- Communication Infrastructure & Services

- Serverless Computing Market

Serverless Computing Market Size, Share, and Growth Forecast, 2026 - 2033

Serverless Computing Market by Service Type (Serverless Compute, Serverless Storage, Serverless Database, Application Integration & Orchestration, Monitoring, Observability & Governance, Misc.), Service Model (Function-as-a-Service (FaaS), Backend-as-a-Service (BaaS)), Deployment Mode (Public Cloud, Private Cloud, Hybrid Coud), Organization Size (Large Enterprises, Small & Medium Enterprises (SMEs)) End-user and Regional Analysis for 2026 - 2033

Serverless Computing Market Size and Trends Analysis

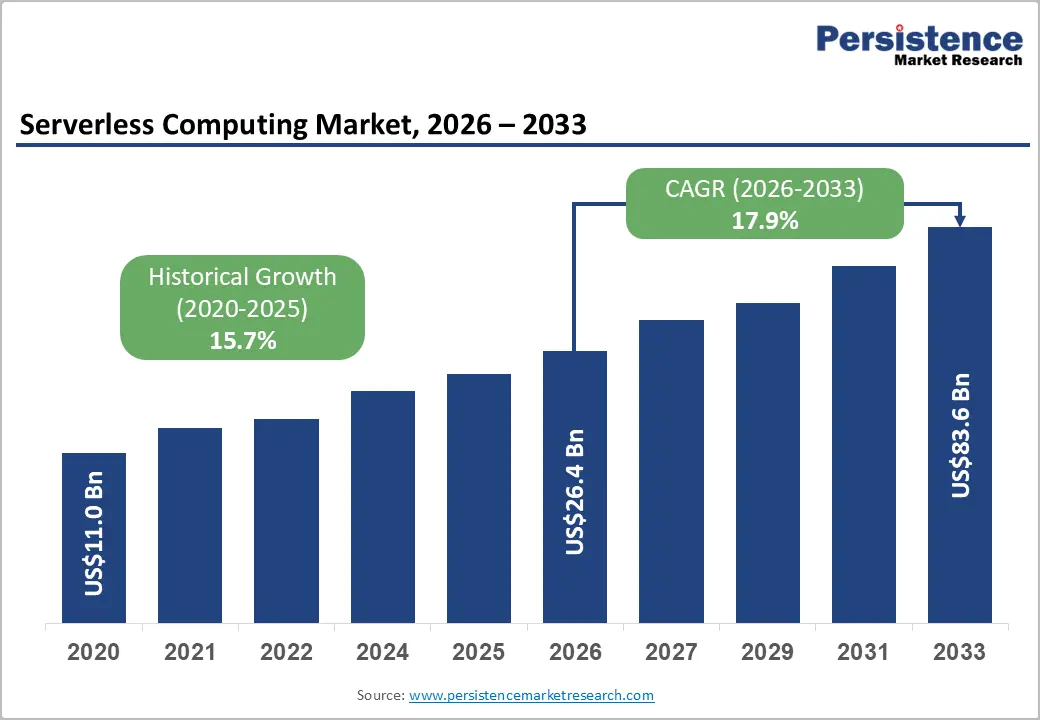

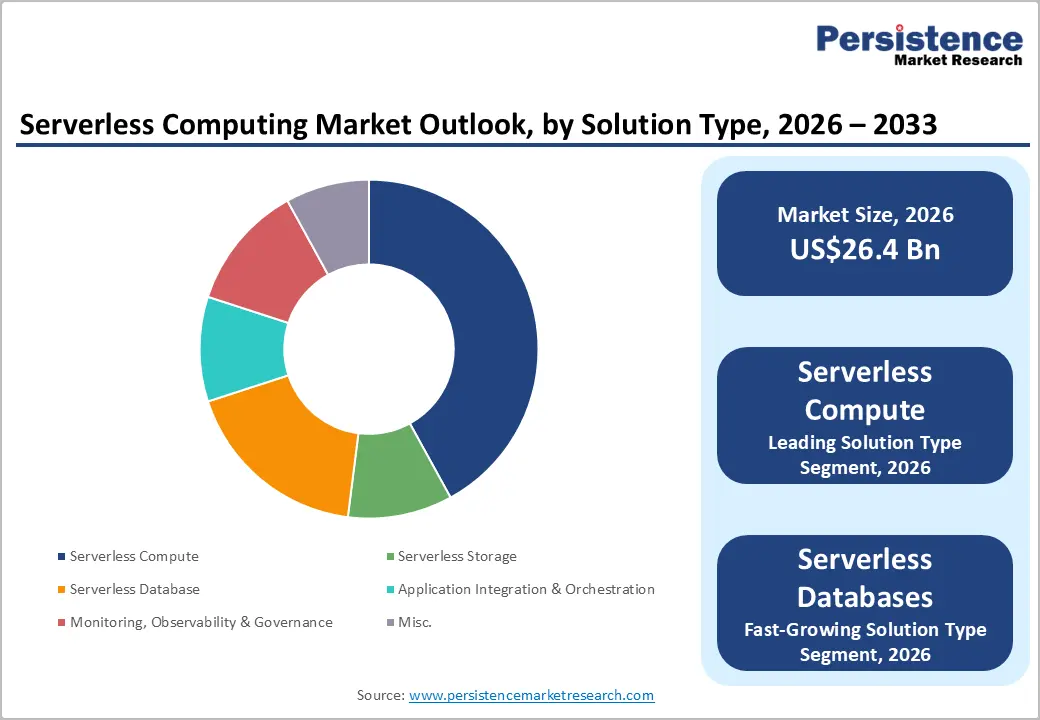

The global serverless computing market size is likely to be valued at US$ 26.4 billion in 2026 and is projected to reach US$ 83.6 billion by 2033, expanding at a CAGR of 17.9% between 2026 and 2033.

This expansion reflects enterprises' transition to cloud-native architectures, eliminating infrastructure management complexity while supporting event-driven, microservices-based applications. Digital transformation initiatives across IT, telecommunications, financial services, retail, healthcare, and government sectors are driving demand for serverless platforms that deliver automatic scaling, consumption-based cost models, and rapid application deployment. The convergence of AI workload integration, multi-cloud adoption requirements, edge computing proliferation, and analytics modernisation has established serverless computing as essential infrastructure, enabling organisational innovation acceleration and operational cost optimisation.

Key Industry Highlights:

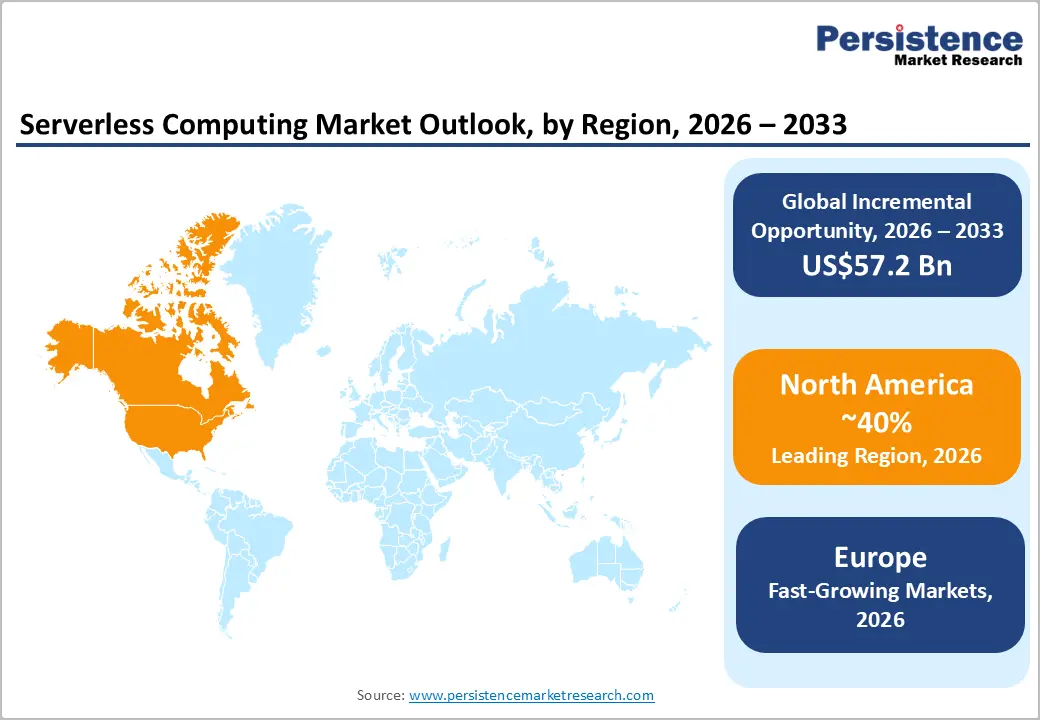

- Regional Leadership: North America dominates the global serverless computing market with ~40% share, supported by hyperscaler leadership, mature cloud-native adoption, and strong enterprise demand across AI, BFSI, and SaaS applications.

- Strong European Presence: Europe accounts for ~25% of market share, driven by the digital transformation of the BFSI sector, GDPR-aligned cloud modernization, and the growing adoption of event-driven architectures across enterprises.

- High-Growth East Asia: East Asia holds ~18% share, led by China and Japan, fueled by large-scale cloud infrastructure expansion, digital banking growth, and rapid adoption of serverless AI and data platforms.

- Leading Solution: Serverless Compute leads with ~42% share, reflecting widespread adoption of Function-as-a-Service for scalable, event-driven microservices and application modernization.

- Fastest-Growing Solutions: Serverless Databases and analytics services are expanding rapidly as enterprises prioritize fully managed, auto-scaling data platforms for AI, real-time processing, and transactional workloads.

| Key Insights | Details |

|---|---|

|

Serverless Computing Market Size (2026E) |

US$ 26.4 Bn |

|

Market Value Forecast (2033F) |

US$ 83.6 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

17.9% |

|

Historical Market Growth (CAGR 2020 to 2025) |

15.7% |

Market Dynamics

Drivers - Microservices Architecture Adoption and Event-Driven Development Models

Enterprises are systematically restructuring application architectures away from monolithic designs toward distributed, event-driven microservices patterns, enabling independent component scaling and rapid feature deployment. The Serverless Computing Market reflects accelerating organisational adoption of cloud-native development methodologies leveraging containerization, Kubernetes orchestration, and serverless function execution, enabling modular, rapidly deployable application components. 89% of organisations have adopted cloud-native technologies to some extent, reflecting a broader strategic shift toward microservices and event-driven architectures supporting faster feature deployment and independent component scaling.

Modern Infrastructure-as-Code tools (Terraform, Pulumi, AWS CDK) and observability platforms provide comprehensive support for serverless deployments across hybrid and multi-cloud environments, enabling organisations to implement sophisticated distributed architecture without requiring deep infrastructure engineering expertise.

The architectural shift toward microservices establishes fundamental market demand for serverless platforms capable of orchestrating thousands of independent functions responding to discrete business events, thereby establishing the Serverless Computing Market as an essential enabler of contemporary application development paradigms that support competitive differentiation through rapid innovation cycles.

AI and Data Analytics Workload Acceleration

Organisations are aggressively integrating artificial intelligence and machine learning capabilities into operational applications and customer experiences, creating computationally intensive workloads that demand flexible, scalable infrastructure allocation without the capital expenditure burden.

The serverless computing market has witnessed accelerating demand, driven by GenAI-specific cloud services growing by more than 160% in Q2 2025, establishing serverless platforms as a natural infrastructure fit for AI inference, model training pipelines, batch processing, and generative AI application deployment. Strategic vendor developments demonstrate this trajectory. IBM announced Serverless fleets with GPU support, enabling large-scale AI training on pay-as-you-go models. Microsoft enabled Azure Container Apps Serverless GPUs for GPU-accelerated workloads, Oracle launched Exadata Database serverless architecture supporting agentic AI, and Alibaba Cloud enables 50% reduction in AI model inference costs.

