- Industrial Machinery

- Small Engine Market

Small Engine Market Size, Share, Trends, Growth, Regional Forecasts 2025 - 2032

Small Engine Market by Engine Displacement (Upto 100 cc, 101-300 cc, 301-600 cc, 601-1000 cc), Application (Domestic, Gardening, Construction), Fuel Type (Gasoline, Diesel), and Regional Analysis 2025 - 2032

Small Engine Market Share and Trends Analysis

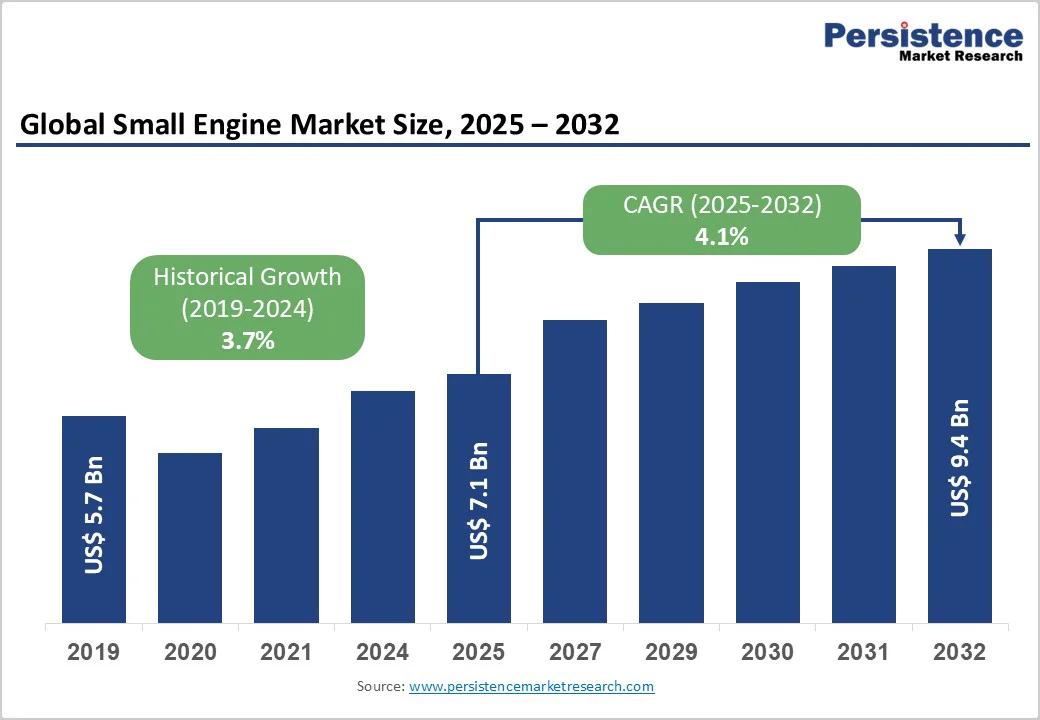

The global small engine market size is likely to value at US$ 7.1 billion in 2025 and is projected to reach US$ 9.4 Billion by 2032, growing at a CAGR of 4.1% between 2025 and 2032.

Market expansion is primarily driven by rising urbanization and mechanization across agricultural, construction, and landscaping sectors, coupled with increasing demand for portable outdoor power equipment in both residential and commercial applications.

The transition toward fuel-efficient engines and hybrid-electric technologies, spurred by stringent emission regulations from environmental regulatory bodies such as the EPA and European Commission, is reshaping product development strategies across the industry.

