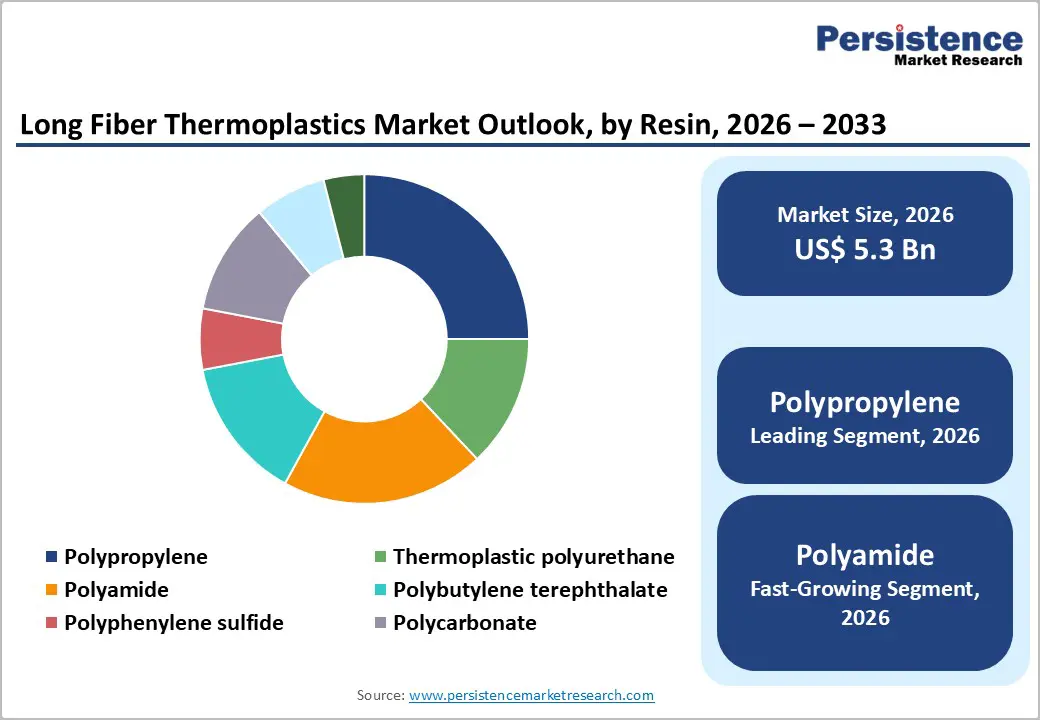

- Leading Resin Type: Polypropylene is projected to represent the leading resin type in 2026, accounting for 58% of the revenue share, driven by its cost-effectiveness and ease of processing.

- Leading Application: The automotive segment is expected to be the leading application type, accounting for over 48% of revenue share in 2026, supported by increasing automotive lightweighting initiatives, rising EV production, and the need to improve fuel efficiency and reduce emissions.

| Key Insights | Details |

|---|---|

| Long Fiber Thermoplastics Market Size (2026E) | US$ 5.3 Bn |

| Market Value Forecast (2033F) | US$ 9.6 Bn |

| Projected Growth (CAGR 2026 to 2033) | 8.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 8.2% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis - Increased Demand for Lightweight Materials in Automotive and Aerospace Industries

Automakers are under increasing pressure to meet stringent fuel efficiency and emission regulations while improving vehicle performance and safety. LFTs offer an excellent strength-to-weight ratio, high impact resistance, and design flexibility, making them ideal for replacing metal and short-fiber composites in structural and semi-structural components. Their use supports vehicle lightweighting, enables part consolidation, and reduces overall manufacturing costs. The rapid growth of electric vehicles has accelerated LFT adoption, as reducing vehicle weight directly enhances battery efficiency and driving range.

In the aerospace industry, lightweighting is equally critical to improving fuel efficiency, payload capacity, and operational performance. Aircraft manufacturers increasingly adopt Long Fiber Thermoplastics for interior panels, brackets, and selected structural components due to their high mechanical strength, thermal stability, and corrosion resistance. LFTs also provide advantages such as faster processing cycles, recyclability, and lower maintenance compared to traditional materials. Air travel demand rises, and sustainability becomes a priority, aerospace OEMs are shifting toward advanced thermoplastic composites.