Modern serverless platforms increasingly incorporate GPU-accelerated resources, enabling organisations to run machine learning tasks and perform real-time AI inference without maintaining dedicated GPU clusters or managing complex hardware infrastructure. Financial institutions deploy serverless AI for fraud detection, healthcare organisations leverage serverless for diagnostic support, retail enterprises implement serverless for personalised recommendations, and manufacturing organizations utilize serverless for predictive analytics. The convergence of AI-driven application requirements, serverless infrastructure readiness, enterprise demand for rapid AI adoption, and elimination of GPU infrastructure management complexity establishes Serverless Computing Market as critical infrastructure enabling enterprise-scale AI application deployment.

Restraint - Cold-Start Latency and Performance Constraints

Serverless function initialization introduces inherent latency overhead during container provisioning and startup, which constrains adoption for latency-sensitive applications that require sub-second response times or deterministic performance characteristics. Organizations deploying real-time trading systems, autonomous vehicle applications, ultra-low-latency gaming, or industrial automation systems report unacceptable cold-start performance, creating barriers to serverless adoption in performance-critical use cases.

While vendors introduce optimization mechanisms including function warm-up strategies and provisioned capacity models, these solutions increase operational complexity and diminish serverless's original cost advantages, creating implementation tradeoffs that constrain market expansion in latency-sensitive application categories and limit the addressable market within performance-critical sectors.

Opportunity - BFSI Infrastructure Modernization and Real-Time Payment Evolution

Banking, financial services, and insurance institutions across developed and emerging markets face urgent infrastructure modernization imperatives driven by fintech competition, modernization of regulatory frameworks, expansion of real-time payment infrastructure, and acceleration of digital financial inclusion. The Serverless Computing Market presents substantial opportunities within financial services modernisation initiatives, particularly across regions transitioning to real-time payment infrastructure, modernising legacy systems, and supporting emerging payment models and financial inclusion objectives.

India's BFSI sector demonstrates exceptional modernization requirements, expanding to US$1 trillion market capitalization in 2025 (contributing 27% to national GDP), with gross NPAs declining from 5.8% (FY22) to 2.2% (FY25), life insurance AUM reaching US$693 billion, and mutual fund AUM reaching US$844 billion, establishing well-capitalized financial institutions as sophisticated technology adopters requiring scalable infrastructure. European banking institutions hold €43.6 trillion in total assets, €26.8 trillion in outstanding loans, and €17.3 trillion in deposits (2023), with digital transformation accelerating through credit institution consolidation and branch reduction driven by efficiency-focused restructuring.

China's banking sector reached RMB 467.3 trillion in assets (+7.9% year-on-year) with inclusive loans to micro and small enterprises expanding 12.3% to RMB 36 trillion, while insurance assets grew 9.2% to RMB 39.2 trillion, establishing substantial financial inclusion expansion requirements.

Latin America's banking sector continues modernisation with over 50% of adults unbanked, driving organisations to implement API-first architectures and cloud infrastructure to support real-time payment platforms like Brazil's PIX. Financial institutions require serverless computing platforms capable of supporting high-frequency transaction processing, real-time settlement operations, fraud detection analytics, regulatory compliance automation, and integrated security. The convergence of regulatory modernization mandates, fintech competitive pressure, real-time payment adoption, and financial inclusion expansion establishes Banking and Financial Services as a substantial opportunity within the Serverless Computing Market.

Retail and E-Commerce Omnichannel Infrastructure Modernization

Retail and e-commerce organisations are modernising their application infrastructure to support omnichannel customer experiences, real-time inventory synchronisation, dynamic pricing optimisation, personalised recommendation delivery, and seamless integration with emerging digital channels, all of which depend on sophisticated event-driven architectures and data processing capabilities. The Serverless Computing Market presents critical opportunities within retail modernisation initiatives as organisations transition from traditional monolithic e-commerce platforms toward composable, microservices-based architectures, enabling rapid feature deployment and seamless channel integration.

