- HVAC

- Oil-Free Screw Compressor Market

Oil-Free Screw Compressor Market Size, Share, and Growth Forecast 2026 - 2033

Oil-Free Screw Compressor Market by Product Type (Portable and Stationary), Stage (Single Stage and Multi Stage), Power Rating (Below 15 kW, 15 – 55 kW, 55 – 160 kW, and Above 160 kW), Industry (Food & Beverage, Pharmaceutical, Semiconductor & Electronics, and Others), and Regional Analysis 2026 - 2033

Oil-Free Screw Compressor Market Size and Share Analysis

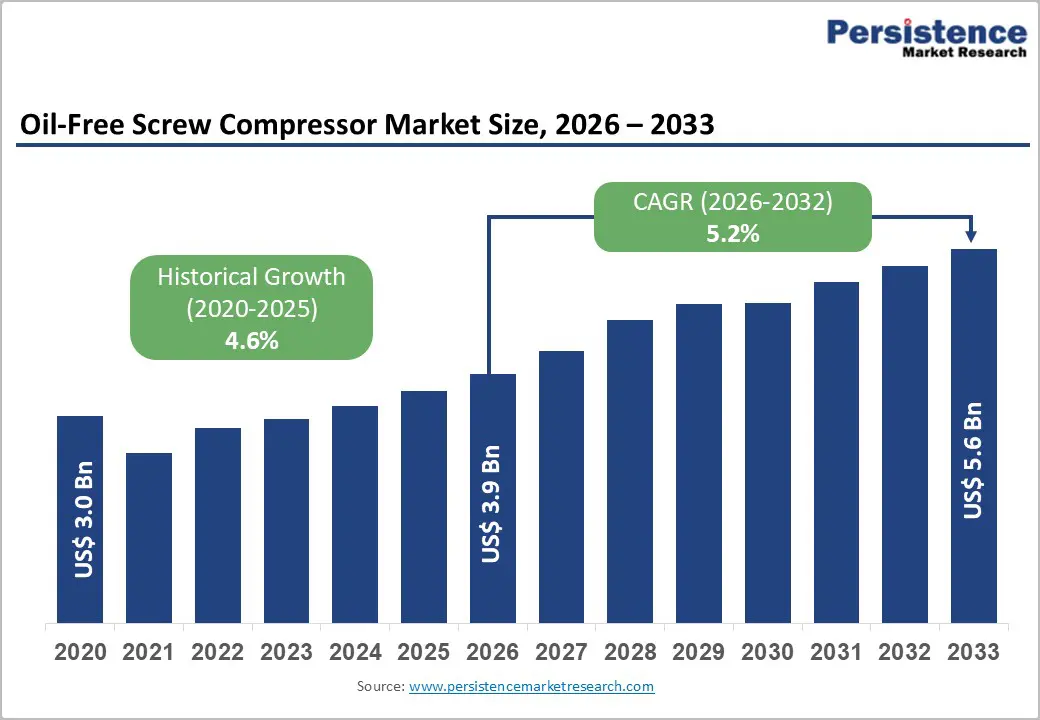

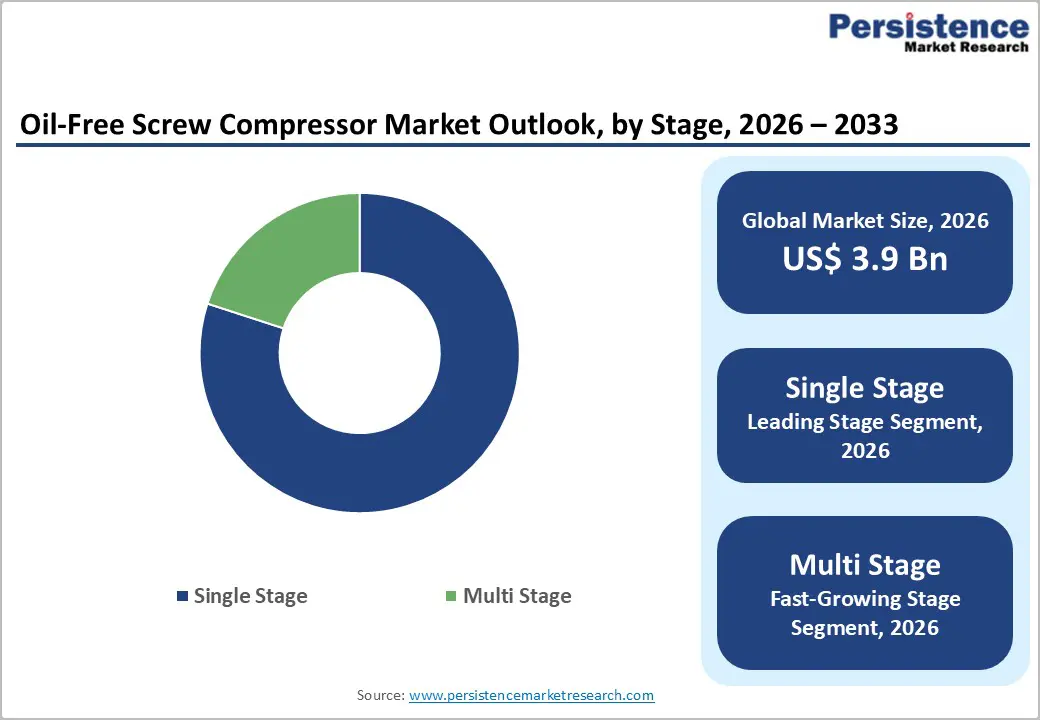

The global oil-free screw compressor market size is likely to be valued at US$ 3.9 billion in 2026 and is projected to reach US$ 5.6 billion by 2033, growing at a CAGR of 5.2% between 2026 and 2033.

