- Hardware & Software IT Services

- SOC as a Service Market

SOC as a Service Market Size, Share, and Growth Forecast, 2026 - 2033

SOC as a Service Market by Service Type (Detection Services, Incident Response Services, Prevention Services), Deployment Mode (Cloud-Native, Hybrid, Private Cloud), Organization Size (Large Enterprises, Small & Medium Enterprises (SMEs)), Application Area (Network Security, Cloud Security, Endpoint Security, Application Security, Misc.), Industry (Banking, Financial Services & Insurance (BFSI), IT & Telecom, Healthcare, Government & Public Sector, Retail & E-commerce) and Regional Analysis for 2026 - 2033

SOC as a Service Market Size and Trends Analysis

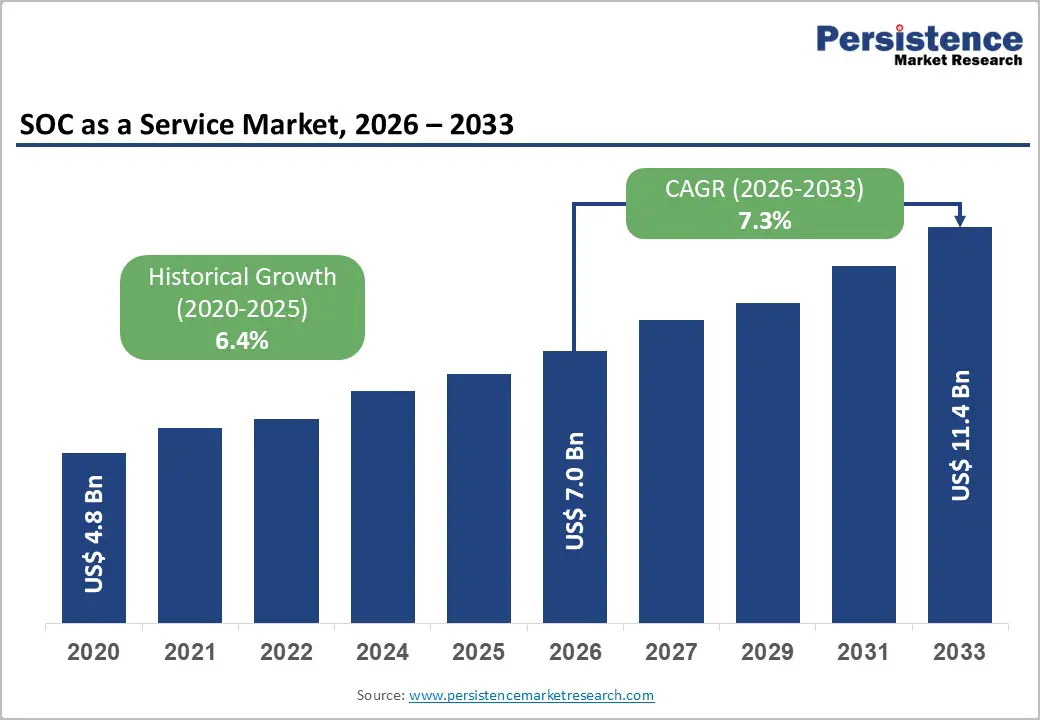

The global SOC-as-a-service market size is likely to reach US$ 7.0 billion in 2026 and is projected to reach US$ 11.4 billion by 2033, growing at a CAGR of 7.3% between 2026 and 2033.

This expansion reflects fundamental shifts in enterprise cybersecurity strategy, driven by the convergence of increasingly sophisticated threats, critical workforce shortages of skilled security professionals, and stringent regulatory mandates across industries. The SOC as a service market has evolved from a specialised offering for large enterprises to a business-critical service across organisational sizes, with acceleration in regulated sectors including financial services, healthcare, and government institutions that require continuous threat monitoring and rapid incident containment capabilities.

