- Smart Packaging

- Returnable Circular Packaging Market

Returnable Circular Packaging Market Size, Share, and Growth Forecast, 2026 - 2033

Returnable Circular Packaging Market by Materials (Rigid Plastics, Metals, Others), Packaging Formats (Crates & Pallets, Drums & Barrels, Others), End-user Industry, and Regional Analysis for 2026 - 2033

Returnable Circular Packaging Market Size and Trends Analysis

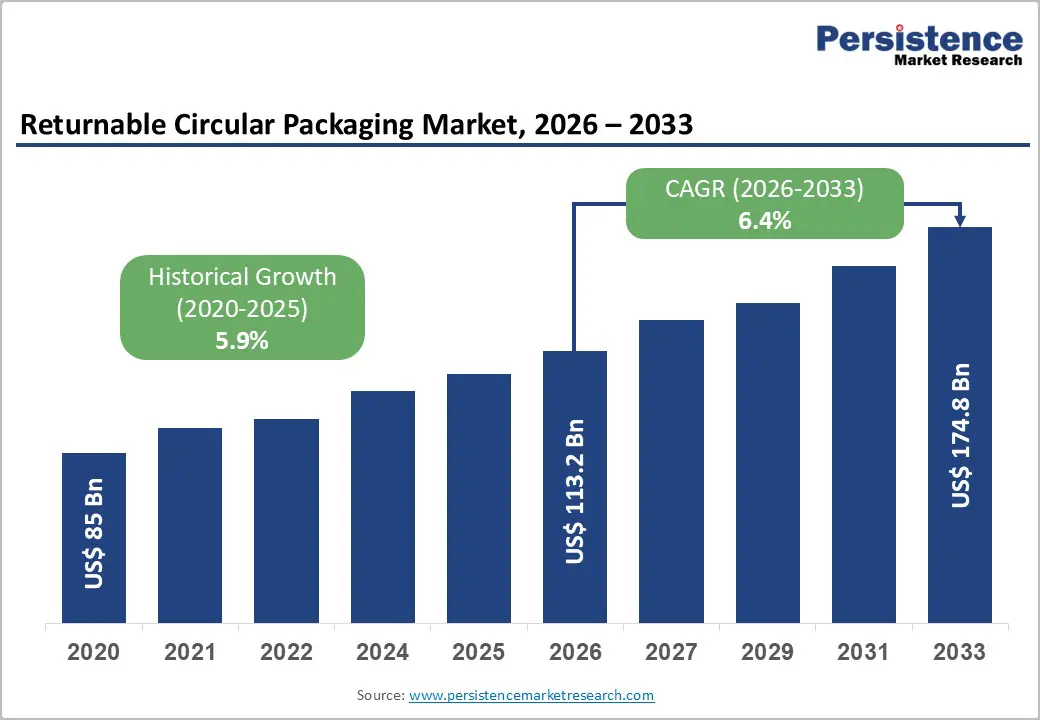

The global returnable circular packaging market size is likely to be valued at US$113.2 billion in 2026 and is expected to reach US$174.8 billion by 2033, growing at a CAGR of 6.4% between 2026 and 2033, driven by regulatory pressure to reduce single-use packaging, manufacturer commitments to reuse and refill systems, and measurable cost-efficiency gains from pooled logistics models.

Industrial end-users across food & beverages, chemicals, and pharmaceuticals are accelerating the adoption of reusable crates, intermediate bulk containers (IBCs), and pallets to lower per-unit packaging costs and lifecycle emissions.