Key Highlights Summary

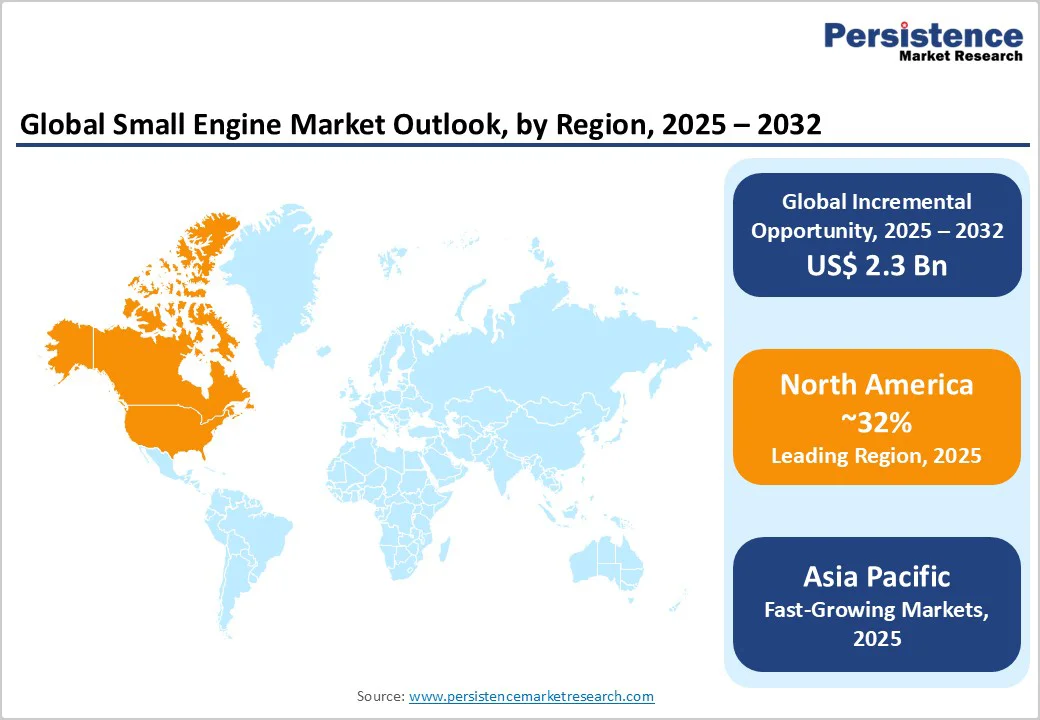

- Asia Pacific demonstrates the strongest growth momentum at 4.9% CAGR, capturing increasing global market share through rapid industrialization and infrastructure modernization

- North America maintains a significant regional position with 32% market share and 3.7% CAGR, reflecting mature market characteristics

- 101-300 cc engine displacement maintains market dominance with 38% market share, while 301-600 cc+ segment expands at an accelerated 4.7% CAGR