Market expansion is driven by escalating regulatory requirements mandating ISO 8573-1 Class 0 certification, establishing zero-oil-contamination standards across the pharmaceutical, food and beverage, semiconductor, and electronics manufacturing sectors, and by exponential growth in critical industrial applications in which contamination risk directly threatens product quality and operational efficiency.

Key Market Highlights

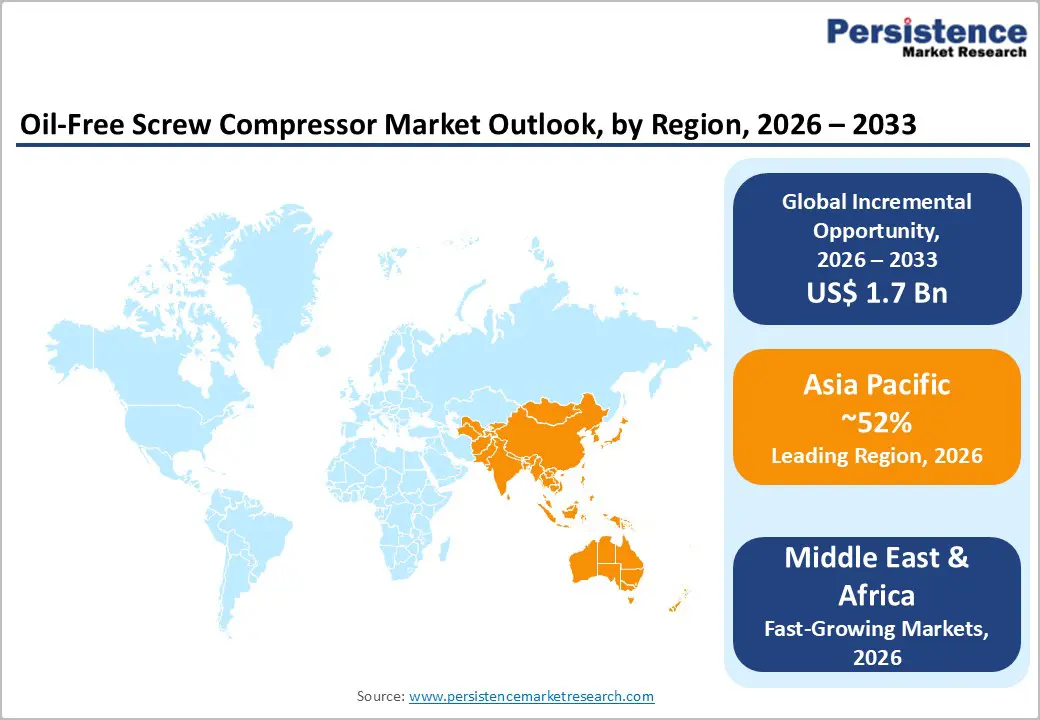

- Leading Region: Asia Pacific maintains market leadership with 53% global share driven by China's manufacturing dominance, India's pharmaceutical expansion, government Make in India initiative, infrastructure investment programs, and emerging market industrialization.