Key Industry Highlights

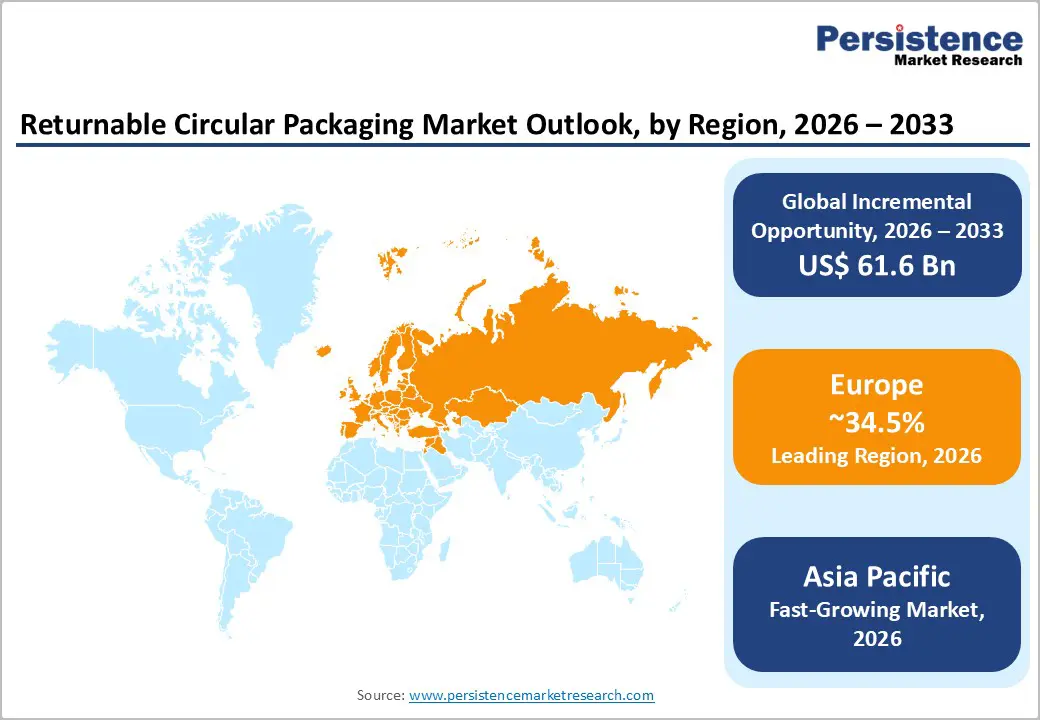

- Leading Region: Europe is projected to hold approximately 34.5% share of the market, driven by regulatory mandates, deposit-return schemes, and mature pooling networks.

- Fastest-Growing Region: Asia Pacific is the fastest-growing region, due to rapid industrialization, e-commerce growth, and rising corporate sustainability initiatives.

- Investment Plans: Expansion of refurbishment hubs, digital asset tracking platforms, and regional pooling networks to support reuse scaling across retail, industrial, and FMCG supply chains.

