- HVAC

- Screw Compressor Market

Screw Compressor Market Size, Share, and Growth Forecast 2025 - 2032

Screw Compressor Market By Lubrication Type (Oil-Injected, Oil-Free), Technology (Stationary, Portable), Power Source (Electric, Others), Capacity (Up to ~50 HP, 51-250 HP, Above 250 HP), End-user Industry (Oil & Gas, Others), and Regional Analysis for 2025 - 2032

Screw Compressor Market Size and Trends Analysis

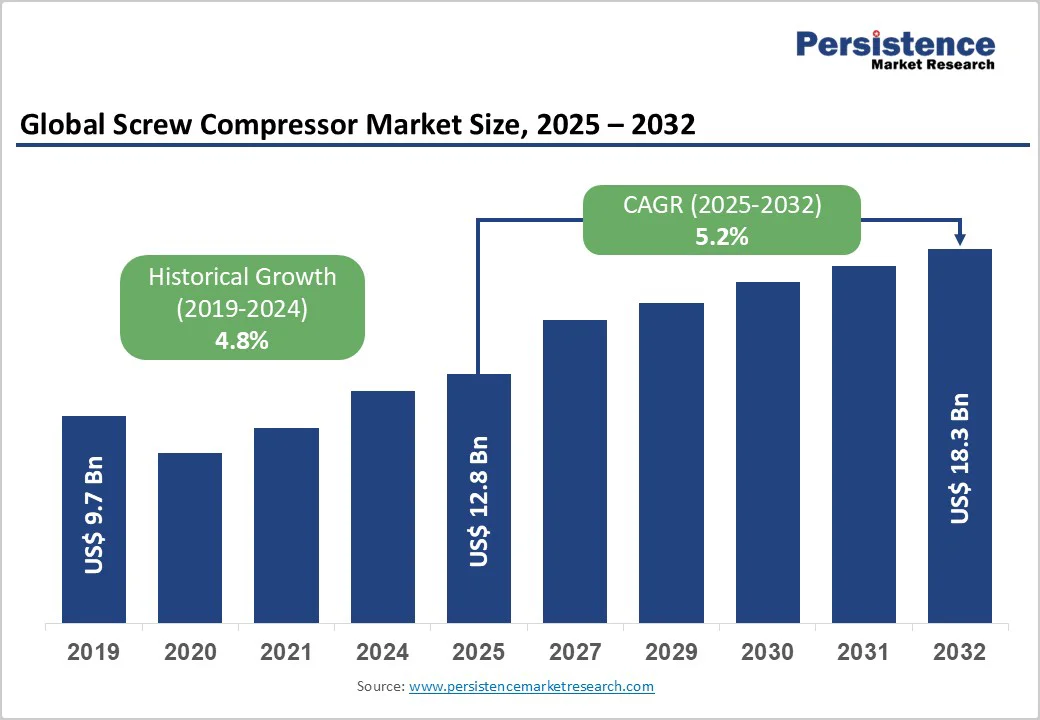

The global screw compressor market size is likely to be valued at US$12.8 billion in 2025 and is expected to reach US$18.3 billion by 2032, growing at a CAGR of 5.2% during the forecast period from 2025 to 2032, driven by increasing adoption across industries that demand reliable and energy-efficient compressed air solutions.

Key sectors such as manufacturing, oil and gas, chemicals and petrochemicals, food and beverage, and automotive are fueling demand. Advancements in compressor technology, stricter emission norms, and growing industrial automation continue to strengthen market expansion.

Key Industry Highlights

- Leading Region: Asia Pacific leads the screw compressor market by share, anchored by China and India’s manufacturing growth and policy support.

- Fastest-Growing Region: Europe emerges as the fastest-growing region due to robust regulatory harmonization, an innovative ecosystem, and high adoption of oil-free, energy-efficient compressors.

- Leading Capacity Type: The 51-250 HP segment dominates capacity due to widespread use in medium-to-large manufacturing and processing facilities, ensuring operational scalability and energy savings.

- Fastest-Growing Lubrication Type Segment: The oil-free screw compressor segment grows fastest, driven by regulatory requirements and demand for contamination-free air in pharmaceuticals, food processing, and electronics.