Key Industry Highlights:

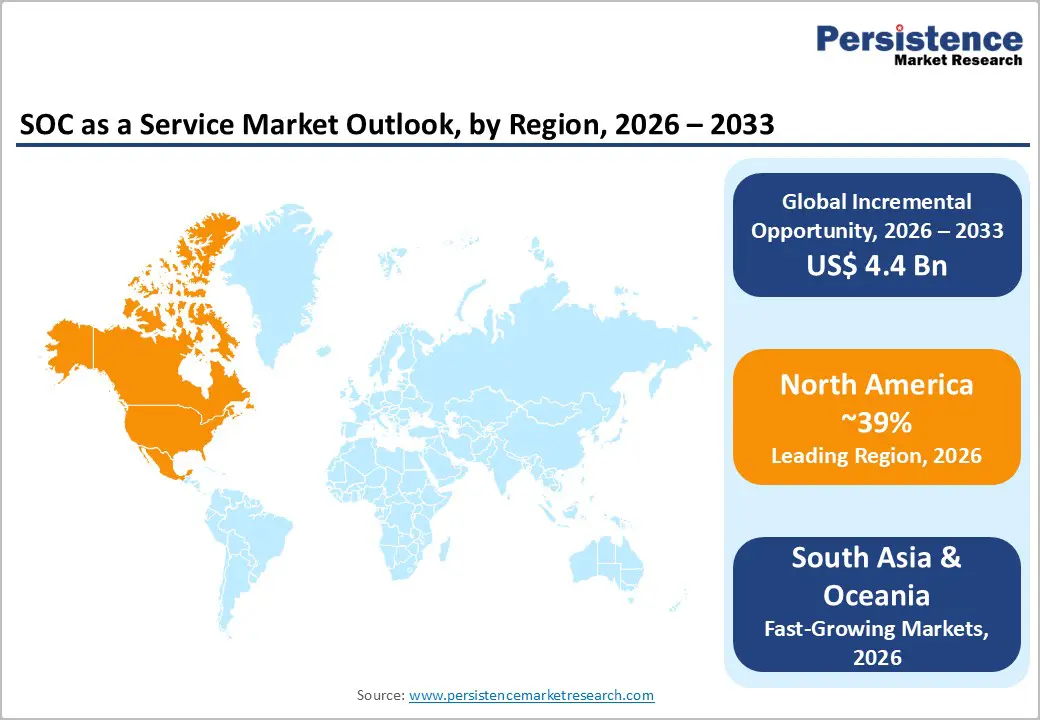

- Regional Leadership: North America leads the global SOC as a Service market with ~39% share, supported by strong regulatory enforcement, high cybersecurity maturity among enterprises, and widespread adoption of managed security services across BFSI, healthcare, and critical infrastructure sectors.

- Fast-growing Markets: East Asia holds ~18% share and represents the fastest-growing regional market, driven by rapid digitalisation, expanding cloud adoption, tightening cybersecurity regulations, and rising threat exposure across China, Japan, and South Korea.

- Leading Service Segment: Detection Services dominate the SOC as a Service market with ~40% share, reflecting enterprises’ primary need for continuous threat visibility, SIEM-led monitoring, and compliance-aligned detection across hybrid IT environments.

- Fastest-Growing Service: Incident Response Services are the fastest-growing segment, benefiting from escalating ransomware sophistication, stricter regulatory scrutiny on response quality, and growing reliance on expert-led containment and forensic support.

| Key Insights | Details |

|---|---|

| SOC as a Service Market Size (2026E) | US$ 7.0 Bn |

| Market Value Forecast (2033F) | US$ 11.4 Bn |

| Projected Growth (CAGR 2026 to 2033) | 7.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.4% |

Market Dynamics

Critical Global Cybersecurity Skills Shortage and Operational Complexity

The SOC as a Service Market operates in an environment shaped by an unprecedented shortage of qualified cybersecurity professionals. As of 2025, the global cybersecurity workforce faces a deficit of 4.8 million unfilled roles, representing the widest talent gap in the industry's history. This shortage is not merely quantitative; 90% of organisations report skills gaps within their security teams, with critical deficiencies across AI-driven threat detection, in which 33% of organizations cite it as the top shortfall, cloud security (30%), zero-trust architecture (27%), and incident response capabilities (25%).