U.S. e-commerce markets demonstrate sustained momentum, with seasonally adjusted e-commerce sales reaching US$310.3 billion in Q3 2025 (5.1% year-on-year growth), representing 16.4% of total retail sales, establishing substantial infrastructure modernisation requirements. EU e-commerce shows 23.8% of enterprises conducting e-sales (up from 17.2% in 2013), with e-commerce representing 19.1% of total business turnover, and web-based sales dominating with 17.7% of enterprises using websites/apps exclusively compared to 3.1% relying on EDI systems.

Large enterprises lead adoption with 46.5% engaging in e-sales and generating 24.4% of turnover digitally, while consumer-facing sectors such as accommodation rely almost entirely on web platforms.

Retail organisations leverage serverless platforms for order processing pipelines, payment gateway integration, inventory management, personalised recommendation engines, customer data analytics, and promotional campaign execution. The convergence of e-commerce acceleration, omnichannel integration imperatives, organisational demand for cost-optimised scalable infrastructure, and the requirement to handle unpredictable seasonal traffic variations establishes Retail and E-Commerce as the fastest-expanding opportunity segment within the Serverless Computing Market.

Category-wise Analysis

Solution Type Insights

Serverless Compute represents the dominant segment within the serverless computing market, commanding 42% market share in 2026 and encompassing Function-as-a-Service (FaaS) platforms that enable developers to deploy individual functions that respond to discrete business events without the infrastructure provisioning complexity. Serverless Compute platforms, including AWS Lambda, Microsoft Azure Functions, and Google Cloud Functions, provide abstraction layers isolating application logic from underlying infrastructure, enabling developers to focus on business logic implementation rather than infrastructure management.

Organizations prioritize Serverless Compute for event-driven workflows, including API request handling, asynchronous processing, real-time data transformation, scheduled batch processing, and trigger-based application orchestration, where functional decomposition aligns with business event patterns. AWS achieved AWS Service Delivery designation for AWS Lambda, validating partner expertise in delivering serverless compute solutions and reinforcing Lambda's role as a core infrastructure service.

The established ecosystem surrounding Serverless Compute platforms, including extensive cloud-provider service integrations, comprehensive developer tooling, and proven deployment methodologies, positions this segment as foundational within contemporary application architectures and as the primary revenue contributor in the serverless computing market.

Serverless Database services represent the fastest-expanding segment within the Serverless Computing Market, driven by organisational demand for fully managed data storage, querying, and analytics capabilities that eliminate infrastructure administration complexity while providing automatic scaling and consumption-based cost models. Tencent Cloud's DLC lakehouse engine was recognized as a representative vendor in Gartner's Market Guide for Data Lakehouse Platforms, enabling auto-scaling and integrated Data+AI workloads. Serverless Database platforms, including Amazon DynamoDB, Azure Cosmos DB, and Google Cloud Firestore, enable organizations to implement sophisticated database architecture without dedicated database administration or infrastructure maintenance responsibilities.

Industry Insights

The IT and telecommunications sectors maintain the largest market share in the Serverless Computing Market at 28% in 2026, reflecting the industry's fundamental reliance on sophisticated application infrastructure supporting network operations, customer-facing digital services, and emerging telecommunications technologies. Global internet adoption is expanding rapidly, reaching approximately 6 billion users by 2025 (74% of the world population, up from 60% in 2020), with 1.3 billion people gaining internet access in the past five years.

India's telecom sector has emerged as a dynamic economic pillar, positioning India as the world's second-largest telecommunications market in 2025 with 1.21 billion subscribers and 86.09% tele-density, while internet adoption reached 979 million users by June 2025. India's telecom gross revenue increased from US$39.22 billion (FY24) to US$43.42 billion (FY25), with wireless services accounting for over 96% of subscriptions and data consumption rising 17.46% year-on-year, with broadband penetration expanding from 149.75 million (2016) to 979 million (2025). The EU information and communication services sector encompasses 1.4 million enterprises employing 7.2 million people, generating €667 billion in value added with apparent labour productivity of €92,800 per person, establishing the region as a globally significant IT and telecommunications hub.