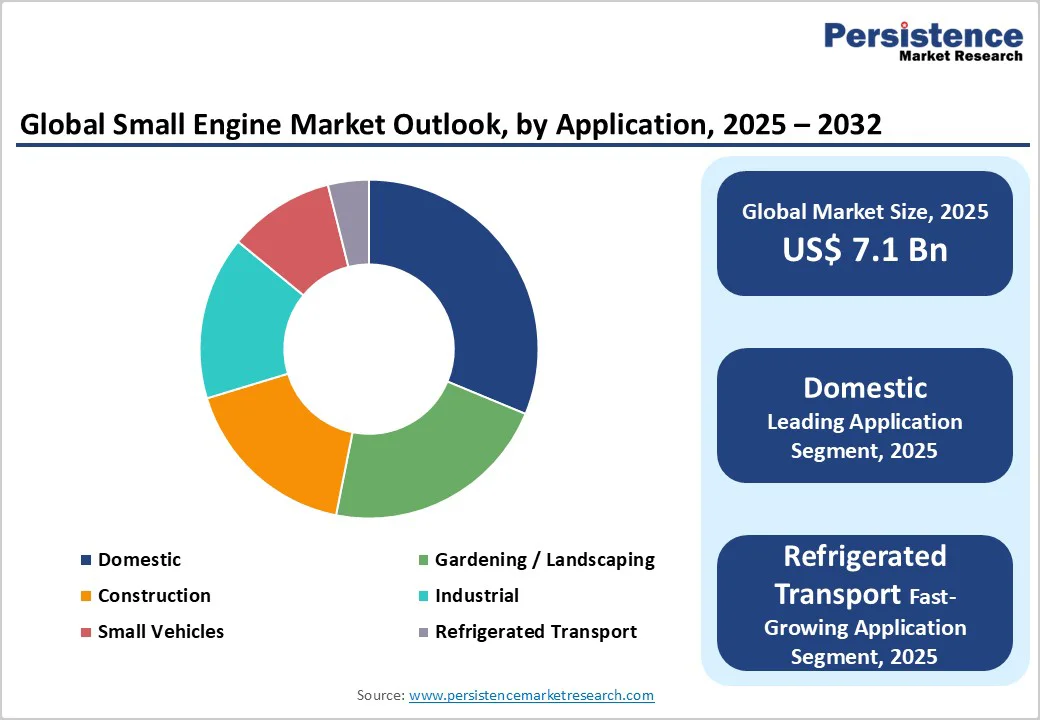

- Domestic/residential applications lead with 31% market share, while refrigerated transport emerges as the fastest-growing segment at 5.3% CAGR

- Gasoline fuels remain dominant with 78% market share, supported by adoption of commercial applications

- Hybrid-electric engine technology adoption represents an emerging competitive frontier, with manufacturers investing substantially in hybrid propulsion development targeting 15-25% market capture potential by 2032

- Strategic M&A activities and product innovation focus on emission compliance technology, fuel efficiency enhancement, and specialized application segment development

| Key Insights | Details |

|---|---|

| Small Engines Market Size (2025E) | US$ 7.1 billion |

| Market Value Forecast (2032F) | US$ 9.4 billion |

| Projected Growth CAGR (2025 - 2032) | 4.1% |

| Historical Market Growth (2019 - 2024) | 3.7% |

Market Dynamics Analysis

Drivers - Rising Urbanization and Residential Outdoor Living Trends

Urbanization continues to be a significant catalyst for small engine market expansion, with the global urban population expected to reach 68% by 2050, compared to 55% in 2018. This demographic shift correlates directly with increased demand for residential landscaping and outdoor maintenance equipment.

In North America, over 82% of the population lives in urban areas, and approximately 60% of apartment dwellers are allocating increased space to gardening areas. The DIY landscaping trend has gained substantial momentum, with homeowners increasingly choosing to maintain their own properties rather than hiring professional services.

This consumer behavior shift is particularly pronounced in developed economies where disposable income levels support equipment purchases.

The residential outdoor power equipment market, which heavily relies on small engines for lawnmowers, chainsaws, and trimmers, generated significant demand, contributing to market growth. Furthermore, the expansion of commercial landscaping services in suburban and urban areas has created additional demand for small engine-powered equipment, with municipalities increasingly investing in green space maintenance and beautification initiatives.

Recreational Vehicle Adoption and Adventure Tourism

The global recreational and powersport vehicle market is projected to grow at a prominent pace at a CAGR of 4.5%. Small engines are the primary propulsion systems for this sector, including ATVs, motorcycles, scooters, and recreational equipment. The ATVs and 2/3-wheeler market segment alone is expected to witness robust growth with a CAGR of 6.5%.

The expansion is driven by rising consumer interest in outdoor recreational activities, adventure tourism, and off-road sports events. Globally, approximately 10 million ATVs were sold in 2023 alone, reflecting strong consumer demand.

North America leads this category, with the United States hosting multiple high-profile racing championships such as the World Off-Road Championship Series (WORCS), comprising nine events across five states, attracting over 50,000 spectators annually.

The proliferation of adventure tourism operators investing in ATV fleets for commercial rental purposes further amplifies market demand. Additionally, increasing disposable income in developed economies and expanding middle-class consumer bases in emerging markets such as India and Southeast Asia are accelerating the adoption rates of powersport vehicles.

Restraint - Increasing Adoption of Electric and Battery-Powered Equipment Alternatives

Growing environmental awareness, emission regulations, and technological advancements are accelerating the global shift toward cleaner power solutions in outdoor and small engine applications.

The small engine market faces mounting substitution pressure from battery-powered and electric alternatives that deliver lower operational costs, reduced noise, minimal maintenance, and zero emissions. Accelerating advances in lithium-ion technology now enable 60-90 minute runtimes and faster charging, fueling rapid adoption across residential and commercial users.