Technological Advancements and Regulatory Changes Promoting Sustainability

Innovations in direct LFT processing, improved injection molding techniques, and advanced compounding technologies have enhanced fiber dispersion, mechanical performance, and production efficiency. These improvements allow manufacturers to produce complex, lightweight components with consistent quality and reduced material waste. Advancements in resin formulations, including high-performance and recyclable thermoplastics, are expanding LFT applicability across automotive, aerospace, and electrical & electronics sectors. Such technological progress lowers lifecycle costs, improves recyclability, and makes LFTs a preferred alternative to traditional metals and thermoset composites.

Regulatory changes focused on sustainability and emissions reduction are driving LFT adoption across end-use industries. Governments worldwide are enforcing stricter environmental regulations related to vehicle emissions, fuel efficiency, and material recyclability. These policies encourage manufacturers to replace heavier, non-recyclable materials with lightweight and sustainable alternatives such as long fiber thermoplastics. LFTs support circular economy goals due to their recyclability and potential use of bio-based or recycled polymers. In automotive and aerospace sectors, compliance with emission norms and sustainability targets has become critical, making LFTs an attractive solution for achieving regulatory compliance while maintaining performance, durability, and cost-efficiency.

Barrier Analysis - High Processing Complexity

Achieving uniform fiber length and consistent dispersion in LFT processing is challenging, as fibers can break under high shear, affecting mechanical performance and part quality. LFTs require specialized equipment, precise temperature control, and optimized molds, increasing setup time and production costs. These challenges can deter small and medium manufacturers from adopting LFTs, limiting market penetration despite their performance benefits.

LFT processing also demands skilled labor and advanced monitoring systems. Balancing parameters such as melt viscosity, fiber orientation, and cooling rates is crucial to avoid defects, warpage, or reduced strength. Compared to short-fiber thermoplastics, LFTs have longer cycle times and higher tooling costs, which can limit scalability and adoption in cost-sensitive applications.

Availability of Substitutes and Regulatory Hurdles

Alternative materials such as short-fiber thermoplastics, aluminum, magnesium alloys, and advanced thermoset composites often compete with LFTs due to lower cost, familiarity, and established supply chains. In automotive and industrial sectors, these materials are preferred for their simpler processing and tooling compatibility. Metals remain dominant for load-bearing applications due to their proven durability, limiting LFT adoption in price-sensitive, high-volume markets.

Regulatory challenges also hinder LFT growth, as components must meet stringent safety, fire resistance, and performance standards, especially in sectors such as automotive, aerospace, and electrical. Certification processes are costly and time-consuming, slowing commercialization. Regional regulatory differences further complicate market entry, while compliance with multiple standards delays LFT adoption.

Opportunity Analysis - Technological Convergence and Policy-Driven Sustainability Initiatives

The integration of advanced compounding methods, automated processing, and simulation-driven design is improving part performance while reducing development cycles. Digital tools enable optimized fiber orientation and part consolidation, expanding LFT use in complex automotive and aerospace components. Convergence with high-performance resins and hybrid composites is opening new applications where strength, durability, and lightweighting are critical. These advancements enhance production efficiency, lower lifecycle costs, and make LFTs increasingly competitive against metals and conventional composites.

Policy-driven sustainability initiatives strengthen opportunities for LFT adoption across markets. Governments are promoting lightweight, recyclable, and low-emission materials through stricter environmental regulations and incentives. LFTs align well with circular economy goals due to their recyclability and compatibility with recycled or bio-based polymers. In the automotive and aerospace industries, policies targeting carbon reduction and fuel efficiency encourage material substitution toward advanced thermoplastics. Combined with sustainability-focused procurement by OEMs, these regulatory initiatives create favorable conditions for expanded LFT usage and long-term market growth.

Bio-based and Hybrid Composites

Industries increasingly focus on sustainability and carbon footprint reduction. Bio-based polymers derived from renewable resources, when reinforced with long fibers, offer comparable mechanical performance to conventional LFTs while reducing dependence on fossil-based materials. Automotive, consumer goods, and construction sectors are showing growing interest in these materials to meet sustainability targets and regulatory requirements. The use of bio-based LFTs supports circular economy initiatives and enhances brand value for manufacturers seeking environmentally responsible material solutions without compromising strength, durability, or processing efficiency.