Organisations experiencing high-level skills shortages encounter breach costs of US$ 5.74 million on average, compared to US$ 3.98 million for those with minimal shortage, a differential of US$ 1.76 million directly attributable to inadequate security capability. The extended dwell time resulting from understaffed and skill-depleted security teams allows attackers to penetrate deeper into networks, exfiltrate sensitive data, and cause substantial damage.

The market represents a strategic response, enabling organisations to access expert-led detection, triage, and incident response without requiring massive internal recruitment, training, or retention investments. This driver is particularly acute in Asia-Pacific, where rapid digitalisation coincides with limited local talent pools, and in Europe, where GDPR compliance and NIS2 incident reporting obligations demand 24/7 operational readiness that most mid-market organisations cannot sustain in-house.

Rise of Ransomware Complexity and Nation-State Threat Evolution

The ransomware landscape has undergone a fundamental transformation, shifting from opportunistic, commodity-based attacks toward sophisticated, state-sponsored and AI-augmented operations. In 2024, over 5,600 ransomware attacks were publicly disclosed globally, with more than 2,600 targeting U.S. organisations, representing a sustained threat vector despite increased defensive awareness.

Dark web analysis reveals a 25% year-over-year increase in ransomware activity between 2024 and 2025, indicating an accelerated operational tempo among threat actors. Critically, emerging ransomware groups such as FunkSec have adopted AI-assisted development practices, automated code generation and deploying sophisticated auction platforms (FunkBID) for victim data exploitation, fundamentally raising the bar for manual SOC analyst response capacity. Ransomware operators increasingly employ double-extortion tactics, exfiltrating data before encryption, then leveraging multiple pressure vectors to coerce payment, extending the incident timeline and escalating business impact.

SOC as a Service Market has become instrumental in defending against these sophisticated attack patterns, as managed providers maintain continuous threat intelligence feeds, deploy advanced detection algorithms across client estates, and execute coordinated response playbooks that transcend individual organisational capability. This driver is particularly pronounced in critical infrastructure sectors where ransomware targeting has accelerated, and in BFSI verticals where regulatory mandates (RBI's 6-hour breach notification requirement for banks in India, NYDFS MFA requirements for financial institutions) necessitate sub-hour detection and containment protocols that managed SOC providers can deliver.

Regulatory Mandate Proliferation and Compliance Reporting Intensity

Regulatory bodies globally have substantially hardened cybersecurity and incident reporting requirements, effectively mandating managed SOC capabilities as a compliance foundation. The GDPR requires breach notification within 72 hours, forcing organizations to establish detection and containment infrastructure capable of rapid threat identification. The European Union's NIS2 Directive mandates 24-hour incident reporting to national authorities, eliminating the feasibility of delayed or asynchronous incident response. In the financial services sector, India's RBI cybersecurity framework requires commercial banks to report cybersecurity incidents to the Cyber Security and IT Examination Cell within 6 hours for critical incidents, and mandates annual cyber audits conducted by RBI-approved auditors.

The NYDFS cybersecurity requirements (amended November 2023) obligate financial institutions to implement quarterly CISO reporting to boards, annual penetration testing, and comprehensive vulnerability management, which require continuous monitoring infrastructure. In China, regulatory oversight of the banking sector has tightened similarly, with the China Banking and Insurance Regulatory Commission imposing strict information security and operational resilience requirements on financial institutions.

SOC as a Service Market directly addresses these regulatory imperatives by delivering audit-ready monitoring, forensically sound incident documentation, and compliance-aligned response protocols that satisfy regulatory examination standards. Organizations in BFSI, healthcare, government, and critical infrastructure sectors increasingly view managed SOC services as mandatory compliance infrastructure rather than discretionary security enhancement, with procurement decisions driven explicitly by regulatory examination findings and breach notification mandates.