The U.S. EPA highlights that gasoline mowers emit high pollutant levels, prompting municipalities and landscapers to embrace electric models for sustainability compliance. This electrification shift represents a structural headwind for internal combustion engines, as declining battery costs and rising energy density enable near performance parity with gasoline units.

The small power battery market is expanding at nearly 15% CAGR, reaching cost parity in many residential segments, though combustion engines remain essential for extended runtime, heavy-duty, and off-grid applications.

Stringent Emissions Regulations and Compliance Costs

Emissions regulations represent a structural challenge to small engine manufacturers globally. The European Union's Euro 7 regulation, which entered into force on May 28, 2024, imposes increasingly stringent emissions standards for heavy-duty vehicles, with nitrogen oxide (NOx) emission limits reduced by 50% and particulate matter limits reduced by 20% compared to previous Euro VI standards.

For light-duty vehicles, Euro 7 introduces new limits for non-methane organic gases (NMOG), methane (CH4), ammonia (NH3), and nitrous oxide (N2O), representing a comprehensive overhaul of emissions control requirements.

In the United States, the EPA has proposed new multi-pollutant emissions standards for light- and medium-duty vehicles effective from model year 2027 onward, requiring approximately 85% reduction in NOx emissions compared to current levels. Regulatory mandates require significant R&D investments for advanced fuel injection systems, catalytic converters, and aftertreatment technologies.

For smaller engine manufacturers, compliance costs can take up 15-20% of production expenses, affecting profitability and competitiveness. The fragmented market, with many regional players, creates technical and financial barriers for developing universal compliance platforms.

Opportunity - Hybrid-Electric Engine Technology Development

The integration of advanced technologies such as electronic fuel injection (EFI), smart sensors, and hybrid propulsion systems is creating substantial growth avenues in the small engine market. Briggs & Stratton’s 2024 launch of the Vanguard 300 exemplifies innovation toward higher performance and reduced maintenance through intelligent fuel management.

Hybrid small engines that merge fuel combustion with electric assistance deliver 15-20% improved fuel efficiency and lower emissions without compromising power. IoT-enabled smart sensors further enhance engine health monitoring, predictive maintenance, and remote diagnostics, extending equipment lifespan by up to 30%.

Growing manufacturer investment in hybrid technology positions it as a bridge toward full electrification, balancing performance with sustainability. Market projections suggest hybrid small engines could account for 15-25% of total demand by 2032, offering strong opportunities in both premium and cost-sensitive markets.

Niche Application Segments and Industrial Integration

Specialized industrial uses such as portable generators for backup power, irrigation pumps for agriculture, and compact construction machinery are unlocking new growth avenues in the small engine market. Increasing demand from equipment rental businesses and rural electrification projects further reinforces market depth across diversified sectors.

Refrigerated transport applications, projected to grow at a 5.3% CAGR, highlight a strong vertical expansion supported by global cold chain logistics growth and modernization of food distribution infrastructure. Simultaneously, small recreational vehicles and micro-utility applications are gaining traction in regions with limited or unreliable grid access.

Manufacturers focusing on developing purpose-built engines tailored to specific duty cycles, power ranges, and environmental conditions can achieve premium pricing and stronger customer retention. These niche, high-value segments collectively enable differentiation, improved margins, and sustained competitive advantage in a maturing global market landscape.

Category-wise Analysis

By Engine Displacement Insights

The 101-300 CC displacement segment leads the global small engine market with a 38% revenue share, reflecting its adaptability across residential lawnmowers, portable generators, and light construction machinery. Balancing power, fuel efficiency, and affordability, this range appeals to both homeowners and professionals.

The broader 101-400 CC category accounted for nearly 47% of 2024 small gas engine revenue, supported by mature supply chains and integration of advanced technologies such as electronic throttle bodies and oxygen sensors. OEMs continue investing heavily in this range to maintain performance and compliance, as seen in Honda’s iGX-series fuel-injection systems designed to enhance combustion efficiency and reduce emissions.

The 601-1000 CC range is witnessing the fastest growth at a 4.7% CAGR, driven by rising demand for heavy-duty zero-turn mowers, standby generators, industrial stationary equipment, and high-performance recreational vehicles. These engines cater to commercial landscaping, municipal operations, and enthusiast markets where reliability, extended runtime, and superior power output command premium pricing and robust margins.

