- Hardware & Software IT Services

- Server Operating System Market

Server Operating System Market Size, Share, and Growth Forecast 2026 - 2033

Server Operating System Market by Operating System (Windows Linux, MacOS, and Others), Virtualization (Virtual Machine and Physical Machine), Deployment (On Premise and Cloud), and Regional Analysis

Server Operating System Market Size and Share Analysis

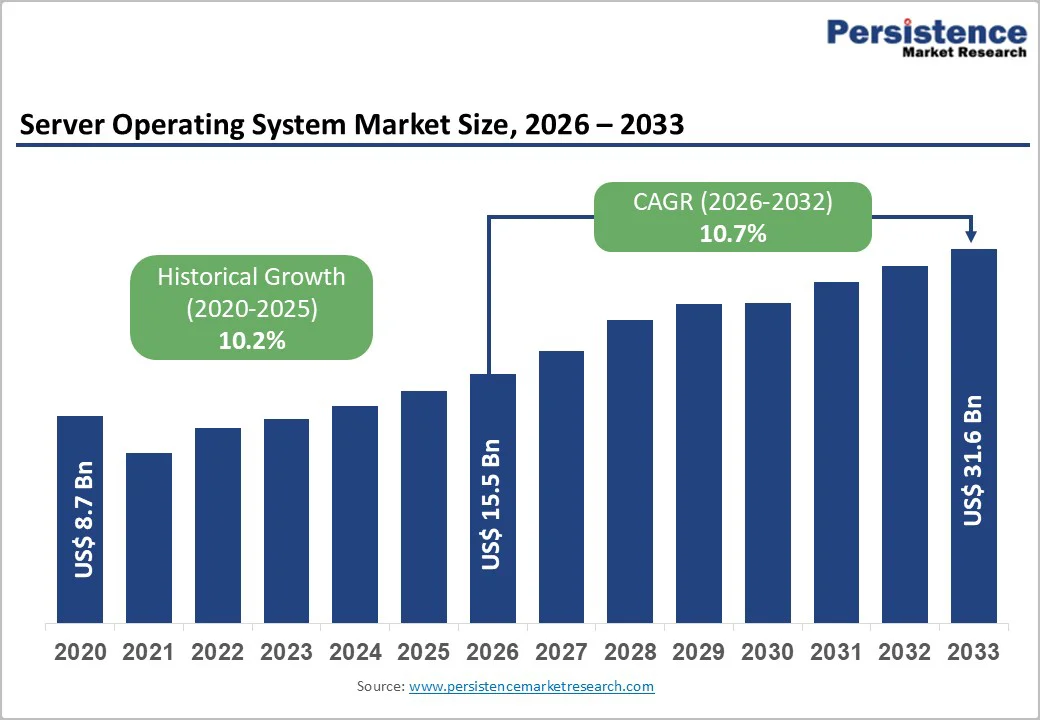

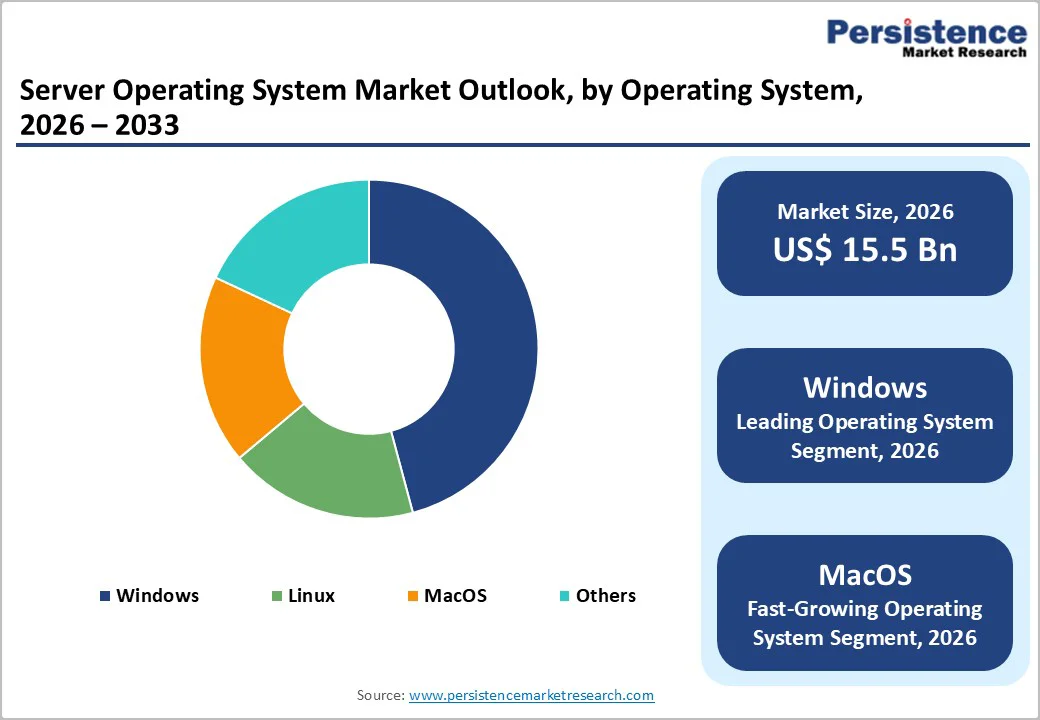

The global server operating system market size is likely to be valued at US$ 15.5 billion in 2026 and is projected to reach US$ 31.6 billion by 2033, growing at a CAGR of 10.7% between 2026 and 2033.

The market is propelled by the rapid adoption of cloud computing, virtualization, and the integration of advanced technologies, including AI, ML, and edge computing, which are transforming data center architectures and enterprise IT infrastructure. The shift toward hybrid and multi-cloud environments, together with intensifying cybersecurity demands and regulatory compliance imperatives, is further accelerating the server operating system market.

Key Industry Highlights:

- Leading Region: North America dominates the server operating system market, with nearly 38% share in 2026, supported by advanced IT infrastructure and high enterprise cloud migration.

- Fastest-Growing Region: Asia Pacific stands out as the fastest-growing region, driven by aggressive data center expansion and the

- rapid adoption of AI, cloud computing, and virtualization technologies.

- Dominant Operating System: Windows OS leads the operating system category, comprising over 58% market share globally, supported by strong enterprise adoption and hybrid cloud capabilities.

- Fastest Growing Virtualization: The Virtual Machines segment shows the most rapid growth in virtualization, accounting for more than 60% of server OS market revenue.

- Key Market Opportunity: Edge computing and AI integration offer substantial market opportunities with rising demand for lightweight, scalable server OS solutions in smart manufacturing, healthcare, and autonomous IoT applications.

| Key Insights | Details |

|---|---|

|

Server Operating System Market Size (2026E) |

US$ 15.5 Bn |

|

Market Value Forecast (2033F) |

US$ 31.6 Bn |

|

Projected Growth CAGR(2026-2033) |

8.1% |

|

Historical Market Growth (2020-2025) |

10.7% |

Market Dynamics

Market Drivers

The rapid growth of cloud computing and virtualization is driving demand for advanced server operating systems.