Restraint - Cost Sensitivity and Budget Allocation Challenges in Economic Uncertainty

Despite the recognised need for managed SOC services, budget constraints have emerged as a primary barrier to adoption. In 2024, cybersecurity budgets grew only 8%, a significant deceleration from the 16-17% growth observed in 2021-2022, driven by macroeconomic uncertainty and inflation pressures.

Organisations have shifted their procurement focus to foundational security investments, with internal assessments accounting for around 60% of discretionary spending and IAM programs accounting for around 58%, diverting resources from managed services toward point solutions. Staffing and compensation account for 37% of security budgets, creating internal trade-offs between hiring and outsourcing decisions that often favour retaining in-house capability over adopting managed services, particularly in large enterprises with existing SOC infrastructure. This restraint particularly affects mid-market organizations that lack economies of scale to absorb managed SOC costs, potentially driving adoption delays in high-growth regions like East Asia, where budget constraints are more acute.

Opportunity - AI-Augmented Detection and Tier-1 Automation in Resource-Constrained Environments

Advanced AI and machine learning technologies are fundamentally reshaping SOC labour economics. Recent strategic developments underscore the industry's pivot toward AI-native SOC platforms: Exaforce's August 2025 launch of an AI-native, agentic SOC platform combined with a fully managed MDR service represents a paradigm shift from traditional tier-1 analyst automation toward end-to-end AI-driven detection, triage, investigation, hunting, and response across the entire security operations lifecycle.

KPMG's September 2025 adoption of CrowdStrike's Next-Gen SIEM powered by AI enables the delivery of advanced SOC services (managed detection, faster incident response) with substantially reduced human analyst dependency, directly addressing the skills shortage constraint. These developments indicate that Market will be capable of delivering expert-level security outcomes at lower operational cost, improving the unit economics of managed services and expanding the addressable market to mid-market and smaller enterprises that historically viewed SOC outsourcing as unaffordable.

Organisations seeking to optimise operational overhead while maintaining compliance-grade security monitoring represent a substantial opportunity for AI-augmented SOC providers, particularly in the BFSI sector, where regulatory mandates drive adoption regardless of cost-optimisation initiatives.

Cloud Migration Acceleration and Multi-Cloud Security Complexity

Enterprise cloud adoption has reached an inflexion point, with most organisations now operating cloud environments and increasingly relying on multi-cloud architectures that combine multiple public cloud platforms with on-premises infrastructure. A growing share of new digital products and features is being built directly in the cloud, signalling a long-term architectural shift. This migration has significantly increased the complexity of security monitoring, as cloud workloads require fundamentally different detection approaches than traditional on-premises systems, particularly across containerised microservices, serverless workloads, and distributed identity frameworks.

The Market is well-positioned to capture this opportunity by integrating cloud-native security capabilities, such as cloud access security and workload protection, into unified monitoring platforms. As cloud security spending accelerates faster than overall cybersecurity budgets, managed SOC providers are benefiting from widening skill gaps in cloud-specific threat detection. Verticals such as IT & Telecom and Healthcare, which are adopting cloud technologies rapidly, represent immediate growth opportunities for SOC providers aligned with cloud infrastructure modernisation initiatives.

Category-wise Analysis

Service Type Insights

Detection Services maintain market dominance with 40% market share in 2026, reflecting organizations' primary need for continuous threat identification across heterogeneous IT environments. This segment encompasses security information and event management (SIEM) infrastructure, intrusion detection system (IDS) operations, and behavioural anomaly analysis, which collectively identify unauthorised network activity, malware execution, and data exfiltration attempts. Detection services form the operational foundation of the managed SOC value proposition, as rapid threat identification directly enables compliance with breach notification timelines (72-hour GDPR requirement, 6-hour RBI reporting requirement for Indian BFSI institutions) and reduces attacker dwell time from historical averages of 200+ days to detection windows measured in hours.

