- Specialty & Fine Chemicals

- Polyisocyanurate Insulation Market

Polyisocyanurate Insulation Market Size, Share, and Growth Forecast 2025 - 2032

Polyisocyanurate Insulation Market By Product Type (Laminated Panels, Others), Application (Walls, Roofs/Ceilings, Others), End-user (Residential Construction, Commercial Construction, Others), and Regional Analysis for 2025 - 2032

Polyisocyanurate Insulation Market Size and Trends Analysis

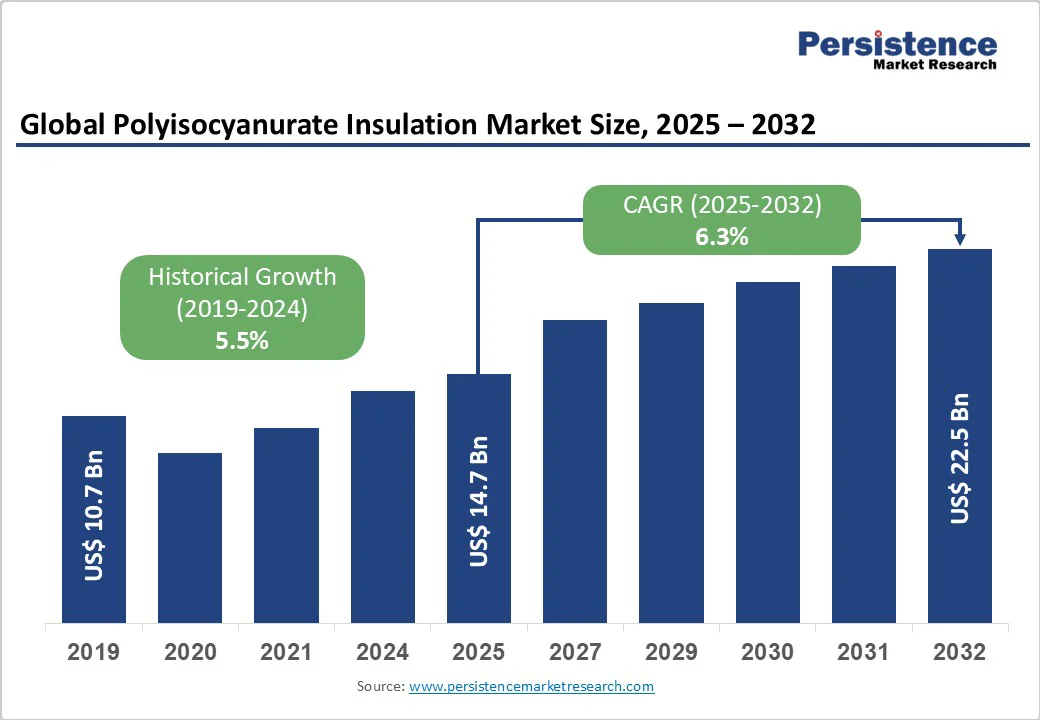

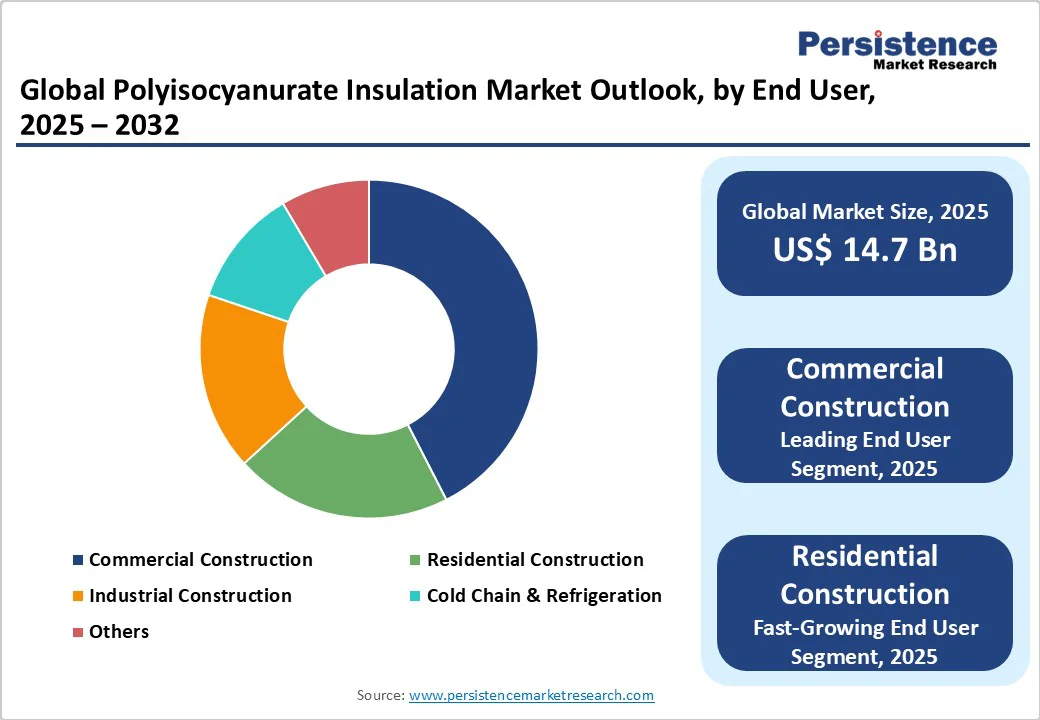

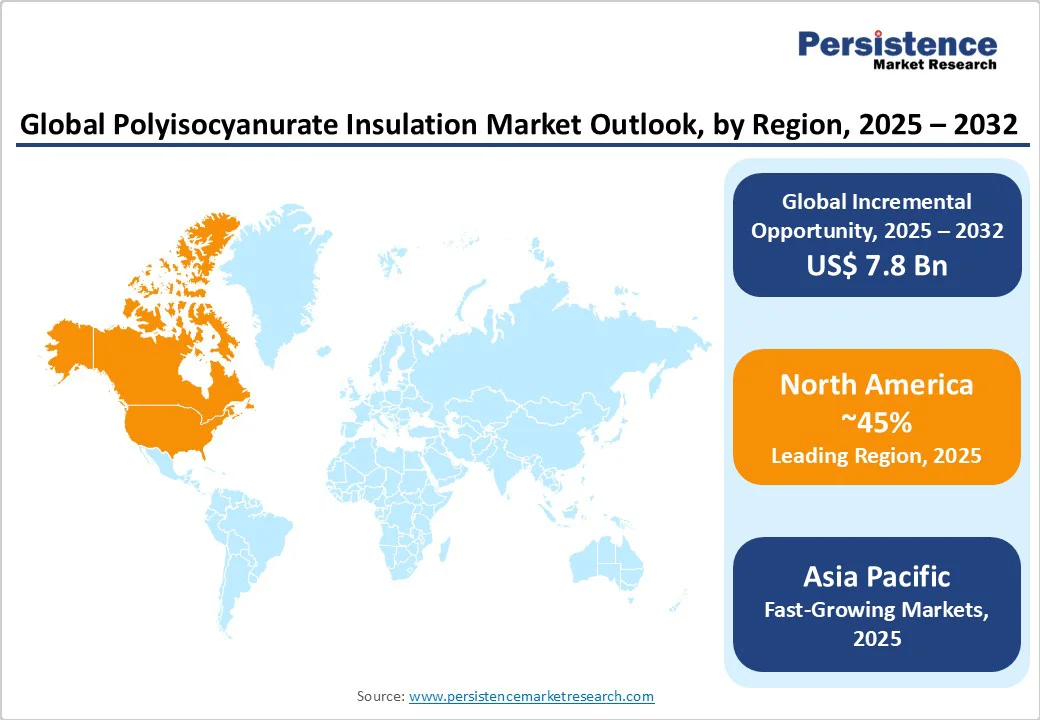

The global polyisocyanurate insulation market size was valued at US$14.7 Billion in 2025 and is projected to reach US$22.5 Billion by 2032, growing at a CAGR of 6.3% during the forecast period from 2025 to 2032, driven by stringent building energy-efficiency regulations and increasing demand for high-performance thermal insulation across the residential, commercial, and industrial construction sectors.

Polyisocyanurate (PIR) insulation offers superior thermal performance, with R-values of 6.5-7.0 per inch, higher than conventional materials. The 2024 IECC, mandating 7.8% site energy savings, is accelerating its adoption in energy-efficient building envelopes.

Key Market Highlights:

- Leading Region: North America leads the PIR insulation market, driven by strict energy codes such as the 2024 IECC and mature commercial construction, ensuring high thermal performance.

- Fastest Growing Region: Asia Pacific grows fastest, fueled by urbanization, housing initiatives, and stricter energy efficiency standards in China, India, and ASEAN countries.

- Dominant Segment: Rigid boards hold ~47% share, widely used in roofs and walls for commercial buildings due to thin profiles and excellent thermal conductivity (0.020-0.022 W/mK).

- Fastest Growing Segment: Cold chain and refrigeration applications rise rapidly, supported by PIR’s temperature tolerance and moisture resistance for pharmaceutical and food logistics.

