- Advanced Materials

- Carbon Fiber Reinforced Thermoplastic Composites (CFRTP) Market

Carbon Fiber Reinforced Thermoplastic Composites (CFRTP) Market Size, Share, and Growth Forecast, 2026 - 2033

Carbon Fiber Reinforced Thermoplastic Composites (CFRTP) Market By Product Type (Carbon Fiber, Others), Application (Aerospace, Automotive, Consumer Durables), and Regional Analysis for 2026 - 2033

Carbon Fiber Reinforced Thermoplastic Composites (CFRTP) Market Size and Trends Analysis

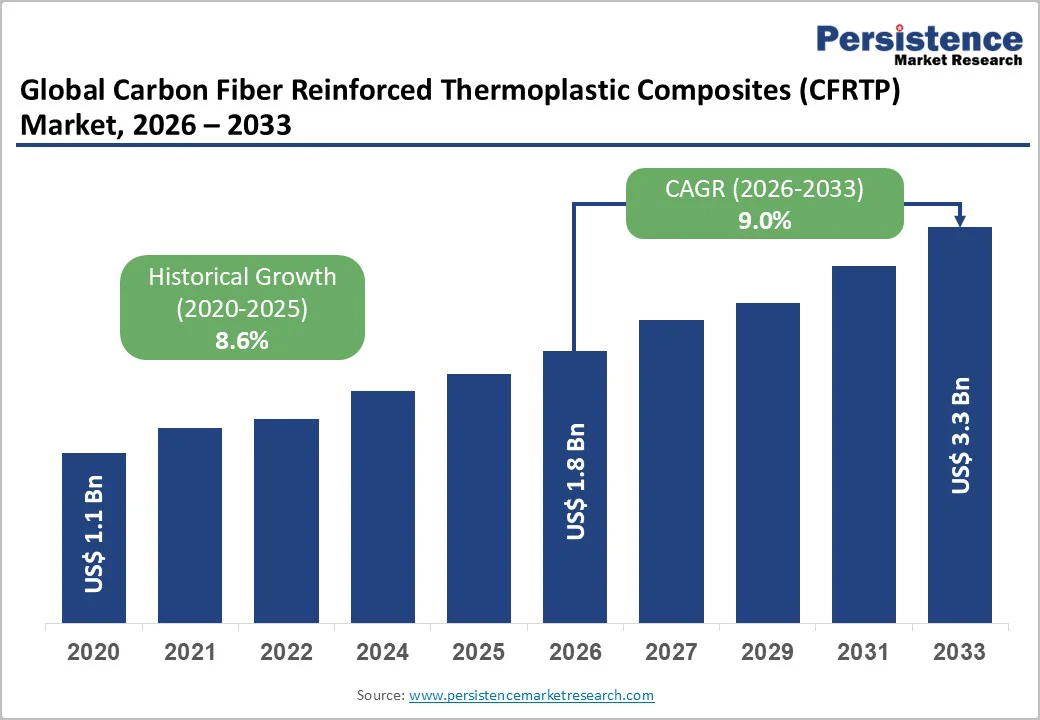

The global carbon fiber reinforced thermoplastic composites (CFRTP) market size is likely to be valued at US$1.8 billion in 2026. It is expected to reach US$3.3 billion by 2033, growing at a CAGR of 9.0% during the forecast period from 2026 to 2033, driven by rising adoption in aerospace, automotive, consumer electronics, and industrial applications, where CFRTP’s high strength-to-weight ratio, recyclability, and rapid processing advantages outperform traditional thermoset composites.

Technological advancements such as automated fiber placement (AFP), hybrid molding, and continuous fiber tapes have significantly lowered production cycle times and improved part uniformity, enabling mass-scale manufacturing.

Key Industry Highlights:

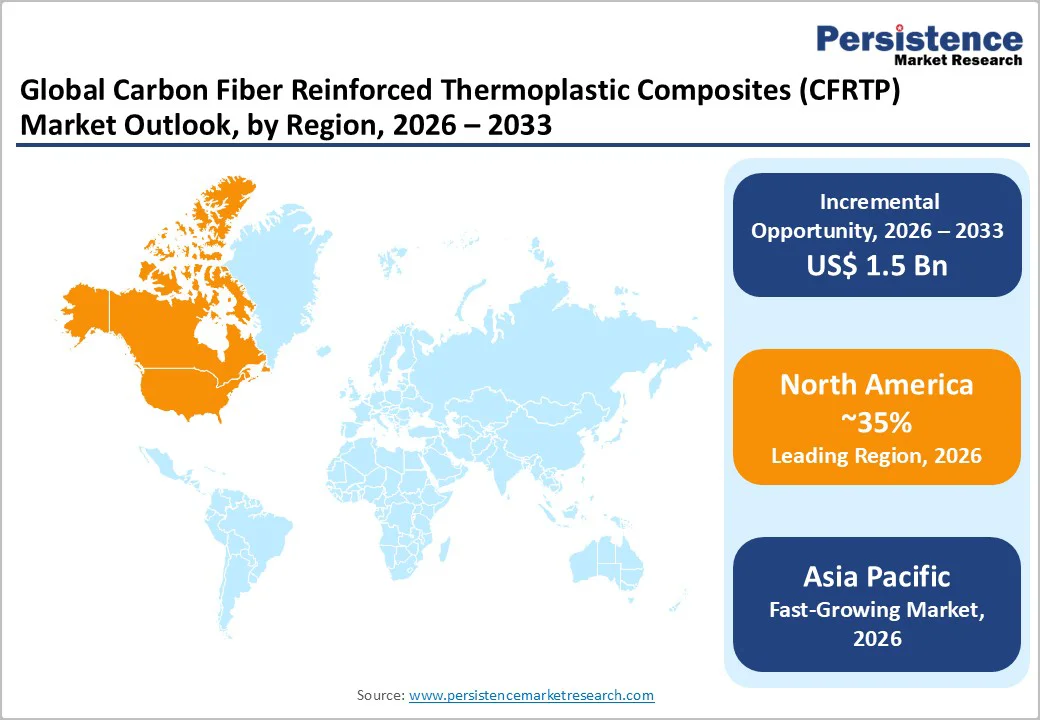

- Leading Region: North America is anticipated to be the leading region, accounting for a market share of 35% in 2026, driven by strong EV adoption, stringent efficiency regulations, and rising aerospace integration.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing region in the market in 2026, driven by large-scale EV production, cost-efficient manufacturing, and expanding aerospace programs.

- Leading Product Type: Long carbon fiber is projected to be the leading product type in 2026, accounting for 45% of the market, driven by its superior strength–processability balance in automotive and structural applications.

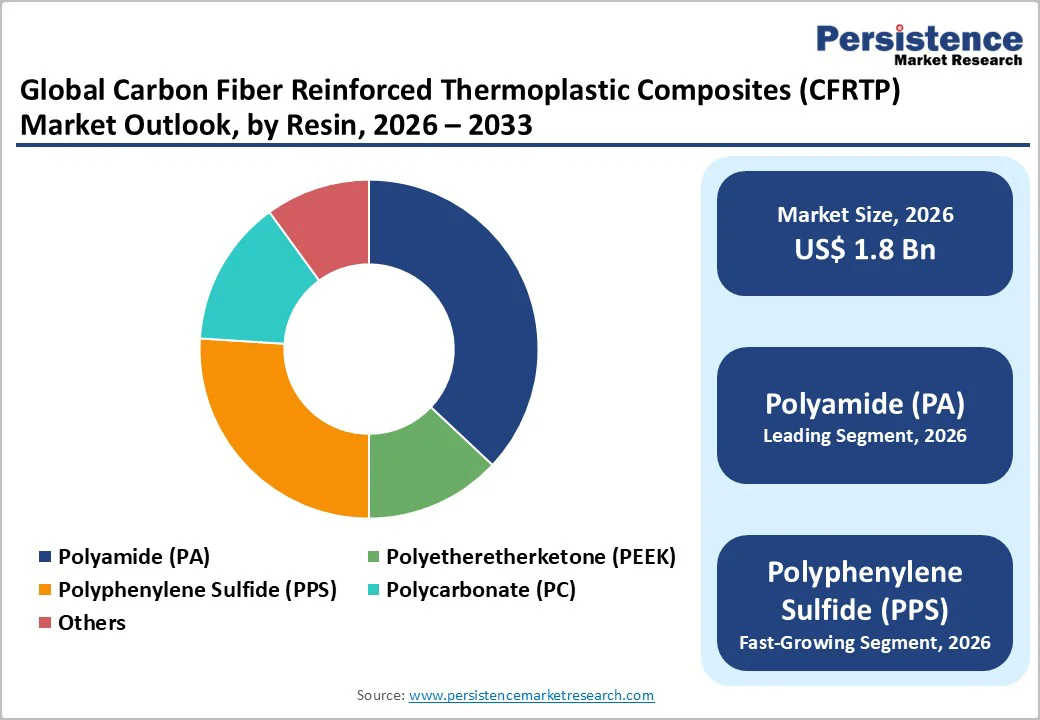

- Leading Resin Type: Polyamide (PA) is anticipated to be the leading resin type, accounting for over 40% of the revenue share in 2026, driven by cost efficiency, versatility, and strong adoption in electronics and automotive parts.