- Key Market Opportunity: Expansion in smart and IoT-enabled compressors with predictive maintenance offers key opportunities for competitive differentiation and enhanced operational uptime.

| Key Insights | Details |

|---|---|

| Screw Compressor Market Size (2025E) | US$12.8 Bn |

| Market Value Forecast (2032F) | US$18.3 Bn |

| Projected Growth CAGR (2025 - 2032) | 5.2% |

| Historical Market Growth (2019 - 2024) | 4.8% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Energy Efficiency and Sustainability Initiatives Driving Industrial Adoption

Industrial sectors are increasingly prioritizing energy-efficient technologies, and screw compressors are at the forefront of this shift. Modern units can reduce energy consumption by up to 35% compared to conventional systems, leading to significant cost savings. Features such as variable speed drives (VSD), IoT-enabled predictive maintenance, and advanced monitoring enhance operational efficiency while minimizing downtime.

Global sustainability goals and stricter environmental regulations are accelerating the adoption of energy-efficient compressors. As countries such as China and India advance industrial automation, screw compressors have become essential for continuous production lines, ensuring stable operations, lower energy costs, and reduced carbon emissions, aligning industrial efficiency with environmental responsibility.

Rapid Industrial Automation and Expansion

The screw compressor market benefits from rapid industrialization and sectoral diversification in Asia Pacific, North America, and Europe, which are driving adoption across multiple industries. The manufacturing sector, in particular, relies on these compressors for uninterrupted air supply in automotive assembly, material processing, and heavy machinery operations.

The oil & gas industry also contributes significantly to market growth, with increasing demand from brownfield revamps, new pipeline installations, and offshore projects. Screw compressors’ ability to deliver consistent, heavy-duty performance under continuous operation makes them indispensable in these sectors, reinforcing both market expansion and technological innovation investments.

Barrier Analysis - High Capital Investment and Maintenance Challenges Limiting SME Adoption

The initial capital requirement for screw compressors, especially oil-free and variable speed drive (VSD) models, remains a significant restraint for small and medium enterprises (SMEs). While these systems provide long-term savings through energy efficiency, the high upfront costs can deter budget-conscious buyers. Associated infrastructure costs, such as installation, air treatment systems, and control units, further elevate the investment burden for smaller facilities.

Maintenance challenges also affect adoption rates. Issues related to noise, heat emission, and service complexity require trained technicians and regular upkeep, which increases operational expenditure. These factors make it harder for screw compressors to penetrate markets where cost sensitivity and minimal maintenance requirements dominate decision-making.

Technical Complexity and Raw Material Price Volatility Affecting the Market Stability

The sophisticated design and operational requirements of screw compressors present barriers for industries lacking technical expertise. Complex installation procedures, coupled with the need for precise calibration and skilled personnel, can delay adoption in facilities with limited technical capacity. This is particularly relevant for oil-free screw compressors, which demand tighter tolerances and higher-quality materials.

Volatility in raw material prices, notably for steel, aluminum, and copper, directly impacts manufacturing costs and profit margins for compressor producers. These fluctuations make pricing less predictable, especially in export-driven markets. Consequently, certain industries continue to rely on reciprocating or scroll compressors due to their lower upfront costs and operational simplicity, restricting screw compressor penetration in niche or cost-sensitive segments.

Opportunity Analysis - Seamless Integration with Smart Factories and IoT-Driven Industrial Ecosystems

The rapid evolution of Industry 4.0 and IoT-enabled manufacturing is unlocking new opportunities for screw compressor manufacturers and service providers. Advanced screw compressors equipped with real-time monitoring, automated diagnostics, and predictive maintenance capabilities allow industries to reduce downtime, optimize performance, and enhance operational transparency. These smart systems also enable data-driven energy management, lowering the total ownership costs for users.

As industries move toward digitally connected and flexible production ecosystems, the integration of screw compressors into smart factory networks has become increasingly critical. This shift supports remote performance tracking, predictive servicing, and even “compressed air-as-a-service” models, allowing manufacturers to offer innovative value propositions and recurring revenue streams within industrial automation environments.

Rising Demand for Oil-Free Compressors in Clean Air and Hygienic Applications

Growing emphasis on air purity and product safety across industries such as food and beverage, pharmaceuticals, and electronics is driving the adoption of oil-free screw compressors. These systems meet stringent ISO Class 0 standards for air quality, ensuring contamination-free and reliable compressed air supply for sensitive manufacturing environments. Their ability to maintain process integrity makes them indispensable in hygiene-critical production lines.