- Key Market Opportunity: Building retrofits and renovations drive demand, with EU and U.S. energy efficiency mandates targeting low-performing existing structures.

| Key Insights | Details |

|---|---|

| Polyisocyanurate Insulation Market Size (2025E) | US$14.7 Bn |

| Market Value Forecast (2032F) | US$22.5 Bn |

| Projected Growth CAGR (2025 - 2032) | 6.3% |

| Historical Market Growth (2019 - 2024) | 5.5% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Stringent Energy Efficiency Regulations Accelerating PIR Adoption

Global mandates for improved building energy performance are driving the rapid adoption of polyisocyanurate (PIR) insulation across construction sectors. The U.S. Department of Energy’s 2024 IECC determination demonstrates energy savings of nearly 8%, emphasizing stricter insulation standards that favor materials such as PIR for superior thermal efficiency.

Similarly, the EU’s revised Energy Performance of Buildings Directive (EPBD), effective May 2024, requires all new public buildings to be Zero-Emission by 2028 and all new builds by 2030. These frameworks prioritize insulation materials with low thermal conductivity (as low as 0.023 W/mK), a benchmark PIR consistently achieves.

With buildings contributing roughly 28% of global energy-related CO? emissions (IEA), regulators are tightening thermal efficiency norms to cut operational emissions. This trend places PIR insulation at the forefront of compliance-driven material demand, reinforcing its role as a key enabler in achieving net-zero and sustainable construction goals worldwide.

Rapid Urbanization and Construction Sector Expansion in Emerging Markets

Accelerating construction across emerging economies-particularly in Asia Pacific-is propelling demand for efficient, durable insulation solutions. India’s insulation materials market is set to rise from USD 2.4 billion in 2024 to USD 3.95 billion by 2035, driven by initiatives such as Housing for All and the Smart Cities Mission, both of which emphasize energy-efficient construction. Simultaneously, China and India are expected to contribute 40% of global foam insulation growth through 2025, with PIR gaining prominence in commercial and industrial infrastructure.

Government regulations such as India’s Energy Conservation Building Code (ECBC) and China’s Green Building Evaluation Standard mandate advanced roof and wall insulation, further supporting PIR’s market penetration. With production capacity of polyurethane and polyisocyanurate foam up 8.5% in 2024, the supply landscape is aligning with the region’s urban development surge, ensuring PIR’s sustained adoption in modern, energy-conscious construction projects.

Barrier Analysis - High Initial Cost Compared to Conventional Insulation Materials

Polyisocyanurate (PIR) insulation’s higher upfront cost compared to conventional materials remains a key restraint to wider adoption. Although PIR offers superior thermal efficiency, achieving R-values between 6.5-7.0 per inch versus polyurethane’s 5.0-6.0, it typically costs 15-20% more, which deters uptake in cost-sensitive residential projects. In markets where initial investment takes precedence over lifecycle energy savings, this cost disparity limits market penetration.

Advanced PIR grades with enhanced fire and moisture resistance command additional premiums, restricting use to high-spec commercial and industrial buildings. Price fluctuations in core feedstocks such as isocyanates and polyols, driven by supply chain volatility and energy price swings, further create uncertainty in procurement, undermining long-term pricing stability and budget predictability for builders and contractors.

Technical Installation Requirements and Regional Climate Variations

Achieving optimal PIR insulation performance requires skilled installation to prevent moisture ingress and thermal bridging, a challenge in markets with limited trained labor. Even minor shrinkage capped at less than 1% during manufacturing can result in perimeter gaps that compromise vapor barrier effectiveness if not addressed through precise, staggered layering during installation.

The diversity of climatic conditions, especially in countries such as India with hot, humid, and composite zones, necessitates region-specific insulation design strategies. This variability complicates standardization and product specification, slowing broader adoption. The prevalence of small-scale manufacturers producing inconsistent-quality panels further erodes builder confidence, while limited testing and certification infrastructure impede consistent performance validation across varied environmental and structural applications.

Opportunity Analysis - Cold Chain and Refrigeration Infrastructure Expansion

The rapid development of cold storage and refrigeration infrastructure globally creates substantial opportunities for polyisocyanurate (PIR) insulation suppliers. PIR panels, with an approximate density of 30 kg/m³, deliver superior thermal resistance and moisture control essential for maintaining precise temperature conditions in refrigerated environments. Compared to polyurethane (PUR) alternatives, PIR offers improved vapor resistance and longer lifespan, making it well-suited for high-humidity applications such as cold warehouses, food logistics, and pharmaceutical storage facilities.