The Retail and E-Commerce sectors represent the fastest-expanding industry segment within the Serverless Computing Market, driven by accelerating digital commerce adoption, omnichannel customer experience requirements, and organisational demand for cost-optimised, scalable infrastructure to support seasonal traffic variations and promotional events.

U.S. e-commerce markets demonstrate sustained expansion momentum, with seasonally adjusted e-commerce sales reaching US$310.3 billion in Q3 2025, up 5.1% year-on-year and accounting for 16.4% of total retail sales, underscoring substantial infrastructure modernization requirements. EU e-commerce shows 23.8% of enterprises conducting e-sales (up from 17.2% in 2013), with e-commerce representing 19.1% of total business turnover, and web-based sales dominating with 17.7% of enterprises using websites/apps compared to 3.1% relying on EDI systems.

Regional Insights and Trends

North America Serverless Computing Market Trends

North America represents the largest geographic market for serverless computing, commanding 40% of global market share and establishing the region as the epicentre of serverless innovation, vendor competition, and enterprise adoption. The United States maintains the highest concentration of globally dominant serverless vendors (AWS, Microsoft Azure, Google Cloud), technology-intensive enterprises, cloud infrastructure providers, and advanced IT talent, driving substantial market demand for sophisticated serverless platforms.

North America benefits from a dense concentration of hyperscale cloud providers, including AWS, Microsoft Azure, and Google Cloud, collectively controlling 60%-65% of the rapidly expanding cloud infrastructure market. These vendors have invested substantially in serverless platform capabilities. AWS introduced Lambda optimisation features, Microsoft enabled Azure Container Apps, Serverless GPUs and achieved Forrester Wave Leader recognition in serverless development platforms, and Google Cloud advanced Kubernetes integration with serverless containers.

Large enterprises in North America, spanning Fortune 500 organizations, venture-funded startups, and technology service providers, have aggressively adopted serverless architectures to reduce infrastructure costs, accelerate deployment cycles, and support emerging AI-driven application requirements. The region's technology-intensive sectors, including financial services, software, digital media, and cloud infrastructure, demonstrate particularly high serverless adoption rates, establishing North America as the mature, highest-revenue market.

East Asia Serverless Computing Market Trends

East Asia represents a rapidly expanding geographic market for serverless computing, commanding 18% of global market share and demonstrating the strongest structural growth dynamics driven by accelerating cloud adoption, digital-first enterprise transformation, and emerging technology leadership positioning. China, India, and Southeast Asian markets are experiencing cloud adoption rates and digital infrastructure modernisation trajectories, establishing substantial serverless market opportunities.

China's banking and insurance sectors demonstrated robust expansion, with total banking assets reaching RMB 467.3 trillion in Q2 2025 (up 7.9% year-on-year), insurance assets expanding 9.2% to RMB 39.2 trillion, and inclusive loans to micro and small enterprises rising 12.3% to RMB 36 trillion. Alibaba Cloud was recognized as a Leader in The Forrester Wave™: Serverless Development Platforms (August 6, 2025) for its Function Compute and Serverless App Engine offerings, achieving top scores across deployment, workload flexibility, observability, and AI application development. Alibaba Cloud launched serverless PAI-Elastic Algorithm Service, reducing AI model inference costs by 50% while supporting LLM and generative AI applications.

Tencent Cloud launched EdgeOne Pages, an edge-native, full-stack serverless development platform featuring global edge distribution across 3,200+ nodes with integrated security, analytics, and AI capabilities. Tencent Cloud's DLC lakehouse engine was recognized as a representative vendor in Gartner's Market Guide for Data Lakehouse Platforms, enabling auto-scaling and integrated Data+AI workloads. India's technology sector continues rapid expansion, with cumulative FDI inflows reaching US$40.07 billion through March 2025 and sustained investment in 5G infrastructure, fiber deployment, and cloud services. The region records serverless adoption rates exceeding 20% annually, positioning East Asia as the fastest-growing geographic market globally.

