- Power Generation, Transmission, & Distribution

- Small Modular Reactor Market

Small Modular Reactor Market Size, Trends, Share, and Growth Forecast, 2025 - 2032

Small Modular Reactor Market by Reactor Technology (Pressurized Water Reactor (PWR), Pressurized Heavy Water Reactor (PHWR), Others (MSR, FNR, LWRG, HTR), and Regional Analysis for2025 - 2032

Small Modular Reactor Market Size and Trends Analysis

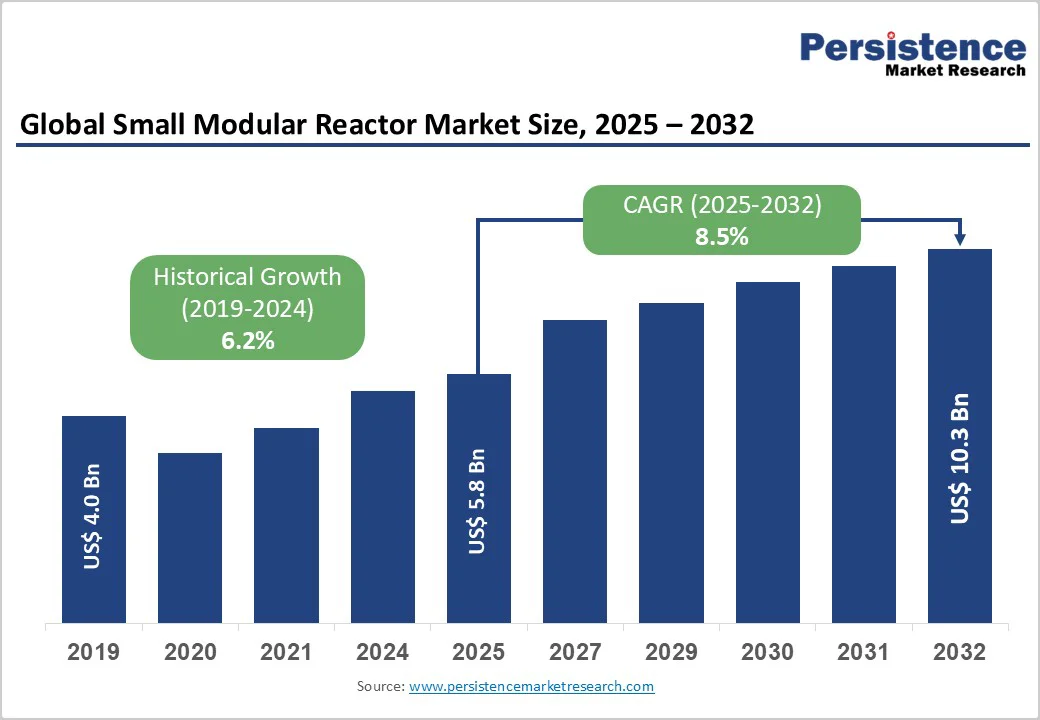

The global small modular reactor market size is likely to value US$ 5.8 billion in 2025 and is projected to reach US$ 10.3 billion, growing at a CAGR of 8.5% during the forecast period from 2025 to 2032.

The market expansion is fueled by global decarbonization mandates and corporate net-zero commitments, driving demand for dedicated nuclear baseload capacity. Rising energy needs from AI and data centers are accelerating multi-gigawatt nuclear power purchase agreements by major tech firms.

The modular factory-fabrication model supports standardized production, cutting construction timelines from decades to months while improving quality and consistency.

Key Industry Highlights:

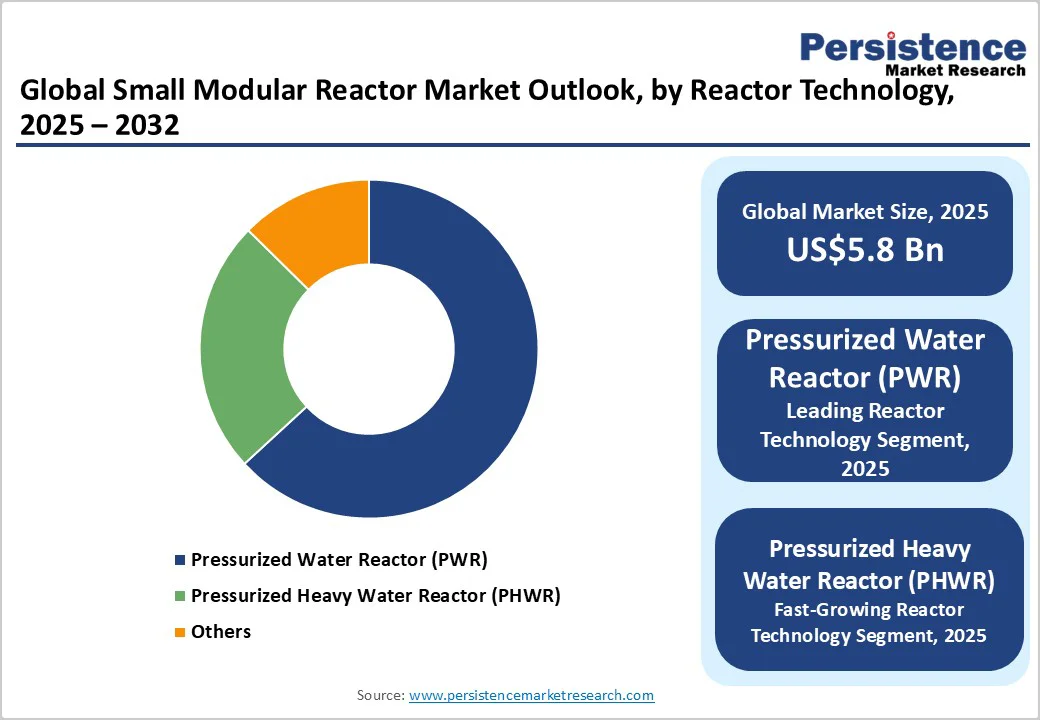

- Leading Reactor Technology: Pressurized water reactor (PWR) dominates with over 60% market share in 2025, led by NuScale’s 77 MWe, Westinghouse AP300 (330 MWe), and Rolls-Royce 470 MWe SMR designs. Proven safety records, regulatory alignment, and modular scalability make PWRs the preferred choice for utilities and industrial users seeking near-term deployment.

- Emerging Reactor Technology: Pressurized heavy water reactors (PHWRs) are gaining traction, with CAPEX projected to reach US$ 2.3 Bn by 2032. India’s 700 MWe PHWR units at Kakrapar 3 & 4 and Rajasthan 7 exemplify scalable, thorium-ready designs leveraging domestic uranium resources of ~4,33,800 tonnes across 47 deposits.