Incident response services are expanding at the fastest rate within the SOC as a Service Market, driven by regulatory mandates requiring documented, contemporaneous response protocols and escalating sophistication of ransomware attacks that demand expert-led containment beyond automated response playbooks. Incident response encompasses forensic analysis, lateral movement containment, attacker eviction, and evidence preservation, functions that require deep security expertise and executive communication capabilities that many organisations cannot sustain internally. The regulatory emphasis on incident response quality (reflected in SEBI's requirement for BFSI institutions to demonstrate control effectiveness under pressure) is driving demand for managed incident response integrated with detection infrastructure, rather than detection-only SOC models.

Industry Insights

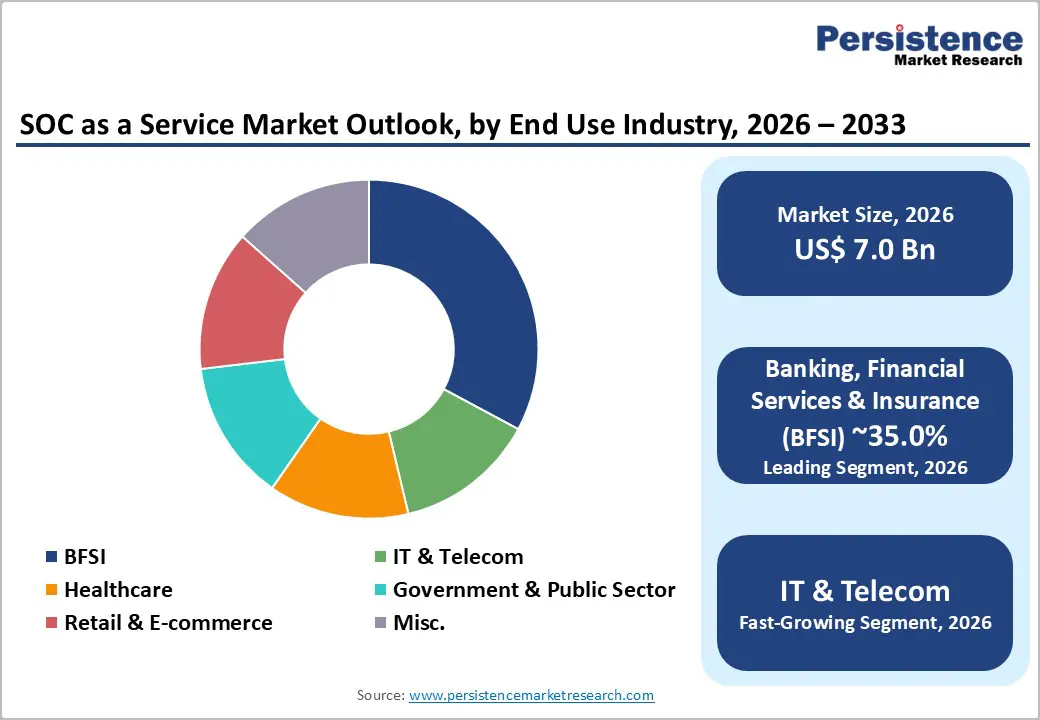

The Banking, Financial Services, and Insurance (BFSI) sector commands approximately 35% market share in the SOC as a Service Market in 2026, reflecting regulatory mandates, sophisticated threat targeting, and high-consequence breach impacts that create strong economic justification for managed security operations. India's BFSI sector has demonstrated exceptional growth, expanding from Rs. 1,80,000 crore (US$ 20.28 billion) in 2005 to Rs. 91,00,000 crore (US$ 1 trillion) in 2025, now contributing 27% to India's GDP (up from 6% in 2005), with substantially improved financial health metrics (gross NPAs declining from 5.8% in FY22 to 2.2% in FY25).