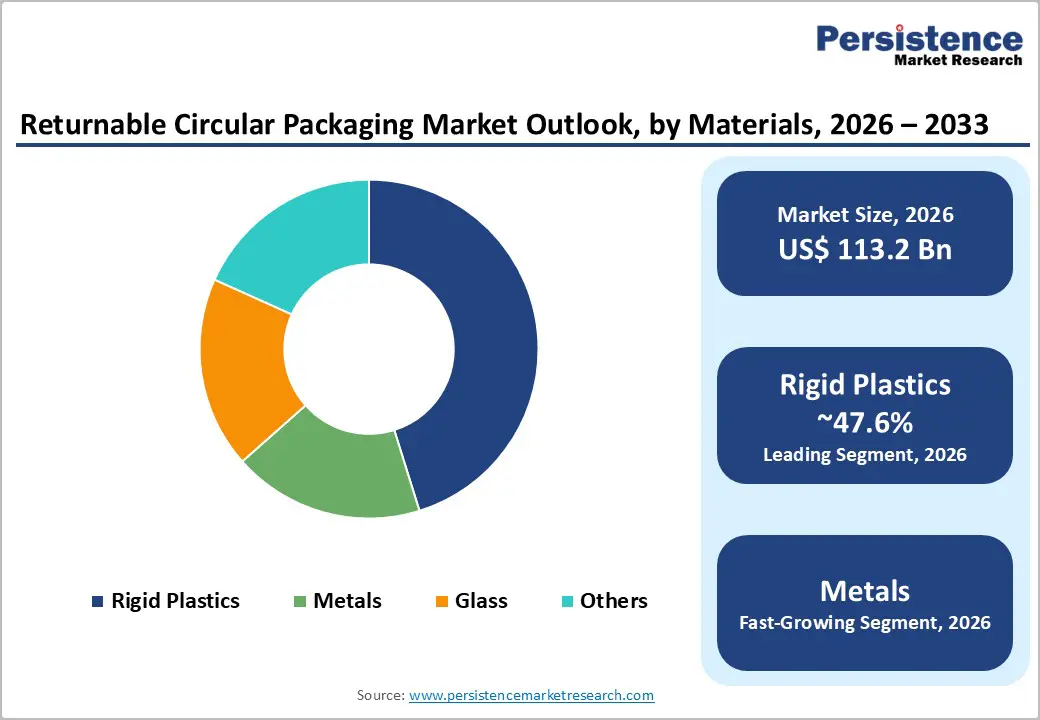

- Dominant Materials: The rigid plastics segment is anticipated to hold 47.6% market share, widely used in reusable plastic crates, pallets, tubs, and bottles.

- Leading Packaging Formats: Crates & pallets are estimated to hold approximately 39.6% market share, forming the backbone of pooled returnable logistics systems.

| Key Insights | Details |

|---|---|

| Returnable Circular Packaging Market Size (2026E) | US$113.2 Bn |

| Market Value Forecast (2033F) | US$174.8 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.4% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.9% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Regulatory and Policy Acceleration for Reuse and Packaging Waste Reduction

Government-led initiatives targeting packaging waste reduction are materially reshaping demand for returnable packaging systems. In Europe, revised packaging regulations and national deposit and reuse schemes are increasing mandatory reuse targets while tightening labeling, traceability, and waste-reduction requirements. These measures raise compliance costs for single-use packaging and improve the economic viability of pooled, digitally enabled returnable systems. Clearly defined implementation timelines and enforcement mechanisms are pushing brand owners to pilot and scale refillable and returnable formats to meet 2030-2040 waste reduction objectives. This regulatory certainty reduces investment risk in reuse infrastructure and strengthens first-mover advantages for logistics providers and pooled-asset operators.

Corporate Sustainability Commitments and Procurement Economics

Large FMCG companies and retailers are increasingly aligning procurement decisions with total cost of ownership and lifecycle emissions metrics. Returnable packaging reduces per-use material costs, minimizes waste management liabilities, and supports improved Scope 3 emissions reporting. Major food and beverage producers have introduced reuse and refill pilots, supported by supplier mandates that favor returnable crates, refillable bottles, and pooled pallets. The economic case is strongest in high-frequency reuse environments, where 50-200+ reuse cycles significantly dilute upfront capital costs and generate net savings across packaging procurement, disposal fees, and extended producer responsibility compliance. This shift is driving procurement-led scaling across regional supply chains and cross-industry pooling networks.

Digital Enablement of Pooling and Reverse Logistics

Advances in digital identification and asset-tracking technologies are enabling the large-scale deployment of returnable packaging. IoT tags, QR codes, and cloud-based platforms support real-time asset visibility, automated billing, and lifecycle management across multi-party pooling systems. These capabilities reduce administrative friction, asset shrinkage, and loss rates while enabling traceability for cleaning, temperature control, and regulatory reporting in food, pharmaceutical, and chemical applications. Integration of digital tracking with logistics optimization improves return flow efficiency and asset utilization, materially lowering unit costs and supporting commercial scalability of returnable packaging networks.

Barrier Analysis - High Upfront Capital and Collection Infrastructure Costs

The deployment of returnable packaging systems requires substantial upfront investment in durable assets, reverse-logistics infrastructure, cleaning and repair facilities, and supporting IT platforms. For smaller suppliers, high capital requirements and uncertain utilization rates can extend payback periods, particularly when return compliance is inconsistent across partners. In low-density regions or fragmented supply chains, collection and redistribution costs may erode anticipated savings. From a risk perspective, pooling systems typically require utilization rates above 40-60% and multi-year contractual commitments to achieve financial breakeven, limiting adoption in low-volume or last-mile-intensive routes.

Cross-Industry Coordination and Standardization Challenges

Effective returnable packaging models depend on interoperability across containers, shared quality standards, and aligned billing and repair frameworks among manufacturers, retailers, and logistics providers. Fragmented specifications, such as non-standard crate dimensions, pallet formats, or IBC fittings, increase handling complexity and reduce pooling efficiency. Delays in standardization slow network effects and raise operational friction. While regulatory alignment around digital data carriers and deposit mechanisms is improving, interim inconsistencies across national and voluntary schemes continue to create uneven adoption patterns and higher transaction costs.