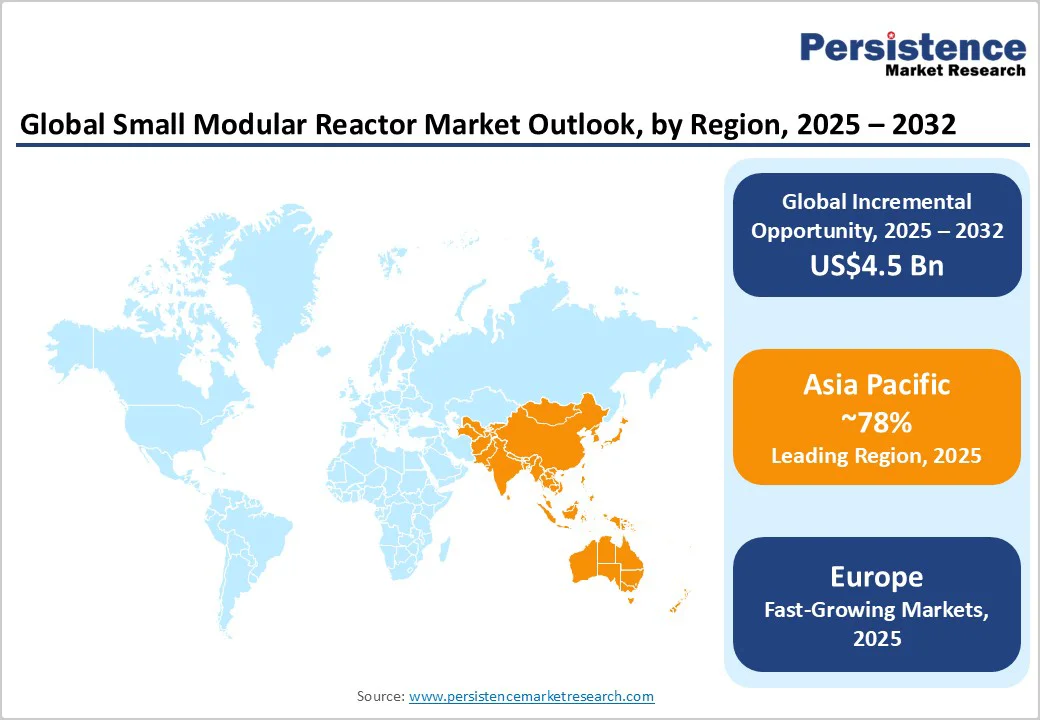

- Leading Region: Asia-Pacific dominates the global SMR market, accounting for over 78% share by 2025 with CAPEX exceeding US$ 4.6 Bn, fueled by government funding, state-owned project execution, and domestic manufacturing integration. China and India lead deployments under long-term nuclear energy missions targeting 100 GW capacity by 2047.

- Emerging Region: Europe exhibits robust momentum, projected to reach US$ 1.9 Bn CAPEX by 2032, supported by the European Commission’s €241 Bn (~US$ 277 Bn) nuclear investment roadmap and the European SMR Alliance promoting regulatory harmonization and cost optimization.

- Key Driver: The surge in AI workloads and data center power demand is reshaping energy strategies, creating a high-value opportunity for SMRs as clean, reliable baseload power. Data center electricity use is expected to reach 945 TWh annually by 2030, equivalent to Japan’s total consumption, while U.S. demand from hyperscale facilities could contribute nearly 50% of national electricity demand growth, accelerating SMR adoption for digital infrastructure.

| Key Insights | Details |

|---|---|

| Small Modular Reactor Market Size (2025E) | CAPEX US$5.8 Bn |

| Market Value Forecast (2032F) | CAPEX US$10.3 Bn |

| Projected Growth (CAGR 2025 to 2032) | 8.5% |

| Historical Market Growth (CAGR 2019 to 2024) | 6.2% |

Market Dynamics

Driver - Global Energy Transition and Climate Action Mandates Drive Nuclear Expansion

Global climate action and net-zero commitments are accelerating nuclear expansion, with the IEA projecting global nuclear capacity to rise from 413 GW in 2022 to 812 GW by 2050 under its “Net Zero by 2050” scenario. India, aiming for net-zero emissions by 2070, has allocated funds in its 2025 budget for SMR R&D and plans to commission at least five indigenously designed SMRs by 2033.

According to the NEA, nuclear deployment, including SMRs, could cumulatively avoid 87 Gt CO2 by 2050 and 5 Gt annually thereafter, comparable to U.S. emissions. SMRs’ modular, flexible, and low-carbon design supports energy security, while clean-energy incentives and corporate decarbonization goals further drive adoption.

Artificial Intelligence and Data Center Power Demand Reshape Energy Strategies

The exponential rise in AI workloads and hyperscale data center expansion is intensifying global power demand, creating a high-value opportunity for small modular reactors as low-carbon, reliable energy sources. According to the IEA, data center electricity use is projected to reach 945 TWh annually by 2030, equivalent to Japan’s current consumption, with U.S. data centers expected to contribute nearly 50% of national electricity demand growth.

This surge is driving major investments. Google’s partnership with Kairos Power targets 500 MW of SMR capacity by 2035, while Amazon’s US$ 500 million investment aims to develop 5 GW of SMR generation by 2039, positioning SMRs as a sustainable power backbone for AI infrastructure.

Regulatory Modernization and Policy Support Accelerate Market Entry

Regulatory modernization and policy support are accelerating SMR market entry through streamlined licensing and harmonized global standards.

The Nuclear Energy Innovation and Modernization Act (NEIMA) milestones aligned with the 12- and 18-month review periods mandated under Executive Order 14300 took effect on May 23, 2025, expediting NRC approvals, such as a 12-month schedule for the Edwin I. Hatch license renewal, 18 months for Dow’s Project Long Mott, and 17 months for TVA’s Clinch River SMR.

The ADVANCE Act of 2024 further enhances affordability by cutting the licensing staff-fee rate to US $148/hour, over 50% lower than the US $318/hour standard, effective October 1, 2025. Globally, harmonization initiatives such as the IAEA’s Nuclear Harmonization and Standardization Initiative and the SMR Regulators’ Forum are unifying safety assessment frameworks, reducing redundant reviews across jurisdictions.