- Leading Application: Automotive is anticipated to be the leading segment, accounting for over 50% of revenue share in 2026, driven by the extensive use of CFRTP in EV light-weighting and structural components.

| Key Insights | Details |

|---|---|

|

CFRTP Market Size (2026E) |

US$1.8 Bn |

|

Market Value Forecast (2033F) |

US$3.3 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

9.0% |

|

Historical Market Growth (CAGR 2020 to 2025) |

8.6% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Increasing Demand for Lightweight Materials in Automotive and Aerospace Sectors

The growing emphasis on weight reduction across the automotive and aerospace industries is significantly accelerating the adoption of CFRTP composites. Automakers are aggressively integrating lightweight materials to meet fuel-efficiency and emissions-reduction mandates, as lighter vehicle bodies can improve energy efficiency and EV range. CFRTP’s high strength-to-weight ratio, rapid processing, and recyclability make it an ideal candidate for structural and semi-structural automotive components such as battery enclosures, brackets, interior modules, crash-absorbing structures, and under-hood parts.

In aerospace, CFRTP is increasingly used to replace traditional metallic parts due to its stiffness, fatigue resistance, and compliance with flame, smoke, and toxicity (FST) standards. Aircraft manufacturers are adopting CFRTP for interior panels, clips, brackets, ducts, and secondary structural components to reduce aircraft weight and boost fuel efficiency. The material’s weldability and repairability provide additional advantages over thermoset composites, enabling faster assembly and maintenance.

Raw Material and Production Costs

Carbon fiber itself is an expensive reinforcement material due to its energy-intensive manufacturing processes, reliance on PAN precursors, and limited supply capacity. Thermoplastic resins commonly used in CFRTP, such as PEEK, PPS, and high-performance polyamides, are also premium-priced, making overall material costs substantially higher than those of traditional metals or standard engineering plastics. The need for specialized equipment, such as automated fiber placement systems, high-temperature molding presses, and precision compounding machinery, adds to capital expenditure.

Production complexity amplifies expenses, as CFRTP manufacturing demands strict quality control, precise fiber orientation, and controlled processing temperatures to ensure uniform performance. Skilled labor shortages and high tooling costs for thermoplastic composites also contribute to elevated production overheads. While advancements such as automated molding and tape-placement technologies are reducing cycle times, the initial setup remains costly.

Expansion in Emerging Markets and Electric Vehicle Integration

Emerging markets offer substantial growth potential for the CFRTP market as manufacturing activity in countries such as China, India, Thailand, and Mexico expands rapidly. These regions are experiencing strong increases in automotive production, consumer electronics demand, and local aerospace component manufacturing. For example, India’s Production-Linked Incentive (PLI) scheme is boosting investments in lightweight material plants, while China’s growing aerospace supply chain is integrating thermoplastic composites for interior and structural components.

Electric vehicle (EV) integration is another powerful growth driver, as CFRTP enables the extreme light weighting needed to enhance range and energy efficiency. The material’s high strength, fast processing, and recyclability make it ideal for EV battery trays, underbody panels, crash structures, and charging system components. For example, BMW uses CFRTP in its i-series EV components to reduce weight and improve performance. As EV platforms evolve, CFRTP's ability to replace heavier metals and thermoset composites positions it as a key material in next-generation electric mobility solutions.

Category-wise Analysis

Product Type Insights

Long carbon fiber is expected to lead the carbon fiber-reinforced thermoplastic composites (CFRTP) market, accounting for approximately 45% of total revenue in 2026, driven by an optimal balance among mechanical strength, durability, and processing efficiency. Its fiber length (>6 mm) enables enhanced load transfer and structural integrity, making it ideal for applications where metal replacement and light weighting are critical. In automotive manufacturing, long carbon fiber CFRTP is increasingly used in interior modules, semi-structural supports, seat frames, and tailgate components due to its superior impact resistance and dimensional stability. For example, Ford uses long carbon-fiber-reinforced PP in front-end carriers.