PIR’s wide temperature service range of -297°F to +300°F (-183°C to 148°C) enables use in cryogenic systems, LNG storage, and ammonia refrigeration lines. As the HVAC insulation market grows, projected to reach US$10.82 Billion by 2035, polyisocyanurate’s >90% closed-cell structure positions it as the preferred solution for energy-efficient duct, pipe, and refrigeration insulation systems.

Retrofit and Building Renovation Market Potential

The global push for energy-efficient building upgrades provides strong growth momentum for polyisocyanurate insulation. In Europe, around 85% of buildings were constructed before 2000, and 75% perform poorly on energy efficiency, yet renovation rates remain near 1% annually. The EU’s Energy Performance of Buildings Directive (EPBD) mandates renovation of 16% of the worst-performing non-residential buildings by 2030 and 26% by 2033, stimulating significant PIR insulation adoption.

In the U.S., insulation imports increased 7.6% in 2024 due to a rise in retrofitting to meet new efficiency codes. Industrial retrofits in refineries and manufacturing plants are also boosting demand for advanced thermal materials. With high R-values and thinner profiles, PIR enables energy efficiency without sacrificing usable space, making it ideal for retrofitting aging structures where interior dimensions and installation constraints are key considerations.

Category-wise Analysis

Product Type Insights

Rigid boards account for roughly 47% of the polyisocyanurate insulation market in 2025, driven by widespread usage in commercial roofing and wall systems. These boards feature a lightweight foam core (around 30 kg/m³) sandwiched between aluminum foil, glass tissue, or kraft paper facings, offering excellent thermal performance with lambda values between 0.020-0.022 W/mK. This enables thinner insulation layers without compromising efficiency, an advantage in space-constrained commercial buildings.

Prefabricated PIR sandwich panels, combining steel facings with a rigid foam core, are widely used in warehouses, factories, and office structures. Their superior dimensional stability, moisture resistance, and consistent performance across temperature variations make rigid boards the preferred choice for roofing, wall cladding, and general building envelope applications.

Application Insights

Roof and ceiling applications dominate polyisocyanurate insulation usage, comprising about 42% of the market in 2025. PIR’s high compressive strength (over 115 kN/m²) and low thermal conductivity support compliance with U-value regulations of 0.13-0.18 W/m²K in modern roofing systems. Despite reduced efficiency mandates under the 2024 IECC, PIR remains favored for its thin profile and high energy performance.

Foil-laminated PIR panels are also essential in HVAC duct insulation and refrigeration systems. The material’s closed-cell structure offers strong vapor barrier properties and consistent performance across extreme temperatures from cryogenic to high-heat environments, aligning with ASHRAE recommendations and the rapidly growing HVAC insulation market.

End-user Insights

Commercial construction leads end-use demand, accounting for about 44% of the polyisocyanurate insulation market in 2025. This dominance stems from stringent building codes and retrofit initiatives targeting office, retail, and institutional facilities. The EU EPBD directive drives large-scale renovations, mandating improved energy performance for 16-26% of non-residential buildings by 2033.

PIR insulation meets BS 476 fire safety standards and contributes to LEED and BREEAM certifications with CFC/HCFC-free, low-GWP formulations. Its durability, high R-value, and moisture resistance make it ideal for sustainable commercial infrastructure. Integration with building automation systems further enhances HVAC efficiency, positioning PIR as a cornerstone of modern, energy-optimized construction.

Regional Insights

North America Polyisocyanurate Insulation Market Trends

North America leads the market, driven by stringent regulatory frameworks and a well-developed construction sector. The 2024 International Energy Conservation Code (IECC), published by the International Code Council (ICC), mandates updated efficiency standards across building envelope components.

The U.S. Department of Energy confirmed 7.8% energy savings over the 2021 edition, further boosting PIR insulation adoption. Flexible residential compliance pathways and revised ceiling and wall insulation requirements under the new IECC version encourage broader application across residential and commercial projects.

Regional innovation emphasizes sustainable product development, with leading manufacturers investing in bio-based polyols and low-emission production methods. Rising retrofitting activities, accounting for a 7.6% increase in insulation imports in 2024, highlight regulatory compliance efforts.

Cold storage and refrigeration infrastructure expansion, especially in walk-in freezers and refrigerated transport, continues to drive PIR demand due to its broad service temperature range and strong moisture resistance.

Europe Polyisocyanurate Insulation Market Trends

Europe remains a pivotal growth region under the influence of the European Green Deal and the revised Energy Performance of Buildings Directive (EPBD, EU/2024/1275). Effective from May 2024, the directive requires Zero-Emission Buildings (ZEBs) for public structures by 2028 and all new buildings by 2030. As buildings contribute 40% of EU energy consumption and 36% of emissions, with 75% performing poorly, the renovation and retrofit market for high-efficiency insulation materials has become a major growth avenue.