Restraint - Extended Construction Timelines and Deployment Delays

Extended construction timelines and deployment delays significantly restrain the market growth by inflating capital costs, extending payback periods, and heightening financial risk. Projects like China’s Shidao Bay HTR-PM, which took around 9-11 years from construction start (2012) to commercial operation (2023), and Argentina’s CAREM-25, still under construction after 11 years since 2014, illustrate chronic schedule overruns.

Supply chain bottlenecks and limited HALEU fuel availability only ~900 kg produced by Centrus Energy in 2025, further hinder timely deployment. These factors erode investor confidence and weaken the overall economic viability of SMR projects.

Opportunity - Industrial Decarbonization and Process Heat Applications

Energy-intensive sectors such as steel, cement, and chemicals demand high-temperature heat that cannot be reliably met through electrification or renewables. SMRs provide a dependable, low-carbon source of both electricity and thermal energy, enabling industries to replace fossil-fuel boilers and meet strict emission targets.

India’s Nuclear Energy Mission for Viksit Bharat exemplifies this with indigenous SMRs such as the 200 MWe BSMR-200 for industrial captive power, 55 MWe off-grid units, and a 5 MWth HTGR for hydrogen production.

To enable private-sector participation, NPCIL is inviting industries to provide land and funding while retaining construction and operation of 220 MWe Bharat Small Reactor units, supporting large-scale, localized clean energy deployment for industrial decarbonization.

Grid Modernization and Renewable Energy Integration

Grid modernization and rapid renewable energy integration are creating significant opportunities. With U.S. solar capacity additions reaching nearly 50 GWdc in 2024, a 21% increase from 2023 and 66% of all new generation capacity is amplifying grid intermittency challenges.

SMRs’ load-following capability enables them to balance variable wind and solar output, providing 24/7 reliable and dispatchable power for critical users like data centres, where renewables and storage meet only ~80% of annual demand. Their modular, scalable, and hybrid designs also support phased grid expansion and cogeneration applications such as hydrogen production and district heating, making SMRs key enablers of a resilient, decarbonized energy ecosystem.

Category-wise Analysis

Reactor Technology Analysis

Pressurized water reactors (PWRs) are expected to account for over 60% of the small modular reactor (SMR) market in 2025, driven by their proven technology, high operational safety, and alignment with the growing need for reliable, low-carbon energy.

They require less space, offer scalable power output, and integrate seamlessly with existing nuclear infrastructure. The global push for energy security and decarbonization further boosts demand for reactors capable of providing stable baseload power, while PWRs meet regulatory standards more easily, reducing licensing and deployment timelines.

Leading PWR-based SMRs include NuScale Power’s 50 MWe design the first SMR to receive U.S. Nuclear Regulatory Commission (NRC) certification with its uprated 77 MWe module also approved in May 2025, Westinghouse’s AP300 delivering 330 MWe, leveraging the licensed and operating AP1000 technology for proven reliability; and Rolls-Royce SMR’s 470 MWe design, chosen as the UK’s preferred technology with £2.5 billion government backing.

The inherent scalability of PWR modular configurations allows customers to add units incrementally, with NuScale offering 4-, 6-, and 12-module plants ranging from 308 MW to 924 MW total capacity, supporting flexible deployment for remote, industrial, and distributed power applications.

Pressurized Heavy Water Reactor (PHWR) Analysis

Pressurized heavy water reactor (PHWR) technology is poised for rapid growth, with projected CAPEX reaching US$2.3 Bn by 2032. PHWRs use natural uranium, reducing fuel enrichment requirements and enhancing energy security. Their modular design allows incremental capacity addition, aligning with rising electricity demand without large upfront investments, while offering superior neutron economy suitable for hydrogen production and desalination applications.

India is prioritizing PHWR expansion to achieve low-carbon energy targets and reduce fossil fuel dependence. As of early 2025, India operates 24 reactors with a total capacity of 8.18 GW, including the newly operational 700 MWe units at Kakrapar (Units 3 & 4) and Rajasthan (Unit 7).

PHWRs’ heavy-water moderation supports better neutron economy and future thorium utilization under India’s three-stage nuclear program, leveraging domestic uranium resources estimated at 4,33,800 tonnes across 47 uranium deposits, according to AMD as of August 2025.

Regional Insights

North America Small Modular Reactor Market Trends

North America is expected to reach CAPEX US$ 0.5 Bn by 2032, driven by strong regulatory frameworks, advanced nuclear infrastructure, high R&D investment spending, and government initiatives positioning the region as a global innovation hub. In the U.S., there are approximately 5,426 operational data centers as of March 2025, which consumed about 17 GW of power in 2022, with projections suggesting grid-power demand could rise to over 130 GW by 2030.