Opportunity Analysis - Rapid Expansion across Asia Pacific

Asia Pacific represents the most significant near-term growth opportunity, led by China, India, and ASEAN economies. Rapid expansion of FMCG distribution, accelerating e-commerce penetration, and evolving extended producer responsibility (EPR) frameworks are strengthening the commercial case for returnable packaging. High urban population density and concentrated manufacturing clusters enable frequent reuse cycles and faster returns on investment from pooling. Rising regulatory pressure to reduce single-use plastics, growing corporate sustainability commitments, and increasing consumer awareness of circular economy practices also drive adoption across retail, food, and industrial supply chains. Improvements in reverse logistics infrastructure, digital tracking technologies, and cross-industry collaboration further enhance operational efficiency and scalability, positioning the region as a key hub for returnable packaging innovation.

Industrial and Chemical Sector Adoption of IBCs and Metal Containers

Industrial and chemical manufacturers increasingly require certified, high-durability returnable containers to meet regulatory and safety standards. The high per-unit value of industrial packaging, combined with strict containment requirements, is accelerating the adoption of returnable IBCs, drums, and metal containers. Forecasts indicate double-digit growth for industrial returnable packaging in multiple application segments. Transitioning to returnable systems reduces recurring packaging purchases and disposal costs while improving hazard compliance and traceability. Providers offering certified cleaning, inspection, and digital maintenance records are well-positioned to capture long-term service contracts.

Category-wise Analysis

Materials Insights

Rigid plastics, primarily HDPE and PP, are expected to maintain the largest share of the returnable circular packaging market, with an anticipated 47.6% market share. Their dominance stems from a strong combination of durability, lightweight design, impact resistance, and compatibility with repeated washing and pooling cycles. These plastics are extensively used in reusable plastic crates (RPCs) for fresh produce, beverage pallets, tubs, and refillable bottles, providing long service life and minimal breakage, which translates to significant total-cost savings for supply chains. For instance, major RPC operators deploy HDPE crates across grocery chains and beverage distribution networks, achieving 50-200 reuse cycles per unit, which lowers packaging procurement costs while improving environmental performance. The lightweight nature of rigid plastics also reduces transportation energy per cycle, supporting lifecycle carbon reduction initiatives compared with heavier materials such as glass or metal.

Metals, including steel and aluminum, represent the fastest-growing material segment, particularly in industrial, chemical, and high-end beverage applications. Metal drums, barrels, and intermediate bulk containers (IBCs) offer superior structural strength, chemical resistance, and compatibility with high-temperature sterilization, making them ideal for hazardous chemicals, lubricants, and refillable beverage containers. Adoption is strongest in sectors where durability and compliance outweigh weight and upfront capital costs, such as chemical manufacturing or pharmaceutical logistics. Companies that supply metal IBCs and drums often integrate inspection, cleaning, and recertification services to ensure safe, repeatable reuse. The combination of long service life and established recycling channels supports circular economy objectives and regulatory compliance, particularly in markets with stringent environmental and safety standards.

Packaging Formats Insights

Crates and pallets are expected to account for approximately 39.6% of the global returnable packaging market, serving as the operational backbone of logistics networks across manufacturing, retail, and distribution. Standardized reusable plastic crates (RPCs) for fruit, vegetables, and beverages, as well as pooled pallets, facilitate high-volume, repetitive flows between packers, distributors, and retailers. Major operators implement nationwide pooling networks that enable tracking, cleaning, repair, and refurbishment services, which reduce handling inefficiencies and inventory costs. Companies deploying these systems, such as large-scale grocery suppliers and beverage producers, benefit from predictable asset cycles and reduced expenditures on single-use packaging. Value creation extends beyond the container itself, encompassing logistics optimization, repair economies, and digital asset management to monitor usage and compliance.