Leading nations such as Germany, France, the UK, and Spain are implementing harmonized building codes with strict U-values (0.13-0.18 W/m²K). This regulation, coupled with mandates to renovate the least efficient 16% of buildings by 2030, positions PIR as a preferred solution due to its low thermal conductivity of 0.020-0.022 W/mK. Regional manufacturers, including BASF SE, Saint-Gobain, and Kingspan, are expanding production capacity, boosting market penetration and technological advancement across Europe.

Asia Pacific Polyisocyanurate Insulation Market Trends

Asia Pacific represents the fastest-growing regional market for polyisocyanurate insulation, underpinned by rapid urbanization and government-driven energy efficiency mandates. India’s building insulation market is evolving rapidly, supported by initiatives such as “Housing for All” and Smart Cities Mission, expected to reach US$3.95 Billion by 2035. Regulatory programs such as the Energy Conservation Building Code (ECBC) drive PIR adoption in commercial buildings, while IGBC and GRIHA certifications promote its integration in sustainable construction.

China and India together account for nearly 40% of global foam insulation growth, driven by expanding cold storage, industrial, and commercial infrastructure. The IEA highlights the need for a 45% reduction in building energy intensity across ASEAN by 2030, further stimulating high-performance insulation demand. With low-cost manufacturing, robust supply chains, and rising technical capabilities, the Asia Pacific is emerging as both a key consumer and a global export hub for PIR insulation materials.

Competitive Landscape

The global polyisocyanurate insulation market is moderately consolidated, with leading multinational corporations holding significant market share while regional manufacturers compete through localized production, cost efficiency, and niche applications. Market competition is defined by innovation in material performance, compliance with evolving building standards, and sustainability-focused product differentiation.

Key strategic priorities include capacity expansion, R&D investments, and integration across the value chain to enhance operational efficiency. Leading producers emphasize advancements such as bio-based formulations, superior fire performance, and smart building compatibility. Strategic mergers and acquisitions continue to refine the competitive landscape, strengthening product portfolios and regional market positioning.

Key Market Developments:

- In October 2024, Knauf Group agreed to acquire Texnopark’s Rock Mineral Wool insulation division in Tashkent, Uzbekistan. The facility features advanced electric melting technology that significantly reduces CO? emissions during production, reinforcing Knauf’s commitment to sustainable manufacturing and expanding its footprint in Central Asia’s insulation materials market.

- In October 2024, BASF expanded its Neopor® (graphite EPS) production capacity at the Ludwigshafen site by 50,000 metric tons. The initiative aims to meet rising demand for energy-efficient insulation materials in Europe while advancing BASF’s sustainability goals through improved resource efficiency and lower lifecycle carbon emissions across its high-performance insulation product portfolio.

- In April 2024, Kingspan launched new high-performance PIR insulation boards tailored for commercial building applications. These products deliver enhanced thermal efficiency, fire resistance, and sustainability credentials, aligning with modern building energy codes and supporting global efforts to improve construction sector energy performance and environmental compliance standards.

Companies Covered in Polyisocyanurate Insulation Market

- Johns Manville

- Owens Corning

- Kingspan Group

- Dow Chemical Company

- Hunter Panels

- Atlas Roofing Corporation

- DowDuPont Inc.

- Saint-Gobain

- Huntsman Corporation

- GAF Materials Corporation

- BASF SE

- Honeywell International Inc.

- IKO Industries Ltd.

- Rmax Operating LLC

- Rockwool International

- Knauf Insulation

- Armacell

- Thermaflex

- Celotex

Frequently Asked Questions

The polyisocyanurate insulation market is projected to reach US$22.5 Billion by 2032 from US$14.7 Billion in 2025, growing at a CAGR of 6.3%, driven by stricter energy codes and rising commercial and refrigeration applications.

Key drivers include strict energy efficiency regulations (2024 IECC, EU EPBD), high thermal performance (R-values 6.5-7.0/inch), and expanding construction in emerging markets, including China and India.

Rigid boards lead with ~47% share, used in roofs and walls for superior thermal conductivity (0.020-0.022 W/mK) and space-efficient installation.

Asia Pacific, led by India and China, is driven by urbanization, government initiatives, and evolving energy codes.

Building retrofits and renovations, especially in the EU and the U.S., are driven by energy code compliance and aging building stock.

Major companies include Kingspan, Owens Corning, BASF, Saint-Gobain, Johns Manville, and others, competing via innovation, sustainability, and capacity expansion.