Tightening global regulations on clean manufacturing practices and increasing consumer awareness about quality assurance continue to accelerate this trend. Innovations in compressor design, filtration technology, and energy-efficient oil-free systems are further expanding market potential. As a result, the clean air segment represents one of the most promising growth frontiers for screw compressor manufacturers worldwide.

Category-wise Analysis

Lubrication Type Insights

Oil-injected screw compressors dominate the market, accounting for around 60% of total installations. Their ability to maintain consistent performance under high-load conditions while minimizing lifecycle costs makes them essential across industries such as automotive manufacturing, general machinery, and petrochemical operations. These compressors also offer higher cooling efficiency and durability, making them ideal for heavy-duty continuous use.

Asia Pacific continues to drive the oil-injected segment due to widespread industrial expansion, infrastructure development, and rising manufacturing investments. The affordability and easy maintenance of oil-injected models have further encouraged adoption among small and mid-scale industries seeking reliable compressed air systems with minimal operational interruptions.

Technology Insights

Stationary screw compressors hold a leading share of over 70% within the market, primarily due to their extensive use in large industrial plants, assembly lines, and automated production systems. These units provide stable air delivery, superior efficiency, and compatibility with long-duty cycles, the key requirements for sectors such as automotive, petrochemicals, and heavy manufacturing.

With the growing push for sustainable operations, electric stationary compressors are increasingly replacing traditional diesel-powered systems. Their reduced emissions, quiet operation, and adaptability to smart monitoring platforms align with modern Industry 4.0 practices, strengthening their position as the backbone of industrial compressed air infrastructure worldwide.

Capacity Insights

The 51-250 HP capacity range leads the market, representing about 35% of installations across medium- and large-scale industrial facilities. These compressors offer an optimal combination of energy efficiency, scalability, and power output, making them highly suitable for continuous operation in manufacturing, automotive, and chemical sectors.

While smaller units (up to 50 HP) remain popular among SMEs due to their affordability and compactness, high-capacity models above 250 HP serve specialized needs such as mining, LNG processing, and large-scale metallurgy. This balanced demand across capacity ranges underscores the versatility and adaptability of screw compressors in diverse industrial operations.

Power Source Insights

Electric screw compressors account for roughly 40-54% of total market demand, supported by global sustainability initiatives and the shift toward low-emission industrial operations. Their advantages, such as consistent performance, low noise, and minimal maintenance, make them ideal for indoor and regulated environments, including electronics manufacturing, pharmaceuticals, and food processing facilities.

In contrast, diesel and hybrid-powered compressors maintain relevance in industries that require high mobility and torque output, such as mining, oilfield services, and construction. Hybrid variants are also emerging as transitional solutions, balancing fuel efficiency and lower emissions for sites lacking consistent power infrastructure.