Drums and barrels are likely to be the fastest-growing segment, driven by the adoption of closed-loop refill systems in chemicals, lubricants, and food ingredients. Regulatory tightening around hazardous materials handling, coupled with rising disposal costs, is encouraging industrial players to replace single-use drums with reusable steel or composite barrels. Each reusable drum delivers high per-unit cost avoidance, making them financially attractive despite higher upfront investment. For example, chemical manufacturers and food ingredient suppliers adopting certified refillable drums can reduce disposal fees and improve supply chain traceability. Service providers offering certified cleaning, recertification, and digital tracking of barrels are capturing incremental revenue streams and positioning themselves as strategic partners for industrial clients. This format’s growth outpaces crates and pallets due to higher asset value per unit and strong regulatory incentives in chemical and industrial logistics.

Regional Insights

North America Returnable Circular Packaging Market Trends - Established Reuse Ecosystem and Digitalized Reverse Logistics

North America remains a significant and rapidly evolving market for returnable circular packaging, anchored by a large installed base of pooled pallets, reusable plastic crates (RPCs), and industrial containers that serve high-volume sectors such as food and beverage, automotive components, electronics, and chemicals. The U.S. accounts for the bulk of regional demand, supported by advanced logistics infrastructure, strong corporate sustainability commitments, and broad uptake of closed-loop supply chain models among major manufacturers and retailers. North America’s reuse ecosystem is strengthened by well-established pool operators and service providers that manage millions of reusable units across national distribution networks, with many logistics centers now routinely integrating RFID and IoT tracking to monitor return flows and asset utilization. A range of practical deployments and regional developments reinforce this market momentum. For example, major grocery distributors and foodservice companies have transitioned from disposable to reusable plastic bins and totes to reduce spoilage and packaging waste, while industrial customers such as temperature-controlled logistics providers have replaced single-use crates with high-durability returnable pallets and containers to cut landfill disposal and minimize handling damage.

Independent initiatives by organizations such as the Reusable Packaging Association also support expanded market adoption by coordinating best practices and member products (including bulk bins, trays, pallets, and containers) across multiple industries. These developments collectively improve reverse logistics efficiency and strengthen the commercial viability of returnable systems. While regulation in North America is generally less prescriptive than in Europe, state-level policies restricting single-use plastics and voluntary zero-waste programs are creating additional momentum for adoption. Procurement leaders at major retailers are increasingly embedding circularity metrics into supplier evaluations, speeding up the adoption of reuse programs and driving greater investment in large-scale refurbishment infrastructure and digital asset tracking systems. These dynamics are elevating North America as both a large established market and a testing ground for innovative reuse frameworks across supply chains.

Europe Returnable Circular Packaging Market Trends - Policy-Driven Leadership and Cross-Border Reuse Networks

Europe is projected to lead the global returnable circular packaging market with an approximate 34.5% share, reflecting a deep integration of circular economy policies, structured deposit and reuse systems, and broad cross-industry collaboration on sustainable logistics models. Countries such as Germany, France, and the Nordic countries stand out for their high adoption of reusable crates, pallets, and industrial containers across automotive, food, and consumer goods supply chains, while the U.K. has become a focal point for retail reuse pilots and closed-loop initiatives. Policy frameworks have shaped this leadership position. Binding waste reduction targets, deposit schemes, and harmonized labeling requirements, alongside strategic regulatory initiatives such as national circular economy plans, create predictable market conditions that reduce investment risk and support scaling of reusable systems across sectors. In practice, this has translated into the widespread deployment of integrated pallet pooling networks, cross-border reusable crate services, and standardized container formats that span multiple industries.

Many European logistics operators report that returnable systems now account for a large share of intra-factory and regional distribution packaging, notably in automotive parts, fresh produce logistics, and retail backhaul flows. Concrete examples illustrate this regional momentum: collaborative reuse and pooling platforms are expanding service footprints across national borders, enabling fleets of millions of reusable containers to circulate between manufacturers, distributors, and retailers with optimized return logistics. Investment in large refurbishment hubs and digital pooling platforms enhances tracking and automation of return flows, while pilot projects benchmark reuse performance in real retail settings, helping brands refine economic models and operational standards. These developments reduce supply chain waste, strengthen regulatory compliance, and incentivize further capital deployment into reuse-focused assets and services.