Application Insights

The domestic application segment, encompassing residential gardening, landscaping, and home maintenance equipment, accounts for 31% of the global small engine market.

The demand is fueled by expanding urbanization, growing property ownership, and lifestyle shifts favoring outdoor living and aesthetic landscaping. Equipment such as walk-behind lawnmowers, trimmers, chainsaws, leaf blowers, and pressure washers dominate this category.

Lawnmowers alone contribute roughly 35% of global domestic revenue, supported by steady replacement cycles, new housing developments, and the strong DIY culture prevalent in North America and Northern Europe. Rising disposable incomes in emerging economies further strengthen consumer adoption of powered garden tools.

The refrigerated transport segment represents the fastest-growing application. This category includes small engines powering refrigeration units in light commercial vehicles and portable cold-chain systems. Growth is underpinned by expanding temperature-controlled logistics networks, surging e-commerce food delivery, and rising demand for perishable goods in emerging markets across Asia, Latin America, and Africa.

Fuel Type Insights

Gasoline-powered small engines dominate the global market at a 78% share, driven by their accessibility, ease of use, and well-established production infrastructure. Their simple design architecture ensures lighter weight, lower manufacturing complexity, and cost efficiency compared to diesel counterparts. The widespread availability of gasoline across global retail networks supports consumer convenience and operational reliability.

Gasoline engines also offer superior power-to-weight ratios, making them ideal for portable tools such as chainsaws, trimmers, and handheld equipment where mobility and compactness are critical. A robust aftermarket ecosystem of spare parts, repair services, and skilled technicians further strengthens their long-standing market leadership.

Diesel-powered small engines, meanwhile, are registering rapid expansion at a 4.7% CAGR, primarily within industrial, agricultural, and heavy-duty applications requiring high torque and long operating life.

Offering 20-30% greater fuel efficiency than gasoline equivalents, diesel engines deliver lower lifetime operating costs and enhanced durability under continuous load conditions. As emission control technologies advance, diesel power units are increasingly meeting stringent environmental standards, reinforcing their adoption in regulated and cost-sensitive commercial environments.

Regional Market Insights

North America Small Engine Market Trends

North America remains the largest small engine market globally, accounting for around 32% of total revenue in 2025. The United States drives regional dominance through widespread residential lawn ownership, high disposable incomes, and robust commercial landscaping demand.

Lawnmowers represent the leading application with a significant share under Gardening / Landscaping equipment revenue, propelled by suburban maintenance trends and the growth of professional landscaping services. Canada is emerging as the fastest-growing market, with cold climate conditions driving strong sales of snow removal equipment, portable generators, and heating solutions.

The region also demonstrates sustained generator demand across residential and construction sectors due to grid reliability concerns and rising emphasis on emergency preparedness.

North America adheres to stringent U.S. EPA Tier 4 Final and California Advanced Clean Fleets emissions regulations, compelling engine manufacturers to advance fuel and emissions technologies. This regulatory framework fosters innovation-driven competition while reinforcing environmental responsibility. A mature aftermarket ecosystem, extensive service infrastructure, and strong distribution networks further sustain the region’s long-term market leadership.

Europe Small Engine Market Trends

Europe accounts for 26% of global small engine market revenue, led by Germany, the United Kingdom, France, and Spain as primary market hubs. The region’s strong regulatory emphasis on sustainability and early adoption of alternative propulsion technologies have shaped its competitive landscape, with battery-powered equipment achieving higher penetration than in North America.

Germany serves as Europe’s technological nucleus, driving innovation in fuel injection, combustion optimization, and emissions control systems. The U.K. remains a major market for residential outdoor power equipment, supported by a strong DIY culture and professional landscaping services. France and Spain are witnessing steady growth, driven by rising suburbanization and expanding residential construction activities.

The Euro 7 regulation, effective from May 2024, enforces unified emissions and noise standards across EU member states, compelling manufacturers to adopt advanced, cleaner technologies. While compliance raises R&D costs, it also encourages innovation in quieter, high-performance small engines. European consumers’ preference for premium, feature-rich equipment supports higher price realization and sustained manufacturer profitability.

