- Home Appliances

- Sustainable Home Decor Market

Sustainable Home Decor Market Size, Share, and Growth Forecast 2026 - 2033

Sustainable Home Decor Market by Product Type (Furniture, Home Textiles, Decorative Accessories, Lighting Fixtures, Flooring & Wall Coverings, Kitchen & Tableware), Material (Recycled/Upcycled Materials, Natural Fibers, Biodegradable Materials, Organic Materials, Reclaimed Wood, Others), Sales Channel (Online Retail, Offline Retail, Direct-to-Consumer, Specialty Stores/Eco-Boutiques, Home Decor Exhibitions), End-user, and Regional Analysis, 2026 - 2033

Sustainable Home Decor Market Size and Trend Analysis

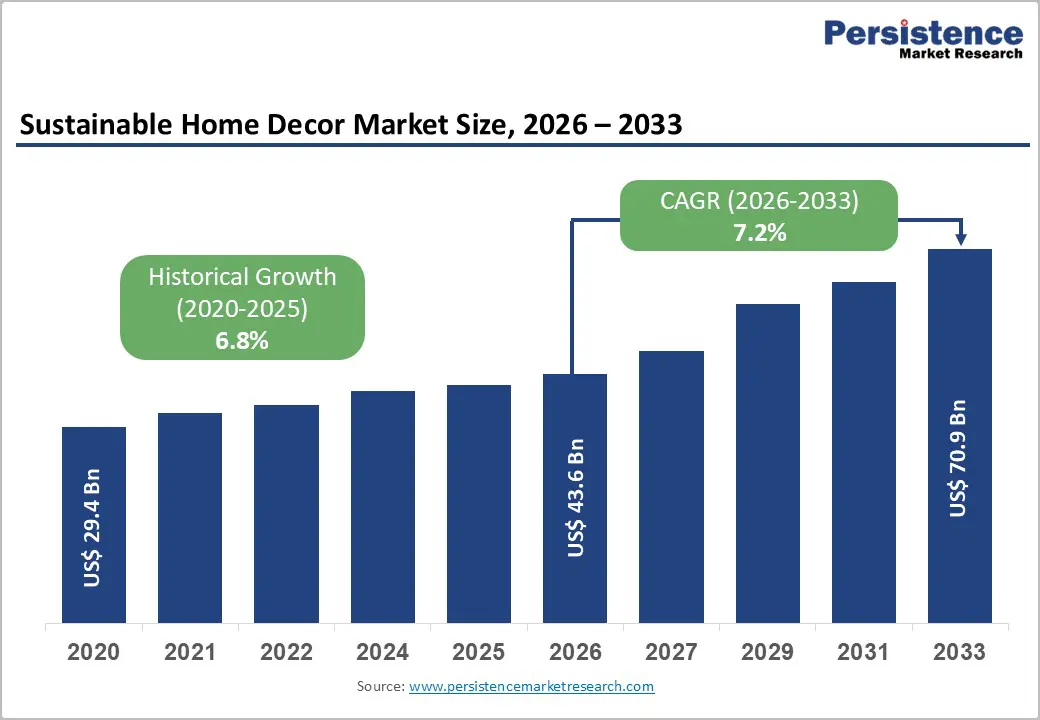

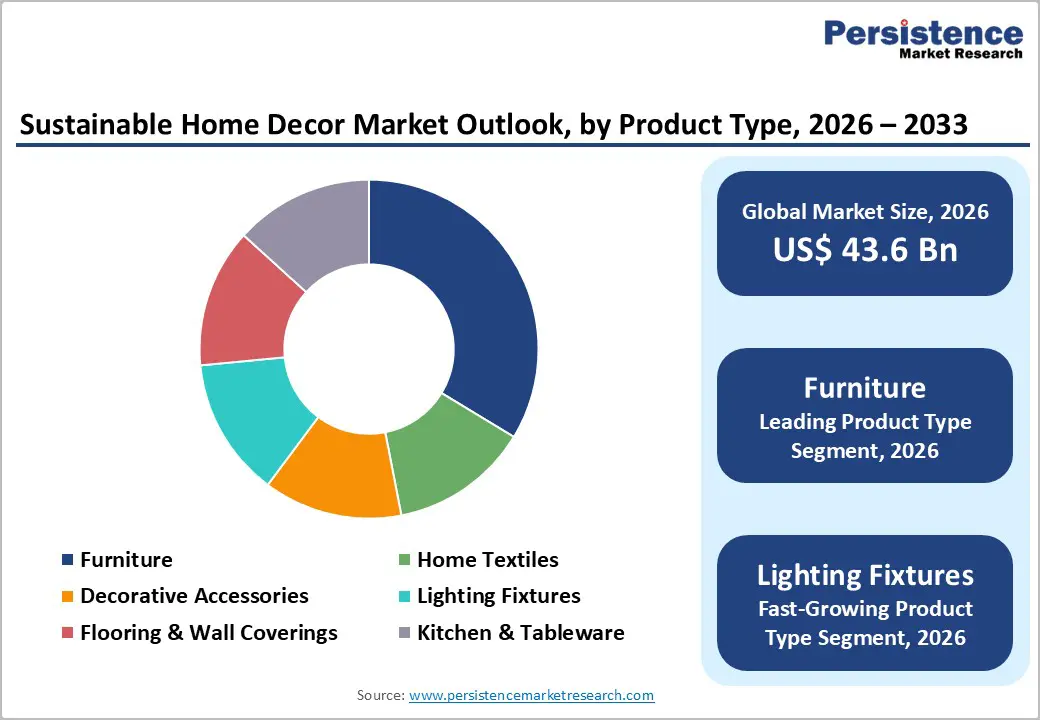

The global sustainable home decor market size is expected to be valued at US$ 43.6 billion in 2026 and projected to reach US$ 70.9 billion by 2033, growing at a CAGR of 7.2% between 2026 and 2033.

This robust acceleration is principally driven by a fundamental and deepening consumer shift toward environmentally responsible purchasing decisions, reinforced by expanding regulatory frameworks mandating sustainable product standards across major global economies. Rising millennial and Gen Z homeownership rates are amplifying demand for eco-certified furniture, natural fiber textiles, and zero-waste decorative accessories, while the rapid growth of direct-to-consumer sustainable lifestyle brands and green e-commerce platforms is expanding market accessibility. Progressive corporate sustainability mandates in commercial interior design, growing availability of certified eco-friendly product lines from mainstream retailers, and increasing disposable income in emerging economies collectively underpin the market’s sustained upward momentum through the forecast horizon.

Key Industry Highlights:

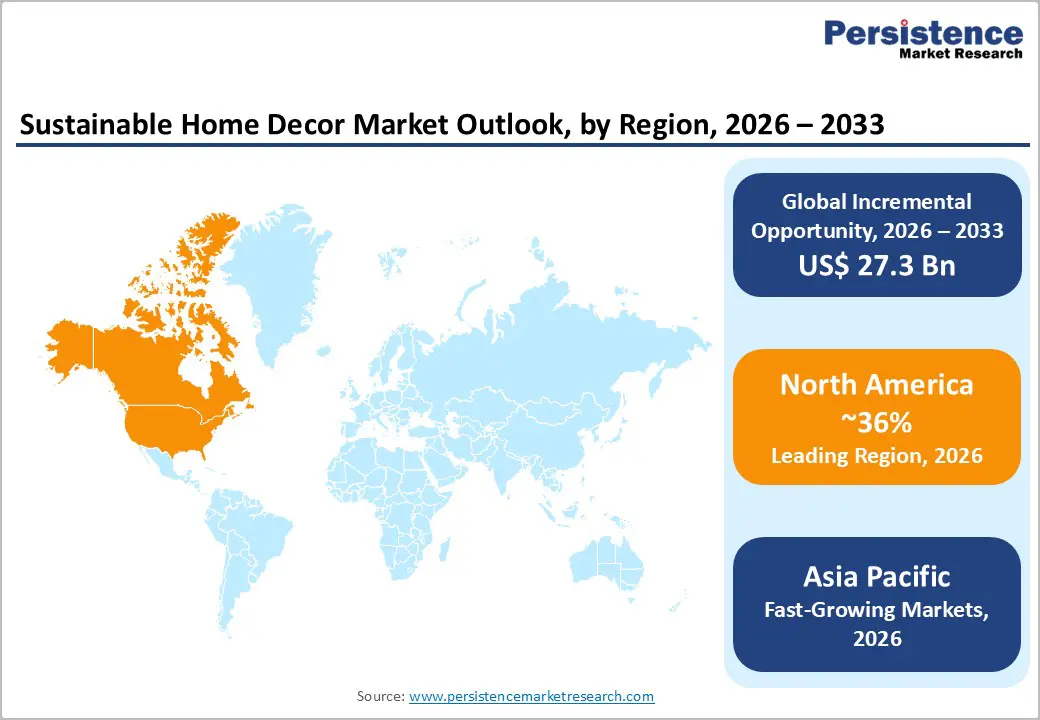

- Leading Region: North America leads the global sustainable home decor market, accounting for approximately 36% of revenue in 2025, underpinned by high consumer spending power, a mature ecosystem of certified sustainable brands, and strong institutional demand driven by LEED and WELL green building standards.

- Fastest Growing Region: Asia Pacific is the fastest growing regional market for 2026-2033, powered by China’s Dual Carbon policy, India’s expanding urban middle class, Japan’s deep cultural sustainability values, and rapidly growing eco-conscious consumer demographics across ASEAN markets.

- Dominant Segment: Furniture is the dominant product type segment with approximately 35% market share in 2025, reflecting its highest unit value among home decor categories and the significant consumer and regulatory focus on sustainable wood sourcing, non-toxic finishes, and circular design principles.

- Fastest Growing Segment: Zero-Waste Products are the fastest growing sustainability attribute segment, propelled by the expanding global zero-waste lifestyle movement, rising municipal plastic bans, and growing consumer demand for products designed around full circular material recovery and end-of-life sustainability.

- Key Opportunity: The commercial sector’s accelerating adoption of LEED, WELL, and corporate ESG-driven interior design mandates represents a substantial and high-volume institutional procurement opportunity for certified eco-friendly sustainable home decor products across offices, hospitality, and healthcare facilities globally.

| Key Insights | Details |

|---|---|

| Sustainable Home Decor Market Size (2026E) | US$ 43.6 Billion |

| Market Value Forecast (2033F) | US$ 70.9 Billion |

| Projected Growth CAGR (2026 - 2033) | 7.2% |

| Historical Market Growth (2020 - 2025) | 6.8% |

Market Dynamics

Drivers - Surging Consumer Environmental Consciousness and Shift Toward Conscious Living

The profound and accelerating shift in global consumer values toward sustainability and environmental responsibility is the single most powerful structural demand driver for the sustainable home decor market. According to the Nielsen Global Sustainability Report, approximately 73% of global consumers indicate they would definitely or probably change their consumption habits to reduce environmental impact, a trend most pronounced among millennials and Gen Z, who collectively represent the fastest-growing homeowning demographic. The United Nations Environment Programme (UNEP) consistently identifies household consumption, including home furnishings, textiles, and accessories, as one of the leading contributors to global resource depletion and carbon emissions, driving heightened consumer awareness of the environmental footprint of interior design choices. Brands such as West Elm, The Citizenry, and Coyuchi have capitalized on this shift through transparent supply chain communications, third-party sustainability certifications, and values-driven marketing, demonstrating that ethical brand positioning is now a primary purchase driver across premium and mid-market home decor segments.