The rapid expansion of cloud computing and virtualization technologies has become a dominant force driving growth in the global server operating system market. Organizations worldwide are increasingly transitioning from traditional on-premises infrastructure to cloud-based environments, creating unprecedented demand for sophisticated server operating systems capable of managing complex virtualized workloads. As businesses adopt hybrid and multi-cloud deployment models, they require flexible, scalable, and secure operating systems that can seamlessly integrate across distributed data centers and cloud platforms.

Server operating systems must now provide advanced resource management, support containerization technologies such as Docker and Kubernetes, and facilitate microservices architectures that enable businesses to optimize their infrastructure utilization and reduce operational costs. The proliferation of cloud services has driven public-private partnerships to develop innovative server solutions to enable smooth data sharing and rapid digitization. As organizations continue to embrace digital transformation initiatives and seek competitive advantage through cloud infrastructure, the market for server operating systems is expected to grow, with cloud computing and virtualization serving as the primary catalysts for this expansion.

Advances in AI, analytics and cybersecurity are creating demand for more powerful and secure server operating systems.

Advances in artificial intelligence, analytics, and cybersecurity have become critical catalysts for driving demand for more powerful and secure server operating systems globally. The exponential growth of AI and machine learning workloads has fundamentally transformed infrastructure requirements, as organizations deploy sophisticated AI models for training, inference, and real-time data processing.

Server operating systems must now handle computationally intensive tasks that require advanced resource management, parallel processing, and optimization for specialized hardware accelerators such as GPUs and TPUs. Linux distributions such as Ubuntu and CentOS have emerged as preferred platforms for AI applications due to their native compatibility with leading frameworks like PyTorch, TensorFlow, and JAX. The integration of AI and machine learning capabilities directly into server operating systems enables automated task execution, intelligent resource allocation, and enhanced data processing efficiency.

The surge in big data and advanced analytics applications has created unprecedented demands for server operating systems capable of processing massive datasets and delivering real-time insights. Enterprises require operating systems that can optimize database management, virtualization, and complex analytical workflows while maintaining exceptional performance and uptime.

Market Restraints

High licensing costs and complex legacy integration constrain server OS adoption.