Hybrid composites combining long fiber thermoplastics with other reinforcements or material systems expand application potential. By integrating LFTs with continuous fibers, fabrics, or metal inserts, manufacturers can tailor performance for demanding applications requiring high stiffness, impact resistance, or thermal stability. Such hybrid solutions enable lightweight structures with optimized mechanical properties, particularly in automotive, aerospace, and industrial equipment. Advancements in bonding technologies and co-molding processes are improving integration efficiency. This flexibility allows designers to balance performance, cost, and sustainability.

Category-wise Analysis

Resin Type Insights

Polypropylene is expected to lead the long fiber thermoplastics market, accounting for approximately 58% of revenue in 2026, driven by its cost-effectiveness, low density, and excellent processability. PP-based LFTs are widely adopted in high-volume automotive applications such as front-end modules, seat structures, and underbody components, where lightweighting and impact resistance are critical. Its good chemical resistance and recyclability strengthen its position, especially as OEMs focus on sustainable material choices. For example, the extensive use of long glass fiber–reinforced polypropylene in automotive interior carriers and structural supports, where it replaces heavier metal parts while maintaining durability and dimensional stability.

Polyamides are likely to represent the fastest-growing segment in 2026, supported by their superior mechanical strength, high heat resistance, and excellent fatigue performance. These properties make PA-based LFTs suitable for structural and semi-structural applications that require durability under high thermal and mechanical stress, particularly in electric vehicles and advanced electronics. For example, the use of long fiber–reinforced polyamide in battery housings and powertrain-adjacent components, where higher temperature resistance and structural integrity are essential. As EV platforms expand and demand for high-performance lightweight materials increases, polyamide LFTs are gaining strong traction, supported by continuous advancements in resin formulation and processing technologies.

Application Insights

The automotive segment is projected to lead the market, capturing around 48% of the revenue share in 2026, supported by stringent lightweighting mandates, emission regulations, and the need for cost-efficient part consolidation. LFTs enable automakers to replace metal assemblies with single molded components, reducing weight and production complexity while maintaining strength and safety. For example, the adoption of LFTs in front-end carriers and door modules, where multiple metal parts are consolidated into lightweight composite structures. The growing shift toward electric vehicles strengthens automotive dominance, as reducing vehicle weight directly improves driving range and energy efficiency.

The aerospace segment is likely to be the fastest-growing application in 2026, driven by the increasing demand for high-strength, low-weight materials that improve fuel efficiency and operational performance. LFTs are increasingly used in aircraft interior panels, brackets, and support structures, offering advantages such as corrosion resistance, design flexibility, and faster processing compared to traditional materials. For example, aircraft interior components manufactured using long fiber thermoplastics help reduce overall aircraft weight while meeting strict safety and performance standards. Airlines and manufacturers prioritize sustainability and efficiency, and aerospace adoption of LFTs continues to accelerate, supported by regulatory and environmental objectives.

Regional Insights

North America Long Fiber Thermoplastics Market Trends

North America is likely to be the fastest-growing region in long fiber thermoplastics in 2026, driven by steady growth and strong adoption across major end-use sectors, particularly automotive, aerospace, and industrial machinery. OEMs in the automotive industry increasingly specify LFTs for structural and semi-structural components to meet stringent fuel efficiency and emissions targets, while aerospace manufacturers favor them for interior parts and non-critical structures due to their favorable strength-to-weight ratios and corrosion resistance. The U.S. remains the largest regional market, supported by a robust supply chain and a strong R&D ecosystem that accelerates material innovation and processing efficiency.

A notable trend shaping the North America long fiber thermoplastics (LFT) market is investments in advanced processing technologies and regional production capacity expansion by key material suppliers. For example, BASF’s development of its Ultramid® Structure long fiber thermoplastic compounds has gained traction in the region for engineering applications requiring high mechanical performance and thermal stability. These PA-based LFTs are designed for demanding transportation and industrial parts, demonstrating improved impact resistance and processing consistency compared to traditional materials.

Europe Long Fiber Thermoplastics Market Trends

Europe is likely to be a significant market for long fiber thermoplastics in 2026, due to strong demand from automotive, aerospace, and industrial sectors. Europe accounts for a significant share of LFT consumption due to its advanced manufacturing base, stringent environmental regulations, and strong emphasis on lightweighting and recyclability in engineering applications. Germany remains a dominant market within Europe, particularly in automotive production, where LFT components help meet fuel efficiency goals and emission standards, reinforcing the use of sustainable materials in premium vehicle platforms.