This growing electricity demand from data-intensive facilities highlights a strong need for reliable, low-carbon, and scalable power, making SMRs an attractive solution. The U.S. Department of Energy (DOE) has reissued a US$900 million solicitation in March 2025 to support Generation III+ SMR deployment. The Canadian Nuclear Safety Commission (CNSC) offers a pre-licensing Vendor Design Review (VDR) process, facilitating early regulatory approval for SMR designs.

Asia Pacific Small Modular Reactor Market Trends

Asia-Pacific small modular reactor market is projected to dominate globally, accounting for over 78% of share by 2025, with CAPEX exceeding US$ 4.6 Bn. This growth is driven by strong government coordination, state-funded deployment programs, and domestic manufacturing integration.

India’s Union Budget 2025-26 launched a Nuclear Energy Mission with a 20,000 crore allocation to develop five indigenously designed SMRs by 2033, targeting 100 GW nuclear capacity by 2047 under the Viksit Bharat initiative. China leads the region, having commissioned the HTR-PM high-temperature gas-cooled SMR and advancing multiple projects through state-backed site selection and accelerated construction timelines.

Europe Small Modular Reactor Market Trends

Europe Small Modular Reactor market is gaining momentum, projected to reach a CAPEX of US$1.9 Bn by 2032, supported by favorable nuclear policies, energy security imperatives, and net-zero commitments. The European Commission estimates €241 billion (~US$277 billion) in nuclear investments by 2050 for both large reactors and SMRs.

The UK aims for 24 GW of nuclear capacity by 2050, while the Czech Republic’s EZ Group is partnering with Rolls-Royce SMR to deploy up to 3 GW in its first phase. The European SMR Alliance is further advancing regulatory harmonization, industrial cooperation, and cost reduction to accelerate SMR deployment across the region.

Competitive Landscape

The global small modular reactor market is highly consolidated, with a few key players dominating the development, manufacturing, and deployment of modular nuclear technologies.

Companies are leveraging strategic partnerships with utilities and governments, investing in advanced R&D to improve reactor safety and efficiency, and securing multi-region licensing and regulatory approvals to accelerate global market entry.

They also emphasizing modular scalability, cost reduction through standardized reactor designs, and localization of supply chains to enhance competitiveness and capitalize on emerging opportunities in the nuclear energy sector.

Key Industry Developments:

- In August 2025, X-energy, Amazon, KHNP, and Doosan Enerbility partnered to accelerate the deployment of X-energy’s Xe-100 advanced SMRs and TRISO-X fuel in the U.S., targeting growing power needs from data centers and AI. The collaboration spans reactor design, supply chain, construction, and investment, aiming to mobilize up to $50 billion in line with U.S.-South Korea trade initiatives.

- In July 2025, Emirates Nuclear Energy Company (ENEC) and Samsung C&T Corporation signed an MoU to explore global civil nuclear energy opportunities. The collaboration focuses on conventional nuclear projects, SMR deployment, nuclear-powered hydrogen, and investment in nuclear services, including potential projects in the UAE, US, South Korea, and Romania.

Companies Covered in Small Modular Reactor Market

- China National Nuclear Corporation

- BWX Technologies Inc.

- GE Hitachi Nuclear Energy

- Mitsubishi Heavy Industries, Ltd

- Bechtel Corporation

- Holtec International

- General Atomics

- Rolls-Royce plc

- Nuclear Power Corporation of India Limited

- NuScale Power, LLC

- Korea Electric Power Corporation

- Westinghouse Electric Company LLC

- Terrestrial Energy Inc.

- Moltex Energy

Frequently Asked Questions

The global small modular reactor market is projected to be valued at CAPEX US$5.8 Bn in 2025.

The global push for clean energy transition, increasing electricity demand, and enhanced energy security needs, is a key drivers of the market.

The small modular reactor market is poised to witness a CAGR of 8.5% from 2025 to 2032.

Rising demand for low-carbon energy, industrial decarbonization, grid modernization, and the need for scalable nuclear solutions in remote and off-grid regions are creating strong growth opportunities.

China National Nuclear Corporation, BWX Technologies Inc., GE Hitachi Nuclear Energy, Mitsubishi Heavy Industries, Ltd, NuScale Power, LLC, Rolls-Royce plc are among the leading key players.