High licensing costs and complex legacy integration represent significant restraints limiting the adoption and expansion of the global server operating system market. Enterprise-grade server operating systems, particularly Windows Server, impose substantial financial burdens on organizations through expensive licensing fees and subscription models that create significant barriers for small and medium-sized businesses seeking to modernize their infrastructure. The core-based licensing model adopted since Windows Server 2016 ties costs directly to physical server cores, with organizations required to license all CPU cores across their infrastructure, often resulting in substantial capital expenditures that can discourage adoption of advanced operating systems.

Legacy system integration presents equally formidable obstacles, as organizations struggle to bridge the gap between outdated infrastructure and modern server operating systems. Approximately 70% of enterprise integration projects involving legacy systems exceed initial time and budget estimates, primarily due to incompatibilities between monolithic legacy architectures and contemporary microservices-based systems. Legacy systems frequently lack modern RESTful APIs and rely on proprietary communication protocols, requiring costly custom development and middleware solutions to facilitate integration with modern server environments.

Market Opportunities

Expanding hybrid and multi-cloud deployments create opportunities for integrated server OS solutions

Expanding hybrid and multi-cloud deployments present substantial market opportunities for integrated server operating system solutions designed to orchestrate workloads across diverse infrastructure environments seamlessly. With 87% of enterprises adopting hybrid and multi-cloud strategies in 2025, organizations increasingly demand server operating systems that enable unified resource management, workload portability, and vendor-agnostic deployments. Modern server OS solutions that support seamless integration across on-premises infrastructure and multiple public cloud platforms, such as AWS, Azure, and Google Cloud, enable organizations to avoid vendor lock-in while optimizing cost efficiency and operational flexibility.

Unified management platforms that incorporate AI-driven optimization are emerging as critical infrastructure components, enabling IT teams to monitor, automate, and balance workloads across heterogeneous environments from a single control point. As enterprises accelerate digital transformation and adopt cloud-first strategies, approximately 95% of new digital workloads will deploy on cloud-native platforms, creating significant demand for server operating systems that support containerization, Kubernetes compatibility, and cross-platform interoperability. Companies investing in open-source server operating systems and solutions that prioritize multi-cloud compatibility are positioned to capture substantial market share as organizations seek flexible, cost-effective infrastructure solutions that support their evolving hybrid deployment strategies.

Expansion of edge computing and IoT ecosystems creates demand for specialized server OS solutions.

The expansion of mobile edge computing and Internet of Things (IoT) ecosystems represents a significant growth opportunity for specialized server operating system solutions designed for distributed, resource-constrained environments. These expanding deployments require lightweight, optimized server operating systems capable of processing data closer to the source while maintaining performance and security standards. Embedded Linux distributions, including Yocto Project, Buildroot, and OpenWRT, have emerged as preferred platforms for edge devices, offering minimal footprints, real-time processing capabilities, and flexibility for customization without vendor lock-in concerns.

Modern specialized server OS solutions for edge environments must support containerization technologies such as Docker and Kubernetes, enabling rapid deployment of AI and machine learning inference workloads across distributed hardware platforms. Industries including manufacturing, telecommunications, healthcare, and smart cities increasingly rely on edge-native server operating systems to reduce latency, enhance data security through local processing, and optimize bandwidth utilization. As enterprises prioritize decentralized computing architectures and 5G network expansion accelerates globally, specialized server operating system vendors positioned to deliver edge-optimized, secure solutions with simplified management capabilities are positioned to capture substantial market opportunities.

Category-wise Analysis

Operating System Insights

Windows remains the clear leader in the server operating system market, commanding an estimated 58% global market share in 2024-2025. Its dominance is rooted in deep enterprise adoption, integration with Active Directory, and compatibility with popular stacks like .NET. Windows Server’s hybrid cloud capabilities and strong management frameworks are preferred for identity services, ERP, and legacy systems, sustaining its market leadership.

Linux is experiencing rapid market expansion and is expected to capture a significant market share during the forecast period. Linux's open-source architecture, combined with significantly lower total cost of ownership and superior performance efficiency, handling 3x more web requests per GB of RAM than Windows Server on identical hardware, positions it as the preferred platform for cloud infrastructure, containerization, and DevOps environments

Virtualization Insights

The Virtual Machine (VM) segment accounts for approximately 60% of server operating system market revenue, reflecting enterprises' strong preference for flexible resource management and optimized hardware utilization. VM-based environments have become foundational for modern enterprise infrastructure, enabling organizations to abstract physical hardware resources into multiple independent virtual instances that can run different operating systems and applications simultaneously. This approach delivers significant cost reductions by consolidating multiple workloads onto fewer physical servers, lowering capital expenditures and energy consumption, while simultaneously improving resource utilization efficiency through dynamic allocation that scales capacity to match actual demand.