Europe Serverless Computing Market Trends

Europe commands 22% of the global Serverless Computing Market share, making it the second-largest market after North America, while demonstrating distinct regulatory dynamics and vertical industry characteristics. European financial and insurance activities sector generated €0.9 trillion in value added in 2022, employing nearly 5 million people across almost 867,000 enterprises with wage-adjusted labor productivity of 236.1%. European banking institutions held €43.6 trillion in total assets and €26.8 trillion in outstanding loans in 2023, while total deposits from businesses and households rose 1.2% to €17.3 trillion, with the sector undergoing structural transformation driven by digitalisation.

EU e-commerce adoption demonstrates steady progress, with 23.8% of enterprises conducting e-sales and e-commerce representing 19.1% of total business turnover, with web-based sales dominating across all countries. The convergence of GDPR and emerging data protection regulations, enterprise digital transformation initiatives, financial services innovation requirements, and consumer-centric e-commerce expansion establishes Europe as a sustained, high-value region.

Competitive Landscape

The global serverless computing market is consolidated, with a handful of major cloud providers dominating the landscape due to their extensive infrastructure, advanced AI integrations, and broad enterprise adoption. Amazon Web Services (AWS) leads the market with its Lambda platform, offering mature, scalable, and event-driven serverless solutions that cater to diverse workloads across startups and large enterprises. Microsoft follows closely with Azure Functions, leveraging its hybrid cloud capabilities and strong enterprise client base to accelerate serverless adoption in critical business operations.

Google Inc. competes aggressively with Cloud Functions and Cloud Run, emphasizing integration with AI/ML services, data analytics, and containerized workloads, appealing to developers seeking seamless cloud-native experiences. IBM Corporation is positioning itself through Cloud Code Engine and Serverless Fleets, targeting high-performance computing and AI workloads with GPU-backed serverless architectures. Oracle extends serverless capabilities via Oracle Autonomous Database Serverless and Exadata Cloud, focusing on mission-critical, enterprise-grade applications with automated scaling and global deployment.

Key Industry Developments

- November 4, 2025 – IBM: IBM expanded its Cloud Code Engine with Serverless Fleets supporting GPU workloads, enabling enterprises to run large-scale AI training, simulations, and high-performance computing on a pay-as-you-go serverless model. This development broadens the applicability of serverless platforms beyond traditional web and event-driven workloads, reducing infrastructure complexity, improving cost visibility, and strengthening IBM’s position in enterprise AI and HPC.

- December 22, 2025 – Tencent Cloud: Tencent Cloud officially launched EdgeOne Pages, an edge-native, full-stack serverless development platform that allows developers to build and deploy web applications globally in minutes without managing servers. Featuring global edge distribution across 3,200+ nodes, integrated security, analytics, and AI capabilities, this development accelerates serverless adoption by reducing operational overhead and enabling rapid, scalable deployment for enterprises and independent developers.

Companies Covered in Serverless Computing Market

- Amazon Web Services (AWS)

- Microsoft

- IBM Corporation

- Google Inc.

- Oracle

- Alibaba Cloud

- Tencent Cloud

- Twilio

- Cludflare

- Mongo DB

- SAP SE

Frequently Asked Questions

The Global Serverless Computing Market is projected to be valued at US$ 26.4 Bn in 2026.

The IT & Telecommunications segment is expected to account for approximately 28.0% of the Global Serverless Computing Market by Use Industry in 2026.

The serverless computing market is expected to witness a CAGR of 17.9% from 2026 to 2033.

The Serverless Computing Market is driven by widespread enterprise adoption of microservices and event-driven architectures alongside the rapid acceleration of AI and data-intensive workloads, supported by hyperscaler innovations such as GPU-enabled serverless platforms that enable scalable, pay-as-you-go execution without infrastructure management.

The Serverless Computing Market offers key opportunities through BFSI infrastructure modernization for real-time payments and financial inclusion and retail & e-commerce omnichannel platform transformation, where scalable, event-driven serverless architectures enable high-frequency transactions, personalized digital experiences, and cost-efficient handling of volatile demand.