Europe's BFSI sector generated €0.9 trillion in value added in 2022, employed nearly 5 million people, and had banking assets of €43.6 trillion in 2023. China's banking assets reached RMB 467.3 trillion in Q2 2025 (7.9% YoY growth), with insurance assets at RMB 39.2 trillion (9.2% YoY growth), maintaining NPL ratios of 1.49% and capital adequacy ratios of 15.58%. The BFSI sector's adoption of SOC as a Service reflects both regulatory examination pressure (RBI's 6-hour incident reporting requirement, SEBI's control effectiveness mandates, NYDFS MFA requirements for financial institutions) and organizational maturity in cybersecurity governance, with BFSI institutions typically among the first to adopt managed security operations within geographic markets.

The IT & Telecom sector is the fastest-growing end-use industry within the SOC as a Service Market, driven by business model dependency on continuous infrastructure availability and substantial compliance obligations across multiple regulatory frameworks. India's telecom sector recorded 1.21 billion subscribers and 86.09% tele-density as of June 2025, with gross telecom revenue reaching US$ 43.42 billion in FY25 (up from US$ 39.22 billion in FY24).

The sector's fundamental reliance on 24/7 network operations, expanding 5G infrastructure (which contributed nearly 25% of wireless data usage in FY25), and the breadth of its attack surface, with recent ransomware targeting telecommunications infrastructure globally, create a compelling economic and operational justification for managed SOC adoption. Europe's information and communication services sector comprises 1.4 million enterprises, employs 7.2 million people, and generated €667 billion in value added in 2022, with computer programming and consultancy accounting for 59.8% of employment. IT & Telecom sector growth in SOC adoption is driven by both external regulatory pressure and internal recognition that continuous infrastructure security monitoring is foundational to business continuity.

Regional Insights and Trends

North America SOC as a Service Market Trends

North America commands 39% of the Global SOC as a service market, reflecting organisational maturity in cybersecurity governance and substantial regulatory mandate density. The region's SOC market is driven by NYDFS cybersecurity requirements, HIPAA Security Rule mandates for healthcare organisations, and SEC cybersecurity disclosure requirements, creating executive-level accountability for breach management.

Organisations in North America demonstrate a higher propensity for managed security services adoption compared to other regions, with approximately 60% of endpoint and cloud managed security market value concentrated among large enterprises requiring 24/7 SOC coverage.

The market is characterised by consolidation among major managed security providers, with strategic acquisitions (Sophos' USD 859 million acquisition of Secureworks in 2023, Palo Alto Networks' pursuit of SentinelOne) reflecting vendor emphasis on comprehensive endpoint-to-cloud security capabilities integrated with managed SOC operations. SMB adoption in North America is constrained by cost sensitivity and IT resource availability, though cloud-based SOC models are enabling SMB penetration, particularly in high-threat sectors where breach costs justify managed service investments.

East Asia SOC as a Service Market Trends

East Asia represents 18% of the global SOC as a service market, with particularly strong growth trajectories in China, South Korea and Japan, driven by digital transformation initiatives and rising threat awareness. China's digital ecosystem reached 1.108 billion internet users by December 2024, with mobile internet users representing 99.7% of all internet users, creating substantial endpoint and network security monitoring requirements. China's cybersecurity regulatory framework (Cybersecurity Law, Data Security Law) mandates localised SOC operations, creating opportunities for domestic providers and constraints for international managed service vendors unable to maintain onshore infrastructure.

East Asia remains the fastest-growing regional market for SOC as a Service, driven by regulatory mandate acceleration and relatively lower managed service market penetration compared to mature North American and European markets.

Europe SOC as a Service Market Trends

Europe accounts for 22% of the global SOC as a service market, with growth constrained by organisational preference for in-house SOC models in large enterprises, data sovereignty regulations limiting multi-tenant managed service adoption, and competitive intensity among European managed security providers.