Expanding Regulatory Frameworks Mandating Sustainable Products and Material Transparency

Government regulations and mandatory sustainability standards governing furniture, textiles, and construction materials are increasingly compelling manufacturers and retailers to accelerate the transition to certified, eco-friendly product lines, thereby expanding the addressable market for sustainable home decor. The European Union’s Ecodesign for Sustainable Products Regulation (ESPR, 2024) extends mandatory sustainability requirements to furniture, textiles, and interior products, requiring digital product passports disclosing material composition, repairability, and end-of-life recyclability. In the United States, the Environmental Protection Agency (EPA) and the California Air Resources Board (CARB) enforce stringent formaldehyde emission standards under CARB Phase 2 that have become the de facto national benchmark for composite wood products used in furniture manufacturing. The Forest Stewardship Council (FSC) and Rainforest Alliance certification standards, adopted as procurement requirements by major retailers such as IKEA and Pottery Barn, are further formalizing the market for sustainably sourced materials and finished products.

Restraints - Price Premium of Sustainable Products Limiting Mass-Market Adoption

Sustainably produced home decor products typically command a significant price premium over conventional alternatives. Eco-certified furniture, organic textiles, and reclaimed-wood accessories can cost 20-80% more than mass-market equivalents, depending on the product category and certification tier. A 2023 online survey indicated that while 60% of consumers express intent to purchase more sustainable products, only 34% actually follow through at the point of purchase when faced with the price differential, a gap known as the “intention-action” divide. For large-population, price-sensitive consumer segments in developing markets and lower-income demographics in developed economies, this pricing barrier represents a genuine and persistent constraint on sustainable home decor market penetration beyond affluent consumer brackets.

Greenwashing and Consumer Trust Deficits Undermining Market Credibility

The proliferation of unsubstantiated environmental claims, commonly referred to as greenwashing, is eroding consumer confidence in the sustainability credentials of home decor products and creating a significant trust deficit that suppresses purchasing decisions. The European Commission’s Green Claims Directive (2023) was introduced in direct response to findings that approximately 53% of green claims in European consumer markets were vague, misleading, or unsubstantiated, according to a sweep conducted by the European Commission’s Consumer Protection Cooperation (CPC) Network. In the United States, the Federal Trade Commission (FTC) has updated its Green Guides to combat misleading environmental marketing. This environment of consumer skepticism increases the due diligence burden on buyers and compels authentic brands to invest more in third-party verification, raising operational costs and extending go-to-market timelines.

Opportunities - Online Retail and Direct-to-Consumer Platforms Unlocking New Sustainable Consumer Demographics

The rapid proliferation of e-commerce and direct-to-consumer (DTC) digital platforms is creating a transformative opportunity for sustainable home decor brands to reach previously inaccessible consumer segments across geographies, income levels, and lifestyle profiles. According to UNCTAD, global e-commerce sales exceeded US$ 27 trillion in 2022 and continue to expand, with home furnishings and decor consistently ranking among the highest-growth online retail categories. Platforms such as Etsy have demonstrated the scalability of artisan, sustainable, and handcrafted home decor, with over 7.5 million active sellers offering eco-conscious, small-batch products to a global buyer base. The DTC model enables sustainable brands to bypass traditional retail intermediaries, communicate their environmental credentials directly to consumers through storytelling and transparency dashboards, and build loyal, values-aligned customer communities. Companies, including Avocado Green Brands and Coyuchi, have successfully leveraged DTC channels to achieve premium brand positioning and strong repeat purchase rates without relying on conventional retail infrastructure.

Commercial Sector Green Building Standards Driving Institutional Procurement of Eco-Friendly Decor

The accelerating global adoption of green building certification standards is generating a large, structured, and rapidly growing procurement opportunity for sustainable home decor products in commercial and institutional end-use settings. The U.S. Green Building Council (USGBC) reports that over 105,000 projects are currently participating in the LEED (Leadership in Energy and Environmental Design) certification program globally, with interior materials, low-emission finishes, and sustainably sourced furnishings directly contributing to certification points across LEED v4 and LEED v4.1 frameworks. Similarly, the WELL Building Standard, administered by the International WELL Building Institute (IWBI), specifies requirements for non-toxic, sustainable interior materials and furnishings in commercial offices, hospitality spaces, and healthcare facilities. As corporate ESG commitments intensify and green building certifications become standard specifications for commercial real estate developments globally, the institutional procurement of certified eco-friendly home decor products, from reclaimed wood furniture to organic textile soft furnishings, is set to represent a fast-growing and high-volume revenue channel for market participants through 2033.