Asia Pacific Small Engine Market Trends

Asia Pacific stands as the fastest-growing regional market, expanding at a strong 4.9% CAGR and steadily increasing its global market share as emerging economies boost infrastructure and agricultural mechanization. China dominates the regional landscape, accounting for 40% of the small off-road engine market through vast manufacturing capacity, export-oriented production, and growing domestic consumption driven by urbanization.

Japan maintains a technology-driven presence with a focus on premium efficiency and sustainability, while India emerges as a high-growth hub with a 4.2% CAGR, fueled by rising middle-class demand, agricultural modernization, and infrastructure investment. ASEAN nations(Thailand, Vietnam, and Indonesia) also show strong momentum, propelled by construction growth and expanding commercial equipment adoption.

Asia Pacific leads global small engine manufacturing, with China and India offering cost advantages and export competitiveness. India’s labor cost of USD 1.5 per hour versus China’s USD 7, coupled with improved logistics and Bharat Stage V emissions alignment, positions it as a key global production base.

China’s mature manufacturing ecosystem, deep R&D expertise, and integrated supply chains accelerate technology commercialization, while the region’s under-mechanized agricultural sector presents vast long-term potential for affordable, efficient small engine solutions.

Competitive Landscape

The global small engine market exhibits a moderately fragmented competitive structure with significant market concentration among established multinational manufacturers.

Leading global players, including Briggs & Stratton, Honda Motor, Kohler, and Yamaha, collectively maintain approximately 35-40% global market share, benefiting from extensive distribution networks and comprehensive product portfolios. Asian manufacturers, including Loncin and Lifan are capturing increasing market share through cost-competitive offerings. Specialized niche players focus on premium commercial applications or high-end residential markets.

Strategic Developments

- Briggs & Stratton Vanguard 300 Series Launch (August 2024) : Briggs & Stratton introduced the Vanguard 300 series, featuring advanced emission control technologies and lower total cost of ownership positioning for commercial equipment applications, demonstrating manufacturer's commitment to premium commercial segment differentiation.

- GE Aerospace Partnership with Kratos Turbine Technologies (July 2024) : Strategic partnership targeting development of small engines for unmanned aerial systems and advanced technology applications, reflecting emerging market applications beyond traditional landscaping and construction segments.

- Briggs & Stratton E-Commerce Platform Enhancement (2024) : Enhanced e-commerce capabilities enabling direct customer access to product specifications and online purchasing functionality, with the 750EX Series featuring 25% improved fuel efficiency compared to prior-generation engines.

Companies Covered in Small Engine Market

- Briggs & Stratton Corporation

- Honda Motor Co., Ltd.

- Kohler Co.

- Yamaha Motor Co., Ltd.

- Kawasaki Heavy Industries

- Kubota Corporation

- Generac Holdings Inc.

- Husqvarna Group

- Subaru Industrial Power (Robin)

- Loncin Motor Co.

- STIHL Group

- Wacker Neuson SE

- Lifan Power

- Champion Power Equipment

- MTD Products (Stanley Black & Decker)

Frequently Asked Questions

The global small engine market was valued at US$ 7.1 Billion in 2025 and is projected to reach US$ 9.4 Billion by 2032, demonstrating consistent market expansion across residential, commercial, agricultural, and industrial application segments globally.

The small engine market is primarily driven by expanding agricultural mechanization and infrastructure development, stringent environmental regulations, and rising consumer demand for DIY landscaping, outdoor recreation equipment, and portable power solutions.

The small engine market is projected to grow at a CAGR of 4.1% between 2025 and 2032.

Key market opportunities include hybrid-electric engine technology development, emerging market expansion in Asia Pacific, and niche application segment development, offering differentiated growth vectors.

Key global market players include Briggs & Stratton Corporation, Honda Motor Co. Ltd., Kohler Co., Yamaha Motor Co. Ltd., and Kawasaki Heavy Industries, collectively commanding significant market share, supplemented by emerging regional competitors including Loncin Motor Co., Lifan Power, and Chinalight Machinery, and other players.