- Fastest Growing Region: North America experiences the fastest growth at a projected 7.1% CAGR, anchored by the United States regulatory framework excellence, occupational health and safety standards, strong semiconductor and electronics manufacturing base, and premium energy-efficient compressor adoption supporting sustained developed market dominance.

- Dominant Product Type: Stationary oil-free screw compressors command market dominance with 70% installation share, driven by industrial-scale application requirements, superior efficiency, reliability, and continuous operational capability supporting sustained segment leadership.

- Growing Power Rating: The 55-160 kW power rating segment is the fastest-growing in Asia Pacific, with a 10.5% CAGR, propelled by large-scale industrial applications in chemical processing, oil and gas refining, power generation, and petroleum operations.

- Key Market Opportunity: Hydrogen economy development and renewable energy sector expansion represent exceptional opportunities, with APAC hydrogen capacity projected to increase fivefold by 2030, creating critical dependence on oil-free compressor technology for clean energy infrastructure.

| Key Insights | Details |

|---|---|

|

Oil-Free Screw Compressor Market Size (2026E) |

US$ 3.9 Bn |

|

Market Value Forecast (2033F) |

US$ 5.6 Bn |

|

Projected Growth CAGR(2026-2033) |

5.2% |

|

Historical Market Growth (2020-2025) |

4.6% |

Market Dynamics

Drivers - Stringent ISO Regulatory Standards and Contamination-Free Air Mandates Across Critical Industries

Global regulatory frameworks, including ISO 8573-1 Class 0 certification requirements, have established mandatory zero-oil-contamination standards compelling the adoption of oil-free screw compressors across pharmaceutical, food and beverage, semiconductor, electronics, and medical device manufacturing sectors. Pharmaceutical industry compliance requirements that ensure drug manufacturing purity, food and beverage sector mandates that prevent product contamination, and semiconductor fabrication specifications that require ultra-high air purity create non-negotiable procurement specifications favoring oil-free compressor technologies.

United Nations Environment Programme carbon-emission reduction targets and government policies promoting industrial sustainability provide additional drivers that accelerate the adoption of oil-free technologies as manufacturers transition from traditional oil-injected systems. The post-pandemic heightened focus on food product safety led to an 87.6% year-over-year increase in packaged food consumption during the early pandemic, establishing a sustained demand baseline that extends beyond the pandemic recovery. Occupational Health and Safety standards across North America and workplace air quality compliance mandates create institutional requirements that support sustained market expansion in developed markets.

Energy Efficiency Innovation and Industry 4.0 Smart Manufacturing Integration

Modern oil-free screw compressors deliver 15-20% superior energy efficiency compared to conventional systems, directly translating to substantial operating cost reduction and accelerated return on investment, justifying premium acquisition costs. Variable Speed Drive (VSD) technology, which enables dynamic adjustment of compressor speed in response to demand, reduces energy consumption by up to 35% compared with conventional fixed-speed systems, providing a compelling economic justification for industrial investment. IoT-enabled smart monitoring systems, artificial intelligence-powered predictive maintenance, and real-time performance tracking, integrated with cloud-based platforms that enable remote diagnostics and optimization, align with the Industry 4.0 manufacturing transformation and establish competitive advantages for early adopters.

Integration with building management systems and manufacturing execution systems enables data-driven energy optimization and automated performance tuning, thereby enhancing operational efficiency and supporting the development of compressed air-as-a-service business models. Remote monitoring capability, elimination of unplanned downtime and extended service intervals, and reducing maintenance costs combine to establish total cost of ownership advantages justifying capital investment for manufacturing facilities.