Category-wise Analysis

Product Type Insights

Furniture is the leading product type segment in the sustainable home decor market, commanding approximately 35% of total market share in 2025. Its dominance reflects furniture’s position as the highest-unit-value product category within home decor, with individual purchases representing significant household expenditures, combined with growing consumer awareness of the environmental implications of conventional furniture manufacturing, which is associated with deforestation, toxic adhesives, and high carbon footprints. Major market participants including IKEA, which has committed to using only renewable or recycled materials by 2030 under its People & Planet Positive strategy, and West Elm, which sources through Fair Trade certified supply chains, are actively expanding their sustainable furniture portfolios to meet growing consumer and regulatory demand. The Forest Stewardship Council (FSC) reports that sales of FSC-certified timber products have grown consistently, reflecting the mainstreaming of sustainably sourced wood furniture. The fastest growing product segment is Lighting Fixtures, driven by the explosive adoption of energy-efficient LED lighting and smart home integration.

Material Insights

Recycled and upcycled materials are the leading segment in the sustainable home decor market, with an estimated 28% market share in 2025. This leadership position reflects both strong consumer appeal, with recycled-material products offering compelling sustainability narratives, and the broader industrial momentum behind circular-economy principles endorsed by regulatory frameworks, including the EU Circular Economy Action Plan (2020) and the U.S. EPA’s Sustainable Materials Management (SMM) Programme. The use of recycled plastics, reclaimed metals, upcycled glass, and post-consumer waste in decorative accessories, lighting fixtures, and flooring products has been actively championed by market leaders. IKEA’s commitment to circular product design and Pottery Barn’s use of recycled and reclaimed materials across select product lines demonstrate how mainstream retailers are leveraging this material category. The fastest growing material segment is Biodegradable Materials, propelled by zero-waste consumer movements and tightening packaging and product end-of-life regulations globally.

Sales Channel Insights

Online retail is the leading sales channel in the sustainable home decor market, accounting for approximately 38% of total channel revenue in 2025. The channel’s dominance is underpinned by the convergence of digital-native consumer behavior, particularly among millennials and Gen Z homeowners, and the inherent advantages of e-commerce in communicating complex sustainability credentials through rich product content, certification badges, supply chain transparency pages, and consumer reviews. The U.S. Census Bureau reports that e-commerce as a share of total U.S. retail sales has grown consistently, reaching approximately 15-16% of total retail by 2023, with home furnishings being among the most actively traded online categories. Platforms like Etsy and brand-owned DTC websites have been instrumental in democratizing access to sustainable home decor products from artisan and small-batch producers globally. The fastest-growing channel is Direct-to-Consumer (DTC), as brands increasingly invest in owned digital channels to maximize margins and build direct consumer relationships aligned with their sustainability mission.

End-user Insights

The residential segment leads the end-use category for sustainable home decor, accounting for approximately 62% of the market share in 2025. This dominance is structurally driven by the fundamental role of home environment in consumer identity expression, wellness, and quality of life, making residential purchasers the most emotionally and values-motivated buyers in the sustainable home decor ecosystem. Post-pandemic lifestyle shifts have intensified residential spending on home improvement and interior personalization, with the National Association of Realtors (NAR) in the U.S. noting a sustained elevation in home improvement expenditure. Millennial and Gen Z homeowners, who, according to the Pew Research Center, are now the largest generational group of home buyers in the United States, are disproportionately likely to prioritize sustainability credentials in home furnishing and decor purchases, reinforcing the residential segment’s market leadership. The fastest growing end-use segment is Commercial, driven by corporate ESG mandates and green building certification requirements.