Short carbon fiber is likely to represent the fastest-growing product type in 2026, driven by its suitability for mass production, cost efficiency, and extensive use in high-volume automotive and electronics applications. With fiber lengths typically below 6 mm, it supports high-speed extrusion, injection molding, and compounding, enabling manufacturers to produce complex components at lower costs. Its uniform dispersion and smooth flow characteristics help minimize defects during molding, making it ideal for under-hood parts, brackets, connectors, consumer gadget housings, and battery-related components. For example, Tesla incorporates carbon fiber components into its electric vehicles to enhance range and performance.

Resin Type Insights

Polyamide (PA) is projected to lead the carbon fiber reinforced thermoplastic composites (CFRTP) market, capturing around 40% of the total revenue share in 2026, driven by its versatility, competitive cost profile, and strong performance across automotive, consumer electronics, and industrial markets. PA-based CFRTP provides excellent stiffness, high impact strength, and reliable thermal resistance, enabling manufacturers to replace metals in light-weighting initiatives. PA enables easy recyclability and provides enhanced moisture resistance through advanced formulations. For instance, Bosch’s implementation of PA-based CFRTP in electronic control unit (ECU) housings improves mechanical strength while keeping part weight low, resulting in better energy efficiency and thermal stability.

Polyphenylene sulfide (PPS) is likely to be the fastest-growing resin type in 2026, due to its exceptional chemical resistance, dimensional stability, and ability to withstand high temperatures without degradation. These characteristics make PPS-based CFRTP highly suitable for aerospace, EV powertrain components, and demanding industrial applications. PPS maintains rigidity and mechanical performance in environments involving prolonged exposure to fuels, oils, hydraulic fluids, and elevated temperatures, making it ideal for fuel system components, connectors, pump parts, and thermal shields. For example, Honeywell’s use of PPS composites in aircraft fuel-line components leverages PPS’s chemical stability and thermal reliability to reduce weight while ensuring long-term structural integrity under harsh operating conditions.

Application Insights

The automotive industry is projected to lead the carbon fiber reinforced thermoplastic composites (CFRTP) market, capturing around 50% of the total revenue share in 2026, driven by the sector’s urgent need for lightweight, high-strength materials that enhance fuel efficiency, extend EV range, and support structural integrity. CFRTP is increasingly replacing steel and aluminum in interior modules, bumper beams, front-end carriers, battery casings, seat structures, and under-hood components. The shift to electric mobility accelerates CFRTP adoption, as weight reduction improves battery range and vehicle performance. Regulatory emissions pressure also drives use in next-generation platforms. For example, Toyota uses CFRTP in Prius hybrid structural brackets to reduce weight while ensuring crash safety and thermal stability.

Aerospace is likely to be the fastest-growing application in 2026, driven by rising demand for lightweight materials that enhance aircraft performance, reduce fuel consumption, and lower maintenance costs. CFRTP offers several advantages over traditional thermoset composites, including weldability, faster processing times, superior impact resistance, and recyclability. CFRTP also meets aviation safety requirements, including flame, smoke, and toxicity standards, making it ideal for interior structures. For example, Airbus is using CFRTP clips and brackets in the A350, enabling faster assembly and material weight reduction while maintaining aerospace-grade reliability.

Regional Insights

North America Carbon Fiber Reinforced Thermoplastic Composites (CFRTP) Market Trends

The North America region is anticipated to be the leading region in the carbon fiber reinforced thermoplastic composites (CFRTP) market, accounting for a market share of 35% in 2026, driven by its dominant aerospace and automotive industries. The region’s advanced R&D infrastructure and well-established manufacturing capabilities enable rapid development and deployment of high-performance thermoplastic carbon-fiber composites. OEMs increasingly use CFRTP for structural automotive components, EV battery enclosures, under-hood parts, and aerospace panels, where light weighting directly improves fuel efficiency, EV range, and overall vehicle performance.

Aerospace applications, including interior panels, ducts, and secondary structural components, also rely on CFRTP due to its excellent strength-to-weight ratio, thermal stability, and compliance with flame, smoke, and toxicity (FST) standards. Regulatory pressure, including stringent fuel efficiency and emissions standards, accelerates adoption, positioning CFRTP as a material of choice for next-generation vehicle and aircraft platforms. Increasing use of automated and additive manufacturing technologies, such as large-format additive manufacturing (LFAM), which enable the production of complex, lightweight components with higher efficiency and precision. For example, a North American LFAM company partnered with aerospace manufacturers.