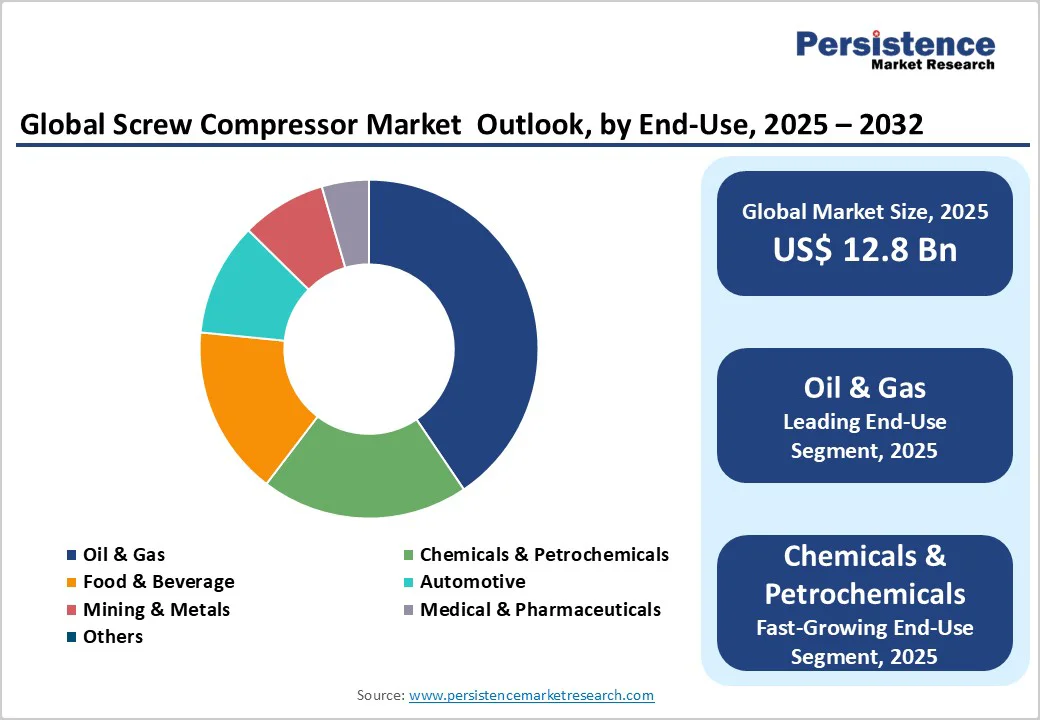

End-user Industry Insights

The oil & gas industry stands out as the fastest-growing end-use segment, with screw compressors playing a pivotal role in upstream drilling, gas gathering, and pipeline compression. Their ability to handle high-pressure operations and ensure continuous flow makes them indispensable in exploration and LNG processing. Rising investments in global energy infrastructure are further fueling adoption across this sector.

Manufacturing, however, continues to dominate overall market share due to widespread use in pneumatic tools, material handling, and process automation. Additional demand stems from pharmaceuticals, food & beverage, and metal processing industries, where clean, efficient compressed air remains critical for precision and productivity.

Regional Insights

Europe Screw Compressor Market Trends

Europe’s screw compressor market is the fastest-growing, benefiting from a well-established manufacturing base and one of the world’s most stringent regulatory environments. The region’s focus on decarbonization and industrial energy efficiency drives adoption of oil-free and variable-speed compressor systems, particularly across healthcare, food processing, and high-precision engineering sectors.

Countries such as Germany, the U.K., and France are at the forefront of developing high-efficiency rotary compressors meeting EU-wide ISO and Ecodesign standards. Regulatory frameworks such as RoHS and F-Gas regulations are pushing manufacturers to adopt sustainable materials and low-GWP refrigerants. This regulatory alignment fosters continuous technological innovation and reinforces Europe’s leadership in clean, high-performance compressor systems.