Sustainability Attribute Insights

Certified eco-friendly products represent the dominant sustainability attribute segment, holding approximately 40% of total market share in 2025. This leadership reflects the growing consumer reliance on recognized third-party certifications as the primary mechanism for navigating an increasingly complex and often confusing landscape of environmental claims. Certifications including FSC (Forest Stewardship Council), OEKO-TEX Standard 100, Global Organic Textile Standard (GOTS), GREENGUARD Gold, and Cradle to Cradle (C2C) provide verifiable, independently audited assurances of product sustainability credentials, offering a decisive trust advantage over uncertified competitors. The OEKO-TEX Association reports that over 22,000 manufacturers and retailers across 100+ countries hold active OEKO-TEX certifications, reflecting the standard’s broad global adoption as a benchmark for textile sustainability. The fastest-growing sustainability attribute segment is Zero-Waste Products, propelled by the rising zero-waste lifestyle movement, expanding municipal plastic bans, and consumer demand for products designed for full circular end-of-life recovery.

Regional Insights

North America Sustainable Home Decor Market Trends and Insights

North America leads the global sustainable home decor market, accounting for approximately 36% of total revenue share in 2025. The United States is the dominant contributor, characterized by high consumer spending power, a deeply embedded culture of home improvement and interior design investment, and a rapidly maturing ecosystem of sustainable lifestyle brands. The U.S. Green Building Council (USGBC) reports over 105,000 LEED-certified and registered projects globally, with a substantial proportion concentrated in North America, directly generating institutional demand for certified sustainable interior products. State-level regulatory leadership, particularly California’s CARB Phase 2 formaldehyde emission standards and its extended producer responsibility (EPR) legislation, continues to raise the bar for product sustainability standards nationwide.

Consumer-facing innovation is also a hallmark of the North American market: companies including Avocado Green Brands, Coyuchi, The Citizenry, and Serena & Lily have built premium sustainable home decor brand identities centered on organic certifications, fair trade sourcing, and transparent supply chain disclosures. Pottery Barn’s partnership with the Rainforest Alliance and West Elm’s expansion of Fair Trade-certified products demonstrate how large-format retailers are mainstreaming sustainability credentials to meet growing shopper demand across multiple income demographics in the region.

Europe Sustainable Home Decor Market Trends and Insights

Europe is the second-largest regional market for sustainable home decor, with Germany, the United Kingdom, France, the Netherlands, and the Nordic countries being the most significant contributing markets. The European market is characterized by exceptionally high levels of regulatory-driven sustainability compliance, underpinned by the EU Green Deal, the Ecodesign for Sustainable Products Regulation (ESPR, 2024), and the EU Circular Economy Action Plan, all of which directly shape product design, material sourcing, and end-of-life requirements for home decor manufacturers operating in or exporting to the European market. Germany leads regional demand, reflecting its strong consumer preference for quality, durability, and environmental responsibility, and its highly developed retail infrastructure for premium sustainable furnishings.

In the United Kingdom, the Competition and Markets Authority (CMA) has actively pursued enforcement action against greenwashing in the retail sector, reinforcing consumer trust in certified sustainable products and raising market-entry standards for authentic eco-friendly brands. France’s Anti-Waste for a Circular Economy (AGEC) Law mandates repairability and material transparency for consumer products, directly advancing the adoption of sustainable home decor principles. The Nordic countries, particularly Sweden and Denmark, exhibit some of the highest per-capita expenditures on sustainable home furnishings globally, driven by deep cultural alignment with minimalist, nature-inspired, and long-lasting design philosophies.

Asia Pacific Sustainable Home Decor Market Trends and Insights

Asia Pacific is the fastest growing regional market for sustainable home decor, projected to record the highest regional CAGR during the forecast period, driven by a confluence of rising affluence, rapidly expanding middle-class homeownership, growing environmental awareness, and escalating government sustainability mandates across key economies. China is the region’s largest and most dynamic market, as both the world’s largest home decor manufacturing base and a rapidly growing domestic consumption market for premium sustainable products. The Chinese government’s “Beautiful China” (2035) ecological vision and “Dual Carbon” (carbon neutrality by 2060) policy framework are progressively encouraging sustainable material adoption across manufacturing and consumer products, while a growing cohort of urban, educated, environmentally conscious Chinese consumers is driving demand for certified eco-friendly interior products.