Restraint - High Capital Investment Requirements and Upfront Cost Barriers for Small and Medium Enterprises

Oil-free screw compressors incorporating advanced variable-speed drive technology, IoT connectivity, and enhanced, energy-efficient components require substantial initial capital investment, substantially exceeding the costs of traditional oil-injected compressors, creating significant affordability barriers, particularly affecting small and medium-sized enterprises with limited capital budgets. Associated infrastructure requirements, including air treatment systems, control units, and installation labor, further increase total project costs, potentially extending the capital payback period. Complex maintenance requirements and the need for specialized technical expertise increase operational costs for facilities that lack in-house expertise.

Technical Standardization Challenges and Supply Chain Vulnerability

Variations in regulatory standards across regions, including divergent ISO interpretations and regional compliance protocols, complicate manufacturers' efforts to achieve multi-market certification and compliance. Supply chain vulnerabilities demonstrated during pandemic disruptions and ongoing raw material availability constraints affect production scheduling and delivery timelines, thereby impacting customer satisfaction and market penetration.

Opportunity - Hydrogen Economy Development and Renewable Energy Sector Expansion

Hydrogen production capacity in the Asia-Pacific region is projected to increase fivefold by 2030, driven by government clean-energy transition initiatives and renewable energy mandates, creating a significant market opportunity for oil-free compressor manufacturers. Hydrogen electrolysis processes that require precise air-flow control and contamination-free operation create a critical dependence on oil-free compressor technology as foundational infrastructure.

Mitsubishi Heavy Industries' deployment of centrifugal oil-free compressors in hydrogen electrolysis plants demonstrates commercial viability and performance validation, establishing market confidence. Biofuel production capacity in the Asia-Pacific region is expected to double by 2030, creating incremental demand for advanced compressor solutions to support refining and processing operations. Solar panel manufacturing, fuel cell production, and other renewable energy applications require specialized air-compression systems, creating premium market opportunities with higher-margin profiles that support sustained growth.

Advanced Thermal Interface Solutions and Aerospace/Defense Application Expansion

Rapid advances in IoT, artificial intelligence, and data analytics technologies enable next-generation oil-free compressor systems equipped with real-time monitoring, automated diagnostics, and predictive maintenance capabilities, thereby creating competitive differentiation opportunities for manufacturers. Compressed air-as-a-service business model development leveraging remote monitoring and cloud-based optimization platforms represents an emerging revenue stream opportunity that supports manufacturers' profitability expansion.

Integration with smart factory networks, manufacturing execution systems, and enterprise resource planning platforms creates switching costs, protecting customer relationships while establishing recurring revenue opportunities through service contracts and optimization algorithms. Decentralized industrial operations requiring flexible compressed air infrastructure and distributed manufacturing networks expanding in emerging markets are establishing growing market segments favorable to the adoption of advanced oil-free compressor systems, supporting sustained expansion through the forecast period.

Category-wise Analysis

Product Type Insights

Stationary oil-free screw compressors command market dominance, accounting for approximately 70% of total installations and 60.8% of the Asia Pacific market share in 2026, driven by superior efficiency, reliability, and continuous operational capability essential for industrial-scale applications. Large manufacturing plants, assembly lines, and pharmaceutical production facilities standardize on stationary systems delivering stable air delivery, exceptional mechanical durability, and compatibility with extended duty cycles. Rotary screw technology, representing 45.1% of Asia Pacific market share in 2024 dominates stationary installations through proven reliability, low maintenance requirements, and cost-effective operation at scale.

Electric stationary compressors are increasingly replacing traditional diesel-powered systems, reflecting sustainability emphasis and alignment with Industry 4.0 practices, including smart monitoring platform integration. Economic advantages of stationary systems, including lower per-unit energy costs and simplified maintenance protocols, support continued dominance throughout the forecast period.

Stage Insights

Single-stage compression is the dominant compressor stage configuration, accounting for approximately 60% of the market, owing to lower capital costs, simplified design, and suitability for most industrial applications. Single-stage compressors that deliver cost-competitive solutions for applications below 55 kW support widespread adoption across small and medium-sized enterprises and in lower-pressure requirement applications. Air-cooled single-stage designs, which eliminate the need for additional cooling infrastructure, simplify installation and reduce total project costs, particularly for retrofit applications in existing facilities.