The EU's financial services sector, €0.9 trillion value added, 5 million employees across nearly 867,000 enterprises and the banking sector (€43.6 trillion in assets, 5,304 credit institutions), represents the primary market for SOC services, with regulatory examination and compliance reporting standards equivalent to or exceeding North American frameworks. Regional data sovereignty requirements and the prohibition on unrestricted international data flows limit the applicability of globally distributed, multi-tenant SOC models, effectively requiring regional SOC infrastructure for major service providers, increasing operational costs and reducing competitive advantage through economies of scale.

Competitive Landscape

Global SOC as a service market exhibits a moderately consolidated to competitive landscape, driven by both large cybersecurity vendors and specialised managed service providers vying for market share. Established global players with broad security portfolios, such as IBM Corporation, Fortinet Inc., Thales, Cloudflare, Inc., and Verizon, leverage their extensive technology stacks and global delivery capabilities to secure enterprise clients and regulatory-heavy sectors.

Niche SOCaaS specialists like Arctic Wolf Networks and ConnectWise, LLC. Differentiate through cloud-native platforms and concierge-style security operations, intensifying competition and innovation in offerings. Regional heavyweights like NTT and AT&T further reinforce the competitive environment by scaling managed SOC services across diverse markets. While the top tier of vendors holds significant influence, the presence of numerous mid-tier and emerging providers keeping pace with AI-driven detection and MDR services indicates a dynamic market with high entry and innovation activity. Overall, SOCaaS is evolving rapidly, with strategic partnerships, AI integration, and service differentiation shaping competitive positioning.

Key Industry Developments

- August 26, 2025 - Exaforce introduced an AI-native, agentic SOC platform combined with a fully managed MDR service, applying multi-model AI across the entire SOC lifecycle, threat detection, triage, investigation, hunting, and response. This development is highly significant as it represents the shift toward end-to-end, AI-powered SOCaaS models, reducing operational overhead while delivering expert-level security outcomes, and sets a new benchmark for next-generation SOC capabilities.

- September 22, 2025 - KPMG / CrowdStrike: KPMG expanded its SOCaaS capabilities by adopting CrowdStrike’s Falcon Next-Gen SIEM and broadening the platform via the Engagement License Program, enabling AI-powered SOC services, faster incident response, and legacy SIEM transformation. This development is notable because it highlights the convergence of next-generation SIEM platforms with outsourced, intelligence-driven SOC service models, reflecting the growing enterprise demand for AI-enhanced, managed security operations.

Companies Covered in SOC as a Service Market

- Check Point Software Technologies Ltd.

- International Business Machines Corporation (IBM Corporation)

- Atos SE

- Thales Group

- Verizon Communications Inc.

- Fortinet, Inc.

- Cloudflare, Inc.

- Arctic Wolf Networks, Inc.

- AT&T Inc.

- Nippon Telegraph and Telephone Corporation (NTT)

- Clearnetwork, Inc.

- ConnectWise, LLC

- Teceze, Inc.

- Eventus Security, Inc.

- Kaseya Limited

Frequently Asked Questions

Global SOC as a Service Market is projected to be valued at US$ 7.0 Bn in 2026.

The Detection Services segment is expected to account for approximately 40% of the Global SOC as a Service Market by Service Type in 2026.

The market is expected to witness a CAGR of 7.3% from 2026 to 2033.

The SOC as a Service Market growth is driven by the global cybersecurity skills shortage, rising ransomware and advanced threat complexity, and increasingly stringent regulatory and compliance mandates that require continuous monitoring, rapid incident response, and audit-ready security operations.

Key market opportunities in the SOC as a Service Market lie in AI-augmented, automation-driven SOC models that reduce analyst dependency amid skills shortages, and in cloud-native, multi-cloud security monitoring services addressing rising complexity from large-scale cloud migration across regulated and cloud-intensive industries.

Key players in the SOC as a Service Market include IBM Corporation, Fortinet Inc., Check Point Software Technologies, Arctic Wolf Networks, and AT&T.