Deployment Insights

The on-premise segment dominated the global server operating system market in 2026, capturing approximately 60.5% market share, reflecting enterprises' ongoing reliance on traditional infrastructure deployments. On-premises server operating systems provide organizations with full control over their data, applications, and infrastructure, delivering enhanced security for sensitive workloads and compliance with stringent regulatory requirements, particularly in highly regulated sectors such as banking, healthcare, and government. This deployment model offers reduced operational costs for organizations already invested in physical data center infrastructure and eliminates concerns about data sovereignty by maintaining complete visibility and governance over infrastructure resources.

Regional Insights

North America Server Operating System Market Trends

North America remains the global leader, representing approximately 38% of market share, driven by robust IT infrastructure, rapid cloud adoption, and enterprise digital transformation. The United States generates more than 80% of the region’s revenue, benefiting from mature data center ecosystems, regulatory leadership in cybersecurity, and innovation in AI-enabled server management. Federal security initiatives and compliance standards prompt continuous OS upgrades, ensuring resilience and regulatory alignment.

Europe Server Operating System Market Trends

Europe is the second-largest regional market for server operating systems, accounting for approximately 30% of the global market share. The European server operating system market is characterized by strong regulatory drivers and energy efficiency mandates that shape purchasing and deployment decisions across the continent. The European Union's Energy Efficiency Directive has compelled data center operators managing infrastructure with IT load above 100 kilowatts to publish energy key performance indicators (KPIs) by September 2024, directly influencing server operating system adoption decisions toward more efficient platforms.

Asia Pacific Server Operating System Market Trends

Asia Pacific is the fastest-growing regional market, with a 10.9% CAGR, projected to achieve the highest compound annual growth rate during the forecast period. This accelerated growth is driven by explosive data center proliferation, with China and India commanding the highest numbers of colocation data centers globally, 87 and 160 facilities, respectively, directly correlating to substantial server operating system demand. Rapid digital technology penetration across countries, including China, Japan, and India, is creating unprecedented market opportunities for server operating system vendors, as organizations modernize legacy infrastructure and adopt cloud-first computing strategies.

Competitive Landscape

The server operating system market is moderately concentrated, with Microsoft Corporation, IBM (Red Hat), and SUSE Group holding a combined commercial revenue share exceeding 55%. Leading enterprises prioritize expansion in cloud-native, edge, and AI workloads; integrate advanced security; and pursue differentiated business models via open-source innovation, vertical-specific solutions, and sustainability initiatives. The competitive landscape mixes established giants and agile emerging vendors, creating dynamic specialization around AI, edge, and hybrid infrastructure.

Competition is further shaped by a mix of established technology giants and high-growth emerging vendors, each carving out differentiation through open-source innovation, specialized distributions, and industry-specific OS variants tailored for telecommunications, financial services, industrial automation, and hyperscale data centers. Vendors are also focusing on sustainability-driven features, including energy-aware schedulers, resource-efficient kernels, and support for liquid-cooled or high-density server deployments.

Key Market Developments:

- In February 2025, it introduced its ProLiant Gen12 server portfolio featuring embedded AI-driven automation designed to optimize workload deployment, system tuning, and predictive maintenance without manual intervention.

- In April 2025, SUSE strengthened its position in telecom and enterprise AI by releasing SUSE Edge for Telco 3.2, a platform tailored for highly distributed, carrier-grade edge infrastructure. The update enables operators to manage thousands of edge nodes with improved orchestration, lifecycle automation, and real-time reliability.

- In May 2025, Dell expanded its AI and data-center hardware portfolio with the launch of the AI Factory, an integrated platform combining Dell infrastructure, Nvidia AI solutions, and pre-validated software stacks to accelerate enterprise AI adoption.

Companies Covered in Server Operating System Market

- Microsoft Corporation

- IBM Corporation

- Google LLC

- Amazon Web Services, Inc.

- Fujitsu Ltd.

- NEC Corporation

- Apple Inc.

- Hewlett Packard Enterprise

- Dell Technologies Inc.

- Canonical Ltd.

- Oracle Corporation

- SUSE Group

- Lenovo Group

- Cisco System

- VMware Inc.

Frequently Asked Questions

The Global Server Operating System Market is valued at US$ 15.5 Bn in 2026 and is projected to reach US 31.6 Bn by 2033, growing at a CAGR of 10.7% from 2026 to 2033.

Primary factors dricing demand are rapid expansion of cloud computing, AI workloads, and edge deployments, which require scalable, secure, and high-performance infrastructure along with the rising enterprise digitalization and the need for advanced automation and zero-trust security are accelerating adoption across industries.

Windows dominates the global server operating system market with an estimated 58% market share in 2026, driven by deep enterprise adoption, seamless Active Directory integration, and strong compatibility with Microsoft ecosystem technologies.

North America leads the global server operating system market, representing approximately 38% of total market share in 2025.

The expansion of edge computing and IoT ecosystems represents the most significant emerging market opportunity, creating demand for lightweight, specialized server OS solutions optimized for distributed, low-latency environments.