Asia Pacific Screw Compressor Market Trends

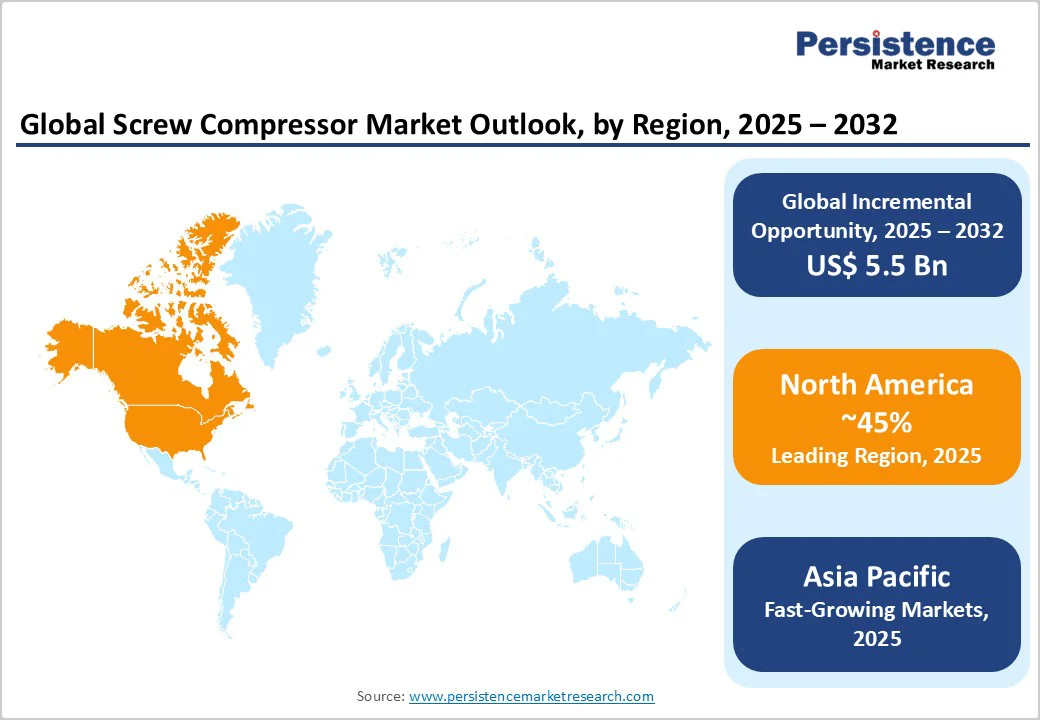

Asia Pacific remains the leading region for screw compressors, accounting for 45% of the market share in 2025, underpinned by rapid industrialization and strong government-backed manufacturing initiatives. Nations including China, India, Japan, and South Korea are witnessing surging investments in automotive, electronics, and food processing sectors, each requiring reliable compressed air systems for large-scale operations.

Programs such as “Made in China 2025” and India’s Production Linked Incentive (PLI) schemes are driving capacity expansion, technology localization, and equipment modernization. The rising infrastructure development, export-oriented growth, and a push for energy-efficient production are reinforcing demand for rotary screw compressors, which now account for more than 70% of total regional installations.

North America Screw Compressor Market Trends

North America exhibits strong adoption of electric stationary screw compressors, driven by expanding construction projects, energy-efficiency mandates, and the revitalization of oil and gas exploration. The region’s emphasis on reducing carbon footprints and enhancing operational reliability has pushed industries toward energy-optimized, low-noise compressor solutions suitable for both indoor and outdoor industrial use.

The U.S. leads in integrating smart compressor technologies, featuring IoT-enabled monitoring and predictive maintenance systems. Key manufacturers such as Atlas Copco and Kaishan USA are focusing on advanced design improvements, durability, and automation compatibility. As industries prioritize safety, emission control, and compliance with tightening federal standards, the demand for next-generation electric screw compressors continues to accelerate.

Competitive Landscape

The global screw compressor market exhibits a moderately consolidated competitive structure, where a limited number of multinational players dominate both regional and global operations. These companies maintain their market positions through extensive manufacturing networks, technological leadership, and strong after-sales service frameworks.

Competition is increasingly shaped by vertical integration, product innovation, and digital transformation. Manufacturers are prioritizing energy-efficient designs, IoT-enabled monitoring, and advanced control systems to meet evolving industrial needs. Strategic partnerships, regional expansions, and service-based business models further enhance market reach, while R&D investments in sustainability and automation continue to define the competitive edge across leading participants.

Key Industry Developments

- In April 2025, Atlas Copco AB launched a new oil-sealed screw vacuum pump, integrated with advanced Variable Speed Drive (VSD) technology and intelligent connectivity, setting new benchmarks for industrial energy efficiency.

- In March 2025, ELGi Equipments Ltd. introduced new compressed air stabilization technology and expanded in-house motor production, aiming to enhance equipment reliability and global operational efficiency.

- In February 2025, Kaeser Kompressoren SE unveiled its next-generation synchronous reluctance motors, improving efficiency and performance across its variable-speed rotary screw compressor range.

Companies Covered in Screw Compressor Market

- Atlas Copco AB

- Ingersoll Rand

- Kaeser Kompressoren SE

- Hitachi Ltd.

- Sullair LLC

- Gardner Denver Industries

- ELGi Equipment Ltd.

- Kobe Steel Ltd. (Kobelco)

- Daikin Industries Ltd.

- Mitsubishi Electric Corporation

- Aerzener Maschinenfabrik GmbH (Aerzen)

- Siemens Energy AG

- BOGE Kompressoren GmbH

- Kaishan Compressor

- Quincy Compressor LLC

Frequently Asked Questions

The market size is projected to reach US$18.3 Billion by 2032, growing at a CAGR of 5.2%.

Rising energy efficiency standards, regulatory mandates, industrial automation, and increasing adoption in food processing, pharmaceuticals, and oil and gas drive demand.

The oil-injected lubrication type remains the leading segment, accounting for around 60% of market deployments due to operational cost savings, durability, and reliable air delivery.

Asia Pacific dominates with the largest market share, led by China and India’s manufacturing and infrastructure investment.

Integration of IoT and smart monitoring systems for predictive maintenance, energy savings, and real-time diagnostics is the key opportunity for market participants.

Major players include Atlas Copco AB, Ingersoll Rand, Kaeser Kompressoren SE, Hitachi Ltd., Sullair LLC, and Gardner Denver Industries.