Maintenance simplicity and extended component service intervals characteristic of single-stage systems reduce operational complexity, thereby supporting total cost of ownership advantages despite a marginally lower efficiency than multi-stage alternatives. Continued market dominance reflects the prioritization of capital efficiency among industrial buyers.

Power Rating Insights

Oil-free screw compressors with power ratings below 15 kW account for 50.4% of the market in 2026, driven by widespread adoption among small and medium-sized enterprises in the food and beverage, pharmaceutical, and electronics manufacturing sectors. Cost-effective solutions that enable SMEs to access contamination-free compressed air without requiring premium investments support market penetration among budget-conscious customer segments. The expansion of the food processing equipment sector at an annual rate of 8.8%, driven by growth in packaged food demand and agricultural value-added processing, creates substantial incremental demand for compact, cost-effective compression systems that meet hygiene requirements.

The portability and space-efficiency advantages of smaller compressor units facilitate installation in existing facilities with space constraints. The 55-160 kW segment is experiencing the fastest growth, with a 10.5% CAGR, reflecting large-scale industrial adoption across the chemical processing, oil and gas, and power generation sectors. Large-scale applications, including petrochemical plants and refining operations, require advanced capacity and performance specifications supporting premium pricing and margin profiles.

Industry Insights

The food and beverage industry represents the largest end-use segment, commanding a dominant market position driven by a surge in packaged food consumption of 87.6% year-over-year during the pandemic. Bottling operations, packaging machinery, and material conveying systems require oil-free, contamination-free compressed air, preventing product spoilage and ensuring consumer safety compliance. Regulatory requirements mandating pathogen-free production environments and zero-risk-of-contamination management create non-negotiable equipment specifications. Post-pandemic consumer preference persistence for packaged and processed foods maintains elevated demand, supporting sustained market expansion.

Pharmaceuticals are likely to account for 35.8% of application demand in 2026, reflecting a critical requirement for sterile, contamination-free compressed air across drug manufacturing, sterilization, and medical air supply systems. Asia Pacific pharmaceutical market dominance, with 30% of global pharmaceutical production, establishes a substantial regional growth opportunity supporting continued sector expansion.

Regional Insights

North America Oil-Free Screw Compressor Market Trends

North America represents a mature, high-value oil-free screw compressor market anchored by United States market dominance driven by stringent occupational health and safety regulations establishing mandatory air quality standards across industrial facilities. Occupational Health and Safety (OHS) standards requirements mandate adoption of contamination-free compressed air supporting systematic market penetration.

Strong regulatory framework including EPA standards and OSHA requirements establish institutional compliance drivers reinforcing sustained market demand. Semiconductor and electronics manufacturing sectors concentrated in North America require ultra-high air purity supporting premium compressor system adoption. Technological innovation leadership and focus on energy-efficient variable speed drive systems reflect developed market sophistication and willingness to invest in advanced technologies supporting operational excellence.

Europe Oil-Free Screw Compressor Market Trends

Europe represents a significant global oil-free screw compressor market with Germany maintaining technology leadership through Kaeser Kompressoren SE, Boge Compressors, and established industrial base commanding premium market positioning. Stringent EU environmental regulations including RoHS directives and F-Gas regulations drive sustainable product development and energy-efficient compressor adoption. Ecodesign standards and regulatory harmonization across EU member states enable standardized compliance frameworks supporting efficient supply chain management.

Food processing, pharmaceutical, and precision engineering sectors concentrate demand across multiple European nations supporting sustained regional market expansion. ISO/Ecodesign standard leadership by German manufacturers establishes competitive differentiation through technology excellence supporting premium positioning.

Asia Pacific Oil-Free Screw Compressor Market Trends

Asia Pacific commands largest global oil-free screw compressor market with 52.67% global market share in 2026. China representing 40.5% of regional sales in 2026 leverages robust manufacturing base, semiconductor industry dominance, and government-backed technology investment establishing regional leadership position. Made-in-China manufacturing roadmap incentivizing CNC machining and automated production drives demand for efficient compressed air infrastructure among manufacturing facilities. Semiconductor industry expansion, particularly SMIC production capacity increases, requires oil-free compressor infrastructure supporting process purity and operational reliability.