India is emerging as one of the most high-potential sustainable home decor growth markets, supported by an expanding urban middle class, a rich artisan and craft heritage that naturally aligns with sustainable and handmade product aesthetics, and growing consumer exposure to global sustainability standards. The Ministry of Environment, Forest and Climate Change (MoEFCC) of India’s advancing regulatory frameworks on material standards and the government’s National Action Plan on Climate Change (NAPCC) are progressively shaping sustainable consumption norms. In Japan, longstanding cultural principles of wabi-sabi (beauty in imperfection and impermanence) and mottainai (waste reduction) resonate strongly with sustainable home decor values, supporting strong demand for artisanal, natural-material, and long-lifecycle interior products. ASEAN markets, particularly Vietnam, Indonesia, and Thailand, are witnessing growing domestic sustainable home decor consumption alongside the development of export-oriented sustainable home furnishings manufacturing ecosystems.

Competitive Landscape

The global sustainable home decor market is highly fragmented, characterized by the presence of large multinational retailers, regional specialty brands, artisan-led enterprises, and digitally native direct-to-consumer startups operating across varied price points. Competition is shaped by product authenticity, sustainability credibility, supply chain transparency, and design differentiation. Large-scale players leverage global sourcing efficiencies, vertically integrated operations, and third-party eco-certifications to institutionalize sustainability across mass-market portfolios, while niche brands compete through purpose-driven positioning, limited-batch production, and traceable artisan networks.

Strategically, companies are expanding certified product assortments, embedding circular economy principles through recycling and take-back initiatives, and investing in low-carbon materials and responsible sourcing. Digital-first engagement models, storytelling-led marketing, and community-building strategies are increasingly central to brand equity development. Partnerships with green building projects and ESG-driven commercial buyers further provide scalable growth pathways within both residential and institutional segments.

Key Developments

- December, 2025: Westwing launches Danilo, a new furniture line crafted with recycled materials, reinforcing its commitment to sustainable design and eco-conscious home decor offerings.

- September, 2025: Renew Room Boards introduces its latest sustainable wall decor collection Renew Room Boards, featuring eco-friendly materials and nature-inspired designs for conscious home interiors.

- January, 2025: Niso Furniture, in collaboration with Kornit Digital, launched a one-of-a-kind sustainable home decor collection unveiled at Heimtextil 2025 in Frankfurt, featuring advanced digital printing and customizable eco-friendly designs.

Companies Covered in Sustainable Home Decor Market

- IKEA

- West Elm

- Pottery Barn

- The Citizenry

- Coyuchi

- Etsy

- Bambeco

- Avocado Green Brands

- Serena & Lily

- Bkr

- Urban Woods

- Unison

- Course Furniture

- Gathered Home

- MUD Australia

- Parachute Home

- Ten Thousand Villages

- Naturepedic

- Medley Home

- Reloved Rugs (Anthropologie Sustainable Line)

Frequently Asked Questions

The sustainable home décor market is projected to reach US$ 43.6 billion in 2026, driven by rising environmental awareness, regulatory standards, and expansion of certified eco-friendly product lines.

Growth is fueled by consumer preference for sustainable products, stricter environmental regulations, e-commerce expansion, and rising adoption of green building standards.

North America leads the market, supported by strong consumer spending, mature sustainable brands, and widespread LEED-certified projects.

Opportunities lie in commercial ESG-driven procurement and direct-to-consumer e-commerce expansion for certified sustainable brands.

The global sustainable home decor market features prominent players including IKEA, West Elm, Pottery Barn, Avocado Green Brands, Coyuchi, The Citizenry, Etsy, Serena & Lily, MUD Australia, Bambeco, Parachute Home, Gathered Home, Ten Thousand Villages, and Naturepedic, among others.