Asia Pacific Returnable Circular Packaging Market Trends - Rapid Industrial Growth Driving High-Volume Reuse Adoption

Asia Pacific is the fastest-growing regional market for returnable circular packaging, fueled by rapid industrialization, booming e-commerce logistics, dense urbanization, and rising consumer and corporate sustainability awareness. The economies of China, Japan, India, and ASEAN dominate regional growth, each contributing distinct dynamics that reflect their local supply chain structures and policy backdrops. In China, large-scale manufacturing and cross-border export flows underpin heavy use of reusable pallets and crates. Hundreds of millions of returnable packaging units are now deployed across industrial and FMCG logistics networks, including automated warehousing and e-commerce distribution centers, which help reduce damage and improve handling efficiency. China’s freight and retail sectors are increasingly integrating reusable models into high-frequency supply chains to lower waste and support circularity objectives.

Japan emphasizes technology-driven reuse systems, supported by national strategies such as the Plastic Resource Circulation Strategy, which aims to significantly scale reuse and recycling by mid-decade. Industries ranging from automotive assembly to consumer goods packaging are adopting standardized reusable containers, and major Japanese corporations are exploring bio-based and hybrid materials for next-generation reusable packaging formats. This regulatory and innovation ecosystem is accelerating implementation in both urban logistics and industrial production lines. India and ASEAN markets are leveraging rapid growth in organized retail and rising e-commerce penetration to extend returnable packaging beyond industrial settings into fast-moving consumer goods and food distribution. Reverse logistics capabilities are expanding through partnerships with local pooling operators, and pilot programs are demonstrating measurable waste reduction and cost savings, particularly in fast turnaround markets where transportation density supports frequent reuse cycles. Although regulatory frameworks across the Asia Pacific are less uniform than in Europe, government waste reduction policies, municipal recycling targets, and corporate ESG commitments are collectively increasing investment in pooling hubs, local repair centers, and tracking systems that enhance returnability and asset utilization.

Competitive Landscape

The global returnable circular packaging market is moderately concentrated at the global pooling and large-asset services level, where a small number of providers manage extensive pallet, crate, and container fleets. In contrast, repair, cleaning, and niche-format segments remain fragmented, with numerous regional specialists. Competitive positioning is defined by network density, service reliability, digital asset management capabilities, and the ability to support standardized, interoperable systems across industries.

Recent strategic activity includes capacity expansions for industrial container production and refurbishment, scaling of reuse pilots by global consumer goods companies, and upgrades to digital tracking and pooling networks across North America and Europe. These developments reflect a shift toward service-led business models and higher asset utilization.

Leading companies emphasize network expansion, digital tracking, vertical integration of cleaning and repair services, and product-as-a-service offerings. Differentiation increasingly depends on interoperability, certification capabilities, and data-driven performance management.

Key Industry Developments

- In April 2025, Brambles announced a strategic partnership with Tetra Pak to co-develop and pilot scalable closed-loop reusable packaging systems in global cold-chain networks, advancing reuse solutions for temperature-sensitive supply chains.

Companies Covered in Returnable Circular Packaging Market

- Brambles/CHEP

- IFCO Systems

- Schoeller Allibert

- ORBIS Corporation

- Schütz GmbH

- Greif

- Loscam

- Mauser/Mauser Packaging Solutions

- Rehrig Pacific

- Owens-Illinois (O-I Glass)

- Paccor Group

- Plastic Logic

- ALPLA Group

- K.Hartwall

- RPC Group

- Cabka Group

- SSI Schaefer

- IPL Group

Frequently Asked Questions

The global returnable circular packaging market size is likely to be valued at US$113.2 billion in 2026.

The returnable circular packaging market is expected to reach US$174.8 billion by 2033.

Key trends include increasing regulatory pressure to reduce single-use packaging, and growing adoption of reusable crates, pallets, and industrial containers in food & beverage, chemicals, and pharmaceuticals.

By material, rigid plastics (HDPE/PP) lead with an anticipated 47.6% share.

The returnable circular packaging market is projected to grow at a CAGR of 6.4% from 2026 to 2033.

Major companies include Brambles/CHEP, IFCO Systems, Schoeller Allibert, ORBIS Corporation, and Schütz GmbH.