European manufacturers are increasingly incorporating recycled content into thermoplastic composites as part of their broader sustainability initiatives. One example is the development of advanced composite portfolios by Lanxess, a specialty chemicals company headquartered in Cologne, Germany. Lanxess’s Tepex® thermoplastic continuous fiber composite solutions are gaining traction across Europe for automotive lightweighting and structural applications, delivering substantial weight reductions and high stiffness compared with conventional materials. The company’s emphasis on innovative processing technologies and tailored material solutions supports OEM requirements for both high performance and sustainability.

Asia Pacific Long Fiber Thermoplastics Market Trends

The Asia Pacific region is anticipated to be the leading region, accounting for a market share of 40% in 2026, driven by large-scale automotive and manufacturing activities across China, Japan, South Korea, and India. The strong industrial base and rapid expansion of electric vehicle production have significantly increased LFT adoption for lightweight structural parts, battery housings, and interior modules in passenger and commercial vehicles. Rising infrastructure development and urbanization are broadening LFT use into industrial machinery and consumer goods, supported by cost-competitive production capabilities that attract multinational OEMs and composite suppliers.

A key trend shaping the Asia Pacific LFT market is the increasing investments by material suppliers to localize production and better serve rapidly growing regional demand. For example, Avient Corporation has established its first dedicated long fiber reinforced thermoplastic composites production line in Shanghai, designed to meet growing demand in the region for high-performance composite materials. This investment enhances localized supply and supports the integration of LFTs in automotive, industrial, and consumer applications requiring excellent impact strength and durability.

Competitive Landscape

The global long fiber thermoplastics market exhibits a moderately fragmented structure, driven by the growing adoption of lightweight, high-performance composites across automotive, aerospace, electrical, and industrial applications, and supported by technological advancements and strategic regional expansion. Manufacturers are increasingly focusing on enhancing material performance, sustainability features, and processing efficiencies to meet stringent industry standards and customer demands.

With key leaders including SABIC, BASF SE, Celanese Corporation, Solvay S.A., and Lanxess AG, competition centers on innovation in resin development, advanced fiber integration, and application-specific solutions that cater to automotive lightweighting and aerospace performance requirements. These players compete through extensive R&D investments, strategic partnerships with OEMs, and regional capacity expansion to strengthen their footprint and supply chain responsiveness.

Key Industry Developments:

- In September 2025, SABIC launched MEGAMOLDING™, an advanced platform for manufacturing large, high-performance thermoplastic parts. The platform combined SABIC’s material expertise with tooling and processing capabilities from value-chain partners. It enabled the replacement of metals and thermosets with lighter, stronger, and more sustainable thermoplastic solutions, addressing challenges such as cost, complexity, and scalability while offering faster cycle times, weight reduction, and lower carbon emissions.

- In February 2025, Polyplastics introduced its eco-friendly PLASTRON® LFT RA627P, a long fiber-reinforced thermoplastic composite made from polypropylene (PP) and 30% regenerated cellulose fibers. The material featured low density, high rigidity, and excellent impact strength, making it ideal for audio components and industrial housings. Compared to short glass fiber-reinforced PP, it reduced the carbon footprint by 30%, with 10% lower density and higher rigidity.

Companies Covered in Long Fiber Thermoplastics Market

- SABIC

- RTP Company

- JNC Corporation

- Avient Corporation

- Celanese Corporation

- LANXESS

- Solvay

- Daicel Corporation

- Kingfa SCI. & TECH. CO., LTD.

- SGL Carbon

- Asahi Kasei Corporation

Frequently Asked Questions

The global long fiber thermoplastics market is projected to reach US$5.3 billion in 2026.

The long fiber thermoplastics market is driven by the increasing demand for lightweight, high-strength materials in automotive, aerospace, and industrial applications.

The long fiber thermoplastics market is expected to grow at a CAGR of 8.9% from 2026 to 2033.

Key market opportunities in long fiber thermoplastics lie in bio-based and hybrid composites, advanced lightweighting applications, and sustainability-driven material adoption.

SABIC, RTP Company, JNC Corporation, Avient Corporation, and Celanese Corporation are the leading players.