India experiences fastest Asia Pacific regional growth as largest global generic pharmaceutical producer creating significant demand for oil-free compressors in sterile drug manufacturing environments. Government Make in India initiative and Production Linked Incentive (PLI) schemes for pharmaceutical APIs and processed foods encourage domestic manufacturing expansion requiring contamination-free compressed air infrastructure. Food processing sector rapid expansion and dairy product manufacturing growth generate incremental compressor demand across packaging and processing operations. Government water treatment facility expansion and wastewater treatment infrastructure development establish emerging application opportunities for advanced compressor systems supporting sustainability objectives.

Competitive Landscape

The oil-free screw compressor market exhibits a moderately consolidated competitive structure dominated by global industrial manufacturers leveraging established technology platforms, manufacturing scale, and global distribution networks. Tier 1 companies including Atlas Copco, Ingersoll Rand, Gardner Denver, and Kaeser Kompressoren collectively command substantial market share through comprehensive product portfolios and technical excellence. Atlas Copco's market leadership through ZR and ZT rotary screw lines demonstrates technology differentiation and energy-efficient design.

Gardner Denver's PureAir Ultima technology introducing dual-motor variable speed architecture establishes competitive innovation advancing energy efficiency standards. Regional manufacturers establish competitive positions through cost competitiveness and localized product customization. Competitive strategies emphasize R&D investment in energy efficiency, IoT integration, and Industry 4.0 compatibility supporting product differentiation and market penetration.

Key Market Developments:

- In October 2025, Hitachi Industrial Equipment Systems Co., Ltd. introduced new G Series oil-free scroll air compressor featuring advanced scroll mechanism technology delivering enhanced performance, reliability, and energy efficiency for semiconductor, electronics, and food processing applications.

- In July 2025, Atlas Copco continues advancement of ZR and ZT oil-free rotary screw compressor lines incorporating latest variable speed drive technology, achieving market-leading energy efficiency and extended service intervals supporting customer operational cost reduction.

- In March 2025, AERZEN introduced new oil-free air compressors with optimum energy efficiency. The new double-stage air compressors of the DS series from AERZEN compress absolutely oil-free in accordance with ISO 8573-1, class 0 for all common applications such as the food and beverage industry, chemical and process engineering as well as medical and pharmaceutical technology.

Companies Covered in Oil-Free Screw Compressor Market

- Atlas Copco AB

- Ingersoll Rand Inc.

- Gardner Denver Holdings, Inc.

- Sullair LLC

- Kobelco Compressors America, Inc.

- CompAir

- Boge Compressors

- Kaeser Compressors, Inc.

- Hitachi Industrial Equipment Systems Co., Ltd.

- Mitsubishi Heavy Industries Compressors

- Rotair SPA

- Dosan Fuel

- Gosling’s Oil Free Screw Compressor

- Havana Club International

- Anest Iwata

Frequently Asked Questions

The global oil-free screw compressor market is projected to reach US$ 5.6 billion by 2032, expanding from US$ 3.9 billion in 2025 at a CAGR of 5.2%, driven by regulatory compliance mandates, energy efficiency requirements, and pharmaceutical and food processing industry expansion.

Market demand growth is driven by multiple converging factors including ISO 8573-1 Class 0 certification mandates establishing zero-contamination standards, post-pandemic sustained demand baseline across food processing and pharmaceuticals, energy efficiency advancement delivering 15-20% superior performance, Industry 4.0 smart manufacturing integration, hydrogen economy development, and renewable energy sector expansion across Asia Pacific and emerging markets.

Stationary oil-free screw compressors command market leadership, representing approximately 70% of total installations and 60.8% of Asia Pacific market share, driven by industrial-scale application requirements, superior efficiency, reliability, and continuous operational capability supporting infrastructure development.

Asia Pacific dominates the global market with 53% global market share in 2026, anchored by China's 30.5% regional share driven by manufacturing dominance, India's fastest growth through pharmaceutical expansion, and rapid industrialization supporting sustained expansion.

Major market opportunities include hydrogen economy development with APAC capacity projected to increase fivefold by 2030; Industry 4.0 smart manufacturing integration enabling predictive maintenance and remote monitoring; renewable energy sector expansion including biofuel production and solar manufacturing; and emerging compressed air-as-service business models.