Europe Carbon Fiber Reinforced Thermoplastic Composites (CFRTP) Market Trends

Europe is likely to be a significant market for CFRTP in 2026, due to a mature automotive and aerospace industry base, strong regulatory pressure for sustainability, and growing emphasis on circular economy principles. Automakers in Germany, France, Italy, and other EU countries are increasingly looking to CFRTP to meet stringent CO2 emissions and recyclability standards under the EU Green Deal and related vehicle-efficiency directives. This drives the demand for lightweight, high-performance thermoplastic composites in structural, semi-structural, and interior automotive components as companies try to reduce weight without sacrificing safety or environmental compliance.

Rising trend toward industrial scale-up of CFRTP production beyond pilot projects. European suppliers and OEMs are investing in high-speed compression molding and automation to lower cycle times and improve manufacturing throughput. For example, German automotive groups such as BMW and Volkswagen are reported to be expanding the use of CFRTP in EV platforms for battery enclosures and semi-structural parts. This shift underscores Europe’s transition toward large-volume CFRTP adoption and light-weighting strategies.

Asia Pacific Carbon Fiber Reinforced Thermoplastic Composites (CFRTP) Market Trends

The Asia Pacific region is likely to be the fastest-growing in the market in 2026, driven by rapid industrialization, rising automotive & EV production, and expanding aerospace demand across China, Japan, South Korea, and India. Manufacturers in the region are increasingly favoring CFRTP for light weighting, particularly in electric vehicles and next-gen mobility, as thermoplastic composites offer a high strength-to-weight ratio, recyclability, and faster production cycles compared with traditional materials.

China is increasingly adopting CFRTP (carbon-fiber-reinforced thermoplastics) for EV battery enclosures and structural components. Domestic EV manufacturers are specifying CFRTP for battery housings and body-in-white parts to reduce weight and enhance energy efficiency, a trend supported by local production capabilities and favorable government policies. CFRTP is gaining popularity due to its high strength-to-weight ratio, recyclability, and rapid processing, making it well-suited for high-volume manufacturing.

Competitive Landscape

The global carbon fiber reinforced thermoplastic composites (CFRTP) market exhibits a moderately fragmented structure, driven by a mix of multinational material-science firms, regional players, and specialized composite manufacturers that compete through innovation, scale, and supply-chain integration. Key leaders, including Toray Industries, Inc., Teijin Limited, Solvay S.A., Hexcel Corporation, and SGL Carbon SE, dominate a substantial portion of the market.

These players compete through continuous product innovation, strategic acquisitions/partnerships, and expansion of global manufacturing and distribution capacity. For example, Toray recently expanded its CFRTP capacity to meet rising demand for EV battery casings and automotive structural parts, while Teijin has collaborated with resin suppliers to develop recyclable thermoplastic CFRTP solutions that address sustainability concerns. Mid-size firms differentiate by offering custom CFRTP grades for specific applications or cost-effective solutions for emerging markets.

Key Industry Developments:

- In September 2025, MaruHachi Corp. was selected by JAXA under the Space Strategic Fund program to develop low-cost, lightweight CFRTP rocket fuel tanks. The project involves collaboration with the University of Tokyo and the Kanazawa Institute of Technology/Innovation Composite Center, emphasizing advanced aerospace applications and the growing adoption of CFRTP in space technology.

Companies Covered in Carbon Fiber Reinforced Thermoplastic Composites (CFRTP) Market

- LANXESS

- Solvay

- PolyOne Corporation

- RTP Company

- Celanese Corporation

- Avient Corporation

- Daicel Corporation

- Sumitomo Bakelite Co., Ltd.

- Mitsubishi Chemical Corporation

- PPG Industries, Inc.

- Asahi Kasei Corporation

- SABIC

- Owens Corning

- TORAY INDUSTRIES, INC

- BASF SE

- SGL Carbon

- SKYi Composites Pvt. Ltd.

- Great Eastern Resins Industrial Co. Ltd.

- JNC Corporation

Frequently Asked Questions

The global carbon fiber reinforced thermoplastic composites (CFRTP) market is projected to reach US$1.8 billion in 2026.

Increasing demand for lightweight, high-strength, and recyclable materials in automotive, aerospace, and industrial applications.

The carbon fiber reinforced thermoplastic composites (CFRTP) market is expected to grow at a CAGR of 9.0% from 2026 to 2033.

Key market opportunities include the increasing adoption of lightweight materials in electric vehicles and aerospace, growth in emerging markets, advancements in automated and additive manufacturing, and the development of recyclable and sustainable thermoplastic composites.

The leading players include LANXESS, Solvay, PolyOne Corporation, RTP Company, Celanese Corporation, Avient Corporation, Daicel Corporation, Sumitomo Bakelite Co., Ltd., and Mitsubishi Chemical Corporation.